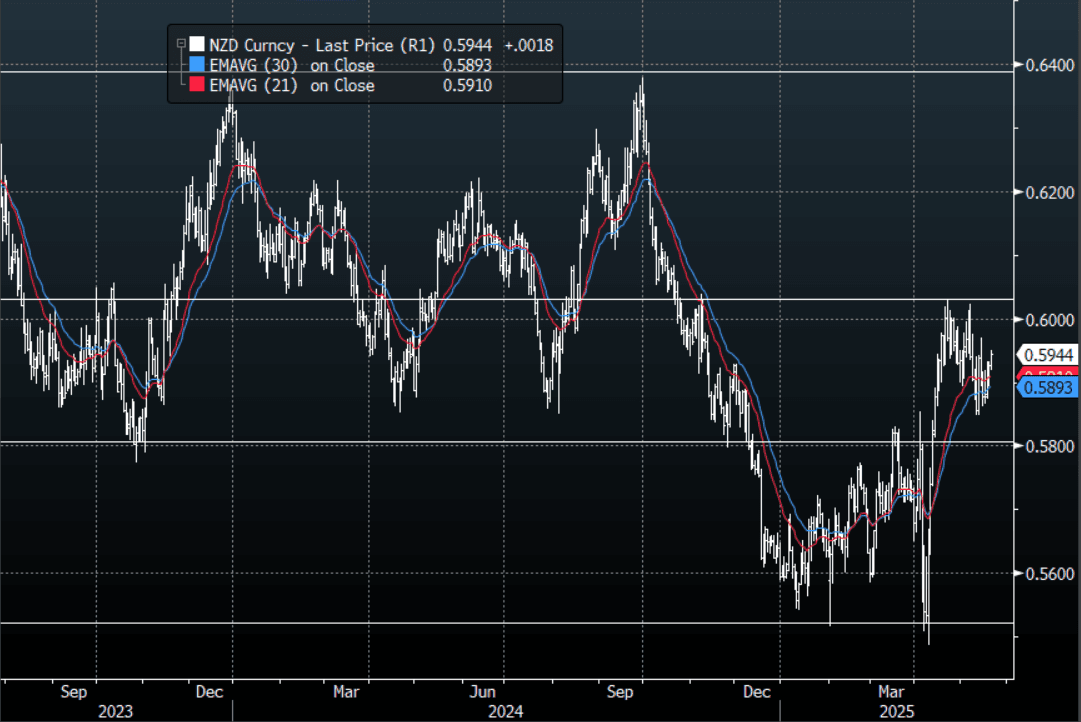

NZD: Asia Wrap - A Weak USD Helps The Kiwi Get Wings

The NZD/USD had a range of 0.5919 - 0.5950 in the Asia-Pac session, going into the London open trading around 0.5945. The USD has come under pressure straight from the opening this morning and has remained heavy across the board all through our session the NZD has benefited from this.

- MNI - RBNZ: " Business expectations for annual CPI inflation increased across all time horizons. Mean one-year-ahead annual inflation expectations increased from 2.25% to 2.44%. Mean two-year-ahead inflation expectations increased from 2.47% to 2.54%. Mean five-year-ahead and ten-year-ahead inflation expectations increased to 3.06% and 3.94%, respectively. "

- MNI China Press - "The Shanghai Port U.S. West Line for mid-June shipment has reached USD9,100 per 40-foot container, a sharp increase from the USD2,250 offered in early May, Yicai news outlet reported, citing industry insiders.”

- The NZD/USD has been bid all of our session as the USD extended its sell-off after the NZD found some decent demand sub 0.5900 overnight

- The NZD now seems to be comfortable in a 0.5800/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break above here could signal a bigger move higher is about to unfold.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5875(NZD349.6m), Upcoming Strikes : 0.5705(NZD805.1m May 23), 0.6150(NZD356.1m May 23), 0.5980(NZD513.4m May26)

AUD/NZD range for the session has been 1.0833 - 1.0851, currently trading 1.0840. The Cross has found some supply just above 1.0900, support is seen back towards 1.0800. A sustained break above 1.0920 is needed to turn the focus higher, until then expect supply on bounces.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Crude Down As US Worries Impact Markets

After rising close to 5% last week, oil prices are lower today driven by a pullback in risk following pressure from US President Trump on the Fed to cut rates and worries regarding the impact of increased protectionism on energy demand. April trade and confidence data will be monitored closely for signs of any early impact. Crude remains well above initial support levels though. The USD is significantly weaker (BBDXY USD index -0.7%) as markets fear political interference in US monetary policy.

