MNI EUROPEAN MARKETS ANALYSIS: US-Japan Trade Talks In Focus

- Japan national CPI showed continued firm core price pressures. Japan PM Ishiba and US President Trump also spoke via phone ahead of further trade talks between the two countries. JGB futures are stronger and at Tokyo session highs, +22 compared to settlement levels.

- Broader USD sentiment remains under pressure, while US Tsys have had a quiet start to Friday trading.

- Looking ahead we have UK retail sales, along with French consumer confidence. In the US, new home sales are out, along with the Kansas City Fed Services Activity print.

MARKETS

US TSYS: Asia Wrap - Quiet session

TYM5 has traded higher within a range of 109-29 to 110-02+ during the Asia-Pacific session. It last changed hands at 109-30+, up 0-04 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.98%, down 0.01 from its close.

- The US 10-year yield is dealing around 4.5270%, unchanged from its close.

- Bloomberg - “Donald Trump’s tax bill faces changes and delays in the Senate after narrowly passing the House. Majority Leader John Thune said senators have questions about tax permanence and are engaged in a “very active discussion” over Medicaid.”

- Bloomberg - “Finance ministers and central bank governors from the G7 nations pledged to address “excessive imbalances" in the global economy, aiming to create a level playing field and increase transparency. The communique called for an analysis of market concentration and international supply chain resilience, and recognised the potential risks of international low-value shipments, often from Chinese retailers.”

- The 10-year found buyers eventually above 4.60% as shorts are pared back into the US long weekend, this demand helped yields back off in the US session. Support seen back towards 4.45/50%, dips look likely to see supply in the short-term. Should yields hold this break higher we will then target the 4.75% area.

- Data/Events : New Home Sales, Kansas City Fed Services Activity

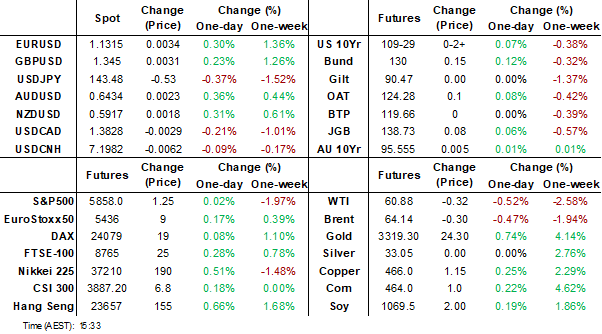

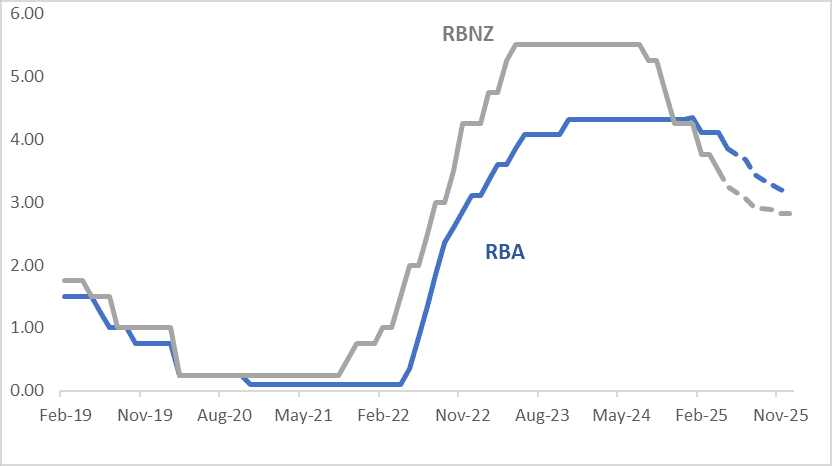

STIR: $-Bloc Markets Little Changed Over Past Week, Except For AUS

Interest rate expectations across dollar-bloc economies were little changed through December 2025 over the past week — except Australia. Australia saw the most significant shift, with a 17bp softening in expected year-end rate. The US rate rose 6bps, with New Zealand and Canada little changed.

- In Australia, the RBA cut rates 25bp to 3.85%, the lowest in two years, as was widely expected. It was a consensus decision following a discussion of unchanged rates versus a cut and then, when the latter was chosen quickly the dialogue became between 25bp or 50bp of easing. 25bp was the strongest argument.

- A 25bp rate cut in July is given a 68% probability, with a cumulative 70bps of easing priced by year-end. The progress on trade deals and any further delays are likely to impact the RBA’s July 8 decision.

- Across the $-bloc more broadly, markets appear content to consolidate recent hawkish repricing, which has largely stemmed from a reduction in downside risks, particularly surrounding trade policy, as headlines around potential deals gained traction.

- The next key event for the region is the RBNZ’s May 28 policy meeting, where a 25bp rate cut is currently fully priced in.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.81%, -52bps; Canada (BOC): 2.40%, -36bps; Australia (RBA): 3.13%, -72bps; and New Zealand (RBNZ): 2.83%, -67bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

JGBS: Bull-Flattener Partially Reverses Some Of This Week's Carnage

JGB futures are stronger and at Tokyo session highs, +22 compared to settlement levels.

- Outside of the previously outlined National CPI, there haven't been many by way of domestic drivers to flag.

- “US President Donald Trump initiated a phone call with Japanese Prime Minister Shigeru Ishiba to discuss tariffs in general terms. The two leaders discussed various topics, including tariff negotiations, economic security cooperation, and national security.” (per BBG)

- " Workers at companies affiliated with the Japan Business Federation won pay hikes exceeding 5% for a second consecutive year, which will help to keep a floor under domestic inflation"(BBG)

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's rally. A light US calendar tonight with New Home Sales and Kansas City Fed Services Activity data due. The US markets will be closed for Memorial Day on Monday.

