MNI EUROPEAN MARKETS ANALYSIS: RBA Expected To Cut Next Week

- The USD has given back part of Thursday's gains, most notably against the yen. Japan Household spending surged in May, well above expectations. US Tsy futures have edged higher.

- US President Trump stated that the US will likely be sending out letters to 10-12 countries outlining tariff rates later today US time.

- Australian household spending for May was also stronger than forecast, but RBA easing odds remain very high for next week's policy meeting.

- With US markets out, we have second tier EU and UK data due.

MARKETS

US TSYS: Asia Wrap - Futures Edge Higher With No Cash Market

The TYU5 range has been 111-07 to 111-11 during the Asia-Pacific session. It last changed hands at 111-10+, up 0-03+ from the previous close.

- No cash market today.

- The 10-year yield has seen a strong bounce in reaction to the better NFP print. This 4.35/40% area offers those who would like to express a long the opportunity to fade. A sustained close back above 4.40/4.45% area though would not be great for the bulls and would see more of the longs prepared back.

- Bob Elliot on X: ”Employment report internals confirm continued labor market weakening. Private sector jobs are weak. Strong payrolls number driven by unusual surge in gov jobs. HH survey employment down since Jan. Unemployment is up. Labor force participation falling. Wage growth is slowing.”

- Bloomberg - “Goldman Sachs has lowered its forecasts for US Treasury yields, expecting 2- and 10-year yields to end the year at 3.45% and 4.20%, respectively. The move follows Goldman's economists revising their expectations for Fed rate cuts, now predicting cuts in September, October, and December.”

- MNI FED: Atlanta's Bostic: "No Time For Significant Shifts" In Policy. Atlanta Fed President Bostic largely reiterates previous commentary on current monetary policy (including at Monday's MNI event) in a speech in Frankfurt. "A period characterized by such widespread uncertainty is no time for significant shifts in monetary policy." "That is especially the case against the backdrop of a still resilient macroeconomy, which offers space for patience."

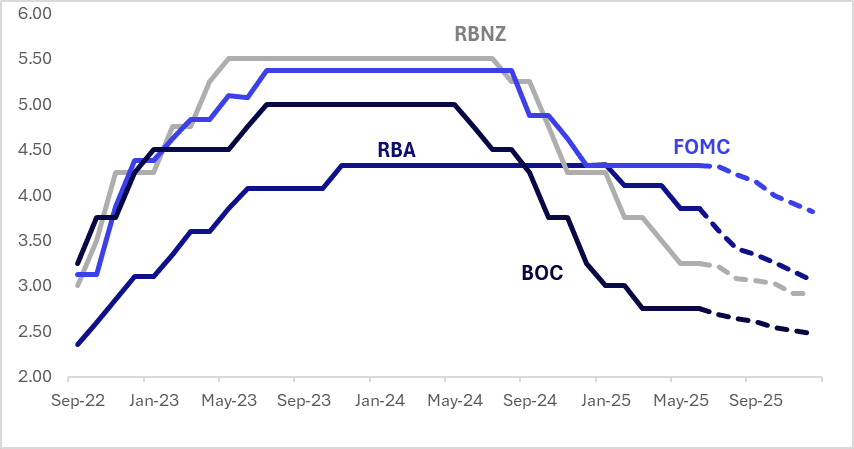

STIR: US Leads $-Bloc Markets Firmer

Interest rate expectations across dollar-bloc economies firmer over the past week, led by a 14bp gain in the US. Canada, Australia and New Zealand saw modest firming in the range of 2-6bps.

- Yesterday, US nonfarm payrolls growth comfortably beat expectations in June with 147k (cons 106k) along with small upward revisions of +16k after a string of releases with large downward revisions. Arguably an even bigger surprise was the pullback in the unemployment rate, which at 4.117% unrounded is the lowest since January, down from 4.244% prior and well below the rounded 4.3% consensus.

- The labour market appears to be in solid enough shape to keep the Fed on the sidelines. Most focus was on the degree to which this effectively closed the door to a July Fed cut, with implied pricing falling to just 1bp (ie under 5% probability of a cut) from 6.5bp. And it brought down the implied 2025 cuts to 2, versus an evenly split pricing between 2 and 3 cuts.

- The next key event for the region is the RBA’s July 8 meeting, where a 25bp rate cut is currently given a 92% probability. The RBNZ decision is scheduled for the following day, with an 11% chance of a 25bps cut priced.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.81%, -52bps; Canada (BOC): 2.48%, -27bps; Australia (RBA): 3.08%, -78bps; and New Zealand (RBNZ): 2.92%, -33bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JGBS: Modest Bear-Steepener, Narrow Ranges With The US Markets Out

JGB futures are slightly stronger and at session highs, +2 compared to settlement levels.

- Japan's real household spending for May rose 4.7%y/y, well above market forecasts of a 1.2% gain. The April outcome was -0.1%y/y. In m/m terms, spending was up a strong 4.6%.

- (Bloomberg) - The grind higher in JGB long-end yields isn't done yet, with Japan's spring wage talks delivering the biggest pay bump in 34 years. Add to that today's pop in household spending -- the strongest since mid-2022 -- and the data drumbeat is starting to give the BOJ exactly what it's been looking for.

- "TACHIBANA: POLICY UNCHANGED FOR SINCERE TARIFF TALKS WITH US" – BBG

- Cash JGBs are flat to 2bps cheaper across benchmarks, with a steepening bias. The benchmark 10-year yield is 0.4bps higher at 1.446% versus the cycle high of 1.596%.

- Ranges have, however, been narrow with the US markets out for the 4th of July holiday. US 10-year futures are trading slightly higher.

- Swaps have twist-steepened, with rates 1bp lower to 1bp higher.

- On Monday, the local calendar will see Labor & Real Cash Earnings and Coincident/Leading Index.

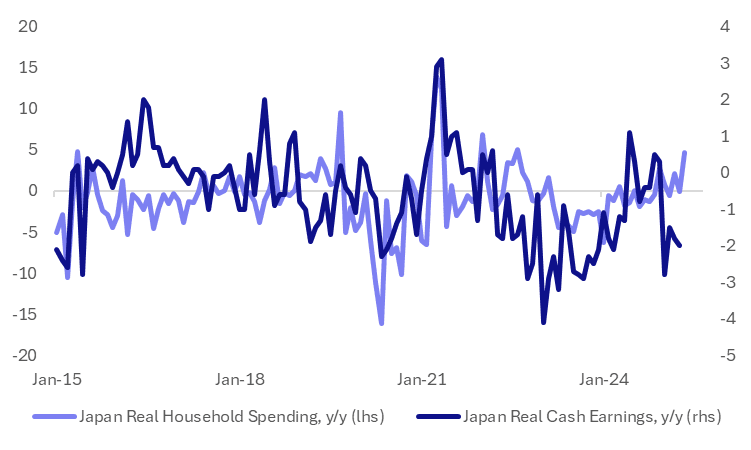

JAPAN DATA: May Household Spending Surges, Diverging From Softer Real Wages

Japan real household spending for May rose 4.7%y/y, well above market forecasts of a 1.2% gain. The April outcome was -0.1%y/y. In m/m terms spending was up a strong 4.6%.

- Focus will be on whether we can sustain this May bounce. The chart below plots real household spending y/y, versus real wages, also in y/y terms. With the May bounce in spending we now have some divergence between the two series. This is not uncommon from an historical standpoint, but usually the trends in both series gravitate towards each other over the medium term.

- Note that next Monday (7th of July) we get May labor cash earnings data.

- The May rise in y/y spending was the strongest outcome since August 2022. This should encourage the authorities, particularly following the stronger Capex data from the Tankan survey earlier this week.

- By category, transport and communication spending rose 25.3%y/y, while spending on recreation, culture was up 11.1%.

Fig 1: Japan Real Household Spending & Real Wages - Y/Y

Source: Bloomberg Finance L.P./MNI

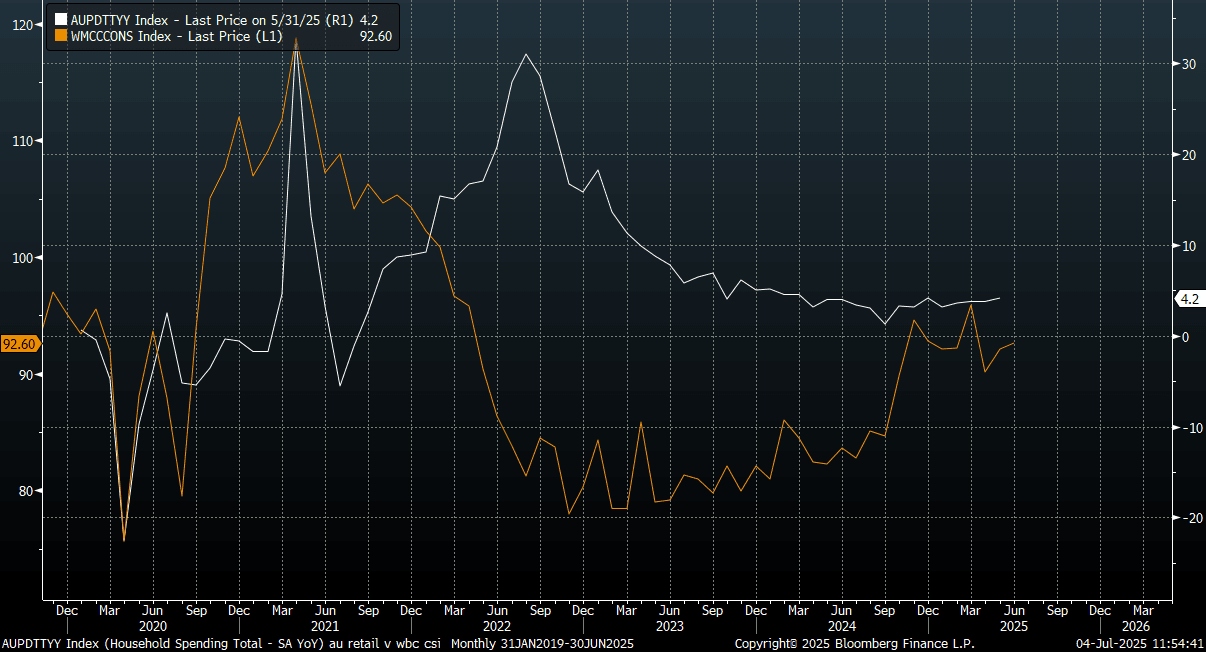

AUSTRALIA DATA: Household Spending Firms In May, Y/Y Trend Improving Modestly

Australian May Household spending data was stronger than forecast, rising 0.9%m/m, against a 0.5% forecast. In y/y terms we printed 4.2%, against an expected gain of 3.5% and prior 3.8% outcome. The April outcome was revised to flat in m/m terms, after initially being reported as a 0.1% gain.

- Today's print contrasts with the earlier retail sales this week, which came in below market forecasts (+0.2%m/m, versus +0.5% forecast). More weight should be given to today's May household spending outcome though, as it will replace the retail sales print from the end of this month.

- The ABS noted: "Robert Ewing, ABS head of business statistics, said: 'The rise in May was driven by spending on discretionary goods and services. 'Discretionary spending rose 1.1 per cent, as households spent more on clothing and footwear, new vehicles, and dining out. ‘Meanwhile, non-discretionary spending was up 0.5 per cent, rising for a fifth consecutive month.’

- Indeed, only food and alcoholic beverages saw m/m falls in May, all other categories saw m/m rises. Outside of alcoholic beverages, all sub indices are up in y/y terms as well.

- The chart below plots household spending in y/y terms against the Westpac Consumer Sentiment reading. Spending is maintaining a modestly positive trend in y/y terms. Sentiment is well up from cycle lows from 2022/2023, but the improvement has stalled since the end of last year.

- The RBA meets next week, with a 25bps cut widely expected. There has been little shift in OIS pricing for next week's meeting post today's data.

Fig 1: Household Spending Y/Y & Westpac Consumer Sentiment Index

Source: Bloomberg Finance L.P./Westpac/MNI

AUSSIE BONDS: Slightly Cheaper, Narrow Ranges, HH Spend Solid

ACGBs (YM -2.0 & XM -1.5) are cheaper but at the Sydney session bests. Ranges have, however, been narrow with the US markets out for the 4th of July holiday. US 10-year futures are trading slightly higher.

- (Bloomberg) Australia's May spending data presents a mixed picture, with weak retail trade data suggesting consumers are cautious, but stronger-than-expected broader spending data showing a surge in discretionary spending.

- Cash ACGBs are 1-2bps cheaper.

- The bills strip is cheaper, with pricing -3 to-4.

- On Monday, the local calendar will see ANZ-Indeed Job Advertisements and Foreign Reserves. The RBA Policy Decision is on Tuesday.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in July is given a 92% probability, with a cumulative 76bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Next week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Closed Flat After Reversing Early Weakness

NZGBs closed flat after reversing early weakness (4bps cheaper) following yesterday’s post-payrolls sell-off in US tsys.

- US markets are out today for the 4th of July holiday. US 10-year futures are trading slightly higher.

- The local calendar was empty today. The next major event on the calendar will be the RBNZ Monetary Policy Review next Wednesday.

- (Bloomberg) - "The market reaction to fresh US economic data on Thursday shows traders remain unconvinced that uncertainty from President Trump's trade war will significantly disrupt the global economy. A rally in global equity indexes as well as a robust bid for credit show increasingly resilient risk sentiment, and rising yields across the globe indicate a lack of demand for safe haven assets."

- Swap rates closed 1bp higher.

- RBNZ dated OIS pricing closed flat to 3bps firmer across meetings. 3bps of easing is priced for July, with a cumulative 31bps by November 2025.

- Interest rate expectations across dollar-bloc economies were firmer over the past week, led by a 14bp gain in the US. Canada, Australia and New Zealand saw modest firming in the range of 2-6bps.

FOREX: Asia FX Wrap - The USD Drifts Lower

The BBDXY has had a range of 1189.73 - 1191.48 in the Asia-Pac session, it is currently trading around 1189. The USD has drifted lower in a quiet Asia-Pac session, -0.18%, the price action is particularly poor given the surge in US yields and a market that is supposedly extremely short. “ The Chinese government plans to cancel the second day of a two-day summit with European leaders, scheduled for later this month, due to tensions between Brussels and Beijing”(BBG). "China Industries Cut Output Amid Price War Crackdown: Sec. Times. Companies across industries, from automobiles and solar to batteries, have begun reducing production or curbing price cuts, as the government intensifies efforts to rein in cut-throat competition, the Securities Times reports Friday." BBG

- EUR/USD - Asian range 1.1754 - 1.1780, Asia is currently trading 1.1775. While the USD remains on the back foot the EUR will be the main beneficiary. This market will now be looking towards 1.2000 and beyond, the price is starting to look a little stretched in the short term. First support is back towards 1.1600.

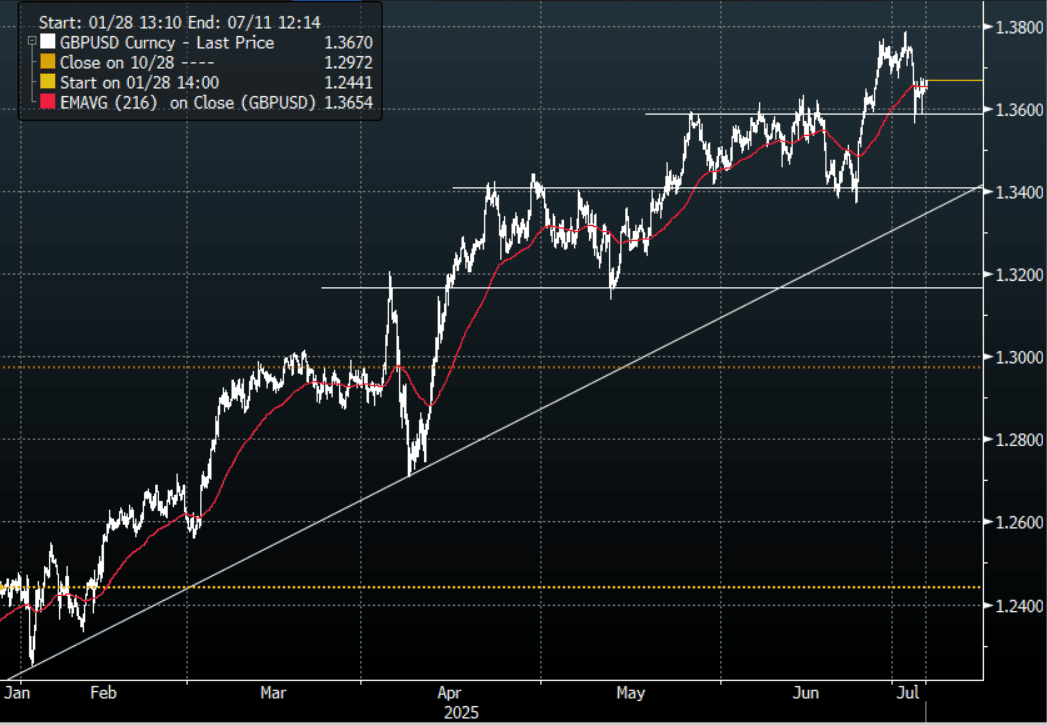

- GBP/USD - Asian range 1.3645 - 1.3668, Asia is currently dealing around 1.3670. For the second time strong demand was seen below 1.3600 helping the support to hold. A sustained move sub 1.3550 needed to signal a deeper correction.

- USD/CNH - Asian range 7.1626 - 7.1709, the USD/CNY fix printed 7.1535, Asia is currently dealing around 7.1630. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.30%, Gold $3340, TYU5 111-11, BBDXY 1189, Crude oil $66.88

- Data/Events : Italy Retail Sales, France Industrial Production, EZ PPI, Spain Industrial Production, Germany Factory Orders, HCOB Construction PMI

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

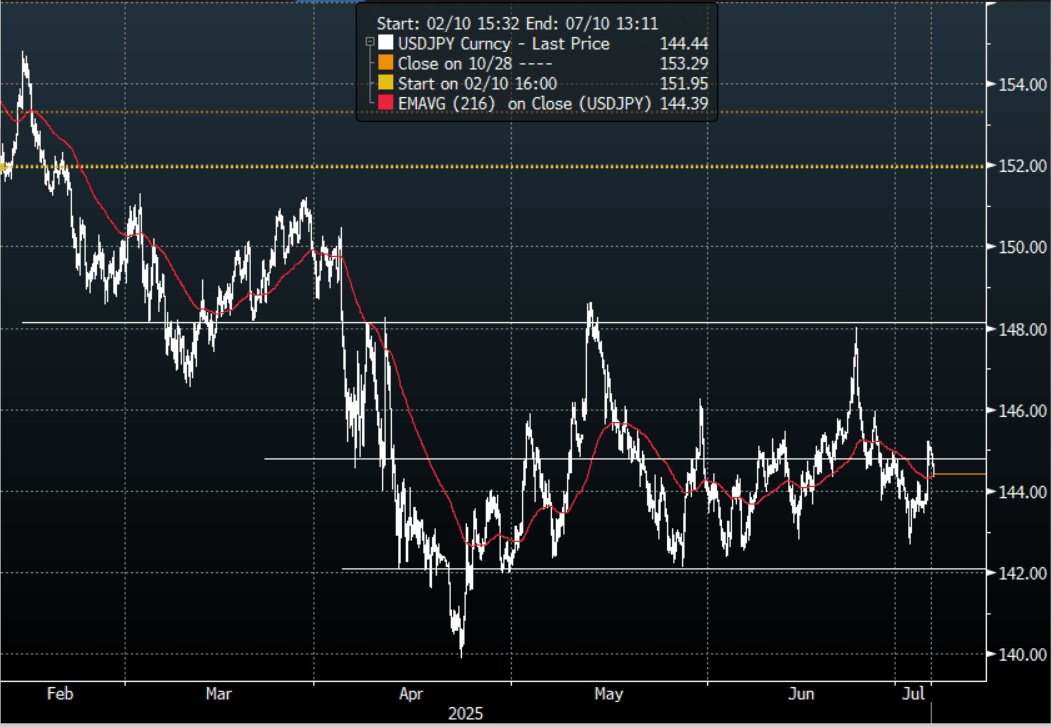

JPY: Asia Wrap - USD/JPY Gives Back Some Of Its NFP Gains

The Asia-Pac USD/JPY range has been 144.34 - 144.98, Asia is currently trading around 144.45, -0.35% drifting off its overnight highs in our session. The market wants to be short USD/JPY so will be disappointed with last night's result as the JPY longs would have been hoping for a reason to test lower. Price is now back in the middle of the wider 142.00 - 148.00 range and the pair will probably continue to take its cue from the US rates market which was also wrongly positioned for a better NFP.

- JAPAN DATA May Household Spending Surges, Diverging From Softer Real Wages : Japan real household spending for May rose 4.7%y/y, well above market forecasts of a 1.2% gain. The April outcome was -0.1%y/y. In m/m terms spending was up a strong 4.6%.

- (Bloomberg) - The grind higher in JGB long-end yields isn’t done yet, with Japan’s spring wage talks delivering the biggest pay bump in 34 years. Add to that today’s pop in household spending -- the strongest since mid-2022 -- and the data drumbeat is starting to give the BOJ exactly what it’s been looking for.

- "TACHIBANA: POLICY UNCHANGED FOR SINCERE TARIFF TALKS WITH US” - BBG

- The rejection of 148.00 points to a potential top being in place now and shows just how quick the market is to return to selling USD’s. USD/JPY was looking for a fresh catalyst to probe the lower end of its range again but NFP did not provide that so we are now back in the middle of the range. The JPY bulls will be hoping the move higher in US yields is capped pretty soon as a break higher in rates would start to make a very long JPY market vulnerable.

- Options : Close significant option expiries for NY cut, based on DTCC data: 142.00($984m), 140.00($1.04b).Upcoming Close Strikes : 142.75($855m July8).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Consolidates In A Quiet Session

The AUD/USD has had a range of 0.6563 - 0.6579 in the Asia- Pac session, it is currently trading around 0.6570, -0.05%. The pair has traded sideways in a very subdued session. US Equity futures have drifted off their overnight highs in Asia, ESU5 -0.22%, NQU5 -0.20%. With US yields surging higher and staying there the USD’s inability to hold onto any gains is a worrying sign for the currency, especially when positioning is supposedly all the same way and at extreme levels. Look for some consolidation again in the AUD/USD as the pair continues to build a base from which to move higher.

- AUSTRALIA DATA - Household Spending Firms In May, Y/Y Trend Improving Modestly: Australian May Household spending data was stronger than forecast, rising 0.9%m/m, against a 0.5% forecast. In y/y terms we printed 4.2%, against an expected gain of 3.5% and prior 3.8% outcome. The April outcome was revised to flat in m/m terms, after initially being reported as a 0.1% gain.

- Today's print contrasts with the earlier retail sales this week, which came in below market forecasts (+0.2%m/m, versus +0.5% forecast). More weight should be given to today's May household spending outcome though, as it will replace the retail sales print from the end of this month

- "REUTERS POLL-RESERVE BANK OF AUSTRALIA TO CUT CASH RATE TO 3.60% ON JULY 8, SAID 31 OF 37 ECONOMISTS; SIX SAID NO CHANGE" - RTRS

- The AUD/USD is breaking through the top of its recent range as the pressure on the USD increases. First support is seen back towards the 0.6500 area.

- The AUD needs a sustained break above 0.6550/0.6600 to potentially start building momentum for an extended move higher, a close back above 0.6600 and the focus would turn back to 0.6900/0.7000.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD2.59b), 0.6500(AUD 1.38b). Upcoming Close Strikes : 0.6600(AUD884m July 7), 0.6375(AUD722m July 8)

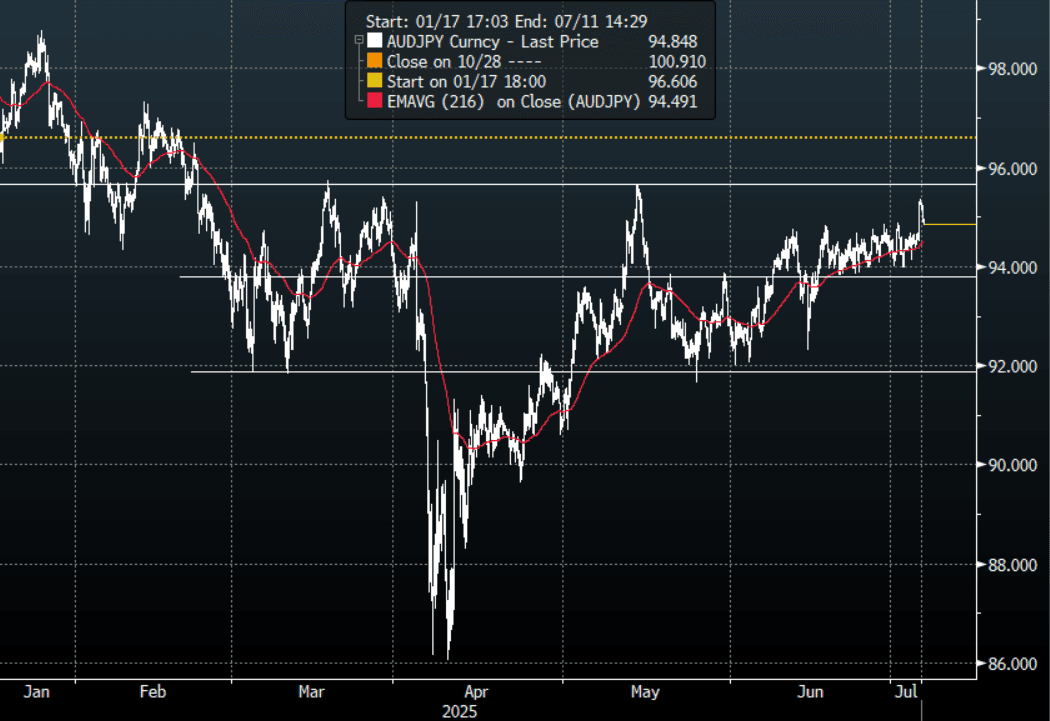

- AUD/JPY - Today's range 94.84 - 95.37, it is trading currently around 94.85, -0.42%. The pair broke above its recent highs around 95.00 overnight and with risk sentiment turning positive it could be turning its focus back towards the 96.00 area.

Fig 1: AUD/JPY spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Trades Sideways In A Subdued Session

The NZD/USD had a range of 0.6064 - 0.6082 in the Asia-Pac session, going into the London open trading around 0.6070, -0.05%.The pair has traded sideways in a very subdued session. US Equity futures have drifted off their overnight highs in Asia, ESU5 -0.3%, NQU5 -0.28%. With US yields surging higher and staying there the USD’s inability to hold onto any gains is a worrying sign for the currency, especially when positioning is supposedly all the same way and at extreme levels. NZD/USD continues its attempt to build a solid base from which to push higher.

- (Bloomberg) - “The market reaction to fresh US economic data on Thursday shows traders remain unconvinced that uncertainty from President Trump’s trade war will significantly disrupt the global economy. A rally in global equity indexes as well as a robust bid for credit show increasingly resilient risk sentiment, and rising yields across the globe indicate a lack of demand for safe haven assets.”

- “Trade Letters May Go Out Later Today, Informing Countries Of Tariff Levels : In earlier remarks US President Trump stated that the administration is likely to start sending letters later today informing countries of where tariff rates will be set. This comes ahead of next week's reciprocal tariff pause deadline.”(BBG)

- A huge bounce from sub 0.5900 and the NZD has now established a foothold above 0.6000, with the USD breaking lower the NZD/USD looks to be building for a potential break higher of its own. A clear break of 0.6100 could provide the momentum to begin a larger move higher, initially targeting the 0.6400/0.6500 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6075(NZD519m July 9).

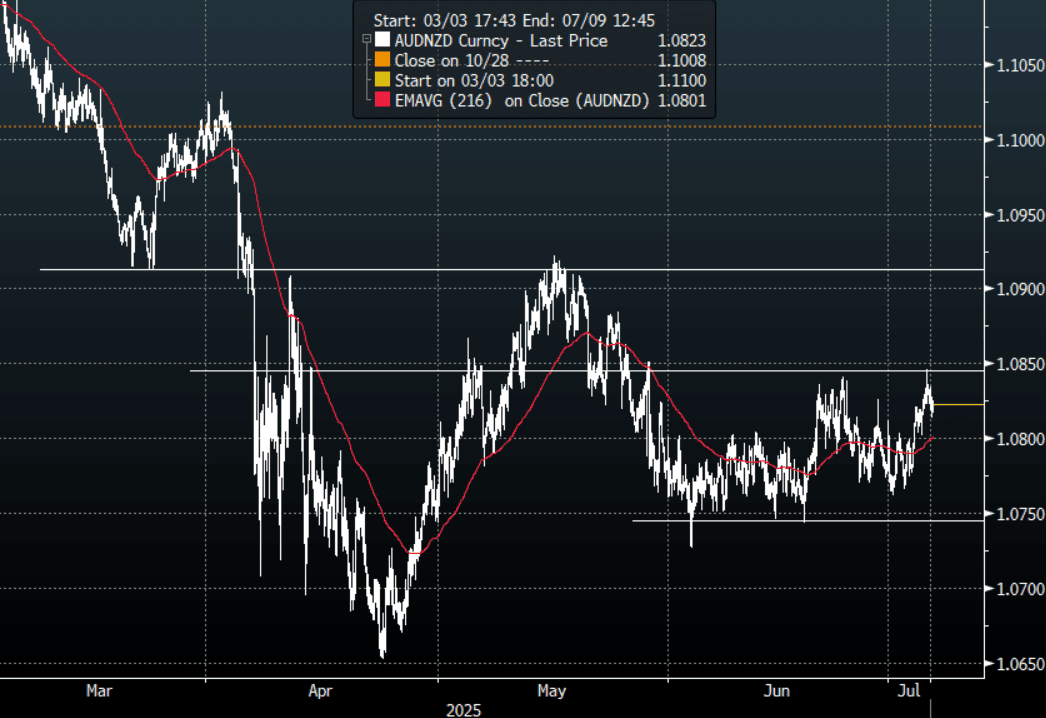

- AUD/NZD range for the session has been 1.0813 - 1.0834, currently trading 1.0820. The cross is struggling to get any momentum for now. It looks to be in a 1.0750 - 1.0850 range for now as it awaits a catalyst to provide some clearer direction.

Fig 1: AUD/NZD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: KOSPI Down Heavily on Tariff Concerns

As the deadline for tariffs looms large, Korea's KOSPI has had heavy falls into the week's end as investors begin to fear the resumption of tariffs on the export orientated economy. After posting strong gains yesterday on the hope that bills to improve governance in the country will be beneficial to equity investors, today saw falls that erased those gains and could see the KOSPI finish lower for the week. This weighed on several key markets in the region with very few delivering any meaningful gains.

- China's major bourses have had a mixed end to the week. The Hang Seng is down with Shenzhen whilst the CSI 300 and Shanghai are up. The Hang Seng is down -0.62% today and -1.66% for the week. The CSI 300 is up +0.41% today and +1.60% for the week and the Shanghai Comp up +0.41% and +1.50% for the week. The Shenzhen Comp is down -0.07% today but has had a strong week up +1.50%.

- Taiwan's TAIEX if down -0.66% today and -0.26% for the week.

- The KOSPI is down -1.61% today and holding on to modest gains of +0.35% for the week.

- The FTSE Malay KLCI is up modestly by +0.13% and has had a strong week delivering gains of +1.50%.

- The Jakarta Composite is down -0.21% today and -0.50% for this week.

- The FTSE Straits Times in Singapore is down -0.30% today but up +1.05% for the week whilst the PSEi in the Philippines fell heavily today by -0.95% and is currenlty flat for the week.

- India's NIFTY 50 is doing very little in their morning session and will need a strong rally to erase the gains week to date of -0.92%

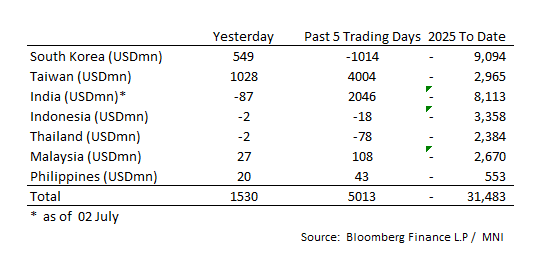

ASIA STOCKS: Strong Inflows Yesterday for Korea and Taiwan

Since the beginning of June, Taiwan has received consistent inflows most days and is now at $7.9bn since then.

- South Korea: Recorded inflows of +$549m yesterday, bringing the 5-day total to -$1,014m. 2025 to date flows are -$9,094. The 5-day average is -$203m, the 20-day average is +$62m and the 100-day average of -$78m.

- Taiwan: Had inflows of +$1,028m yesterday, with total inflows of +$4,004 m over the past 5 days. YTD flows are negative at -$2,965. The 5-day average is +$801m, the 20-day average of +$460m and the 100-day average of -$3m.

- India: Had outflows of -$87m as of the 2nd, with total inflows of +$2,046m over the past 5 days. YTD flows are negative -$8,113m. The 5-day average is +$409m, the 20-day average of +$143m and the 100-day average of $1m.

- Indonesia: Had outflows of -$2 yesterday, with total outflows of -$18m over the past five days. YTD flows are negative -$3,358m. The 5-day average is -$4m, the 20-day average -$23m and the 100-day average -$32m.

- Thailand: Recorded outflows of -$2m yesterday, with outflows totaling -$78m over the past 5 days. YTD flows are negative at -$2,384m. The 5-day average is -$16m, the 20-day average of -$13m and the 100-day average of -$21m.

- Malaysia: Recorded inflows of +$27m yesterday, totaling +$108m over the past 5 days. YTD flows are negative at -$2,670m. The 5-day average is +$22m, the 20-day average of -$9m and the 100-day average of -$19m.

- Philippines: Recorded inflows of +$20m yesterday, with net inflows of +$43m over the past 5 days. YTD flows are negative at -$553m. The 5-day average is +$9m, the 20-day average of -$2m the 100-day average of -$5m.

Oil Down Today but Set for Weekly Gain

- In a market where liquidity was low ahead of the US holiday, stronger than expected jobs data and the ongoing discussions from OPEC+ about an increase supply were enough to push oil lower in the Asia trading day.

- WTI is down in the Asia trading session by -0.46% at US$66.86 bbl but remains up over 2% for the week.

- WTI sits marginally above the 20-day EMA of $66.76 and below the 200-day EMA of $66.27.

- Brent is down -0.39% today at $68..59 and for the week is up +1.20% following strong gains on Wednesday.

- American refiners are relying on oil supplies from the country's biggest shale basins more than ever as flows of denser varieties from places like Mexico and Canada ebb. US drillers are using the lightest oil on record, according to recent government data, leaning heavily on shale formations in Texas, New Mexico and North Dakota. The shift comes as heavy crude supplies are strained by falling production from Mexico, a trade spat with Canada and a de facto US ban on imports of Venezuelan oil. (source BBG)

- China avoided purchasing US crude for the third straight month - the longest stretch since 2018 - delivering a fresh blow to shale drillers already facing lower oil prices.

- Iranian oil output reached a 46-year high in 2024 and is expected to increase again this year, despite US oil sanctions. The country's energy sector has emerged unscathed, with energy export revenue hitting a 12-year high of $78 billion last year.

Gold Set to Finish Week Higher

- With the US out and trading volumes low, gold looks set to finish the week higher thanks to gains on Monday and Tuesday.

- With Middle East tensions easing, gold traders turn their attention to US data as a guide for interest rates and trade talks. As data overnight indicated a stronger economy the probability of interest rate cuts are being pushed out. With a deal announced with Vietnam it is anticipated in the coming days further new announcements with countries be revealed.

- Gold is up +1.93% and is currently trading at US$3,337.90 just $94.44 off the May high.

- Year to date gold is up +28%. If it were to hold those returns it would be the best year since 2010 in which it delivered 29.5% of gains.

- Gold move today sees is just above the 20-day EMA of $3,337.34

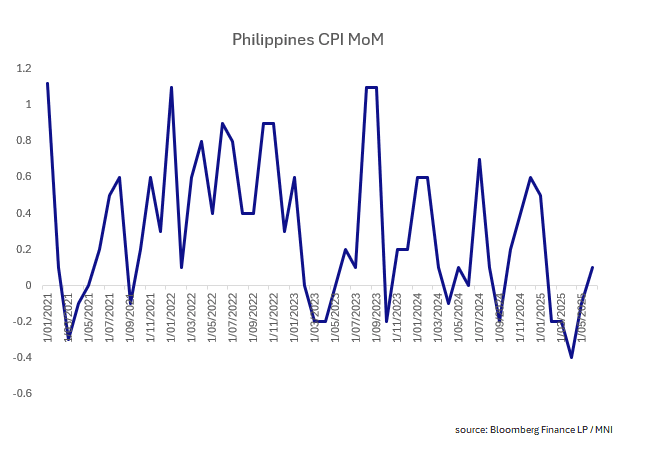

PHILIPPINES: Inflation Going Nowhere in the Philippines

- June's inflation release showed little sign of pricing pressures returning to the Philippines.

- The YoY figure nudged up to +1.4% in June, from +1.3% in May, with the market expecting +1.5%.

- Prices in the capital rose +2.6% YoY whilst core rose +2.2% YoY with some pricing pressure in housing, water and electricity.

- The first half of the year result for CPI was a rise of +1.8% YoY.

- In December, the Development Budget Coordination Committee, in consultation with the BSP, set the inflation target at 2-4% from this year until 2028.

- The Month on Month figure moved just into positive territory, rising +0.1% after -0.1% in May.

ASIA FX: Muted End To The Week, USD/KRW Above1360 As Kospi Weakens

In North East Asia FX markets, FX trends have been quite muted in the first part of Friday trade. USD/CNH has drifted down a touch, while KRW and TWD are biased weaker against the USD. USD/HKD remains close to the top end of the peg band.

- USD/CNH has drifted a little lower, the pair last near 7.1625/30, so still within recent ranges, but unwinding some of Thursday's NFP induced bounce. USD/JPY is lower, which may be helping CNH at the margins. The China authorities it was speeding up implementation of the framework agreed with the US in London. This involves approving export licenses for controlled items (e.g. rare earths). This comes after the US reinstated approvals for IT software exports. China equities are higher, outperforming weakness in other parts of the region.

- Spot USD/KRW got above 1367 before finding selling interest. The pair was last back at 1364/65, little changed for the session. Local equities are down sharply, the Kospi off 1.65%, which may reflect some profit taking after the Commercial Revision Act was passed yesterday. US President Trump stated the US will also be sending out letter on tariff levels to countries, starting today. South Korea is sending officials to the US to continue to negotiate in the lead up to next week's reciprocal tariff pause deadline.

- USD/TWD is a little higher, last near 28.85, which is up a touch from earlier lows just under 28.80. Weakness has also been evident from Taiwan stocks today, the Taiex down 0.70%.

- USD/HKD has gravitated back towards the top end of the trading band, near 7.8500. Further HKMA intervention hasn't induced a sharp rise in short end Hibor rates.

INDONESIA: Country Wrap: Boosting US Imports to Get Better Deal

- he Indonesian government is seeking lower import tariffs from the United States than those recently granted to Vietnam, in an effort to improve the competitiveness of Indonesian products in the US market. Vietnam secured a new tariff agreement with the US this week, with duties set at 20 percent, down from an initial 46 percent proposed by former President Donald Trump in April. Trump announced the revised deal on Truth Social on Thursday, saying it was the result of direct talks with Vietnam’s top leader, To Lam, ahead of a July 9 deadline. (source Jakarta Globe)

- The Indonesian government has proposed boosting imports from the United States by up to $34 billion as part of ongoing negotiations aimed at securing relief from trade tariffs imposed by President Donald Trump. Coordinating Minister for Economic Affairs Airlangga Hartarto said on Thursday that the proposal includes significant purchases of energy and agricultural commodities, as well as investment plans involving Indonesia’s sovereign wealth fund, Danantara. (source Jakarta Globe)

- The Jakarta Composite is down -0.21% today and -0.50% for this week.

- The rupiah is flat on the day at 16,198 and is where it started for the week.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 04/07/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 04/07/2025 | 0645/0845 | * | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Unemployment | |

| 04/07/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/07/2025 | 0800/1000 | * | Retail Sales | |

| 04/07/2025 | 0800/1000 | ECB Elderson Speech At IMF OEDNE/World Bank Meeting | ||

| 04/07/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/07/2025 | 0900/1100 | ** | PPI | |

| 04/07/2025 | 1500/1600 | BOE Taylor Speech On Natural Interest Rate |