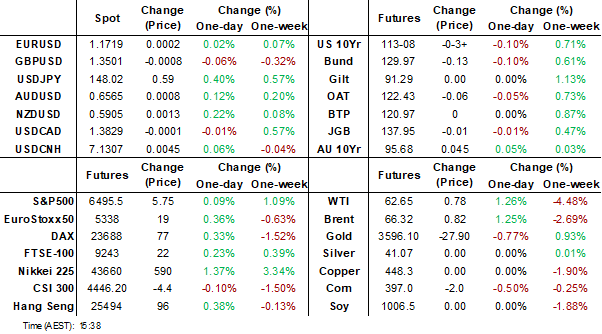

MNI EUROPEAN MARKETS ANALYSIS: Oil Prices Higher On Monday

- Early focus was on fallout in Japan after PM Ishiba announced he will step down. Yen weakened and the JGB curve steepened, but we are away from earlier extremes. An LDP leadership election is likely for early Oct.

- US Tsy yields retraced a touch higher, while the USD was mostly softer (ex JPY).

- Oil prices fell sharply on Friday ahead of the weekend’s OPEC decision but given the cautious 137kbd increase in the output target from October, there appears to be a relief rally today.

- Later August NY Fed 1-yr inflation expectations, July US consumer credit and German July trade & IP print. The focus of the week will be on Tuesday’s US payroll benchmark revisions, Wednesday’s August PPI and Thursday’s August CPI.

MARKETS

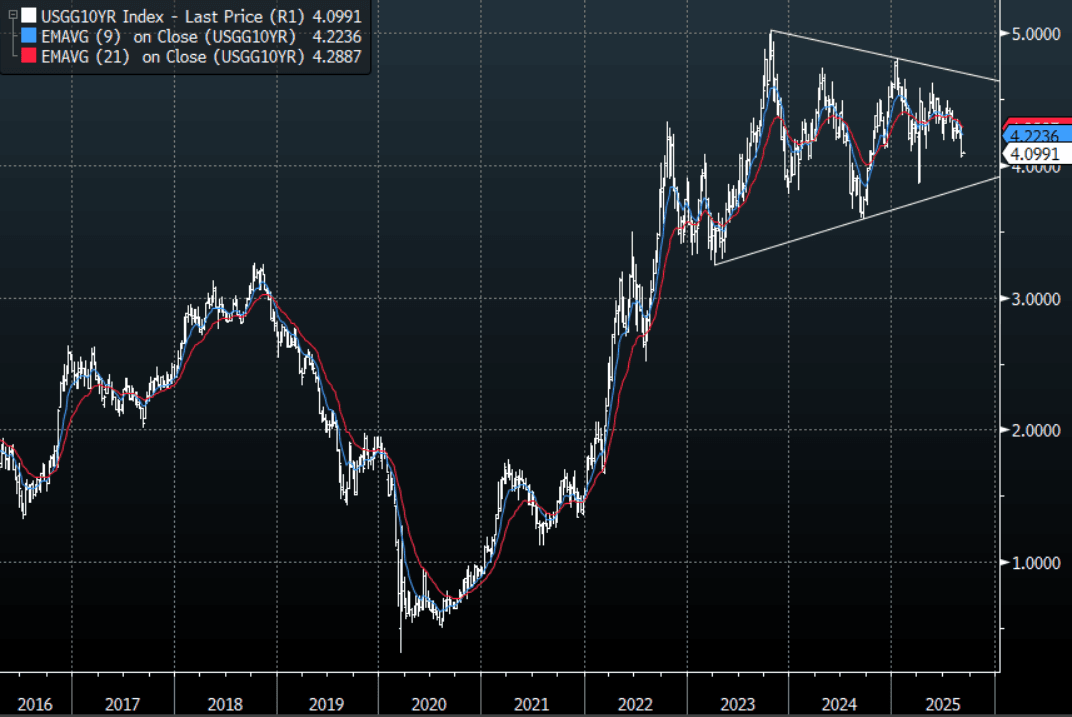

US TSYS: Asia Wrap - Yields Retrace A Little In Asia

The TYZ5 range has been 113-07+ to 113-14 during the Asia-Pacific session. It last changed hands at 113-08+, down 0-04 from the previous close.

- The US 2-year yield has edged higher trading around 3.526%, up 0.02 from its close.

- The US 10-year yield has edged lower trading around 4.099%, up 0.02 from its close.

- 10-Year Yields have broken through its support as the market reacts to a labour market that is rapidly cooling. This move should now see buyers return on bounces with the first buy-zone back towards 4.20%. First target the 4.00% zone then the 3.80% area.

- Zerohedge on X: “Morgan Stanley: We now expect quarterly rate cuts beginning in September for a terminal target range of 2.75-3.0% by end-2026.”

