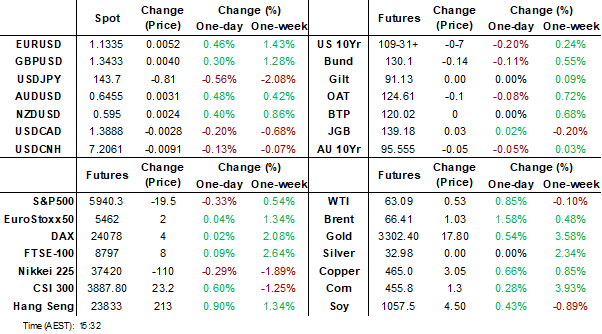

MNI EUROPEAN MARKETS ANALYSIS: USD Continues To Falter

- Oil prices spiked early on CNN headlines that Israel was planning to strike Iran nuclear facilities (per US Intelligence). US equity futures are weaker, although regional Asia Pac equities are showing better trends. US yields have continued to extend higher. JGB's have also seen a steeper curve, with yields flat to 7bps higher.

- The USD is down against all of the majors and Asian FX, with safe havens CHF and JPY outperforming.

- Later the Fed’s Barkin and Bowman and ECB’s Lane appear. The ECB’s May Financial Stability Review is published. UK April CPI is released and likely to show impacts from government policy changes.

MARKETS

US TSYS: Asia Wrap - Yields Extend Higher

TYM5 has traded higher within a range of 110-00 to 110-10+ during the Asia-Pacific session. It last changed hands at 110-0, down 0-06 from the previous close.

- The US 2-year yield has edged higher, dealing around 3.977%, up 0.01 from its close.

- The US 10-year yield has extended higher, dealing around 4.507%, up 0.02 from its close.

- “Donald Trump is losing patience with demands to raise a draft SALT cap past $30,000, a person familiar said. But some House Republicans still plan to oppose the bill unless their changes are made.”(BBG)

- “There is a clear narrative building on Wednesday in Asia as long-end bond futures extend losses, which is helping to undermine US equity contracts. While it isn’t yet a full repeat of the “Sell America” theme, there is broad weakness developing for the greenback.”(BBG)

- The 10-year found sellers again back towards 4.40% overnight. Asia is having another look back above 4.50% in our session, a sustained break above 4.55/60% needed to see another round of selling targeting the 4.75% area. Support seen back towards 4.35/40%, dips back towards here should see supply emerge once more.

- Data/Events : MBA Mortgage applications, Richmond Fed President Tom Barkin , Fed Governor Michelle Bowman to participate in a “Fed Listens” event

IRAN: CNN Reports Of Israeli Plans To Attack Iran May Be To Force A Nuclear Deal

CNN is reporting that US intelligence has found that Israel is considering an attack on Iran’s nuclear infrastructure but a final decision is yet to be made and it may just reflect pressure on Iran to reach a nuclear deal with the US. The news has driven WTI up 2.5% to $63.59 at the start of today’s trading. The leak suggests that the US administration may want to pressure Iran while talks on a nuclear agreement are ongoing.

- Israel relies on US support and an attack on Iran without an agreement from the US would strain the relationship. CNN says that “there is deep disagreement within the US government” about the possibility of an Israeli strike.

- The likelihood of an attack looks to depend on what Israel thinks of US-Iran nuclear talks, as it won’t be happy if Iran retains any ability to refine Uranium.

- According to CNN, the US has seen Israeli movement of “air munitions and the completion of an air exercise”.

- Oil markets continue to be sensitive to a deterioration in the already fraught situation in the Middle East. Iran would retaliate if Israel attacked especially its nuclear facilities.

- The US has also threatened Iran with military action if it doesn’t reach a nuclear deal and President Trump has said that US negotiations are finite with a 60-day deadline. It has been 38 days since they began.

- Meanwhile, Iranian President Pezeshkian said it won’t give up its non-military nuclear programme and Ayatollah Ali Khamenei voiced his doubts that the talks with the US will result in an agreement.