- Cash JGBs have bull-flattened, with yields 1-6bps lower. The benchmark 30-year yield is 4.5bps lower (2bps lower in the last 10mins) at 3.135% versus the high of 3.204% set this week.

- Swap rates are little changed out to the 7-year range but 1-3bps lower beyond. Swap spreads are mixed.

- On Monday, the local calendar will see Coincident/Leading Index data alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

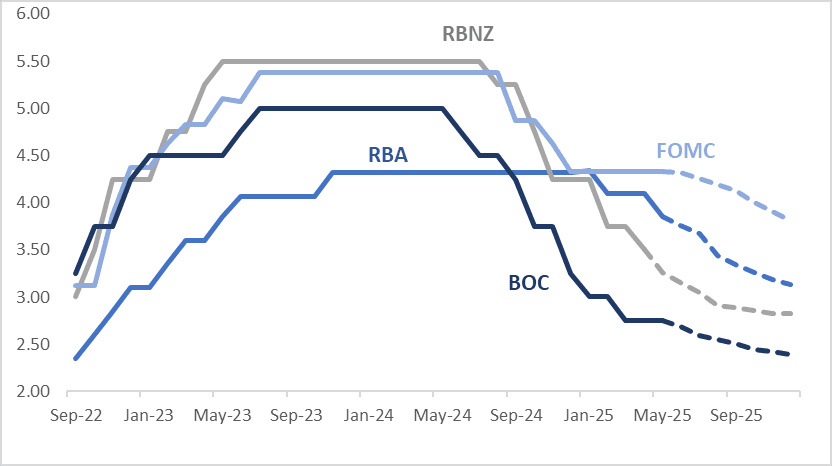

JAPAN DATA: April National CPI Still Shows Firm Underlying Price Pressures

Japan April national CPI was close to market forecasts and continued to show elevated y/y inflation momentum. The headline printed at 3.6%y/y, versus 3.5% forecast (3.6% was the March outcome). Ex fresh food rose 3.5%y/y, also a touch above forecasts (3.4%, while the prior print was 3.2%). Ex fresh food and energy was 3.0%y/y, in line with forecasts (2.9%y/y was the March outcome).

- The chart below plots the y/y trends for these various inflation indicators. The measure which excludes fresh food and energy (the dark blue line) continues to show a steady upside trend. At face value the print will add marginally to BoJ confidence around achieving its inflation target.

- In m/m terms, headline rose 0.1%, while the core measures maintained positive m/m gains. Goods prices rose 0.4%, while services were down 0.1%.

- Food prices were lower, with fresh food off5.8%m/m. Education also fell sharply, down -5.7% in the month. Utilities rose 3.0%, while entertainment, up 1.4%, along with household goods (+1.4%) and clothing (+1.3%) were other positives.

- In y/y terms, education at -5.6%, is the only negative sub category. Utilities is the highest at 8.4%. Headlines crossed earlier that the government is mulling measure to cut utility bills (FNN via BBG).

- This may help headline inflation pressures, but underlying pressures still remain firm at this stage. Note next Friday we get May Tokyo CPI.

Fig 1: Japan National CPI Trends Y/Y

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Modestly Mixed, Subdued Session, US Holiday Mon, CPI On Wed

ACGBs (YM -1.0 & XM +1.5) are slightly mixed on a light local-data day.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's rally. US markets will be closed for Memorial Day on Monday.

- Cash ACGBs are 1bp cheaper to 1bp richer with a flatter 3/10 curve.

- The AU-US 10-year yield differential is -8bps, positioned in the bottom half of the +/- 30bps range that has largely held since November 2022.

- The bills strip is -1 to -3 across contracts.

- RBA-dated OIS pricing is little changed across meetings today but 8-17bps softer than Tuesday's pre-RBA levels. A 25bp rate cut in July is given a 64% probability, with a cumulative 67bps of easing priced by year-end.

- As a result, the expected year-end policy rate differential between Australia and New Zealand has narrowed by approximately 16bps over the past week, currently sitting at +30bps.

- The local calendar will be empty on Monday and Tuesday ahead of April's CPI on Wednesday.

- Next week, the AOFM plans to sell A$400mn of the 4.25% 21 June 2034 bond on Tuesday and A$1200mn of the 4.25% 21 March 2036 bond on Friday.

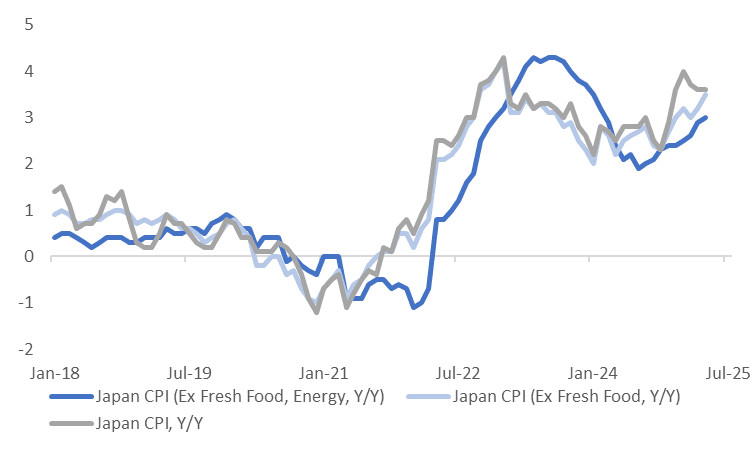

AUSSIE BONDS: AU-US 10Y Diff Sits In Bottom Half Of Range

The AU-US 10-year cash yield differential currently stands at -10bps, positioned in the bottom half of the +/- 30bps range that has largely held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is close to fair value, estimated at -14bps.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently near the bottom of the range at ~-25bps.