- (Bloomberg) - “Standard Chartered Sees Half-Point Fed Rate Cut This Month. Standard Charterer’s strategists see more aggressive easing, changing their previous call for a 25bp Fed interest-rate cut, following a weaker-than-expected payroll report Friday. “We think the August labor-market data has opened the door to a ‘catch-up’ 50bps rate cut at the September FOMC meeting, just as it did this time last year,” strategists John Davies and Steve Englander, write in a note.”

- Holger Zschaepitz on X: "The real surprise came in the revisions: BLS revealed that the US economy lost 13k jobs in June, marking the first monthly decline in employment since Dec2020. That also means the 53mth streak of continuous job growth ended in May; a major turning point for the US labor market.”

- Bob Elliott on X: “Labor market weakening needed to get the cuts so many want also means that growth is far weaker than what's currently priced in.”

- Data/Events: NY Fed 1-Yr Inflation Expectations, Consumer Credit

Fig 1: 10-Year US Yield Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Futures Off Friday Highs, Swap Rates Higher For 20-40 Yr

JGB futures sit at 137.98, +.02 versus settlement levels in latest dealings. We are away from Friday highs (138.37), but dips under 138.00 have been support so far today.

- Focus remains on who will be the new PM, after Ishiba decided to step down over the weekend. Local media report that the leadership election may be held on Oct 4 (per TBS via BBG). An official announcement is expected tomorrow. A number candidates are likely to put their names forward.

- When Ishiba secured the PM position last Oct, the runner up was Sanae Takaichi. Via ABC news: "A Nikkei survey held at the end of August put Ms Takaichi as the most "fitting" successor to Ishiba." Takaichi could arguably generate the most significant market reaction if she is successful becoming the new PM, as she has been outspoken in terms of being more dovish in terms of the BoJ outlook and looking to boost fiscal spending. Former Minister, Toshimitsu Motegi, will reportedly run.

- Earlier on the data front, we had Q2 GDP revisions, which were firmer than market expectations. Stronger private consumption offset weaker capital investment the data showed.

- The cash JGB 2/30s curve is steeper, but away from session highs (+245bps) We were last +243bps. The outright 10yr yield is little changed, last near 1.575%.

- In the swap space, the move in 20-40yr rates has been larger than the cash JGB yield move. The 30yr is up around 5bps, last near 2.52%.

- Tomorrow on the data front, we have August money stock figures and August machine tool orders.

JAPAN DATA: Q2 GDP Growth Revised Higher, Consumption Up, Capex Down

Japan Q2 GDP revisions were stronger than expected. Headline Q2 GDP rose 0.5%q/q, against a 0.3% expectation (which was the initial print). Nominal GDP rose 1.6%q/q, against a 1.3% forecast. The y/y deflator was unchanged though at 3.0%.

- In terms of the detail, private consumption growth was revised up to 0.4%q/q from 0.2%, but capex was revised to 0.6%q/q growth (from 1.3%). The inventory contribution was flat, versus an initial -0.3pt drag. Exports contribution was unchanged at 0.3%pt.

- It's also likely that public investment improved versus initial estimates. Our policy team noted last week: "Public investment is expected to be revised to flat on quarter from the initial -0.5%."

- The revisions are welcome from a broader growth standpoint. We have now had 5 consecutive quarters of growth (albeit with Q1 only marginally positive at 0.1%q/q).

- The authorities will be hoping that this trend is sustained, with near term focus on the tariff fallout. Its impact on profitability/capex is a BOJ watchpoint, with the next Tankan survey, out at the start of Oct, to help gauge impact.

AUSSIE BONDS: Futures Holding Firmer, But Away From Session Highs

Aussie bond futures hold positive but away from from best levels for the session. The 10yr future (XM) was last at 95.685, +5bps. Session highs rest at 95.70. 3yr futures (YM), were last 96.55 (+3.5bps). Session highs rest at 96.59. The slight softness in US TSY futures, with TY off -04+, maybe crimping Aussie bond futures gains at the margin.

- In the cash ACGB yield space, we are around 3-5bps weaker across the curve, led by the back end. The 3yr yield near 3.43%, off close to 4bps, while the 10yr is just under 4.29%, off close to 5bps.

- The ACGB 3/10s curve is just under +86bps, so like elsewhere, moving off recent highs.

- The AU-US 10yr differential sits off recent highs last around +20bps.

- Local news flow has been light, while the data focus this week will be on Tuesday survey/sentiment data. Tuesday sees September Westpac consumer confidence which rose each of the four months to August helped by lower rates and the prospects of further RBA easing. The NAB August business survey is also out on Tuesday. Business confidence has been trending higher since March and is positive again.

