MNI EUROPEAN MARKETS ANALYSIS: US Tsy 10yr Sub 4%, NFP Later

- Risk off continued to dominate market sentiment and moves today. US equity futures weakened further, as did all the major regional Asia Pac bourses. US yields fell with the 10yr under 4.0%.

- The USD was higher against AUD and NZD, but safe havens and EUR outperformed. AUD/JPY fell to fresh YTD lows. President Yoon's impeachment was upheld in South Korea.

- Key US data tonight will be the NFP, along with Fed Chair Powell speak. For NFP the market may look through a better than expected outcome, but a downside surprise might drive further risk off.

MARKETS

US TSYS: Rally Extends As Risk-Off Remains

TYM5 is 113-08+, +0-20 from closing levels in today's Asia-Pac session.

- According to MNI's technicals team, today's move puts TYM5 above the key technical resistance at 113-05 (1.764 proj of the Jan 13 - Feb 7 - Feb 12 price swing).

- Cash US tsys 5-7bps richer in today's Asia-Pac session after finishing Thursday's NY session broadly richer, with yields 3-18bps lower.

- Attention now turns to today's US payrolls data and a speech by Fed Chair Powell.

- Nonfarm payrolls are seen increasing a seasonally adjusted 140k in March in the Bloomberg survey after 151k in February. The unemployment rate is seen holding at 4.1% after a surprise increase in Feb, although at 4.14% it can very easily round higher as some analysts are expecting. Its recent high was 4.23% in Nov whilst the median FOMC participant raised the 4Q25 forecast a tenth higher to 4.4% in last month's SEP.

- See MNI US Payrolls Preview here.

CROSS ASSET: HY Credit Spreads - Pointing To More Pain

Credit spreads have continued to explode higher as extreme risk aversion takes hold.

- Credit spreads have behaved pretty well for most of the year, but are now starting to accelerate higher.

- The break of the pivotal 400 area could see this move really gather pace as people attempt to exit the HY space in search of better liquidity and safe havens.

- This break does not bode well for stocks, every time we have seen an acceleration through this pivotal area it has coincided with a period of extreme volatility and lower stocks.

- This move could add further fuel to an already nervous market, with scope for a further move lower in yields and a weaker USD, particularly against safe havens.

Fig 1: HY Spreads - Past 400 Area

Source: MNI - Market News/Bloomberg

STIR: $-Bloc Markets Soften Sharply Following Trump Tariff Details

Rate expectations across the $-bloc have softened sharply through December 2025 following President Trump’s announcement of reciprocal tariffs late Wednesday.

- Since last Friday, markets have repriced significantly: US rate expectations have eased by 40bps, Australia by 37bps, New Zealand by 30bps, and Canada by 19bps.

- On Tuesday, the RBA left the cash rate unchanged at 4.10%. In its accompanying statement, the central bank acknowledged a significant decline in inflation since 2022 in line with forecasts but maintained a cautious tone amid ongoing uncertainty around growth, inflation, and global trade. The RBA reiterated its priority of returning inflation to target sustainably and signalled it will adjust policy as required.

- Looking ahead, the next key policy decisions in the $-bloc are the RBNZ on 9 April and the BoC on 16 April. Markets are currently more than fully pricing a 27bp cut from the RBNZ, while assigning only a 35% probability to a cut from the BoC.

- Looking ahead to December 2025, the projected official rates and cumulative easing across the $-bloc are as follows: US (FOMC): 3.31%, -103bps; Canada (BOC): 2.12%, -63bps; Australia (RBA): 3.08%, -102bps; and New Zealand (RBNZ): 2.75%, -100bps.

JGBS: Massive Rally Led By The Belly, 10YY Falls 40bps This Week

JGB futures are sharply stronger, +177 compared to settlement levels, aligning with US tsys.