- In early February, the 1Y3M differential had declined approximately 95bps since mid-September 2024, falling from +60bps to -35bps.

Figure 1: AU-US Cash 10-Year Yield Differential Vs 1Y3M (%)

Source: MNI – Market News / Bloomberg

STIR: Expected YE AU-NZ Official Rate Diff Narrowed Substantially This Week

RBNZ-dated OIS pricing has seen little change across meetings compared to this time last week, with rates remaining 2–18bps above levels observed prior to the Q1 CPI release on April 17.

- By contrast, RBA-dated OIS pricing was 4–40bps higher than pre-CPI levels (April 30) as of last week.

- However, following Tuesday’s RBA easing and dovish tilt, RBA OIS pricing has retraced and is now only 8–25bps above pre-CPI levels.

- As a result, the expected year-end policy rate differential between Australia and New Zealand has narrowed by approximately 16bps over the past week, currently sitting at +30bps.

Figure 1: RBA & RBNZ Official Rate Profile (%)

Source: MNI - Market News / Bloomberg

BONDS: NZGBS: Modest Twist-Flattening To Finish The Week, RBNZ Decision On Wed

NZGBs closed off bests, showing at twist-flattening, with benchmark yields 1bp higher to 2bps lower.

- Today’s supply saw solid demand across the lines with cover ratios ranging from 2.92x (Apr-29) to 3.33x (Apr-33).

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's rally. A light US calendar tonight with New Home Sales and Kansas City Fed Services Activity data due. The US markets will be closed for Memorial Day on Monday.

- Swap rates closed little changed.

- The local calendar will be empty for Monday and Tuesday next week ahead of the RBNZ Policy Decision on Wednesday. 25bps of easing is fully priced next week meeting.

- RBNZ-dated OIS pricing has seen little change across meetings compared to this time last week, with rates remaining 2–18bps above levels observed prior to the Q1 CPI release on April 17.

- However, following Tuesday’s RBA easing and dovish tilt, RBA OIS pricing has softened 8-17bps versus pre-RBA levels.

- As a result, the expected year-end policy rate differential between Australia and New Zealand has narrowed by approximately 16bps over the past week, currently sitting at +30bps.

NEW ZEALAND: Q1 Retail Volumes Up More Than Forecast, Y/Y Pace Edges Higher

New Zealand Q1 retail sales volumes rose 0.8%q/q, versus a flat market forecast. The Q4 rise was also nudged a little higher to +1.0% (against an originally reported 0.9% gain). Today's print is a positive in the sense that other retail/consumer spend indicators have suggested a more adverse backdrop. In y/y terms spending was up 0.65%, a modest improvement on the 0.32% outcome seen in Q4 last year. This suggests further modest improvement in underlying spending momentum (we were at -4.04%y/y back in Q4 2023). The RBNZ meets next week and is expected cut the policy rate by 25bps.

NZ stats noted: "The biggest contributors to the rise in retail activity in the March 2025 quarter were:

- motor vehicles and parts retailing – up 3.1 percent

- pharmaceutical and other store-based retailing – up 3.7 percent

- clothing, footwear, and accessories – up 3.2 percent

- accommodation – up 2.9 percent."

Adding: "Ten of the 15 retail industries had higher retail sales volumes in the March 2025 quarter, compared with the December 2024 quarter, after adjusting for price and seasonal effects."