BONDS: NZGBS: Yields Lower, 2/10s Curve 8bps Flatter From Recent Highs

NZGB benchmark yields are holding lower across the benchmark, although the 2yr yield is a touch above opening lows. The 2yr yield was last near 2.93%, still down close to 3bps for the session. The 10yr is holding close to session lows, last near 4.33%, off nearly 6bps.

- The NZGB 2/10s curve has flattened further, last around +140bps. Highs from last week were close to +148bps.

- The NZ 2yr swap rate is around 2.74%, against earlier lows near 2.72%. This leaves late August lows still near-by.

- US Tsy yields have drifted a little higher in the first part of Monday dealings, but are still holding the bulk of Friday losses. The 10yr benchmark is still just under 4.10%.

- Local news flow has been light and while Q2 manufacturing activity prints tomorrow, it is unlikely to shift market sentiment. Q2 GDP prints on 18 of Sep.

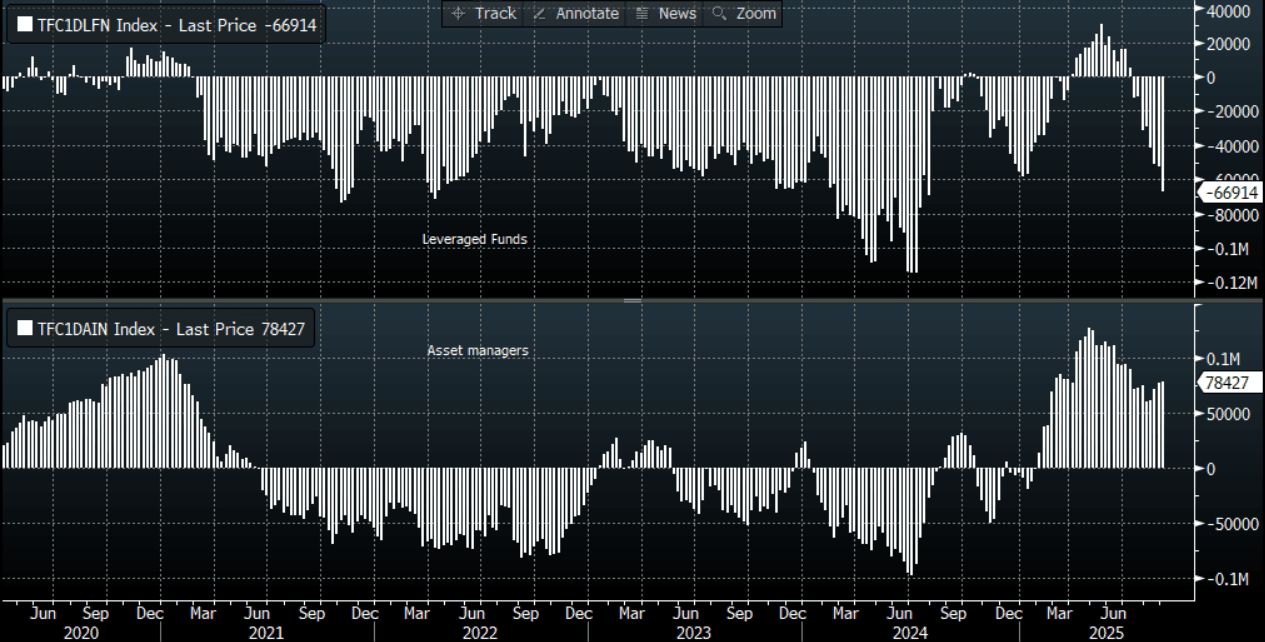

FOREX: Leveraged Contracts In Favor Of USD - Per CFTC

Last week's CFTC positioning update (for the week ending the 2nd of Sep) was notable on the leveraged side, where the skew was notably in favor of the USD, see the table below. JPY shorts were added to by 14.6k, while EUR and GBP net longs were cut back in the leveraged space. Indeed, for EUR, leveraged contracts are almost back to a net short position. AUD and CAD net selling by leveraged players was also evident, adding to existing shorts for both currencies.

- These shifts came ahead of the NFP print on Friday, which was weaker than expected, but didn't do material damage to the USD. The BBDXY index dipped under 1200, but rebounded and is slightly firmer in early Monday dealings. USD/JPY gains will be welcomed by the leveraged players (post PM Ishiba stepping down) who extended shorts in yen last week.

- Still, it is difficult to see a meaningful USD rebound as US yield differentials weaken against major currency blocs.

- In the asset manager space, positioning shifts were more modest. GBP shorts were added to, but AUD shorts were cut, along with those for CAD.