JGBS: Bear-Steepener Extends, 30YY Hits 3.20%, BOJ Noguchi Talks Tomorrow

JGB futures are weaker, -8 compared to the settlement levels, after dealing in a relatively narrow range in today’s Tokyo session.

- (Financial Times) -- 'Yields on the longest-dated Japanese government bonds surged to record highs on Tuesday after a dismal debt auction added to investor fears of a lack of demand."

- (Reuters) - "BOJ urged to boost bond buying in wake of spike in super-long yields " http://reut.rs/3S9aspw

- Cash US tsys have extended yesterday's bear-steepener, with yields 1-3bps higher, in today's Asia-Pac session.

- Cash JGBs have bear-steepened across benchmarks, with yields flat to 7bps higher. The benchmark 20-year yield is 3.5bps higher at 2.571% after yesterday's poor auction.

- The JGB 30-year yield had extended higher earlier to print 3.204% up 0.09 on the day. This is starting to look pretty ugly. At what level do the Japanese Lifers sell US assets and repatriate funds to buy this? This has implications for both US stocks and bonds.

- Swap rates are 1bp lower to 9bps higher, with a steeper curve.

- Tomorrow, the local calendar will see Jibun Bank PMIs (P), Core Machine Orders and International Investment Flow data alongside a speech from BOJ Board Noguchi in Miyazaki.

AUSSIE BONDS: Cheaper, 70bps Of Easing Priced By YE, RBA Hauser Speech Tomorrow

ACGBs (YM -2.0 & XM -5.0) are weaker and near Sydney session lows on a data-light session.

- (AFR) “Reserve Bank of Australia governor Michele Bullock says the prospect of another leg-up in property values will not deter her from lowering interest rates, as economists argue housing has become so expensive that any future price upswing will be modest.” (See link)

- Cash US tsys have extended yesterday's bear-steepener, with yields flat to 2bps higher, in today's Asia-Pac session.

- Cash ACGBs are 1-5bps cheaper with the AU-US 10-year yield differential -6bps.

- The bills strip is mixed with late whites outperforming, with pricing -3 to +2.

- RBA-dated OIS pricing is flat to slightly softer across meetings today as the market continues to digest yesterday’s dovish tilt from the RBA. RBA-dated OIS pricing is now 8-20bps softer than yesterday’s pre-RBA levels.

- A 25bp rate cut in July is given a 68% probability, with a cumulative 70bps of easing priced by year-end.

- Tomorrow, the local calendar will see S&P Global PMIs (P) and a speech from RBA Hauser.

- The AOFM plans to sell A$800mn of the 2.75% 21 November 2028 bond on Friday.

BONDS: Modest Bear-Steepener, Budget Tomorrow

NZGBs closed near cheaps, showing a modest bear-steepener, with benchmark yields 1-3bps higher.

- Swap rates closed 2-3bps lower, with implied swap spreads tighter.

- The RBNZ has released its first official business expectations survey for Q2 2025 after trialling it over H2 2024. It found that inflation expectations rose across time horizons from 1-year to 10-years. Data released last week also showed an increase for Q2.

- The RBNZ decision is to be announced on May 28 and it is likely to cut rates 25bp but rising inflation expectations may make its tone more cautious.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for May, with a cumulative 64bps by November 2025.

- Tomorrow, the local calendar will see the Budget.

- “New Zealan’d budget update is likely to project a slower near-term fiscal consolidation path as a weaker economy weighs on revenues. The half-year economic and fiscal update projected GDP growth of 0.5% in fiscal 2024-25. We forecast the economy is on track to contract 0.8%. The Reserve Bank of New Zealand projects a 0.9% contraction.” (per BBG)

- On Friday, the NZ Treasury plans to sell NZ$250mn of the 3.00% Apr-29 bond, NZ$150mn of the 3.50% Apr-33 bond and NZ$50mn of the 1.75% May-41 bond.