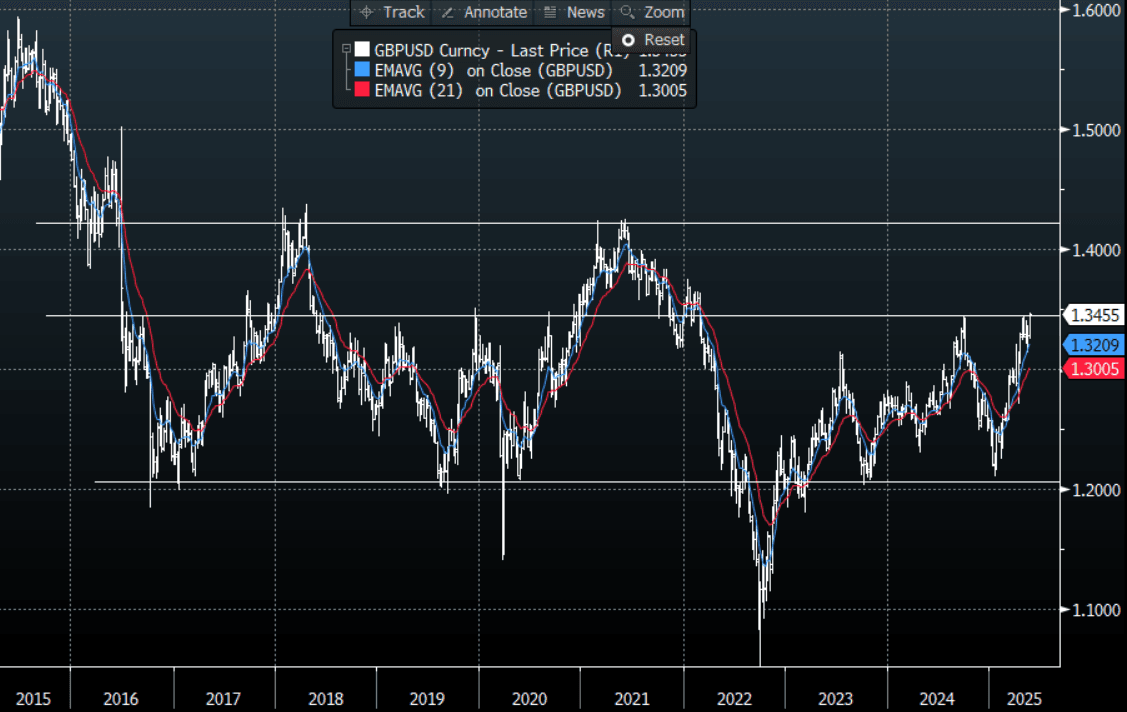

FOREX: Asia FX Wrap - Fresh USD Selling In Asia

The BBDXY has had a range of 1217.67 - 1221.00 in the Asia-Pac session, it is currently trading around 1217. “The PBOC’s net injections of liquidity via one-year medium-lending facility for a third month in May suggests a policy focus to stabilize growth, according to a report by Shanghai Securities News" - BBG. “The White House’s chief economist rejected the notion that a secret currency accord to weaken the dollar is in the works, and instead touted the benefits of a strong greenback.” - BBG

- EUR/USD - Asian range 1.1279 - 1.1319, Asia is currently trading 1.1310. A quiet Asian session with EUR drifting higher. The market is still expected to use dips as a buying opportunity where dips back towards 1.10 should see buyers remerge.

- GBP/USD - Asian range 1.3412 - 1.3451, Asia is currently dealing around 1.3450. A quiet Asian session with GBP drifting higher. The GBP is back to testing Pivotal Weekly Resistance in the 1.3500 area, expect it to do some work here. A sustained break signals a potential acceleration of the trend higher.

- USD/CNH - Asian range 7.1967 - 7.2058, the USD/CNY fix printed 7.1919. Asia is currently dealing around 7.1985. Sellers should continue to be found on a bounce back towards the 7.2400 area again.

- Cross asset : SPX +0.01%, Gold $3315, US 10-Year 4.53%, BBDXY 1217, Crude oil $60.86

Data/Events : Ger GDP, Fra Consumer Confidence, Fed Governor Lisa Cook, St. Louis Fed President Alberto Musalem and Kansas City Fed chief Jeff Schmid are scheduled to speak later Friday. Chicago Fed President Austan Goolsbee will also be interviewed on CNBC.

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg

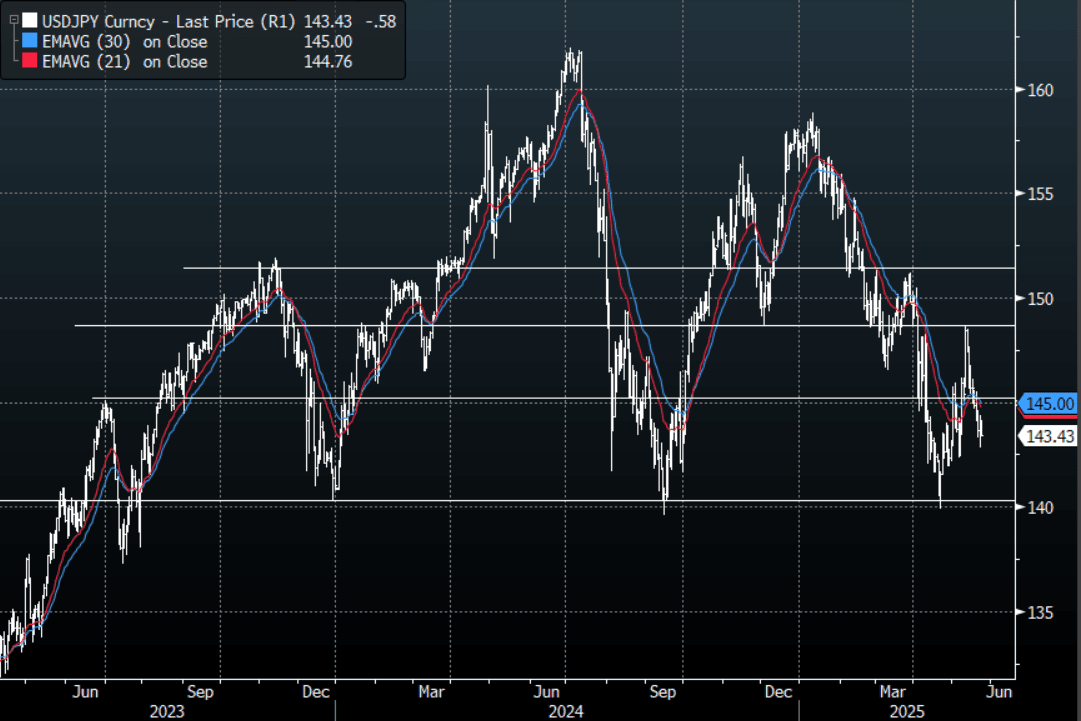

JPY: Asia Wrap - Sellers Cap Move Above 144.00 Again

The Asia-Pac range has been 143.40 - 144.14, Asia is currently trading around 143.45. The relief from USD selling overnight did not last long, USD/ASIA has seen a fresh round of selling in our session as Asia's major markets have another strong week of inflows with almost $2bn recorded to yesterday.

