FOREX: USD Strength Extends, NZD and GBP Continue to Underperform

Sep-25 15:33

- The firmer-than-expected US data on Thursday has kept the greenback trading with a very supportive tone throughout the US session. The dollar index (+0.58%) has been steadily grinding higher, extending to a high of 98.44 in recent trade, now 2.3% above the post-Fed cycle lows. The DXY appears to have solidly broken above the 50-day EMA, a bullish development.

- While associated declines across the G10 have been broad based, with the likes of EUR and JPY falling around half a percent, both GBP and NZD are the clear underperformers with significant technical breaks exacerbating downside momentum.

- For GBPUSD (-0.77%) specifically, we highlighted the breach of two support trendlines, drawn from both the Aug 01 and the January lows. Spot has moved sharply lower, and has significantly narrowed the gap to the first target of 1.3333, the Sep 3 low and a key support. Below here, a key medium-term level is at 1.3140.

- Both fiscal uncertainty and political tensions are rising in the UK, potentially underpinning the fundamentals behind the latest GBP pessimism. We posted earlier on Andy Burnham (current mayor of Greater Manchester) treading a fine line on offering support to the gov't while also failing to deny ambitions to unseat Sir Keir Starmer as Labour leader and PM, just days ahead of the Labour party conference.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: Midday September'25-December'25 Roll Update: 70%-80% Complete

Aug-26 15:27

Latest Tsy quarterly futures roll volumes from September'25 to December'25 below. Percentage complete currently 70%-80% ahead "First Notice" date this Friday, August 29. Current roll details:

- TUU5/TUZ5 appr 1,266,500 from -9.12 to -8.75, -9.0 last; 80% complete

- FVU5/FVZ5 appr 1,528,800 from -5.5 to -5.0, -5.25 last; 70% complete

- TYU5/TYZ5 appr 926,800 from -1.25 to -0.5, -0.75 last; 71% complete

- UXYU5/UXYZ5 app 550,300 from -0.25 to +0.5, 0.00 last; 72% complete

- USU5/USZ5 appr 312,600 from 12.0 to 12.75, 12.25 last; 79% complete

- WNU5/WNZ5 appr 435,700 from 7.0 to 8.25, 7.75 last; 74% complete

- Reminder, Sep futures don't expire until next month: 10s, 30s and Ultras on September 22, 2s and 5s on September 30.

OPTIONS: Larger FX Option Pipeline

Aug-26 15:16

- EUR/USD: Aug29 $1.1600(E1.3bln), $1.1625(E4.0bln), $1.1700(E1.1bln), $1.1725(E1.1bln)

- USD/JPY: Aug29 Y146.50($1.1bln)

- EUR/GBP: Aug29 Gbp0.8563-80(E2.0bln)

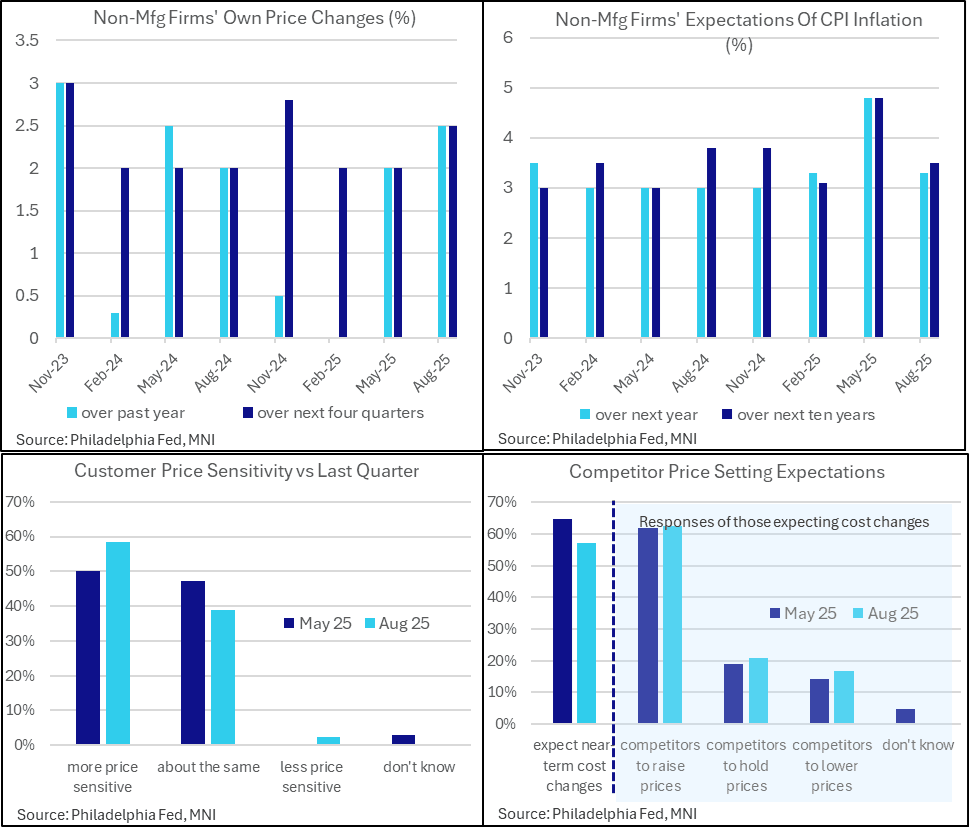

US DATA: Philly Non-Mfg Firms See Faster Price Increases Despite Sensitivity

Aug-26 15:08

- The Philly Fed non-manufacturing survey special questions on inflation expectations show a somewhat similar split in the activity indexes touched upon earlier with their historically large discrepancy between strong firms’ own activity and weak regional activity in August.

- The median firm reported increasing its own prices by 2.5% over the past year, up from 2.0% in the May question and having essentially paused annual price increases through end 2024/early 2025. It’s the strongest actual increase since the May 2024 survey.

- Own price expectations also firmed from 2.0% to 2.5%, above a typical median of 2% in surveys over the past almost two years but not an unprecedented level.

- Firms’ expectations of consumer inflation meanwhile cooled from a particularly strong May release, with those for the next year reverting to 3.3% from 4.8%. Ten-year ahead expectations also cooled to 3.5% after 4.8%, still above the 3.1% in February prior to reciprocal tariff announcements but within ranges.

- Elsewhere, these non-manufacturing firms reported greater price sensitivity over the quarter (59% reported higher sensitivity vs 50% in May) and fewer expect cost changes over the near-term (57% vs 65%). Of those that do expect cost increases, a similar almost two thirds expect those to be higher, with price changes over a median 3 months vs 2.5 months in the May survey.