- BoJ Governor Ueda said, “US tariffs have added uncertainty to the economic outlook and will weigh on growth, in comments that indicate the central bank may need more time to assess the impact of Donald Trump’s policies before lifting its benchmark rate.” (per BBG)

- “Bank of Japan Deputy Governor Shinichi Uchida said on Friday the central bank will keep raising interest rates if the chance of underlying inflation achieving its 2% target heightens. "We will examine at each policy meeting, without any preconception, whether our (economic and price) forecasts would be achieved" in deciding monetary policy, Uchida told parliament. “ (per RTRS)

- Cash US tsys 5-7bps richer in today's Asia-Pac session after finishing yesterday's NY session 3-18bps richer, with the curve steeper. Attention now turns to today's US payrolls data and a speech by Fed Chair Powell.

- Cash JGBs are 7-20bps richer across benchmarks, with the belly of the curve outperforming. The benchmark 10-year yield is 19.5bps lower at 1.176% versus the cycle high of 1.596%, set last week.

- Swap rates are 13-18bps lower. Swap spreads are mixed.

- On Monday, the local calendar will see Labor & Real Cash Earnings and Coincident & Leading Indices data.

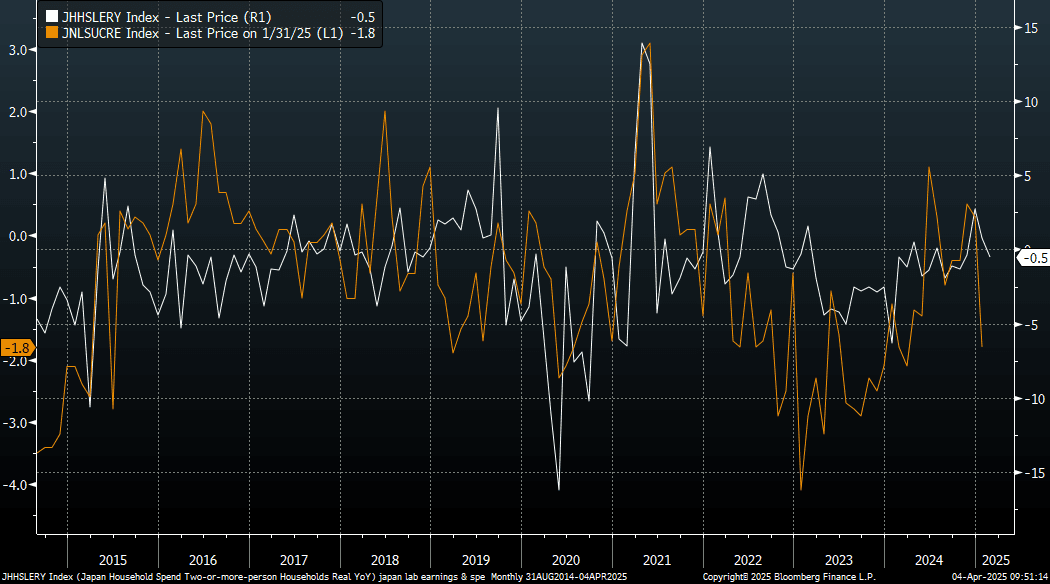

JAPAN DATA: Real Household Spending Negative Y/Y, Incomes Weaker As Well

Japan real household spending printed slightly better than market forecasts but was still in negative territory. We printed -0.5%y/y for Feb, versus -0.8% forecast and +0.8% prior. This is the first negative print since Nov last year. Base effects likely played a role as spending from Jan to Feb in 2024 went from -6.3% to -0.5% in y/y terms.

- The chart below plots this real spending measure against real wages growth (which is the orange line on the chart). Feb's decline in real spending is also in line with the softer real wages backdrop.

- This remains a key point for the government and the BOJ in terms of driving positive real wage growth and in turn consumer spending. Real household incomes were at -2.3%y/y in Feb, continuing a recent downtrend.