Table 1: CFTC Positioning Change & Outright Position By Major Currency

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | -14639 | -66914 | 1666 | 78427 |

| EUR | -6771 | 1817 | 2056 | 405115 |

| GBP | -6278 | 21300 | -5098 | -79948 |

| AUD | -5413 | -11860 | 12733 | -66025 |

| NZD | 510 | 285 | -384 | -5127 |

| CAD | -7985 | -46299 | 5712 | -64276 |

| CHF | 1343 | 1632 | -821 | -40327 |

| MXN | 6062 | 34591 | 2101 | 35343 |

Source: CFTC/Bloomberg Finance L.P/MNI

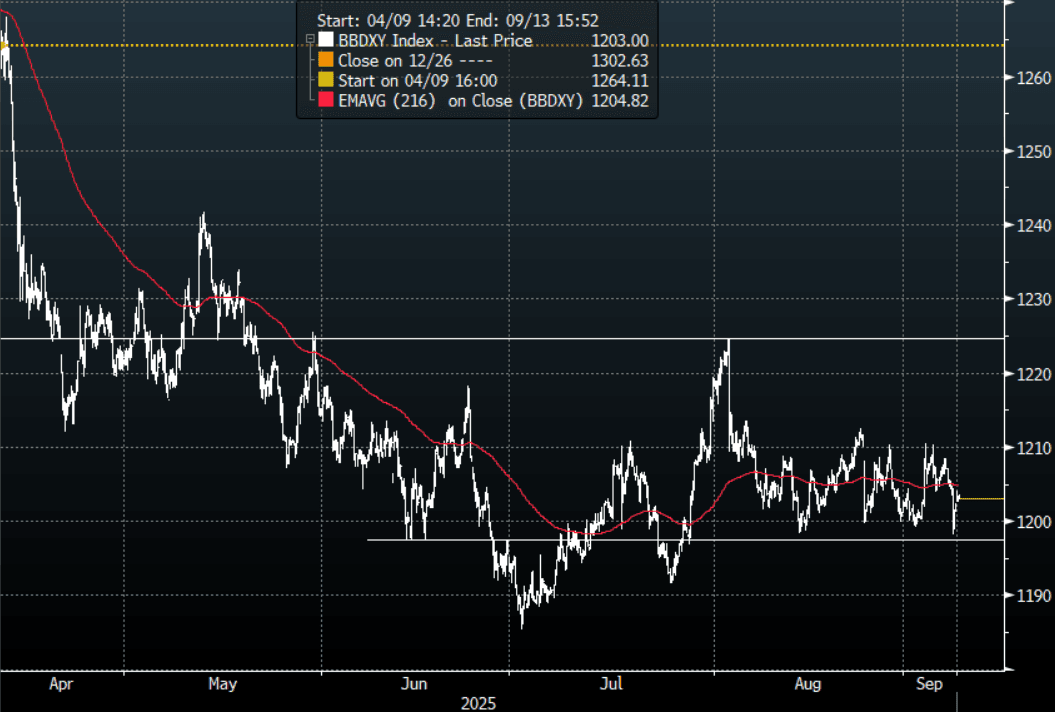

FOREX: Asia FX Wrap - The USD Support Continues To Hold For Now

The BBDXY has had a range of 1202.47 - 1204.11 in the Asia-Pac session, it is currently trading around 1203, +0.10%. The USD was again surprisingly able to shrug off the extension lower in US yields and found solid demand below 1200 helping it keep the support in place for now. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows.

- EUR/USD - Asian range 1.1704 - 1.1721, Asia is currently trading 1.1715. The pair bounced on Friday in response to the NFP but momentum stalled into the close. EUR trades firmly within its wider 1.1350-1.1850 range with a bias to the topside.

- GBP/USD - Asian range 1.3483 - 1.3506, Asia is currently dealing around 1.3495. The pair bounced strongly off its support around 1.3350 last week. The move above 1.3500 on NFP has stalled but price is now back in the middle of its 1.3350-1.3650 range. A sustained break below 1.3350 is needed to open up a move back to 1.3100.

- USD/CNH - Asian range 7.1244 - 7.1283, the USD/CNY fix printed 7.1029, Asia is currently dealing around 7.1325. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.10%, Gold $3581, US 10-Year 4.10%, BBDXY 1203, Crude Oil $62.58

- Data/Events : EZ Sentix Investor Confidence, Germany Industrial Production/Trade Balance

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY - Ishiba Gives Leveraged JPY Shorts A Reprieve

The Asia-Pac USD/JPY range has been 147.93-148.58, Asia is currently trading around 148.20, +0.50%. USD/JPY collapsed lower with US yields on Friday in reaction to the NFP, again challenging its support on a 146 handle. This support looked destined to be challenged to start this week but news of Ishiba stepping down has given the JPY bears another reprieve as the market has gapped higher on the open in response. CFTC data shows leveraged funds again added a decent clip to their short JPY position last week so this morning's move will have taken some pressure off them to start the week. Is this news enough to turn USD/JPY higher ? I suspect not but time will tell.