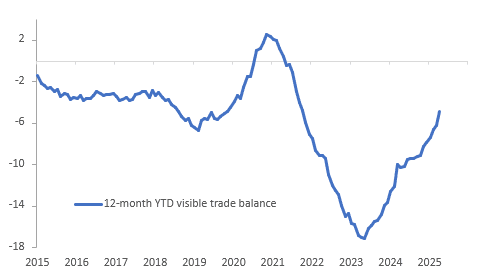

NEW ZEALAND: Strong Primary Exports Boost Trade Surplus

NZ posted its third consecutive monthly merchandise trade surplus in April at $1426.04mn up from $794.43 to drive a further narrowing in the YTD deficit to $4812mn from $6250mn, the lowest since October 2021. The improvement has been the result of export growth outpacing imports with shipments to China, the US and Europe particularly strong.

NZ merchandise trade balance NZ$bn YTD

- Goods exports rose 4.2% m/m & 24.0% y/y in April up from 16.2% y/y. Statistics NZ notes that the dairy and fruit seasons coincided and so the pickup in exports and thus the record high trade surplus were driven by primary producers.

- The value of shipments of dairy products rose 38% y/y, meat 34% y/y helped by higher prices, and fruit +29% y/y.

- Like other countries, NZ appears to be attempting to beat US tariff deadlines with exports rising 25.5% y/y driven by meat, dairy & fruit. NZ is set to face the minimum duty of 10%. Exports to China increased 29.9% y/y (dairy & timber), +31.4% y/y to Europe, +12.2% y/y to Japan and 4.9% y/y to Australia.

- Imports fell 0.9% m/m to be up only 1.2% y/y as domestic demand remains weak and lower oil prices reduced the value of petroleum cargoes. Plant & equipment contracted 7.4% y/y while transport jumped 36.8% y/y. Consumer goods rose 2.6% y/y.