- Spending in m/m terms was still strong though up 3.5%, the strongest rise since 2021. It follows a -4.5%m/m dip in Jan, but was mostly positive through the tail end of 2024.

- From a BoJ standpoint this result may not change much in terms of near term thinking, with the central bank focused on external risks from US tariffs and likely in wait and see mode.

Fig 1: Japan Real Spending Dips Y/Y In Feb

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Bull-Steepener Ahead Of US Payrolls

ACGBs (YM +14.0 & XM +5.5) are holding sharply richer, with the curve steeper.

- Cash US tsys 5-7bps richer in today's Asia-Pac session after finishing yesterday's NY session broadly richer, with yields 3-18bps lower. Attention now turns to today's US payrolls data and a speech by Fed Chair Powell. Nonfarm payrolls are seen increasing a seasonally adjusted 140k in March in the Bloomberg survey after 151k in February. See MNI US Payrolls Preview here.

- Cash ACGBs are 3-11bps with the 3/10 curve steeper and the AU-US 10-year yield differential at +20bps.

- The bills strip has sharply bull-flattened, with pricing +8 to +16.

- Market expectations for RBA easing in 2025 have strengthened following President Trump's reciprocal tariff announcement late Wednesday. A 25bp rate cut in May is now priced at 118% probability, with a total of 103bps of easing expected by year-end (based on an effective cash rate of 4.09%).

- On Monday, the local calendar will see ANZ-Indeed Job Advertisements and Foreign Reserves data.

- Next week, the AOFM plans to sell A$400mn of the 4.25% 21 June 2034 bond on Tuesday, A$1000mn of the 2.75% 21 November 2028 bond on Wednesday and A$600mn of the 2.75% 21 June 2035 bond on Friday.

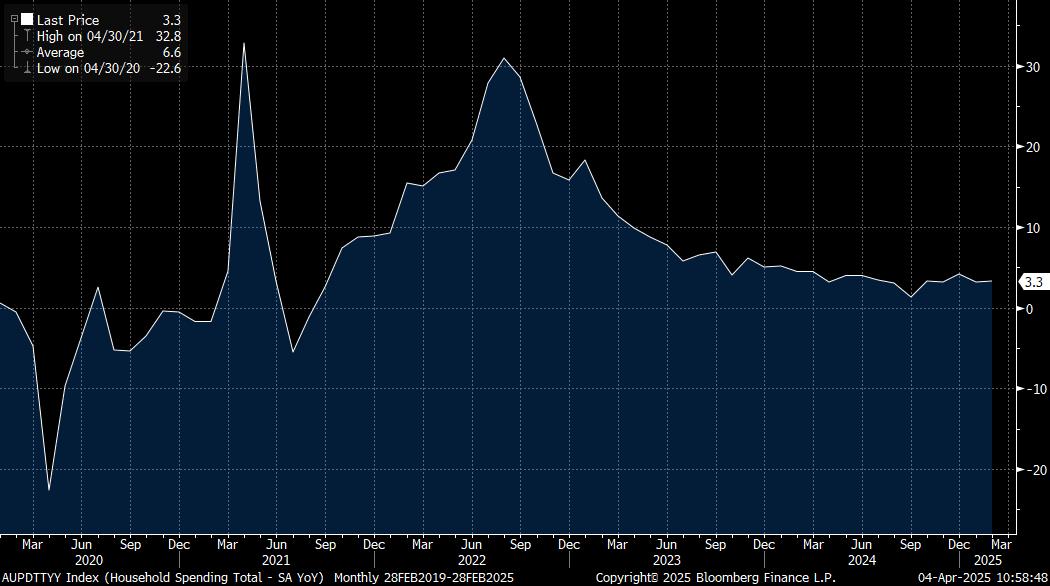

AUSTRALIA DATA: Household Spending Close To Forecast - Steady Trend Near 3%y/y

Australian Feb household spending data was close to market expectations. The m/m outcome was 0.2% (versus 0.3% forecast and a revised 0.5% gain in Jan). In y/y terms we rose 3.3%, against a 3.2% forecast and prior 3.2% outcome (originally reported as a 2.9% gain). Note this release will replace the retail sales release from June this year.