- MNI BRIEF: Japan Q2 GDP Revised Up On Consumption. Japan’s economy expanded faster in April-June than initially estimated, as stronger private consumption offset weaker capital investment, second preliminary GDP data from the Cabinet Office showed Monday.

- Focus will now turn to the LDP leadership race. When Ishiba secured the PM position last Oct, the runner up was Sanae Takaichi. Via ABC news: "A Nikkei survey held at the end of August put Ms Takaichi as the most "fitting" successor to Ishiba."

- Takaichi could arguably generate the most significant market reaction if she is successful becoming the new PM, as she has been outspoken in terms of being more dovish in terms of the BoJ outlook and looking to boost fiscal spending.

- "JAPAN LDP'S AIZAWA: WILL SET LEADERSHIP ELECTION DATE TUESDAY" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($1.1b), 149.00($882m), 145.75($792m).Upcoming Close Strikes : 145.75($1.12b Sept 11), 150.00($1.1b Sept 9) - BBG.

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +78427( Last +76761), leveraged funds though again used the dip to add a decent clip to their newly built short JPY position -66914(Last -52275). One of them is going to be wrong.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

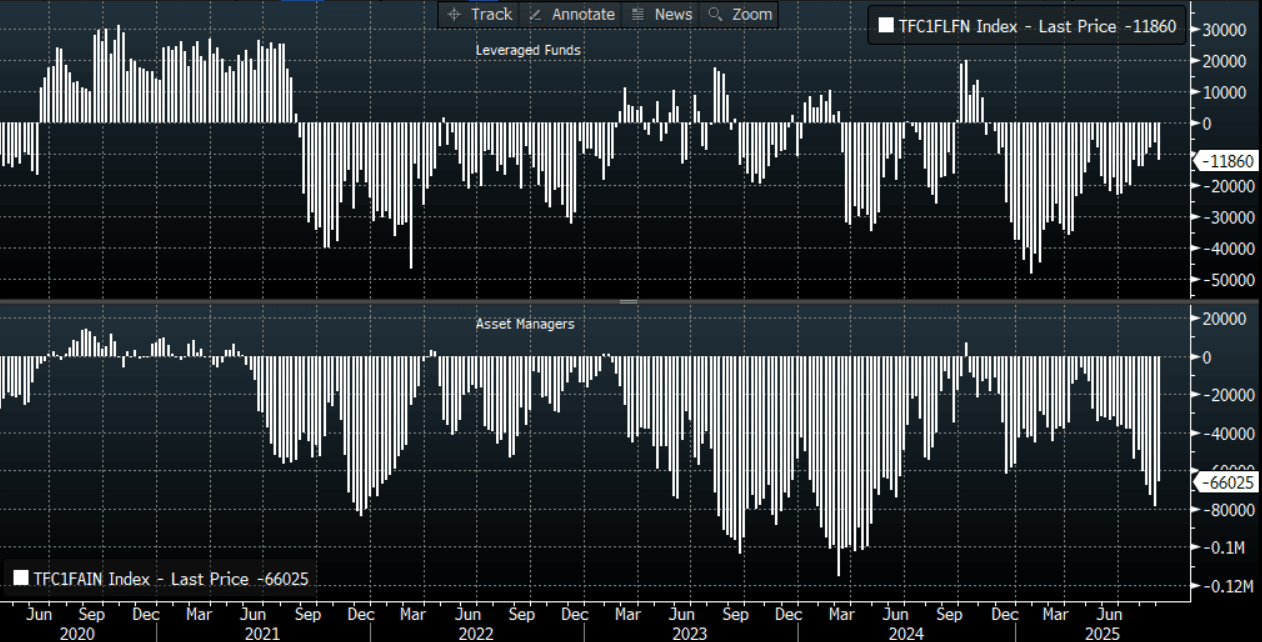

AUD/USD - Tries Higher On NFP, Move Stalls Ahead Of 0.6600

The AUD/USD has had a range of 0.6546 - 0.6568 in the Asia- Pac session, it is currently trading around 0.6560, +0.05%. The AUD tried to move higher initially on NFP but momentum failed and it spent the rest of the N/Y session trading heavy and drifting lower. The AUD remains in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction for now.

- Tuesday sees September Westpac consumer confidence which rose each of the four months to August helped by lower rates and the prospects of further RBA easing. At 98.5 last month, it is now approaching the neutral 100-level. The NAB August business survey is also out on Tuesday. Business confidence has been trending higher since March and is positive again. Conditions however remain soft, although June/July printed above the 2025 average. Employment and cost/price components will be monitored closely.