NZ goods exports vs imports y/y% 3-mth ma

Source: MNI - Market News/LSEG

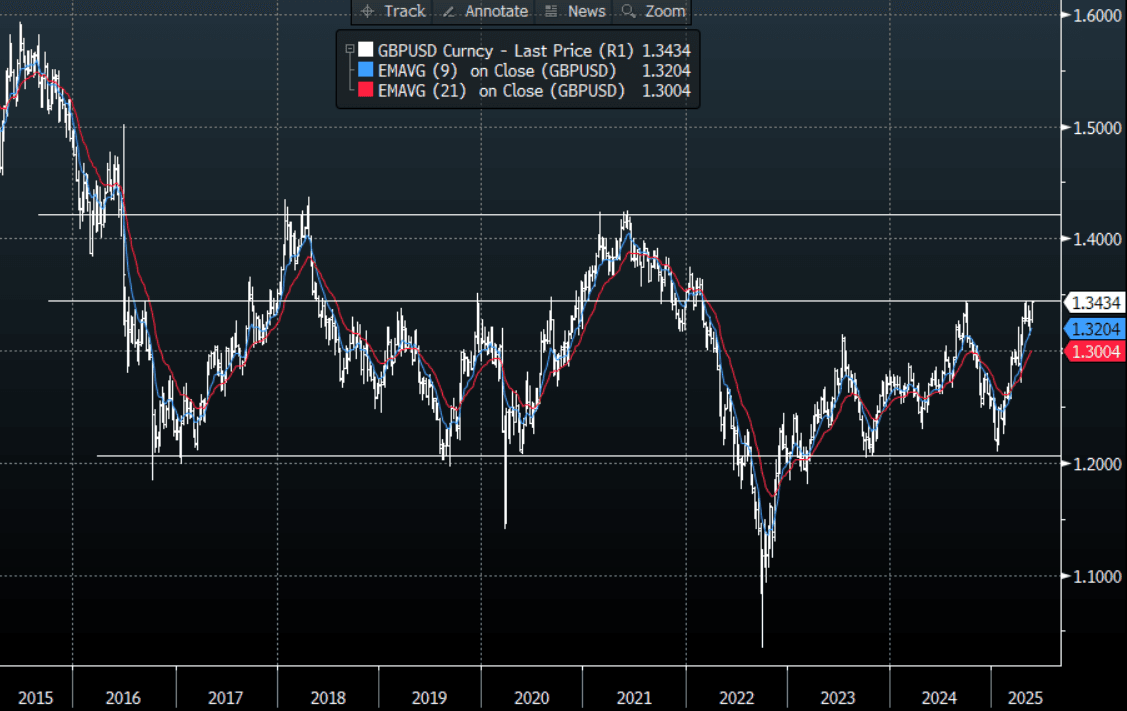

FOREX: FX Wrap - USD Breaking Down

The BBDXY has had a range of 1217.80 - 1222.27 in the Asia-Pac session, it is currently trading around 1218. Ministry of Finance data shows the Chinese government deficit tipped CNY2.6tn in the year to April. This deficit is one of the largest on record and represented a 50% increase year on year. “The BOE may relax post-crisis rules that forced banks to separate retail and investment arms. HSBC, NatWest and Lloyds asked Chancellor Rachel Reeves last month to abolish ring-fencing, saying it made the British banking industry less competitive.”(BBG)

- EUR/USD - Asian range 1.1281 - 1.1340, Asia is currently trading 1.1230.The market is still expected to use dips as a buying opportunity and dips back towards 1.10 should see buyers remerge. Can it find upward momentum again ?

- GBP/USD - Asian range 1.3381 - 1.3435, Asia is currently dealing around 1.3430. Decent demand for GBP all through the Asian session has seen it break above 1.3400. The GBP is back to testing Pivotal Weekly Resistance in the 1.3500 area.

- USD/CNH - Asian range 7.2040 - 7.2198, the USD/CNY fix printed 7.1937. Asia is currently dealing around 7.2050. Sellers should be found on a bounce back towards the 7.2400 area again.

- Cross asset : SPX -0.38%, Gold $3305, US 10-Year 4.50%, BBDXY 1218, Crude oil $63.14

Data/Events : MBA Mortgage applications, Richmond Fed President Tom Barkin , Fed Governor Michelle Bowman to participate in a “Fed Listens” event.

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg

JPY: Asia Wrap - USD/JPY Breaking Support

The Asia-Pac range has been 143.73 - 144.61, Asia is currently trading around 143.75. USD/JPY has been under pressure from the open and remained so all through our session as the USD took another leg lower across the board.

- (Financial Times) -- ‘Yields on the longest-dated Japanese government bonds surged to record highs on Tuesday after a dismal debt auction added to investor fears of a lack of demand.”

- Reuters - “BOJ urged to boost bond buying in wake of spike in super-long yields “reut.rs/3S9aspw

- The JGB 30-Year yield extended higher again to print 3.201% up 0.09 on the day. This is starting to look pretty ugly, at what level do the Japanese Lifers sell US assets and repatriate funds to buy this? This has implications for both US stocks and bonds.

- USD/JPY is breaking through its support and the price action is interesting considering the bounce we have had in stocks recently.

- The price action shows the market is still more comfortable selling rallies. If we close down at these levels on the day focus will turn once more to the pivotal 140.00 area.

Options : Closest significant option expiries for NY cut, based on DTCC data: 145.50($1.03b May 20), 145.00($789.7m May 20) , Upcoming Strikes : 145.00($2b May 23),144.00($1.37b May 23), 140.00(1.67b May 23)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

AUD: Asia wrap - Pushes Higher In Asia

The AUD/USD has had a range of 0.6417 - 0.6452 in the Asia- Pac session, it is currently trading around 0.6445. The USD has come under pressure straight from the opening this morning and has remained heavy across the board all through our session. If you want to express a short in the AUD the crosses look a better way to do it.

- Bloomberg - “Australia’s hefty A$1.2b sale of December 2035 debt went off with decent demand metrics. That underscores that the concerns swirling around Japanese and US government bonds at the longer end don’t really resonate for the South Pacific economy given its cleaner fiscal fundamentals.”