- The ABS noted: "In seasonally adjusted, current price terms, household spending increased for five of the nine spending categories. The largest increases were in: recreation and culture (+0.9%), food (+0.6%), hotels, cafes and restaurants (+0.5%)."

- It added: "In seasonally adjusted, current price terms, discretionary spending rose 0.3% month-on-month, driven by increased spending on purchase of vehicles, recreational and cultural services, and personal effects." Non-discretionary spending was down modestly.

- The chart below plots the y/y trend in household spending, which is largely sideways since early 2024, with a slightly uptick in early Q4 last year, aided by government support. This suggests a modestly positive spending backdrop. Today's data is unlikely to shift RBA thinking.

Fig 1: Australian Household Spending - Y/Y, Largely Sideways Trend

Source: MNI - Market News/Bloomberg

BONDS: NZGBS: Closed On A Strong Note As Global Bonds Extend Rally

NZGBs closed on a strong note, with benchmark yields 9-14bps lower.

- With the local calendar empty today, the market’s focus remains on the fall-out from President Trump’s announcement of reciprocal tariffs late Wednesday.

- Cash US tsys 5-7bps richer in today's Asia-Pac session after finishing yesterday's NY session broadly richer, with yields 3-18bps lower. Attention now turns to today's US payrolls data and a speech by Fed Chair Powell. Nonfarm payrolls are seen increasing a seasonally adjusted 140k in March in the Bloomberg survey after 151k in February. See MNI US Payrolls Preview here.

- NZ-US and NZ-AU 10-year yield differentials are little changed versus yesterday’s close.

- Swap rates closed 6-13bps lower, with the 2s10s curve steeper.

- Rate expectations across the $-bloc have softened sharply through December 2025. Since last Friday, markets have repriced significantly: US rate expectations have eased by 40bps, Australia by 37bps, New Zealand by 30bps, and Canada by 19bps.

- Looking ahead, the next key policy decisions in the $-bloc are the RBNZ on 9 April and the BoC on 16 April. Markets are currently more than fully pricing a 25bp cut from the RBNZ, while assigning only a 35% probability to a cut from the BoC.

FOREX: USD Index Ticks Down, AUD/JPY Falls 1.8% Amid Further Equity Risk Off

The BBDXY opened around 1250 in Asia and has drifted slightly lower going into the London session to open around 1248. We are still up from intra-session lows on Thursday (1244.84). The 10yr yield has broken the pivotal 4% and stocks remain under pressure.

- EUR/USD - Asia has had a range of 1.1037 - 1.1099, and is trading around 1.1085 going into the London open. For now though dips look likely to remain supported and buying interest is likely emerge anywhere back towards 1.1000 on the day.

- GBP/USD - very quiet day Asian session with a range of 1.3081 - 1.3110.

- AUD/USD - has traded for poorly in the Asian session, and is being sold across the board in the crosses. AUD remains a favourite as a risk proxy so expect it the headwinds to continue while stocks remain under pressure. AUD/JPY has hit fresh lows under 91.00. August 2024 lows rest at 90.15.

- USD/CNH - the Asian range has been 7.2450 - 7.2966, we are going into the London session trading heavy near the lows. This pair will continue to be managed but CNH is outperforming higher beta FX so far today. Note China and Hong Kong markets have been out today.

- USD/JPY - the Asian range has been 145.30-146.41. After bouncing back to 146.40 area into the Japanese fix, USD/JPY has drifted lower most of our session looking to open the London session around the lows at 145.40. Bounces will find eager sellers while risk remains under pressure. CHF has outperformed yen, USD/CHF back under 0.8530, fresh 6 month lows.

