INDONESIA: Indonesia CDS Back to FV

May-23 01:29

- In Early April we published on Indonesia noting "CDS Just Off Highs, FX Reserves Well Placed Relative To History" as tariffs were being threatened, and the trade war escalating Indonesia's equity market had struggled leading up to the EID break and before the tariff announcement, already down 8% year to date.

- Soon after the BI were vigilant and kept rates on hold at their April meeting. This spoke to their confidence and seemingly investors got the message thereafter. Leading up to the April meeting exchange data (via WFII on BBG) showed foreign investors pulling their money in the month prior to the tune of US$1bn of outflows. In the month since the April meeting the turnaround has been significant with inflows reaching US$190m. In that same time the Jakarta Composite has delivered gains of 14%.

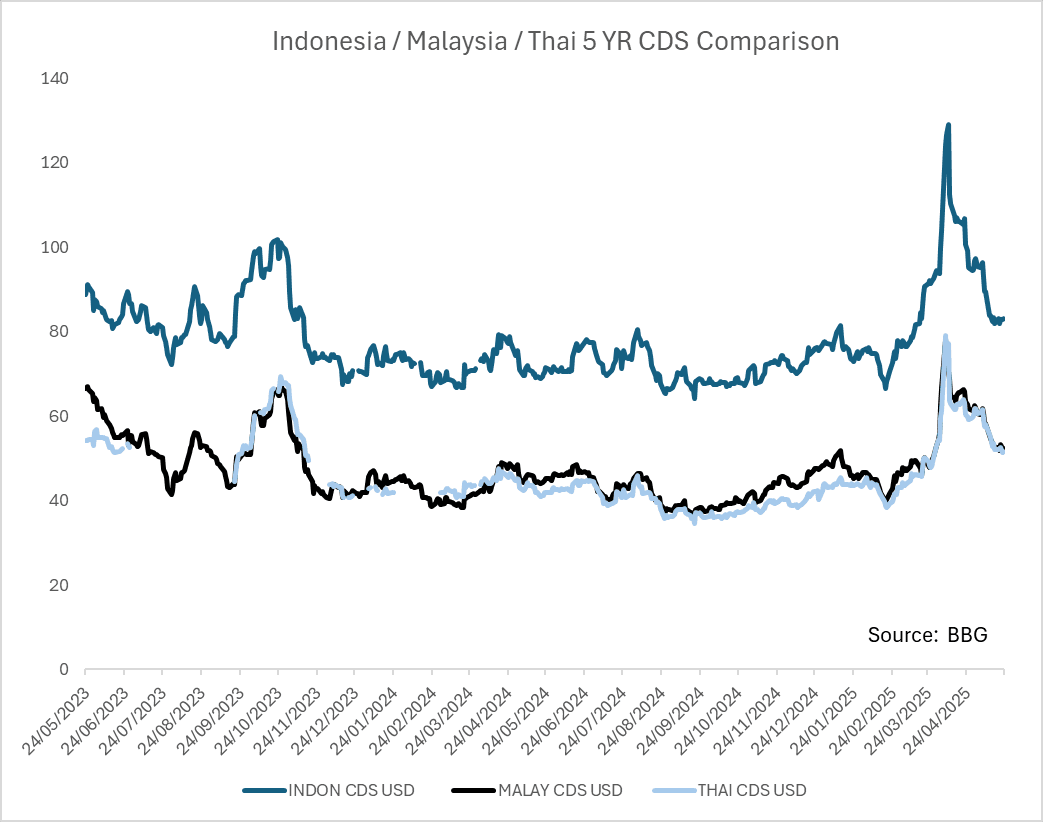

- CDS had performed strongly into February with the 5-year touching 67bps in mid-February before widening on equity volatility to be 90bps just prior to the break. Upon return from the EID break the CDS capitulated to reach 131bps. At the time of our last post on April 11 the CDS was at 116. In context, the equity volatility in 2022 saw CDS widen to 161bps and during the height of COVID markets, the 5-year CDS touched 210bps.

- Today, following a very strong period for the equity markets CDS is at +83bps.

- Indonesia's markets are typically one of the more volatile in Southeast Asia with bond volatility linked closely to FX volatility and feeding directly into investor sentiment. Concerns earlier in the year that the Prabowo government policies were having a severe (negative) impact on the fiscal position were softened this week with news that the fiscal position is stabilizing for now.

- Additionally, the rupiah has gained over 3% in the last month, albeit coinciding with a near US$5bn decline in reserves.

- Yet that has been a point sometimes missed by investors. The BI today is not the same as before and is much better equipped to manage the currency thanks to the tools they have available to them.

- The rally in CDS has seen the CDS rally by +33bps over the last month. Indon 5 YR CDS still enjoys a 30bps premium over Malaysia and Thailand. The Indon / Malay relationship is back to its 3 year average whereas the Indon / Thai relationship is below its 3 year average.

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: USD/CNY Fixing Higher, But Error Term Rewidens On USD Bounce

Apr-23 01:25

The USD/CNY fix printed at 7.2116, versus a BBG market consensus of 7.3417.

- Today's fix saw a re-widening of the error term to -1301pips from -818pips yesterday. This fits with higher USD index levels over the past 24 hours.

- The actual fix was still below recent highs, which rest at 7.2133.

- USD/CNH dipped to lows of 7.2922 earlier, but sits back around 7.3050 in latest dealings. We saw earlier support for CNH following comments from US President Trump that the final tariff rate on China would be lower than the 145% that currently prevails.

MNI: CHINA PBOC CONDUCTS CNY108 BLN VIA 7-DAY REVERSE REPO WEDS

Apr-23 01:22

- CHINA PBOC CONDUCTS CNY108 BLN VIA 7-DAY REVERSE REPO WEDS

US TSY FLOWS: Block BUY: USM5

Apr-23 01:20

2800 of USM5 traded at 114-22, post-time 01:25:20 BST (DV01 $353,492). The contract is currently dealing at 114-12, +0-25 from closing levels.