- "Japan's hotter-than-expected core inflation boosts odds of a Bank of Japan rate hike in July, ING's Min Joo Kang says in a research report. Consumer prices excluding fresh food rose 3.5% in April from a year earlier, up from March's 3.2% increase, and exceeded the market consensus of a 3.4% increase, the senior economist for South Korea and Japan notes. Excluding fresh food and energy, core-core CPI rose 3.0% on year in April, which suggests underlying inflation will remain above the BOJ's target of 2.0%, the economist says." (DJ via BBG)

- “ Workers at companies affiliated with the Japan Business Federation won pay hikes exceeding 5% for a second consecutive year, which will help to keep a floor under domestic inflation”(BBG)

- “ISHIBA: FEEL TRUMP AND I SHARED BROAD UNDERSTANDING, CONVEYED HOPE FOR PRODUCTIVE TALKS OVER TRADE; WILL KEEP SEEKING REMOVAL OF ADDITIONAL US TARIFFS" - BBG

- USD/JPY again struggled to hold onto any gains above 144.00, fresh USD/Asia selling has seen the USD broadly lower in our session.

- The price action for the week shows the market is still much more comfortable selling rallies, resistance is now back towards 145.00/146.00. The longer we stay down here the focus will turn once more to the pivotal 140.00 area.

Options : Closest significant option expiries for NY cut, based on DTCC data: 145.00($2.1b May 23),144.00($2.09b May 23), 140.00(1.67b May 23). Upcoming Strikes : 143.00($1.36b May 28), 145.00($1.39b May 28).(BBG)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

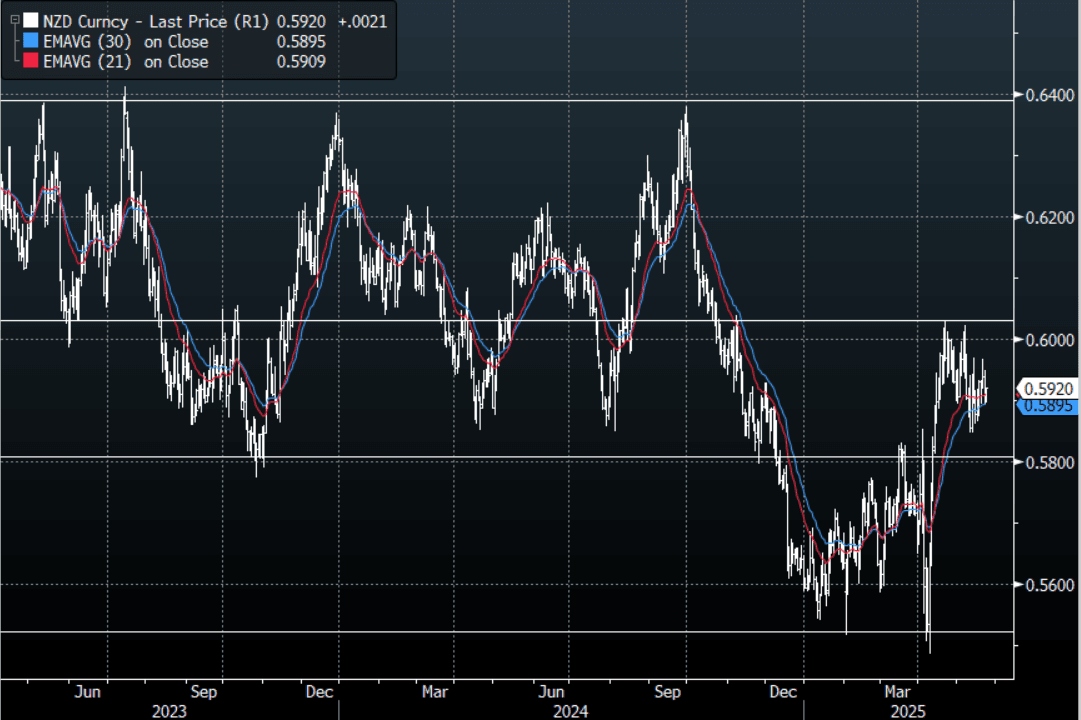

NZD: Asia Wrap - NZD/USD Bounces Off 0.5900

The NZD/USD had a range of 0.5896 - 0.5921 in the Asia-Pac session, going into the London open trading around 0.5920. The USD found some good demand overnight as some positions were pared back heading into the US long weekend. This price action has not followed into our session as fresh selling in USD/ASIA has seen the USD struggle across the board today, Asia's major stock markets had another strong week of inflows with almost $2bn recorded to yesterday.

- Q1 Retail Volumes Up More Than Forecast, Y/Y Pace Edges Higher : New Zealand Q1 retail sales volumes rose 0.8%q/q, versus a flat market forecast. The Q4 rise was also nudged a little higher to +1.0% (against an originally reported 0.9% gain). Today's print is a positive in the sense that other retail/consumer spend indicators have suggested a more adverse backdrop.

- “The Treasury cut projections for bond issuance by NZ$2 billion each of two fiscal years starting in July, The reduction in issuance projections was “tangible positive news,” ANZ senior strategist David Croy writes in a note.”(BBG)

- The NZD/USD has traded quietly bid in Asia today bouncing off the support it found around the 0.5900 area overnight.

- The NZD continues to look comfortable in a 0.5850/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break here is needed to regain momentum.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none, Upcoming Strikes : 0.5705(NZD805m May 23), 0.5980(NZD513m May26)

AUD/NZD range for the session has been 1.0862 - 1.0884, currently trading 1.0875. A sustained break above 1.0930 is needed to turn the focus higher, until then expect supply on bounces.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - AUD/USD Benefits From USD/Asia Selling

The AUD/USD has had a range of 0.6408 - 0.6438 in the Asia- Pac session, it is currently trading around 0.6435. The USD found some good demand overnight as some positions were pared back heading into the US long weekend. This price action has not followed into our session as fresh selling in USD/ASIA has seen the USD struggle across the board today, Asia's major stock markets are staring at another strong week of inflows with almost $2bn recorded to yesterday.