- Cross asset sentiment trades very poorly US equities down around 0.8%, and strong demand for treasuries breaking the 4% support area in terms of the 10yr yield. Commodities trade poorly as the market reevaluates what the events of this week mean for global growth going forward.

- Key US data tonight will be the NFP, along with Fed Chair Powell speak. For NFP the market may look through a better than expected outcome, but a downside surprise might drive further risk off.

ASIA STOCKS: Another Brutal Day for Asian Bourses

With China out today, eyes were on South Korea where the decision on President Yoon was pending. Korea's KOSPI held its breath leading into the decision but headed lower quickly after the court verdict to impeach Yoon results in an immediate removal and a presidential election within 60 days.

- The KOSPI moved lower quickly to be -1.80% on the day, capping off a challenging week in which the index has declined -4.5%.

- Malaysia's FTSE Bursa KLCI is down and in a week shortened by holidays is only down -0.50%.

- In Singapore, the FTSE Straits Times is down heavily today by -2.90%, marking its worst decline for the year and a -3.6% decline for the week.

- The Philippines reported weaker than expected CPI prompting forecasters to call for a rate cuts at the BSP's meeting next week as the PSEi declined -1.17% today, down.

- In India, the NIFTY 50 fell only modestly yesterday by -0.35% yet it opening up much weaker today to be lower by -1.23%.

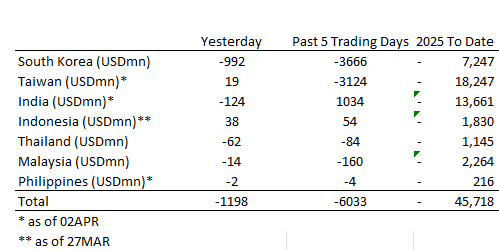

ASIA STOCKS: Korea’s Outflows Continue.

Global Investors continue to withdraw from Korea with another day of significant outflow as India’s strong run of inflows turns negative.

- South Korea: Recorded outflows of -$992m yesterday, bringing the 5-day total to -$3,666m. 2025 to date flows are -$7,247m. The 5-day average is -$733m, the 20-day average is -$157m and the 100-day average of -$120m.

- Taiwan: Had inflows of +$19m as of the 2nd, with total outflows of -$3,124m over the past 5 days. YTD flows are negative at -$18,247. The 5-day average is -$625m, the 20-day average of -$505m and the 100-day average of -$256m.

- India: Had outflows of -$124m as of 2nd, with total inflows of +$1,034m over the past 5 days. YTD flows are negative -$13,661m. The 5-day average is +$207m, the 20-day average of +$6m and the 100-day average of -$145m.

- Indonesia: Had inflows of +$38m as of the 27/3, with total inflows of +$54m over the prior five days. YTD flows are negative -$1,830m. The 5-day average is +$11m, the 20-day average -$33m and the 100-day average -$34m

- Thailand: Recorded outflows of -$62m yesterday, totaling -$84m over the past 5 days. YTD flows are negative at -$1,145m. The 5-day average is -$17m, the 20-day average of -$22m the 100-day average of -$17m.

- Malaysia: Recorded outflows of -$14m yesterday, totaling -$160m over the past 5 days. YTD flows are negative at -$2,264m. The 5-day average is -$32m, the 20-day average of -$53m the 100-day average of -$36m.

- Philippines: Saw outflows of -$2m as of 2nd, with net outflows of -$4m over the prior 5 days. YTD flows are negative at -$216m. The 5-day average is -$1m, the 20-day average of +$2m the 100-day average of -$7m.

Oil Slips Further During in Asia's Day

- Whilst the tariff announcement may have provided certainty on what was to be levied, the create uncertainty as to the outlook for the global economy; pressurizing oil prices.

- Add to this, OPEC+ decision to add 411,000 barrels of supply from May created a perfect storm for oil prices.

- Oil declined the most in two years with prices down over 6%.