- MNI INTERVIEW: Fed To Cut Faster After Weaker Jobs - William English. "There's no doubt the labor market report was soft, and that causes them to lean in the direction of easier policy," he said in an interview Friday. "It leans in the direction of easing policy further, faster than maybe the Fed had been inclined to."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6475(AUD596m), 0.6500(AUD531m), 0.6625(AUD445m). Upcoming Close Strikes : 0.6650(AUD597m Sept 11) - BBG

- CFTC Data last week shows Asset managers reduced their shorts for the first time in a while -66025(Last -78758), the Leveraged community though look to be rebuilding their own shorts after winding them down -11860(Last -6447).

- AUD/JPY - Asia-Pac range 96.95 - 97.33, Asia is trading around 97.20.The pair looked to have topped out again after NFP, but this morning’s Ishiba news has thrown a spanner in the works. A sustained break above 97.50/98.00 is needed to reignite the upward trend.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

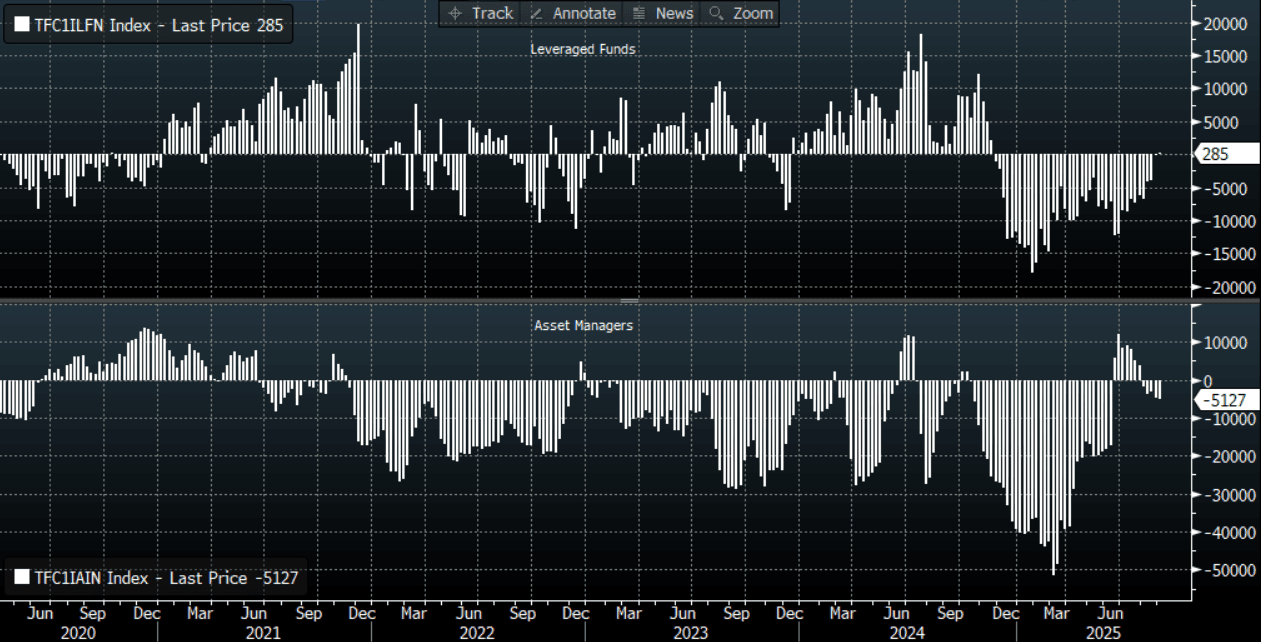

NZD: Asia Wrap - NZD/USD Consolidates Around 0.5900

The NZD/USD had a range of 0.5883 - 0.5904 in the Asia-Pac session, going into the London open trading around 0.5900, +0.12%. The NZD pushed higher in reaction to the NFP but found good selling above 0.5900 capping the move for now. This 0.5900-0.5950 area presents a good opportunity to fade for those who are bearish the NZD, but the caveat to this trade remains the USD’s ability to not break down. CFTC Data shows light positioning in a market that is struggling for a strong trend.

- Q2 manufacturing data print Tuesday including volumes. Manufacturing volumes rose 2.4% q/q in Q1. Q2 GDP prints on September 18, which the RBNZ expected to fall 0.3% q/q in its August projections.

- Bloomberg - “Dollar Vulnerability Turns to Downtrend on Payroll Miss. Further dollar weakness looks inevitable, with soft jobs data and falling rate expectations reinforcing the case for sustained downside. Together, easier Fed policy and the potential return of passive hedging flows create a feedback loop that makes sustained dollar strength increasingly difficult to justify.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5800(NZD515m Sept 10), 0.5870(NZD320m Sept 10) - BBG

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -5127(Last -4743), the Leveraged community have completely exited their short and have turned a fraction long +285(Last -225).

