MNI RBNZ WATCH: 5-1 Vote Drives 25bp Cut To 3.25%

The first dissenting vote on the Reserve Bank of New Zealand’s monetary policy committee in over two years was prompted by a disagreement over timing rather than policy direction, Acting Governor Christian Hawkesby told reporters after the five-one decision to cut the official cash rate by 25 basis points to 3.25% on Wednesday.

“We did form a consensus around our set of projections that we published today and that included a central projection for the OCR,” Hawkesby said, referring to the updated Monetary Policy Statement, which showed a 2.9% rate by December – 10 basis points lower than February’s forecast, suggesting at least one more cut this year.

Despite the dissent, Hawkesby said the RBNZ’s assessment showed less inflationary pressure than forecast in February. “We also acknowledge that there is a high degree of uncertainty around that,” he added, noting recent price strength.

“That is just one central projection. There are many other paths the economy could take, and the confidence ranges around that central projection are wide enough for us to not have a bias either way in terms of what the next step is at the next meeting. It will be dependent on developments and what those developments mean for medium-term inflation pressure in New Zealand.”

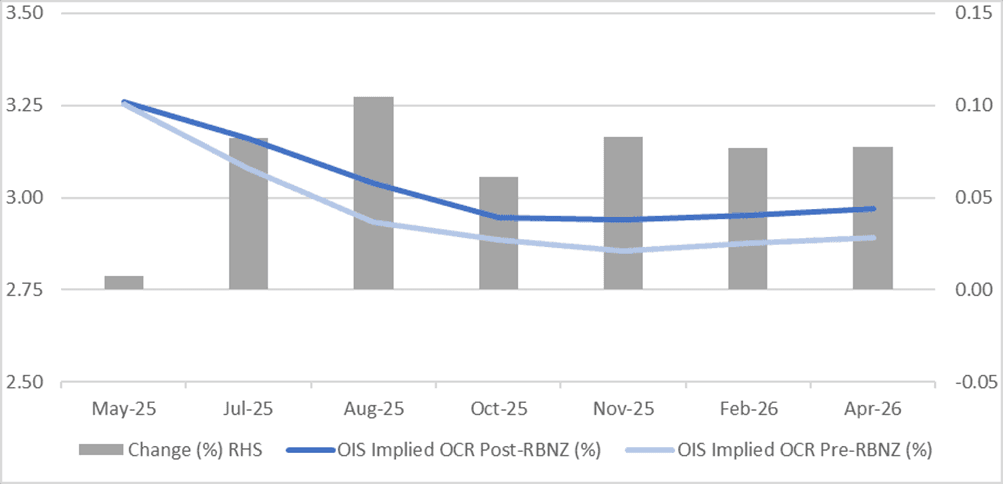

While Wednesday’s decision was largely anticipated, the split vote appeared to push market pricing for further rate cuts higher following the press conference. (See MNI RBNZ WATCH: MPC Set To Cut 25bp, Lean Into Future Data)

Market pricing now aligns with the MPS’s OCR track, assigning a 35% probability of a cut in July and 52% in August.

GREAT EXPECTATIONS

Though Hawkesby emphasised the likelihood of lower inflation ahead, he acknowledged expectations remained elevated, likely due to recent headline price strength. The MPC will continue to monitor these expectations, which he said were likely overly sensitive following the recent period of high inflation.

“Some [MPC] members put more emphasis on the risk that those higher inflation expectations might be a sign of something more persistent,” he said. “Other members put more emphasis on the amount of spare capacity there is in the economy, and therefore inflation pressure is likely to come out.”

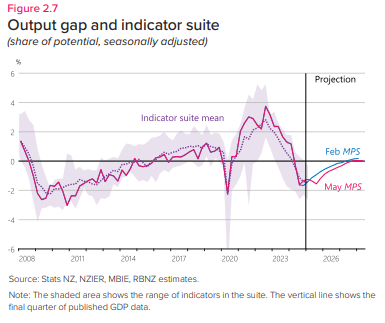

The RBNZ believes significant spare capacity now exists in the economy and that the output gap has moved into negative territory. (See chart)

Hawkesby also noted that the U.S. tariff offensive may have influenced inflation expectations, despite the Reserve’s view that the impact would likely be deflationary for domestic prices.

However, the RBNZ’s statement flagged heightened uncertainty over whether the global trade shock would ultimately act as a net negative demand shock – inducing disinflation – or a net negative supply shock that would fuel prices. For the first time in five years, the Bank included two alternative scenarios in its forecasts: one reflecting weaker demand, in which the OCR falls to 2.55%, and another showing a supply shock, where the OCR initially drops to 2.9% before rising to 3.5% later in the forecast period.

NEUTRAL LEVEL

Chief Economist Paul Conway said the current 3.25% OCR sits near the top of the RBNZ’s 2.5-3.5% neutral range.

“When we get close to neutral, which is definitely where we are now, it's more a matter of feeling our way, rather than being too definitive about whether policy is stimulatory or otherwise,” Conway said. “That's very much the world that we're in currently.”

He added that the Reserve would focus on how the economy responds to the OCR to determine the level of current monetary restriction.

The MPC next meets July 9.