- WTI had fallen -6.64% overnight to US$66.63 trading through all major moving averages.

- The falls didn’t end there with a decline -0.37% to $66.38, leaving it down almost 4% for the week.

- Brent fell -6.42% overnight $69.85 also trading through all major moving averages.

- The falls continued in Asia, sliding to $69.58 leaving it down 5% for the week

- With tariffs placed on India and China being more significant, the outlook for these two major crude importers is now uncertain and oil price movements have reflected this.

- The US Department of Energy is to announce the award of a contract in excess of $1bn for the management of the US Strategic Reserve, with an objective of restocking the depleted reserves. This could have significant implications for demand as the reserve has capacity of up to 700 million barrels and is less than half of that at present.

- Exxon Mobil says it may deliver a $2.7bn gain in quarterly profit as a result of higher prices last year.

GOLD: Even Gold Suffers With Tariffs

- Gold is ending the week with poor momentum, down -0.70% in Asia trading.

- With a new high in place at US$3,167.83 gold opened in Asia at $3,114.80 only to move lower throughout the trading day to be at $3,093.81.

- Gold has had somewhat of a more volatile week so far as profit takers emerge on new historic highs.

- Gold is holding on to a weekly gain standing at +0.30% at present, having recorded just one week of declines in 2025.

- The National Bank of Kazakhstan was a seller of gold last year as prices rose and had previously indicated that they would be a seller at USD$3,100 but for now the Deputy Governor prefers to wait given global uncertainty.

- The finalization of the tariffs from the US has brought to a halt an arbitrage in gold markets that has driven bullion demand for several months. For some time, New York prices traded at a premium to global prices, incentivizing the importation of gold into the US prior to tariffs. However, with tariffs now finalized this window has now closed.

SOUTH KOREA: Country Wrap: Yoon Impeached.

- The Constitutional Court unanimously upheld the impeachment of President Yoon Suk Yeol on Friday, removing him from office over his short-lived imposition of martial law in December. The verdict, which was read by acting court chief Moon Hyung-bae and televised live, took effect immediately, requiring the country to hold a snap presidential election to pick Yoon's successor within 60 days, which many expect to fall on June 3. (source: Yonhap)

- Fitch, an international credit rating agency, downgraded its sovereign credit rating from "A+" to "A," saying it is expected to weaken the Chinese government's finances and increase national debt. China's Ministry of Finance strongly protested, saying it could not be admitted. According to China's state-run Xinhua News Agency and Reuters on the 4th, Fitch announced in a statement the previous day that it would lower China's long-term foreign currency-denominated bond credit rating. However, the credit rating outlook was presented as "stable." (source: MAEIL)

- The KOSPI moved lower quickly to be -1.80% on the day, capping off a challenging week in which the index has declined -4.5%.

- KRW: the won strengthened post the news on Yoon and has gained +.910% today to be at 1,437.80.

- Bonds: a strong rally across the curve with the 3YR leading, down by -7bps to 2.45% and the KTB 10YR 2.72% (-3bps)

INDIA: Country Wrap: Services Continue to Strengthen in India:

- Morgan Stanley forecasters see up to 60bps hit to GDP growth from tariffs with possible downside risks as the tariffs exceeded estimates (source: BBG).

- March's PMI services showed the service sector in good shape in India, despite the growing global uncertainties. At +58.5 (from +59 in February) the release shows the strength in the sector despite the employment component falling to its lowest in a year. Prices charged fell also relative to the prior month for the lowest reading since September 2021. Following the PMI Manufacturing result from earlier in the week of +58.1, this left the PMI Composite rising to +59.5, from +58.6 in February and its best result since August last year. (source: MNI – Market News)

- The NIFTY 50 fell only modestly yesterday by -0.35% yet it opening up much weaker today to be lower by -1.23%.

- INR: a positive day for regional currencies as the heat came out of the USD. The rupee is up +.40% in early trade at 85.09.