- AUD/NZD range for the session has been 1.1115 - 1.1133, currently trading 1.1120. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Strong Start to the Week for Regional Bourses

Japanese equities have greeted the political news positively with strong gains, post PM Ishiba's decision to step down as leader. This injects fresh political uncertainty into Japan's broader economic outlook. Focus will now turn to the LDP leadership race. When Ishiba secured the PM position last Oct, the runner up was Sanae Takaichi. Via ABC news: "A Nikkei survey held at the end of August put Ms Takaichi as the most "fitting" successor to Ishiba." Takaichi could arguably generate the most significant market reaction if she is successful becoming the new PM, as she has been outspoken in terms of being more dovish in terms of the BoJ outlook and looking to boost fiscal spending. Shenzhen's announcement that it will join Beijing and Shanghai in easing home-buying rules has given China's building shares a boost in Monday's trading.

- China's key bourses are all higher, with the exception of the CSI 300 which is flat. The Hang Seng is up +0.35%, Shanghai up +0.17% and Shenzhen up +0.45%.

- The Nikkei has started the week strongly with gains of +0.90%

- The TAIEX in Taiwan is higher by +0.45%

- The KOSPI's good run is continuing, up +0.17% today.

- The FTSE Malay KLCI was up only marginally in a shortened week last week and is higher by +0.48% today.

- The Jakarta Composite had a modest week last week, yet it up strongly today by +0.55%.

- The NIFTY 50 is up strongly Monday after key industries noted that the benefits from the GST cut will be passed onto consumers. The NIFTY 50 lags regional peers over the last three months as the sole index with falls yet starts this week off, up +0.32% to trade through key technical levels.

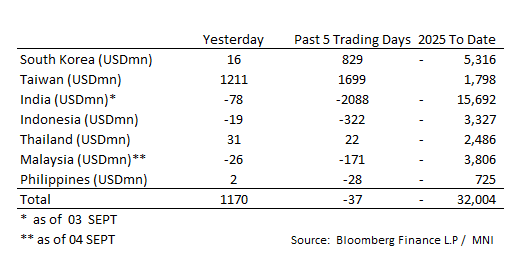

ASIA STOCKS: Equity Flow Update for Major Regional Bourses

Taiwan has had its largest inflow in a month.

- South Korea: Recorded inflows of +$16m as of Friday, bringing the 5-day total to +$829m. 2025 to date flows are -$5,316m. The 5-day average is +$166m, the 20-day average is -$13m and the 100-day average of +$62m.

- Taiwan: Had inflows of +$1,211m yesterday, with total inflows of +$1,699 m over the past 5 days. YTD flows are positive at +$1,798m. The 5-day average is +$340m, the 20-day average of -$139m and the 100-day average of +$209m.

- India: Had outflows of -$78m as of the 3rd, with total outflows of -$2,088m over the past 5 days. YTD flows are negative -$15,692m. The 5-day average is -$418m, the 20-day average of -$215m and the 100-day average of -$3m.

- Indonesia: Had outflows of -$19m as of the 3rd, with total outflows of -$322m over the prior five days. YTD flows are negative -$3,327m. The 5-day average is -$64m, the 20-day average +$21m and the 100-day average -$13m.

- Thailand: Recorded inflows of +$31m Friday, with inflows totaling +$22m over the past 5 days. YTD flows are negative at -$2,486m. The 5-day average is +$4m, the 20-day average of -$40m and the 100-day average of -$14m.

- Malaysia: Recorded outflows as of the 4th of -$26m, totaling -$171m over the past 5 days. YTD flows are negative at -$3,806m. The 5-day average is -$34m, the 20-day average of -$34m and the 100-day average of -$11m.

- Philippines: Recorded inflows of +$2m Friday, with net outflows of -$28m over the past 5 days. YTD flows are negative at -$725m. The 5-day average is -$6m, the 20-day average of -$5m the 100-day average of -$4m.

OIL: Crude Higher Following OPEC’s Cautious Output Increase

Oil prices fell sharply on Friday ahead of the weekend’s OPEC decision but given the cautious 137kbd increase in the output target from October, there appears to be a relief rally today. WTI is up 1.2% to $62.58/bbl after an earlier peak of $62.70 and Brent is 1.2% higher at $66.27/bbl after reaching $66.36. The USD index is slightly higher.

- The latest OPEC production increase is significantly less than previous +400kbd rises but the continued rise in the output target signals that it is now focussed on regaining market share. The oil market may have been reassured by its cautious tone though as it said it could withdraw earlier output hikes.

- However, OPEC could still unwind its earlier 1.66mbd reduction in its target, which was scheduled to be in place until end-2026, but it will depend on “evolving market conditions”. The group has added 2.2mbd over the last five months.

