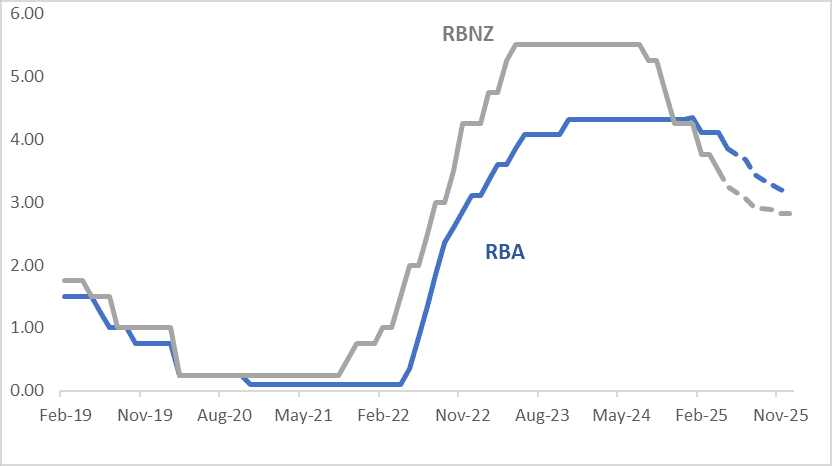

STIR: Expected YE AU-NZ Official Rate Diff Narrowed Substantially This Week

RBNZ-dated OIS pricing has seen little change across meetings compared to this time last week, with rates remaining 2–18bps above levels observed prior to the Q1 CPI release on April 17.

- By contrast, RBA-dated OIS pricing was 4–40bps higher than pre-CPI levels (April 30) as of last week.

- However, following Tuesday’s RBA easing and dovish tilt, RBA OIS pricing has retraced and is now only 8–25bps above pre-CPI levels.

- As a result, the expected year-end policy rate differential between Australia and New Zealand has narrowed by approximately 16bps over the past week, currently sitting at +30bps.

Figure 1: RBA & RBNZ Official Rate Profile (%)

Source: MNI - Market News / Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Yields Drift Lower In The Long End

TYM5 has traded higher with a range of 110-20 to 111-00+ during the Asia-Pacific session. It last changed hands at Heading 110-29, up 0.04 from the previous close.

- The US 10-year yield is drifting lower, dealing around 4.34%, down from its open around 4.40%

- The US 2-year yield is unchanged, dealing around 3.81%

- Risk has reversed higher as Trump makes a U-turn saying he won’t fire Powell and made comments that seemed to soften his stance towards China.

- Block Curve flattener flows : SELL 8200 of USM5 traded at 108-06, post-time 01:25:20 BST (DV01 $353,017). BUY 2800 of USM5 traded at 114-22, post-time 01:25:20 BST (DV01 $353,492).

- 10-year Yields, having bounced off their support around the 4.25 area, yields are consolidating with the range looking something like 4.25/4.50% for now.

Data/Events : US S&P Global Services & Manufacturing PMI, New Home sales

AUSSIE BONDS: Holding A Twist-Flattener, Light Local Calendar

ACGBs (YM -6.0 & XM +1.5) are dealing mixed on a data light Sydney session, with the short-end under pressure as markets re-assess tariff-tied risks to global trade and the Trump Admin's efforts to meddling with the Federal Reserve's independent policy making.

- Risk-on sentiment extended into today’s Asia-Pacific session after US President Trump stated that he had no intention of firing Fed Chair Powell (which has been a cause of concern recently and around the outlook for Fed Independence).

- Trump also stated that the final tariff number for China wouldn't be near the current 145%. He also expressed optimism around trade deals with lots of countries and spoke of the large investment agreements reached for flows into the US.

- Cash US tsys have twist-flattened in today's Asia-Pac session, with yields 2bps higher to 8bps lower.

- Cash ACGBs are 6bps cheaper to 1bps richer with the AU-US 10-year yield differential at -10bps.

- Swap rates are flat to 5bps higher, with the 3s10s curve flatter.

- The bills strip is cheaper with pricing -4 to -9.

- RBA-dated OIS pricing is 2-10bps firmer across meetings today. A 50bp rate cut in May is given a 14% probability, with a cumulative 114bps of easing priced by year-end (based on an effective cash rate of 4.09%).

JGBS: Follows US Tsys Into A Twist-Flattener At Lunch

At the Tokyo lunch break, JGB futures are weaker, -32 compared to the settlement levels, but above session lows.

- Cash US tsys have twist-flattened in today’s Asia-Pac session, with yields 2bps higher to 8bps lower. This comes with risk-on sentiment extending into today’s Asia-Pac session after US President Trump stated that he had no intention of firing Fed Chair Powell (which has been a cause of concern recently and around the outlook for Fed Independence). Such fears were a further weight on broader US asset related sentiment.

- Trump also stated that the final tariff number for China wouldn't be near the current 145%. He also expressed optimism around trade deals with lots of countries and spoke of the large investment agreements reached for flows into the US.

- The cash JGB curve has twist-flattened, pivoting at the 20-year, with yields 4.5bps higher to 5bps lower. The benchmark 10-year yield is 3.6bps higher at 1.351% versus the cycle high of 1.596%.

- The swaps curve has also twist-flattened, with rates 3bps higher to 4bps lower.

- Today, the local calendar has been light, with Jibun Bank PMIs as the highlight. The Tertiary Industry Index is due later. Tomorrow will see PPI Services.