- MNI - Expectations of sustained strong pricing at auctions proved accurate, with the latest round of ACGB Dec-35 supply seeing the weighted average yield print 0.55bp through prevailing mids (per Yieldbroker).

- The AUD/USD has seen a decent bounce today, price action against the USD is pretty impressive considering what was thrown at it yesterday. First target looks to be the highs just above 0.6500, a sustained break above here would signal the potential for a larger move higher.

- Expect buyers to be around on dips while the support in the AUD holds, a close back below 0.6300/50 is needed to negate the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6380(AUD300m), Upcoming Strikes : 0.6375(AUD483.6m May 23), 0.6550(AUD480.3m May 23)

AUD/JPY - Today's range 92.56 - 92.90, it is trading currently around 92.65. Decent demand seen towards the 92.50 area where it holds again in our session. A sustained close back below 91.50/92.00 is needed to turn the focus back towards the lows again.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg

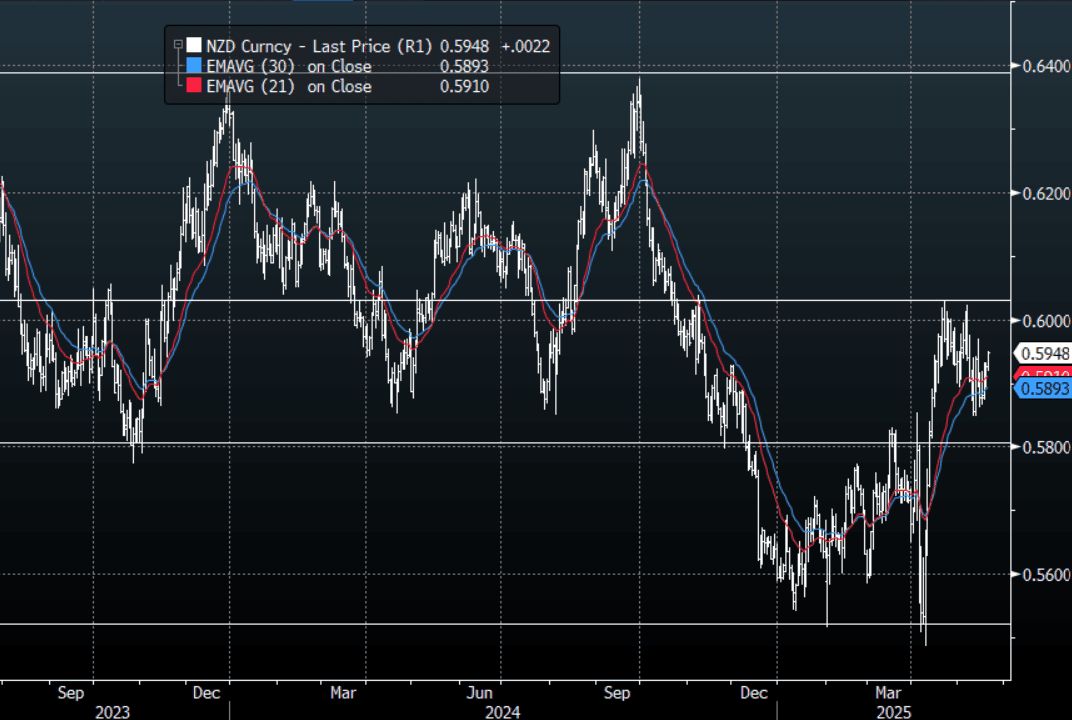

NZD: Asia Wrap - A Weak USD Helps The Kiwi Get Wings

The NZD/USD had a range of 0.5919 - 0.5950 in the Asia-Pac session, going into the London open trading around 0.5945. The USD has come under pressure straight from the opening this morning and has remained heavy across the board all through our session the NZD has benefited from this.

