MNI RBNZ WATCH: OCR To Hold, Split Vote Likely

The Reserve Bank of New Zealand’s Monetary Policy Committee is expected to hold the Official Cash Rate at 3.25% when it meets next Wednesday, though another split vote appears likely as policymakers weigh both domestic and international headwinds.

The RBNZ has now cut a cumulative 225 basis points across six consecutive meetings since August 2024. With the OCR approaching the upper bound of the Bank’s estimate of the neutral rate, the MPC is expected to pause and assess how current settings are influencing economic activity.

However, as at the May meeting, which resulted in a 5-1 vote, debate is likely to centre on the economy’s underlying weakness, the persistently negative output gap, and the potential benefits of waiting before making what could be an inevitable further cut. (See MNI RBNZ WATCH: 5-1 Vote Drives 25bp Cut To 3.25%)

Markets are assigning just a 13.1% probability to a rate cut next week, but expect the OCR to reach 2.9% by November, consistent with the Bank’s May projections. That implies at least one more reduction before year-end.

MIXED DOMESTIC DATA

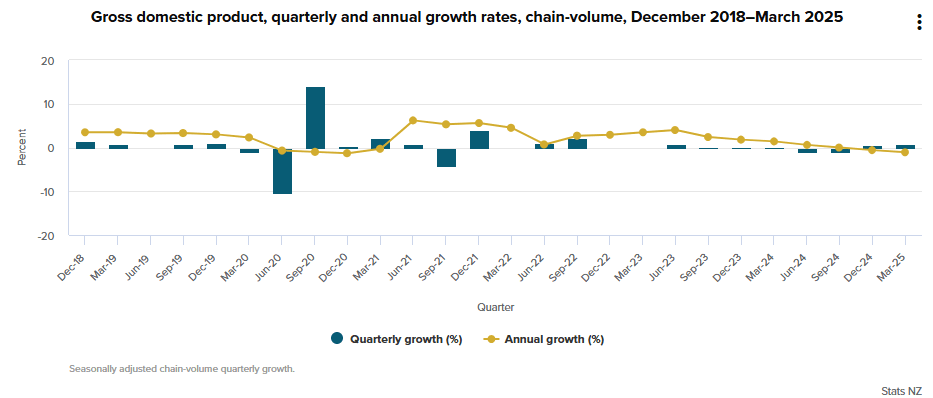

First-quarter GDP growth surprised to the upside at 0.8% q/q, stronger than assumptions in the May Monetary Policy Statement. This may indicate a less negative output gap than the Bank’s last -1.3% estimate, reflecting a slightly more resilient economy.

Improved business sentiment in the Q2 Quarterly Survey of Business Opinion adds to the evidence of modest momentum, giving the RBNZ breathing room to monitor developments abroad – particularly the U.S. administration’s actions after the July 9 tariff deadline. However, the survey also showed real activity and demand remaining weak.

May’s Selected Price Index pointed to modest upside risk for near-term inflation, supporting the Bank’s forecast for CPI inflation to rise to 2.7% in Q3 – above the 2% midpoint of its 1-3% target range.

Meanwhile, both the PSI and PMI posted contractions in May, suggesting renewed weakness, especially in the manufacturing sector – fuel for doves on the MPC who remain concerned about slowing domestic demand.

GLOBAL UNCERTAINTY

Complicating next week’s decision is its timing – just hours ahead of the July 9 tariff deadline set by the U.S. administration. This makes it difficult for the committee to weigh external risks with confidence.

Chief Economist Paul Conway has acknowledged the heightened uncertainty facing the Bank in the months ahead. (See MNI INTERVIEW: RBNZ's Uncertainty To Persist-Chief Economist) At the May meeting, the lone dissenting member voted to hold, preferring more time to see whether elevated inflation and inflation expectations would settle before easing further.

Looking ahead, the MPC will likely prefer to see greater clarity on U.S. trade policy and its implications for global growth before weighing another cut at its Aug 20 meeting.