- WTI is down 1.5% to $63.69/bbl during holiday-impacted APAC trading today. It reached a low of $63.38 earlier and is now around 10% softer this month with the bearish theme remaining intact. Last week’s rally helped the oversold condition to unwind. Initial support is at $55.12 with resistance $64.49.

- Brent has sold off 1.6% to $66.87/bbl following a low of $66.61. Last week’s 4.8% rise is considered corrective with the trend direction down. Initial support is at $62.00 with resistance at $67.95.

- Talks appear to be progressing between the US and Iran on its nuclear programme, which if successful could result in increased oil exports. Iranian comments continue to support its right to enrich uranium though and the lack of an agreement may result in tighter sanctions, which if enforced would support oil prices.

- The US has suggested that a lasting ceasefire in the Ukraine would allow an easing of sanctions on Russia, which would also add to global oil supplies, but it seems that the Easter truce has not been respected.

- Later the Fed’s Goolsbee appears and the US March leading index is released. Europe remains closed.

FOREX: Risk Averse Currencies Around A Percent Stronger Vs US Dollar

Market concerns of political interference in US monetary policy and continued tariff uncertainty have weighed heavily on the US dollar during APAC trading today. The BBDXY USD index is down 0.7% to 1216.10, close to the intraday low, with all G10 currencies stronger against the greenback but especially risk-averse yen, Swiss franc and euro. Risk-sensitive AUD and CAD are underperforming.

- USDJPY is down 1.0% to 140.73, close to the intraday low of 140.62 and below support at 141.00 after breaching 141.62 on Friday, which opens 140.32, 17 September 2024 low.

- EURUSD is just off its high of 1.1529 but is still +1.0% to 1.1512, breaking above resistance at 1.1473 and 1.1495 opening up 1.1555.

- The Swiss franc is 1.0% stronger against the greenback with the pair at 0.8085, its lowest since 2011. EURCHF is little changed at 0.9308.

- GBPUSD is up 0.6% to 1.3377 thus EURGBP 0.4% higher at 0.8606 off the peak of 0.8619.

- AUDUSD has breached resistance at 0.6392 opening 0.6409. The pair is currently up 0.4% to 0.6404, close to the intraday high. However, Aussie is weaker against other major currencies with AUDJPY -0.6% to 90.13 after briefly falling below 90.00 to a low of 89.97. AUDEUR is down 0.6% to 0.5564 after a trough of 0.5555. AUDNZD is -0.4% to 1.0696, still above Friday’s low of 1.0684.

- Equities are mixed with both the S&P & Nasdaq e-minis down 0.9% and TAIEX -1.4% but the CSI 300 is up 0.2% and Straits Times +1.2%. Oil prices are down with WTI -1.8% to $63.53/bbl. Copper is down 0.7% but iron ore is higher at around $99/t.

- Later the Fed’s Goolsbee appears and the US March leading index is released. Japan’s March Tokyo condominium sales print today. Europe remains closed.

ASIA STOCKS: Outflows Continue to Challenge Asian Bourses

The ongoing theme of outflows dominate Asia markets again as any inflows are short lived.

- South Korea: Recorded outflows of -$88m as of 18th, bringing the 5-day total to -$1,001m. 2025 to date flows are -$12,479, m. The 5-day average is -$200m, the 20-day average is -$431m and the 100-day average of -$156m.

- Taiwan: Had outflows of -$552m as of 18th, with total outflows of -$2,292m over the past 5 days. YTD flows are negative at -$20,009. The 5-day average is -$458m, the 20-day average of -$240m and the 100-day average of -$233m.

- India: Had inflows of +$470m as of the 17th, with total outflows of -$72m over the past 5 days. YTD flows are negative -$15,486m. The 5-day average is -$14m, the 20-day average of +$17m and the 100-day average of -$142m.

- Indonesia: Had outflows of -$487m as of 17th, with total outflows of -$1,273m over the prior five days. YTD flows are negative -$3,440m. The 5-day average is -$255m, the 20-day average -$100m and the 100-day average -$47m

- Thailand: Recorded outflows of -$40m as of the 18th, outflows totaling -$33m over the past 5 days. YTD flows are negative at -$1,422m. The 5-day average is -$7m, the 20-day average of -$25m the 100-day average of -$19m.

- Malaysia: Recorded inflows of +$9m as of the 18th, totaling -$75m over the past 5 days. YTD flows are negative at -$2,853m. The 5-day average is -$15m, the 20-day average of -$50m the 100-day average of -$40m.

- Philippines: Saw inflows of +$0m as of 17th, with net inflows of +$5m over the past 5 days. YTD flows are negative at -$287m. The 5-day average is +$1m, the 20-day average of -$4m the 100-day average of -$5m.