- MNI - RBNZ: " Business expectations for annual CPI inflation increased across all time horizons. Mean one-year-ahead annual inflation expectations increased from 2.25% to 2.44%. Mean two-year-ahead inflation expectations increased from 2.47% to 2.54%. Mean five-year-ahead and ten-year-ahead inflation expectations increased to 3.06% and 3.94%, respectively. "

- MNI China Press - "The Shanghai Port U.S. West Line for mid-June shipment has reached USD9,100 per 40-foot container, a sharp increase from the USD2,250 offered in early May, Yicai news outlet reported, citing industry insiders.”

- The NZD/USD has been bid all of our session as the USD extended its sell-off after the NZD found some decent demand sub 0.5900 overnight

- The NZD now seems to be comfortable in a 0.5800/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break above here could signal a bigger move higher is about to unfold.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5875(NZD349.6m), Upcoming Strikes : 0.5705(NZD805.1m May 23), 0.6150(NZD356.1m May 23), 0.5980(NZD513.4m May26)

AUD/NZD range for the session has been 1.0833 - 1.0851, currently trading 1.0840. The Cross has found some supply just above 1.0900, support is seen back towards 1.0800. A sustained break above 1.0920 is needed to turn the focus higher, until then expect supply on bounces.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: KOSPI and TAIEX Lead

The broader sentiment for Asia's major bourses today was positive with the best performers the KOSPI and the TAIEX. Both market have enjoyed a turnaround in fortune in recent weeks as strong inflows have been enjoyed. Taiwan for example as experienced over $7bn of inflows in May alone and the Korea $750m.

- China's major bourses were all positive today with the CSI 300 leading the way, up +0.68%, the Hang Seng up +0.53%, Shanghai up +0.38% and Shenzhen up a mere +0.09%.

- The KOSPI had a very strong day rising +1.06% to take returns into positive for the week.

- The TAIEX is up +1.03% today yet after strong falls on Monday remains behind for the week.

- The FTSE Bursa Malaysia KLCI is having a weak period at present and is down for a fifth day in a row, by -0.28%.

- The Jakarta Composite's strong period continues up +0.67%, ahead of the Central Bank decision today.

- In Singapore, the FTSE Straits Times fell -0.35% and the PSEi in the Philippines was flat.

- India's NIFTY 50 has had a strong start to the trading day rising +0.53% after three days of losses.

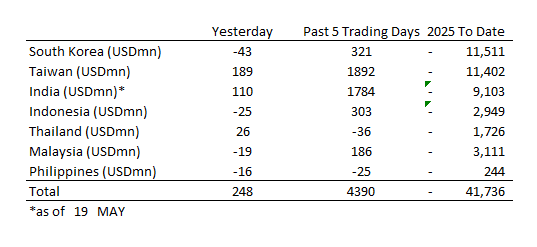

ASIA STOCKS: Strong Flows Continue for Taiwan and India

The ongoing resurgence of inflows into Taiwan and India continues to dominate flows across major markets.

- South Korea: Recorded outflows of -$43m yesterday, bringing the 5-day total to +$321m. 2025 to date flows are -$11,511. The 5-day average is +$64m, the 20-day average is +$44m and the 100-day average of -$120m.

- Taiwan: Had inflows of +$189m yesterday, with total inflows of +$1,892m over the past 5 days. YTD flows are negativ4e at -$11,402. The 5-day average is +$378m, the 20-day average of +$432m and the 100-day average of -$123m.

- India: Had inflows of +$110m as of the 19th, with total inflows of +$1,784m over the past 5 days. YTD flows are negative -$9,103m. The 5-day average is +$357m, the 20-day average of +$319m and the 100-day average of -$109m.

- Indonesia: Had outflows of -$25m as of yesterday, with total inflows of +$303m over the prior five days. YTD flows are negative -$2,949m. The 5-day average is +$61m, the 20-day average $0m and the 100-day average -$33m

- Thailand: Recorded inflows of +$26m as of yesterday, outflows totaling -$36m over the past 5 days. YTD flows are negative at -$1,726m. The 5-day average is -$7m, the 20-day average of -$17m the 100-day average of -$18m.