- Bonds: India’s 10YR continues to rally , down 10bps on the week at 6.48%.

ASIA FX: USD/Asia Pairs Lower Despite Equity Weakness, Won Outperforms

Asia currencies are all on the front foot in the first part of Friday trade. Carry over USD weakness from Thursday's session is aiding sentiment, while the majors in terms of EUR, JPY and CHF are all up again against the USD. Regional equity sentiment is mostly down though. AUD and NZD are softer, both off by more than 1.0% so far today, with higher beta Asian FX plays outperforming though, most notably the won.

- Spot USD/KRW has fallen sharply since the open, the pair last under 1440, up close to 1% in won terms. We dipped under the 100-day EMA (around 1436.4) ahead of Yoon's impeachment notice. Session lows were at 1430.5. There may be some optimism that with Yoon's impeachment upheld it clears the way for greater clarity around the local political outlook and therefore provide a boost to domestic confidence. An election for a new President has to be held within 60 days.

- Spot USD/CNH is also weaker, back near 7.2530, up around 0.40% in CNH terms. A reminder onshore markets are closed today. Downside focus is likely to be at the simple 200-day MA (near 7.2200), which marked March lows.

- USD/MYR is down stronger, last near 4.4200, up 0.50% in MYR terms. USD/PHP is sub 57.00, last near 56.80/85 (up 0.45% for PHP). This is fresh lows back to Oct last year for this pair. The decline in March inflation provides an opportunity for the Central Bank (the "BSP") to cut at their meeting next week. March's YoY CPI fell to +1.8%, the first print below target since September 2024.

THAILAND: CPI in March Rises Less than Estimated.

- March’s CPI y/y rose just +0.84%, from +1.08% in February and against estimates of +1.00%.

- Core CPI came in at +0.86% y/y from +0.99% in February.

- The NSA MoM CPI turned further negative at -0.20%, from -0.02% in February.

- The Bank of Thailand cut rates at their meeting in February by 25bps, marking their third cut since October 2024.

PHILIPPINES: CPI Decline Opens Door For BSP

- The decline in March inflation provides an opportunity for the Central Bank (the “BSP”) to cut at their meeting next week.

- The BSP has an inflation target of 2.0 – 4.0 percent for 2025 – 2026 and set the same inflation target for 2027 – 2028.27

- March’s YoY CPI fell to +1.8%, the first print below target since September 2024.

- Leading into the September CPI print the BSP had cut in August, following up with cuts in October and December.

- The MoM CPI release for March was negative for a second straight month at -0.2% - the same as in September last year.

- Core consumer prices in March was +2.2% y/y with a downward trend in food prices in place according the Statistics Agency.

- The forecasts for next week are somewhat mixed with the majority of those surveyed forecasting a cut of 25bps, with one outlier at 50bps

- The BSP meetings on 10 April to decide on the Overnight Borrowing Rate and the Standing Overnight Deposit Facility Rate.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 04/04/2025 | 0545/0745 | ** | Unemployment | |

| 04/04/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 04/04/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/04/2025 | 0630/0730 | DMO announce Apr-Jun issuance operations | ||

| 04/04/2025 | 0645/0845 | * | Industrial Production | |

| 04/04/2025 | 0700/0900 | ** | Industrial Production | |

| 04/04/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/04/2025 | 0800/1000 | * | Retail Sales | |

| 04/04/2025 | 0800/1000 | ECB's De Guindos Gives Lecture In Barcelona | ||

| 04/04/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/04/2025 | 1230/0830 | *** | Employment Report | |

| 04/04/2025 | 1525/1125 | Fed Chair Jerome Powell | ||

| 04/04/2025 | 1600/1200 | Fed Governor Michael Barr | ||

| 04/04/2025 | 1645/1245 | Fed Governor Chris Waller | ||

| 04/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 04/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/04/2025 | 0915/1115 | ECB's Schnabel At Economy and Finance Workshop |