- Bloomberg - “Donald Trump’s tax bill faces changes and delays in the Senate after narrowly passing the House. Majority Leader John Thune said senators have questions about tax permanence and are engaged in a “very active discussion” over Medicaid.”

- “The path lower for dollar-yuan is being endorsed by a trickle down of PBOC daily fixings and its directional relationship with the forwards curve.”(BBG)

- The AUD has been quietly bid for most of the Asian session benefitting from fresh selling across the board in USD/ASIA.

- The AUD/USD is looking comfortable in a 0.6350 - 0.6550 range. The AUD continues to hold up pretty well against the USD so If you want to express a short it looks best to do that in the crosses for now.

- Expect buyers to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6375(AUD683m May 23),0.6475(AUD500m May 23) 0.6550(AUD529m May 23), Upcoming Strikes : 0.6510(AUD1.4b May 27)

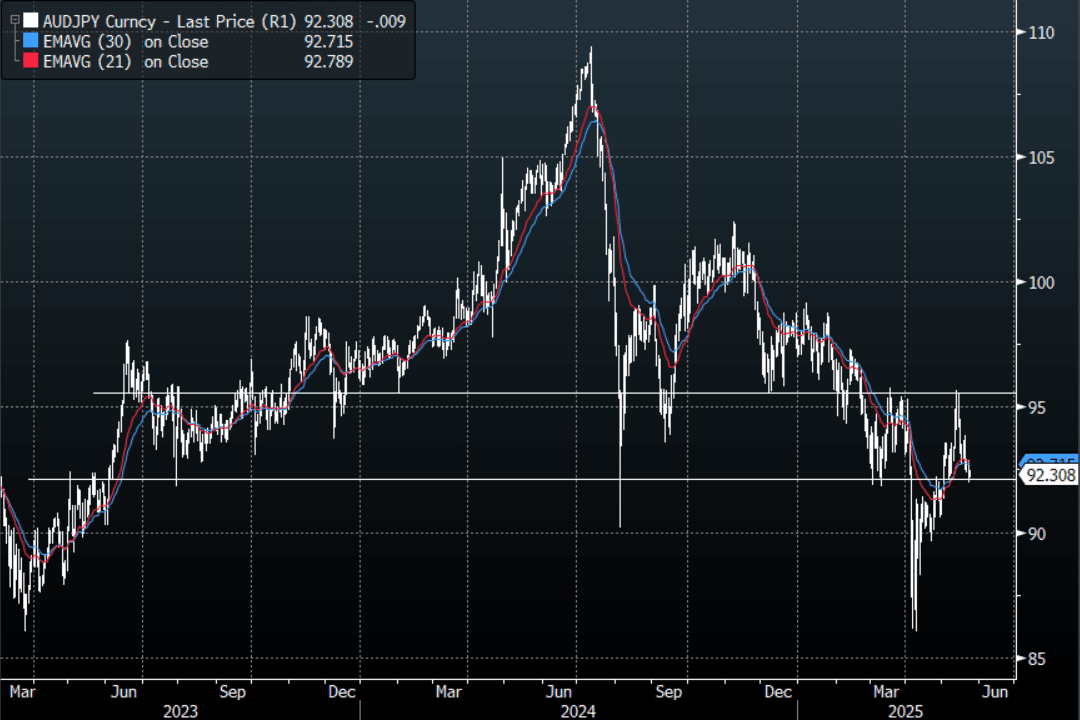

AUD/JPY - Today's range 92.16 - 92.48, it is trading currently around 92.30. Decent demand again seen towards the 92.00 area as it holds overnight. A sustained close back below 91.50/92.00 is needed to turn the focus back towards the lows again. With stocks looking like they could have more to go in this retracement it could provide further headwinds for this pair.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Major Bourses Mixed as US Fiscal Concerns Remain

Asia's major indexes have had a mixed week this week as deep concerns as to the US fiscal position impacted markets with China being the exception. Asian shares had a better day Friday as bond yield's climb higher stalled.

- China's major bourses all gained today with the Hang Seng up +0.58% and +1.43% for the week. The CSI 300 rose +.30% and is up +0.94% for the week; Shanghai is up a mere +0.08% and +0.46% for the week and Shenzhen gained +0.55% today and +0.77% for the week.

- The KOSPI was down marginally today by -0.05% and is off by -1.33% for the week.

- The FTSE Malay KLCI bounced higher today by +0.48% yet is down by -2.38% for the week.

- The Jakarta Composite is up +0.36% and is one of the best performers in the region up +1.22% for the week.

- The FTSE Straits Times in Singapore is lower by -0.18% and down by -0.63% for the week and the PSEi in the Philippines bounced strongly today by +0.89% yet remains -1.6% lower for the week.

- India's NIFTY 50 is up +0.80% whilst remaining down by -0.85% for the week.

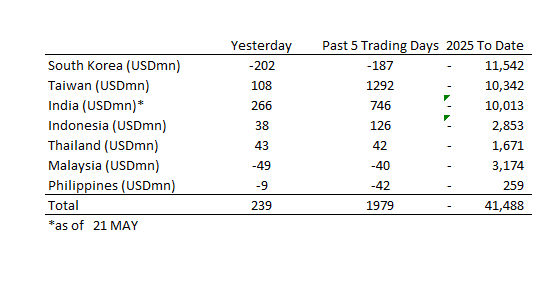

ASIA STOCKS: Another Strong Week of Inflows for Major Markets

Asia’s major markets are staring at another strong week of inflows with almost $2bn recorded to yesterday.