- Malaysia: Recorded outflows of -$19m as of yesterday, totaling +$186m over the past 5 days. YTD flows are negative at -$3,111m. The 5-day average is +$18m, the 20-day average of +$40m and the 100-day average of -$22m.

- Philippines: Saw outflows of -$16m as of yesterday, with net outflows of -$25m over the past 5 days. YTD flows are negative at -$244m. The 5-day average is -$5m, the 20-day average of +$2m the 100-day average of -$3m.

OIL: Geopolitical Concerns Driving Prices Again

Oil prices are higher today following a CNN report that US intelligence believes that Israel is considering an attack on Iran’s nuclear infrastructure but it is yet to make a decision which is likely to depend on the outcome of US-Iran talks. WTI is up 1.7% to $63.07, holding above resistance at $62.90, after spiking to $64.19 early in the APAC session. Brent is also 1.7% higher at $66.48 but made its intraday high of $66.63 more recently, above the 50-day EMA. The weaker greenback is also providing support (BBDXY USD index -0.4%).

- CNN says that “there is deep disagreement within the US government” about the possibility of an Israeli strike on Iran. The US has seen Israeli movement of “air munitions and the completion of an air exercise”. Oil continues to be sensitive to a deterioration in the already fraught situation in the Middle East. Iran would retaliate if Israel attacked.

- Markets had been monitoring progress of US-Iran talks, which are scheduled to continue on the weekend in Rome, to see if sanctions are likely to be eased allowing it to increase its crude exports. A possible threat from Israel is likely to make discussions even more difficult.

- The EU imposed new sanctions on Russia targeting financial intermediaries and its shadow oil tankers following what it deemed an unsuccessful call between Trump and Putin this week. Trump believes more sanctions will only push Russia away from negotiations.

- Bloomberg reported that another 2.5mn barrels were added in the US, according to people familiar with the API data. However, gasoline stocks fell 3.24mn and distillate 1.4mn suggesting still robust demand. The official EIA data is out later today.

- Later the Fed’s Barkin and Bowman and ECB’s Lane appear. The ECB’s May Financial Stability Review is published. UK April CPI is released and likely to show impacts from government policy changes.

GOLD: Bullion Finds Support From Middle East Concerns

After falling almost 2% on Tuesday, gold prices are moderately higher during today’s APAC session on concerns over a deterioration in the situation in the Middle East following CNN reports that Israel is considering a strike on Iran’s nuclear infrastructure. Bullion has range traded though reaching a high of $3314.69 followed by a low of $3285.50 and is now 0.4% higher at $3304.50/oz to be little changed in May.

- Technicals continue to be consistent with a corrective bear cycle, but today gold held above initial resistance at $3256.6, 20-day EMA, opening up $3347.5, 9 May high. Moody’s downgrade of US sovereign debt has encouraged flight-to-quality buying this week. Initial support is at $3121.0, 15 May low.

- Apparently Israel is yet to decide on whether to attack Iran and the likelihood looks to depend on what it thinks of US-Iran nuclear talks, as it won’t be happy if Iran retains any ability to refine uranium, according to CNN.

- Equities are generally stronger with the Hang Seng up 0.5% and KOSPI +1.0% but S&P e-mini down 0.4%. Silver is off its intraday low of $32.93 but is currently little changed on the day at $33.08. Oil is higher with WTI up 1.9% to $63.21. Copper is +0.7% and iron ore just under $100/t. The USD index is down 0.4%.

- Later the Fed’s Barkin and Bowman and ECB’s Lane appear. The ECB’s May Financial Stability Review is published. UK April CPI is released and likely to show impacts from government policy changes.

CHINA: January April Deficit Record

- Ministry of Finance data shows the Chinese government deficit tipped CNY2.6tn in the year to April.

- This deficit is one of the largest on record and represented a 50% increase year on year.

- The government is looking to cushion the economy as it is buffeted by the impacts of the trade war.

- Total expenditure rose 7.2 per cent to CNY12 trillion yuan, the data showed.

