ASIA STOCKS: Korea’s Outflows Continue.

Apr-04 03:45

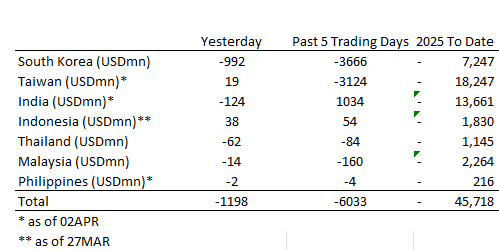

Global Investors continue to withdraw from Korea with another day of significant outflow as India’s strong run of inflows turns negative.

- South Korea: Recorded outflows of -$992m yesterday, bringing the 5-day total to -$3,666m. 2025 to date flows are -$7,247m. The 5-day average is -$733m, the 20-day average is -$157m and the 100-day average of -$120m.

- Taiwan: Had inflows of +$19m as of the 2nd, with total outflows of -$3,124m over the past 5 days. YTD flows are negative at -$18,247. The 5-day average is -$625m, the 20-day average of -$505m and the 100-day average of -$256m.

- India: Had outflows of -$124m as of 2nd, with total inflows of +$1,034m over the past 5 days. YTD flows are negative -$13,661m. The 5-day average is +$207m, the 20-day average of +$6m and the 100-day average of -$145m.

- Indonesia: Had inflows of +$38m as of the 27/3, with total inflows of +$54m over the prior five days. YTD flows are negative -$1,830m. The 5-day average is +$11m, the 20-day average -$33m and the 100-day average -$34m

- Thailand: Recorded outflows of -$62m yesterday, totaling -$84m over the past 5 days. YTD flows are negative at -$1,145m. The 5-day average is -$17m, the 20-day average of -$22m the 100-day average of -$17m.

- Malaysia: Recorded outflows of -$14m yesterday, totaling -$160m over the past 5 days. YTD flows are negative at -$2,264m. The 5-day average is -$32m, the 20-day average of -$53m the 100-day average of -$36m.

- Philippines: Saw outflows of -$2m as of 2nd, with net outflows of -$4m over the prior 5 days. YTD flows are negative at -$216m. The 5-day average is -$1m, the 20-day average of +$2m the 100-day average of -$7m.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Bear-Steepener, RBNZ Gov. Orr Resigns

Mar-05 03:42

NZGBs closed showing a bear-steepener, with benchmark yields 6-11bps higher.

- “Governor Adrian Orr unexpectedly resigned without giving a reason for his sudden departure. Orr will officially leave the bank on March 31, and Deputy Governor Christian Hawkesby will be Acting Governor until then. Finance Minister Nicola Willis will appoint a temporary governor from April 1 for a period of up to six months, following a recommendation from the RBNZ Board.” (per BBG)

- The ANZ World Commodity Price Index rose 3% month-over-month in February.

- Cash US tsys have twist-steepened, with yields 2bps lower to 2bps higher, in today’s Asia-Pac session after yesterday’s heavy session.

- Trump, in his address to Congress, praised the drop in interest rates and pledged to balance the federal budget. He urged Congress to pass tax cuts and mentioned discussions with major US car companies.

- Swap rates closed 5-9bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing is 1-6bps firmer across meetings today.

- Tomorrow, the local calendar will see CoreLogic Home Values, Volume of All Buildings data and Government 7-Month Financial Statements.

- The NZ Treasury plans to sell NZ$250mn of the 0.25% May-28 bond, NZ$200mn of the 4.25% May-36 bond and NZ$50mn of the 1.75% May-41 bond tomorrow.

CHINA: Bond Futures Not Reacting to Headlines.

Mar-05 03:34

- Ahead of the NPC headlines are emerging as to potential policy amendments to support the Chinese economy.

- Policies that potentially impact the bond market include a 5% growth target, a lower CPI target, a 4.4% rise in fiscal spending and the issuance of CNY1.3tn of ultra long term treasury bonds, up from CNY1 trn in 2023 and an increase in the 2025 quota on local government special bonds to CNY4.4tn, from CNY3.9tn.

- Surprisingly the market has not reacted to the increased supply risk and has seen bond future rally today.

- China’s 10YR bond future is up by +.10 to 108.445, from yesterday’s close of 108.345.

- Having trended away from the converging 20-day EMA of 108.53 and 50-day EMA of 108.50, today’s rally sees the 10YR approaching these levels.

- China’s 2YR future remains unchanged at 102.61, below the 200-day EMA of 102.63.

- Despite the proposed longer dated issuance to come, cash bonds have hardly moved with the CGB10YR at 1.75% and the 30YR unchanged at 1.89%

- The major economic release for today was the Caixin PMI services which was up at +51.4 and on the 7th sees the trade data for February

FOREX: USD Index Firms As Trump Talks Tariffs, AUD and NZD Wekaer

Mar-05 03:18

The USD is strengthening as Trump addresses Congress. AUD and NZD are the weakest performers. The BBDYX index has ticked up, last close to 1285.3.

- AUD/USD is back to 0.6245, off 0.45%, while NZD is down to 0.5645, off around 0.35%. USD/CNH is back above 7.2700.

- Trump has reiterated recent comments around tariffs, stating that reciprocal tariffs will come into effect from April 2. He also stated tariffs for CHina India and South Korea are high.

- Recall earlier remarks from Commerce Secretary Lutnick around potential tariff relief from tomorrow for Canada and Mexico, although Trump has elaborated on this so far in his speech. Trump stated it was time to start using tariffs but that it may cause a little disturbance.

- Other remarks have focused on tax cuts, bringing down interest rates and balancing the budget. He also stated that chipmakers aren't going to get more money from the CHIPS act (which was put in place by the Biden administration)

- In the cross asset space, US equity futures are still firmer, up around 0.60%, but off best levels. US yields are a little softer at the front end, but steady at the back end, the 10yr near 4.25% in latest dealings.

- USD/JPY is a little higher, last near 150.00. Yen is only down modestly so far today, outperforming AUD and NZD. Earlier, Bank of Japan Deputy Governor Shinichi Uchida said the BoJ will continue to raise the policy interest rate and adjust the degree of monetary accommodation, failing to offer a timeline.

Trending Top

Jan-30 21:43

Jan-30 21:11