- South Korea: Recorded outflows of -$202m yesterday, bringing the 5-day total to -$187m. 2025 to date flows are -$11,542. The 5-day average is -$37m, the 20-day average is +$61m and the 100-day average of -$120m.

- Taiwan: Had inflows of +$108m yesterday, with total inflows of +$1,292m over the past 5 days. YTD flows are negative at -$10,342. The 5-day average is +$258m, the 20-day average of +$443m and the 100-day average of -$117m.

- India: Had inflows of +$266m as of the 21st, with total inflows of +$746m over the past 5 days. YTD flows are negative -$10,013m. The 5-day average is +$149m, the 20-day average of +$238m and the 100-day average of -$116m.

- Indonesia: Had inflows of +$38m as of yesterday, with total inflows of +$126m over the prior five days. YTD flows are negative -$2,853m. The 5-day average is +$25m, the 20-day average +$9m and the 100-day average -$33m.

- Thailand: Recorded inflows of +$43m as of yesterday, inflows totaling +$42m over the past 5 days. YTD flows are negative at -$1,671m. The 5-day average is +$8m, the 20-day average of -$9m the 100-day average of -$16m.

- Malaysia: Recorded outflows of -$49m as of yesterday, totaling -$40m over the past 5 days. YTD flows are negative at -$3,174m. The 5-day average is -$21m, the 20-day average of +$35m and the 100-day average of -$22m.

- Philippines: Saw outflows of -$9m as of yesterday, with net outflows of -$42m over the past 5 days. YTD flows are negative at -$259m. The 5-day average is -$8m, the 20-day average of +$1m the 100-day average of -$3m.

Oil Heading for Large Weekly Fall

- As OPEC+ continues to discuss yet another increase in production, oil prices have delivered large losses for the week.

- OPEC+ are discussing another rise in oil production for July with the final decision to be made next month.

- WTI has steadied today at US$60.84 bbl today and is on track to be lower by over -2.5% for the week.

- The falls this week sees WTI now trading below all major moving averages.

- Brent steadied in the Asia trading day to stem the overnight falls, yet remains on track to be lower by -2.00% for the week and is below all major moving averages.

- The EU is economy chief said it would be 'appropriate to lower the price cap on Russian oil to $50 bbl' to toughen Moscow's ability to fund the war in Ukraine. The current cap is set at $60, operators can buy oil from Russia only when it's purchased below the cap.

GOLD: Yesterday's Losses Forgotten

- Gold all but erased last night's losses to gain +0.54% in the Asian trading session to reach US$3312.33.

- The rally today puts gold on track to deliver gains over 3% for the week as fear over the US fiscal position saw a flight to bullion.

- Gold sits above all major moving averages; the nearest being the 20-day EMA of $3,272.06 with all moving averages sloping upwards, a sign that the bullish momentum remains.

- Gold has only failed to deliver a weekly gain in five of the twenty two weeks of the year so far.

- China’s onshore, gold-backed exchange-traded funds saw inflows resume as prices rebounded, according to a report by China Securities Journal. Some 20 gold ETFs listed on Chinese bourses received inflows of about 370m yuan on May 21, report said, citing data from Wind (source BBG)

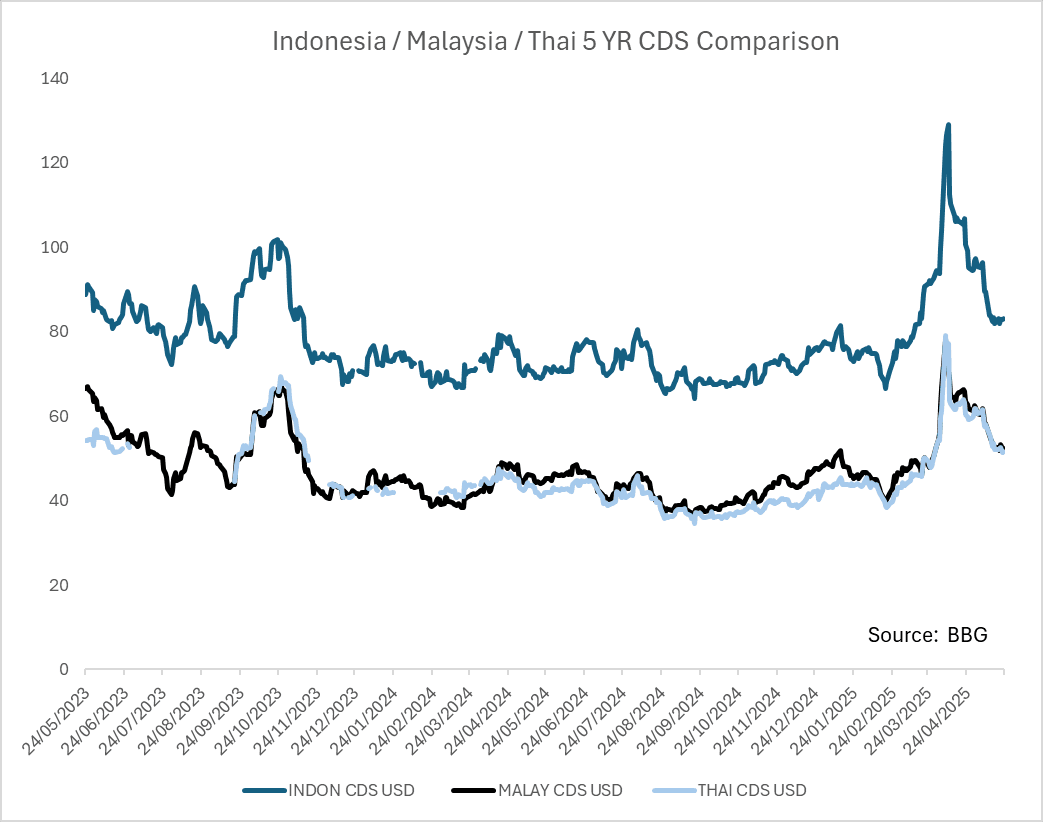

- In Early April we published on Indonesia noting "CDS Just Off Highs, FX Reserves Well Placed Relative To History" as tariffs were being threatened, and the trade war escalating Indonesia's equity market had struggled leading up to the EID break and before the tariff announcement, already down 8% year to date.