- In signs the economy may be stabilizing, tax revenue rose 1.9% from a year earlier after a 2.2% decline in March.

- Signs that the wave of government bond issuance are impacting the fiscal position were evident as interest payments rose 11%.

- With signs that the US China relationship is thawing and this release could represent the low point in the deficit as signs that economic activity is stabilizing.

SOUTH KOREA: Early Exports Fall a Sign of Tariff Threat

- South Korea's early May trade data released today showed that exports are falling, particularly to the US.

- Early month exports declined -2.4% (there were no working day effects) year on year.

- This is a bigger decline than the -5.2% decline for the first 20 days in April.

- Imports declined by -2.8% year on year (from -11.8% the month prior)

- Shipments to China declined by over 7%

- Shipments to the US declined by over 14%.

- A delegation from South Korea’s trade ministry will visit the US over May 20-22 to hold follow-up discussions in efforts to reach a compromise before US President Donald Trump’s tariffs on Korea's exports resume in in July.

ASIA FX: NEA FX Firmer, Led By The Won, USD/HKD Remains Elevated

North East Asia FX is firmer versus the USD, albeit mainly concentrated in terms of won gains. CNH and TWD have seen more modest rises against the USD. Recent ranges also continue to hold in terms of all three pairs. USD/HKD has edged higher, but remains sub 7.8300 at this stage.

- USD/CNH saw some support emerge after headlines cross from China's MOFCOM, stating that the US is abusing export controls in the chip sector and that China will protect its interest in the space. It remains to be seen if this dents progress around broader US-China trade negotiations. From highs near 7.2200, USD/CNH turned lower though, amid broad USD losses. We were last near 7.2050. Local equities are up, the CSI 300 +0.70%.

- Spot USD/KRW is under 1390 and looking to consolidate the recent downtrend. Focus will be on earlier May lows just under 1382. We were last near 1386, up around 0.55% in won terms so far today. Local equities are up +1%, adding to the generally positive risk mood (outside of weaker US equity futures). Earlier data showed exports down modestly in y/y terms for the first 20-days of May, showing the tariff impact, with exports to the US falling sharply.

- USD/TWD spot is a touch lower, but holds above 30.10 at this stage. Reports from yesterday, per Reuters, suggested exporters were asked to curb USD sales to reduce TWD appreciation pressures. This may point to near term sensitivity around a fresh break back sub the 30.00 level.

- Spot USD/HKD is tracking just short of recent highs, last near 7.8285. Continued focus on depressed forward points and short term yield differentials in favor of the USD, leaves an upside bias in the pair.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 21/05/2025 | 0600/0700 | *** | Consumer inflation report | |

| 21/05/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 21/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 21/05/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 21/05/2025 | 1600/1800 | ECB's Lane at Monpol Panel Discussion | ||

| 21/05/2025 | 1615/1215 | Richmond Fed's Tom Barkin, Fed Gov. Michelle Bowman | ||

| 21/05/2025 | 1620/1220 | Fed Governor Michelle Bowman | ||

| 21/05/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 22/05/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 22/05/2025 | 2350/0850 | * | Machinery orders | |

| 22/05/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 22/05/2025 | 0600/0700 | *** | Public Sector Finances | |

| 22/05/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 22/05/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 22/05/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 22/05/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 22/05/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 22/05/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 22/05/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 22/05/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 22/05/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 22/05/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 22/05/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 22/05/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 22/05/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 22/05/2025 | 1050/1150 | BOE's Breeden On Climate Panel | ||

| 22/05/2025 | 1100/1200 | BOE's Dhingra On UK Productivity Panel | ||

| 22/05/2025 | 1130/1330 | ECB April Minutes Released | ||

| 22/05/2025 | 1200/0800 | Richmond Fed's Tom Barkin | ||

| 22/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 22/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 22/05/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/05/2025 | 1230/1330 | BOE's Pill At MonPol Conference (Text 16:30BST) | ||

| 22/05/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 22/05/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 22/05/2025 | 1345/0945 | *** | S&P Global Services Index (flash) |