MNI US Macro Weekly: Stage Set For A Hawkish Fed Cut

Dec-05 17:28By: Chris Harrison

US+ 1

Download Full Report Here

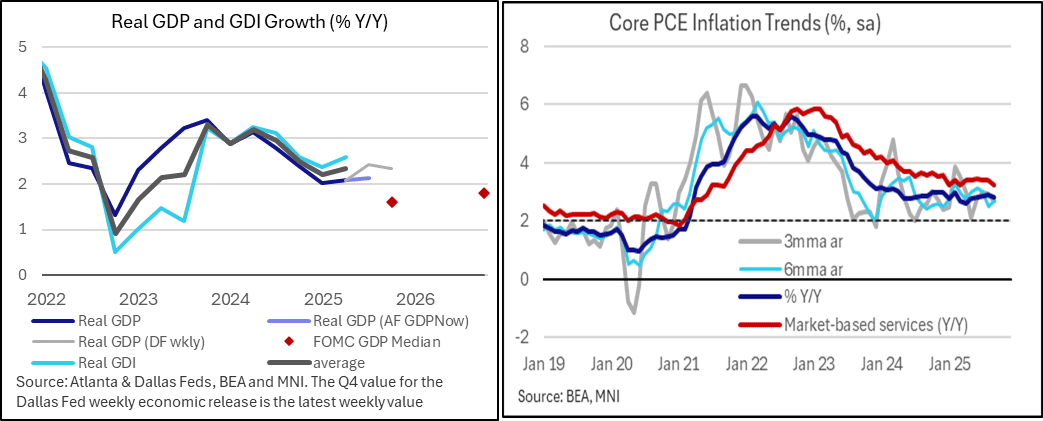

- Real GDP growth tracking has been trimmed after a softer than expected personal income & outlays report for September, although is still seen at a solid 3.5% annualized for Q3 in the last update before the FOMC.

- Core PCE inflation was slightly softer than expected in that same delayed September report, still running at above 2% target rates but ruling out a further acceleration.

- Headlining a slew of labor market updates this week, ADP confirmed a return to declining payrolls employment having now dropped in three of the past four months, although weekly jobless claims data don’t suggest any further deterioration. Initial claims in particular were extremely low but likely down to Thanksgiving adjustment issues.

- Major business surveys were mixed, with ISM services firming but also seeing lower new orders and prices paid whilst ISM manufacturing returned to the lower end of its recent range in contractionary territory.

- NECs Hassett’s probability of being chosen as the next Fed Chair has climbed on the week as a whole although were trimmed modestly on media reports of Wall Street pushback – he’s still seen at >70%. Trump says he will probably announce his pick early next year.

- US Tsy Sec Bessent meanwhile has gone into further details on his plan to enforce that regional Fed presidents have lived in their district for at least three years. It comes ahead of what could be a more controversial renewing of president five-year terms in Feb 2026. Hassett has given his approval.

- Next week is dominated by the FOMC decision, widely expected to deliver a third consecutive 25bp cut after NY Fed Williams’ uncharacteristic guidance following the delayed September payrolls report. It’s likely to be a contentious meeting though with many FOMC members preferring to have paused.

- Being a SEP meeting, the dot plot distribution will be watched keenly whilst we expect the economic projections to show an upward revision for GDP growth and downward revision for core PCE inflation.

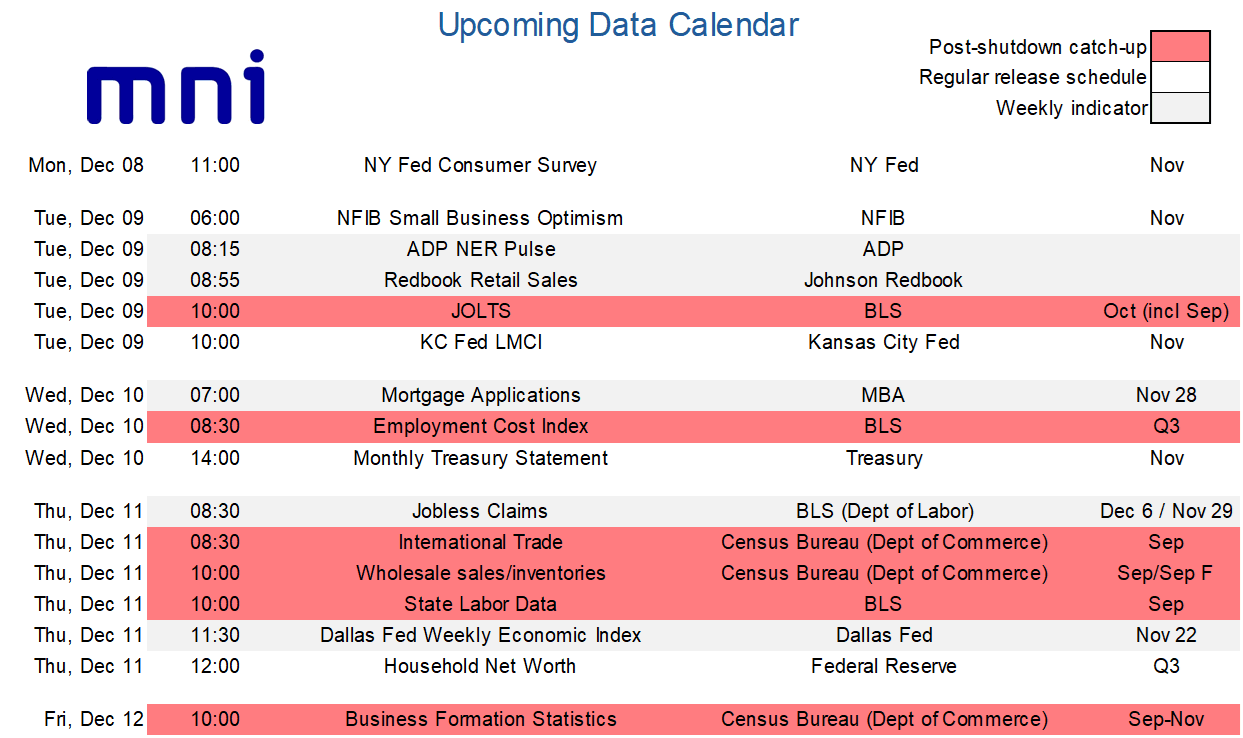

- The FOMC will see two months of JOLTS data on the first day of their two-day meeting otherwise must wait until the following week for NFP (Dec 16) and CPI (Dec 18) reports for November. A reminder that these will see various degrees of backfilling for missing October values.