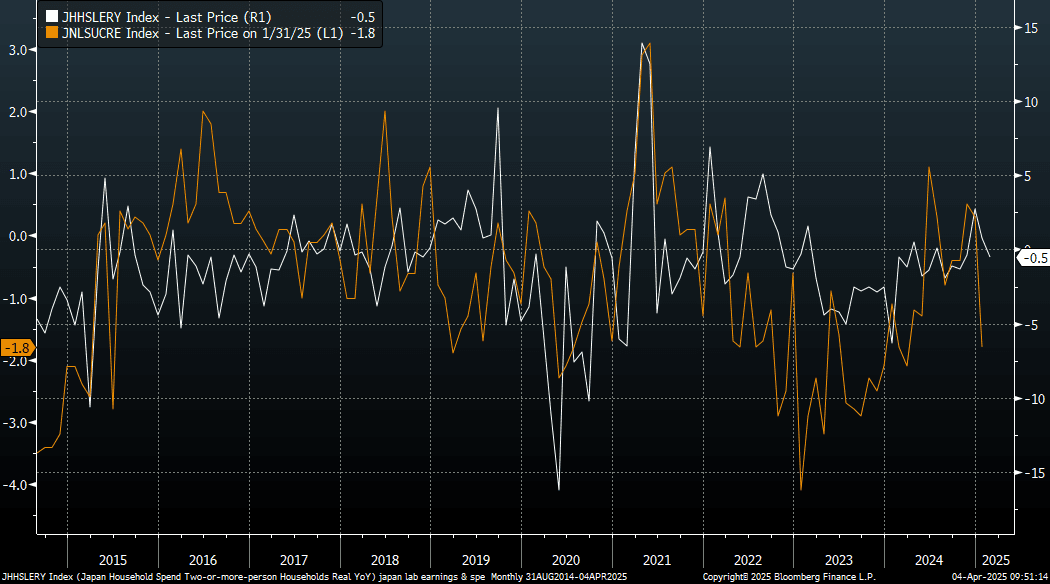

JAPAN DATA: Real Household Spending Negative Y/Y, Incomes Weaker As Well

Japan real household spending printed slightly better than market forecasts but was still in negative territory. We printed -0.5%y/y for Feb, versus -0.8% forecast and +0.8% prior. This is the first negative print since Nov last year. Base effects likely played a role as spending from Jan to Feb in 2024 went from -6.3% to -0.5% in y/y terms.

- The chart below plots this real spending measure against real wages growth (which is the orange line on the chart). Feb's decline in real spending is also in line with the softer real wages backdrop.

- This remains a key point for the government and the BOJ in terms of driving positive real wage growth and in turn consumer spending. Real household incomes were at -2.3%y/y in Feb, continuing a recent downtrend.

- Spending in m/m terms was still strong though up 3.5%, the strongest rise since 2021. It follows a -4.5%m/m dip in Jan, but was mostly positive through the tail end of 2024.

- From a BoJ standpoint this result may not change much in terms of near term thinking, with the central bank focused on external risks from US tariffs and likely in wait and see mode.

Fig 1: Japan Real Spending Dips Y/Y In Feb

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Crude Bearish Trend Reinforced, US Tariffs Create Volatility

Oil prices trended lower through the APAC and European sessions on Tuesday driven by news that OPEC is likely to stick with its plans to increase output from April. Crude then recovered during the US session despite weaker risk appetite on concerns of a supply tightening in the US but comments from US Commerce Secretary Lutnick on a tariff compromise with Canada and Mexico pushed it lower again to be down slightly on the day.

- WTI fell 0.5% on Tuesday to $68.04/bbl after a high of $68.56. It had reached a low of $66.77, below initial support at $67.75, which has reinforced the bearish trend. The next level to watch is $66.41 with key support at $65.41.

- Brent is down 0.8% at $71.04/bbl after reaching a low of $69.75 earlier, below initial support at $70.96 opening up key support at $69.59. Tuesday’s move maintains the current bear price sequence of lower lows and lower highs.

- 10% tariffs on US imports of Canadian oil have gone into effect driving higher Canadian heavy crude oil prices with the discount to WTI narrowing 15c. Bloomberg reported that a Canadian gasoline tanker diverted from New York to Amsterdam because of the tariffs.

- The US administration gave Chevron until April 3 to close its Venezuelan production which are worth around 20% of the country’s output and could remove as much as 200kbd from the global market if a deal doesn’t reverse the decision, according to Bloomberg.

- Bloomberg reported that US oil inventories fell 1.455mn barrels last week after 640k the week before, according to people familiar with the API data. Gasoline was down 1.25mm, while distillate rose 1.1mn and distillate. The official EIA data is released later today.

JGB TECHS: (H5) Sharp Bounce Off Lows

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 142.73/144.48 - High Dec 9 / High Nov 11

- PRICE: 139.57 @ 16:18 GMT Mar 4

- SUP 1: 138.71 - Low Feb 19

- SUP 2: 138.62 - 2.0% Lower Bollinger Band

- SUP 3: 138.00 - 1.0% 10-dma envelope

JGBs extended the recent bounce Friday, firming further off recent lows as global equity markets underperformed. The show through 139.99 resistance shows the move could have legs - opening early December highs should the pace be maintained. 144.48 is the medium-term target for bulls.

AUSSIE BONDS: ACGB Mar-36 Supply Faces Lower Yield & Flatter Curve Than Opening

The Australian Office of Financial Management (AOFM) will today sell A$800mn of the 4.25% 21 March 2036 bond. This new line was sold by syndication on 5 February 2025 for A$15.0bn. Bidding at today’s auction is likely to be shaped by several key factors:

- The outright yield is roughly 5bps lower than the February 5 syndication and about 15bps below the late February peak.

- The 3/10 yield curve is around 5bps flatter than at the time of the syndication but sits near its steepest level since August 2022.

- Sentiment toward longer-dated global bonds has improved over recent weeks, as reflected in the US 10-year Treasury yield, which is currently 55bps below its recent highs.

- Notably, this bond is not included in the XM futures basket, which may limit demand.

- Overall, firm pricing is still anticipated at today’s auction, given the higher yields and other favourable factors.

- Results are due at 0000 GMT / 1100AEST.