- Soon after the BI were vigilant and kept rates on hold at their April meeting. This spoke to their confidence and seemingly investors got the message thereafter. Leading up to the April meeting exchange data (via WFII on BBG) showed foreign investors pulling their money in the month prior to the tune of US$1bn of outflows. In the month since the April meeting the turnaround has been significant with inflows reaching US$190m. In that same time the Jakarta Composite has delivered gains of 14%.

- CDS had performed strongly into February with the 5-year touching 67bps in mid-February before widening on equity volatility to be 90bps just prior to the break. Upon return from the EID break the CDS capitulated to reach 131bps. At the time of our last post on April 11 the CDS was at 116. In context, the equity volatility in 2022 saw CDS widen to 161bps and during the height of COVID markets, the 5-year CDS touched 210bps.

- Today, following a very strong period for the equity markets CDS is at +83bps.

- Indonesia's markets are typically one of the more volatile in Southeast Asia with bond volatility linked closely to FX volatility and feeding directly into investor sentiment. Concerns earlier in the year that the Prabowo government policies were having a severe (negative) impact on the fiscal position were softened this week with news that the fiscal position is stabilizing for now.

- Additionally, the rupiah has gained over 3% in the last month, albeit coinciding with a near US$5bn decline in reserves.

- Yet that has been a point sometimes missed by investors. The BI today is not the same as before and is much better equipped to manage the currency thanks to the tools they have available to them.

- The rally in CDS has seen the CDS rally by +33bps over the last month. Indon 5 YR CDS still enjoys a 30bps premium over Malaysia and Thailand. The Indon / Malay relationship is back to its 3 year average whereas the Indon / Thai relationship is below its 3 year average.

Source: MNI - Market News/Bloomberg

ASIA FX: USD/KRW Dipping Towards Recent Lows, USD/TWD Eyeing 30.00 Test Again

In North East Asia FX markets, the USD bias has been weaker, albeit pairs have respected recent ranges. USD/CNH is lower, but only marginally sub the 7.2000 level. The won has been the standout, up 0.75%, putting USD/KRW back close to recent lows. TWD has climbed but has been unable to breach the 30.00 level. USD/HKD is higher though, as liquidity makes long USD/HKD an attractive carry trade.

- USD/CNH sits near 7.1980 in latest dealings, down a touch on end NY levels from Thursday. The USD/CNY fixing edged higher, but broader USD losses, particularly against the majors has provided an offset. Once again though, the CNH has maintained a very low beta with respect to such moves. The CSI 300 has climbed but remains below recent highs.

- Spot USD/KRW is back close to 1372/73, up around 0.75% in won terms and tracking towards recent lows sub 1370. KRW has been the best Asian FX performer so far this week, aided by on-going speculation around US-South Korea FX policy discussions. A clean break lower could see 1350 targeted on the downside.

- With USD/TWD support continuing to hold around 30.00, we may be seeing some rotation back into KRW, where more near term gains may materialize. The USD/TWD NDF space is seeing greater downside though, with the 1 month back under 29.70 today.

- Spot USD/HKD is close to week to date highs, last near 7.8320. Continued moves lower in Hibor rates is weighing on HKD.

ASIA FX: SEA FX Firmer, MYR & THB Lead

In South East Asian FX markets, USD selling pressures have been dominate. MYR has been a strong performer today, as has THB. We have seen more modest gains elsewhere, but nevertheless a clear USD downside bias. This fits with the majors where G10 currencies have rebounded against the USD, after Thursday saw some USD stability.

- USD/MYR is back under 4.2500, near recent lows. Downside focus will rest with a test back under 4.2000. The ringgit has been a strong performer in the past week, outperforming a softer local equity backdrop, along with higher US real yields. Commodity prices are also mostly under pressure. The MYR may be benefiting from repatriation flows given large FX deposits.

- USD/THB is back under 32.70, with upticks back towards 33.00 faded in recent sessions. Gold supported above $3300 is helping.

- USD/PHP is lower, back to 55.40/45 after holding steady in recent days. We had numerous comments from BSP Governor Remolona earlier. 2 more cuts are likely in 2025, although they won't necessarily be consecutive. The central bank looks at monthly trends in FX before deciding if its intervention thresholds have been met. Earlier May lows in the pair were at 55.235.

- USD/IDR is lower but holding above 16300 for now, which is very close to recent lows.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 23/05/2025 | 0600/0800 | ** | Unemployment | |

| 23/05/2025 | 0600/0700 | *** | Retail Sales | |

| 23/05/2025 | 0600/0800 | *** | GDP (f) | |

| 23/05/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 23/05/2025 | 0830/1030 | ECB's Lane Inflation Lecture in Florence | ||

| 23/05/2025 | 1230/0830 | * | Quarterly financial statistics for enterprises | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1335/0935 | Kansas City Fed's Jeff Schmid | ||

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1600/1800 | ECB's Schnabel Speech on Financial Education and Monpol | ||

| 23/05/2025 | 1600/1200 | Fed Governor Lisa Cook | ||

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |