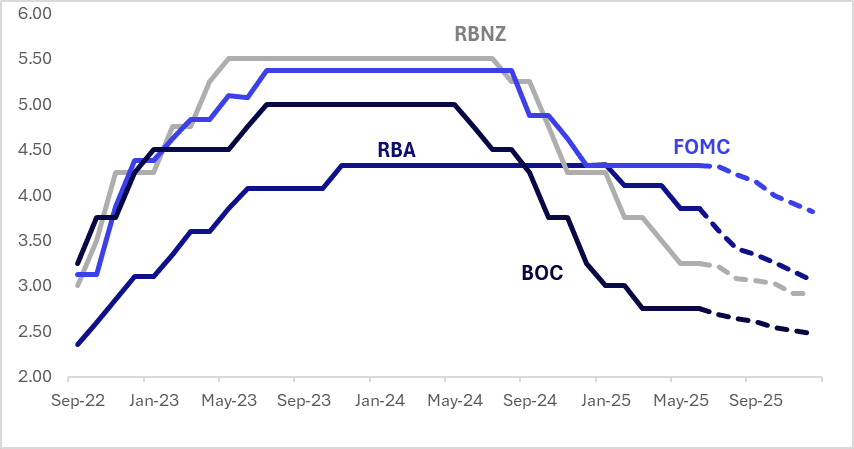

STIR: US Leads $-Bloc Markets Firmer

Interest rate expectations across dollar-bloc economies firmer over the past week, led by a 14bp gain in the US. Canada, Australia and New Zealand saw modest firming in the range of 2-6bps.

- Yesterday, US nonfarm payrolls growth comfortably beat expectations in June with 147k (cons 106k) along with small upward revisions of +16k after a string of releases with large downward revisions. Arguably an even bigger surprise was the pullback in the unemployment rate, which at 4.117% unrounded is the lowest since January, down from 4.244% prior and well below the rounded 4.3% consensus.

- The labour market appears to be in solid enough shape to keep the Fed on the sidelines. Most focus was on the degree to which this effectively closed the door to a July Fed cut, with implied pricing falling to just 1bp (ie under 5% probability of a cut) from 6.5bp. And it brought down the implied 2025 cuts to 2, versus an evenly split pricing between 2 and 3 cuts.

- The next key event for the region is the RBA’s July 8 meeting, where a 25bp rate cut is currently given a 92% probability. The RBNZ decision is scheduled for the following day, with an 11% chance of a 25bps cut priced.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.81%, -52bps; Canada (BOC): 2.48%, -27bps; Australia (RBA): 3.08%, -78bps; and New Zealand (RBNZ): 2.92%, -33bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Bond Futures Mixed

- China's key bond futures are moving in the opposite direction today as the OMO maintained liquidity with a very modest withdrawal.

- The 10YR future is lower by -.03 at 108.63 having just breached the 100-day EMA of 108.64

- The 2YR future is up +.01 to 102.36 and remains below all major moving averages. The nearest being the 20-day EMA at 102.42.

- Bonds are seeing limited movement with the CGB10YR at 1.70. The CGB10YR has traded in a tight range of 1.61-1.71 since early April.

JGBS: Slightly Cheaper At Lunch

At the Tokyo lunch break, JGB futures are weaker, -19 compared to the settlement levels, and hovering near Tokyo session lows.

- (Bloomberg) -- Japan currently hasn’t received a letter from the US Trade Representative’s office, sent to trading partners as a deal deadline reminder, Japanese Chief Cabinet Secretary Yoshimasa Hayashi says in a regular press conference Wednesday.

- Japan's private sector experienced a loss of growth momentum in May, with the headline au Jibun Bank Japan Services Business Activity Index easing to 51.0 in May from 52.4 in April.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session after yesterday's modest losses. The 10-year yield continues to find good support around 4.35/40%.

- Cash JGBs are flat to 1bp cheaper across benchmarks, with the futures-linked 7-year underperforming. The benchmark 10-year yield is 0.7bp higher at 1.501% versus the cycle high of 1.596% after yesterday's strong auction result.

- Swap rates are slightly higher. Swap spreads are mostly tighter.

AUSTRALIA DATA: Weak Productivity, Rising Compensation & ULC Above 5% y/y

There was no progress on the productivity front in Q1 with GDP per hour worked posting its second consecutive unchanged quarter leaving it down 0.9% y/y. A 0.2% q/q drop in Q2 is needed to reach the RBA’s May Q2 productivity forecast of -0.6% y/y, and so that remains possible but may be a little pessimistic. Unit labour costs growth rose again at 5.1% y/y up from 4.7% and the highest since Q2 2024.

Australia productivity vs ULC y/y%

Source: MNI - Market News/ABS

- Average compensation per employee rose 1.0% q/q, the second straight quarterly rise around 1% or above since Q3 2022. Annual growth picked up to 3.7% y/y from 3.5%. Q1 WPI inflation rose 0.2pp to 3.4% y/y. While wage growth is subdued it appears to be picking up and with weak productivity growth is not consistent with the RBA’s inflation target.

- Total employee compensation rose 1.5% q/q to be up 6.5% y/y in Q1, the highest in a year, after 2.0% & 6.0%.

- The current RBA GDP outlook and slower but steady hours worked doesn’t achieve sustained productivity growth of the historical average of 1%. If hours fall over the rest of 2025, then some solid growth can be realised above 2%.

- Unit labour cost growth would slow to around 2.5% y/y if hours worked continue to rise but if they fall then it will trough at around 0.5% y/y.

Australie average compensation per employee y/y%

Source: MNI - Market News/LSEG