- The IEA has forecast a record market surplus for 2026, which has pressured oil prices. The EIA short-term energy outlook is published Tuesday with the IEA and OPEC monthly reports on Thursday.

- Later August NY Fed 1-yr inflation expectations, July US consumer credit and German July trade & IP print. The focus of the week will be on Tuesday’s US payroll benchmark revisions, Wednesday’s August PPI and Thursday’s August CPI.

GOLD: Bullion Holds Below Friday’s Record High

Gold reached a new record of $3600.16/oz on Friday following disappointing August US payrolls data. It has been unable to return to that level during Monday’s APAC session but has range traded between $3579.73 and $3597.26 and is currently down 0.1% to $3583.5 as the US dollar is marginally stronger and yields slightly higher. Non-interest bearing bullion has found support this month from growing Fed easing expectations.

- Fed independence remains in focus too with markets awaiting the legal ruling on whether President Trump can remove Governor Cook.

- Silver is underperforming falling 0.9% today to $40.64 after a low of $40.532. It spiked to $41.066 early in the session.

- Equities are generally stronger today with the S&P e-mini up 0.1%, Nikkei +1.3% and Hang Seng +0.4% but the CSI 300 is flat. Oil prices are higher with WTI +1.2% to $62.60/bbl. Copper is up 0.1%.

- Later August NY Fed 1-yr inflation expectations, July US consumer credit and German July trade & IP print. The focus of the week will be on Tuesday’s US payroll benchmark revisions, Wednesday’s August PPI and Thursday’s August CPI.

THAILAND: Markets Approve Of New Cabinet, Instability Looks Likely To Continue

The cabinet choices of new Thai PM Anutin, the third since 2023, have been met by relief. He appears to have chosen experience and continuity which is particularly important given that he promised to hold elections within four months to win the support of the People’s Party who hold the most number of seats in the House of Representatives. The SE Thai rose 1% on Friday and is +0.8% on Monday’s opening while USDTHB is down 1.2% since Tuesday. The THB NEER has remained elevated.

- Outgoing BoT Governor Sethaput warned that Thailand’s credit rating is at risk unless political uncertainty declines which would be needed to rein in fiscal policy. However, given opinion polls, political instability looks likely to continue.

- The latest NIDA poll taken at the end of June, after former PM Paetongtarn’s leaked call but before her suspension, showed that the People’s Party (formerly Move Forward) would gain 46.1% of the vote up from 2023’s 38%, while Paetongtarn’s Pheu Thai would win only 11.5% down from 28.8% followed by United Thai on 14.4% (2023 12.5%) and Anutin’s Bhumjaithai on 10.6% (3.0%).

- It was difficult forming a government after the 2023 election given the need for the senate’s approval which is controlled by the military. Also, Move Forward won the most seats on a platform of reform including of the constitution, the military in politics and the lese majeste law.

- A new Suan Dusit Poll reported that 68% of respondents want the new PM to focus on cost of living and 49% the Thai-Cambodian border dispute. 76.7% believed that elections should be held within four months. 59.2% in a Nida poll taken over 4-5 September said that parliament should be dissolved immediately. Around 59% in this survey were supportive of constitutional reform.

ASIA FX: THB & IDR Outperform, KRW Lags In Monday Trade

Asian currencies are mixed to start the week. THB and IDR have rallied, while the won has lost some ground (albeit remaining with recent ranges).

- USD/CNH has crept back above 7.1300 this afternoon. Earlier lows in the pair were at 7.1244 around the time of the USD/CNY fxing. The fix was set at a fresh low back to Nov last year, but didn't have a lasting impact on sentiment. August trade data was slightly below expectations. Exports rose 4.4%y/y (5.5% was forecast), while imports were up 1.3%y/y (3.4% was forecast). The trade surplus pushed back above $100bn. China equities are lagging the firmer tone seen elsewhere for much of the Asia Pac region, which may a CNH headwind at the margins.

- Spot USD/KRW is back around 1391 in latest dealings. We are off earlier highs close to 1394. Some negative spill over from the weaker yen is likely in play, while headlines have focused on the detained workers at the Hyundai/LG plant in the US. They are expected to be repatriated this week, after being detained as part of a US ICE investigation. Headlines crossed a short while ago from the South Korean FinMin - "S.KOREA FINMIN: WILL CONSULT WITH U.S. TO PREVENT INCIDENTS SIMILAR TO LAST WEEK'S IMMIGRATION RAID AT HYUNDAI PLANT FROM HAPPENING AGAIN", along with "S.KOREA FINMIN: FOREIGN EXCHANGE WILL BE INCLUDED IN TRADE DEAL ANNOUNCEMENT WITH U.S. - [RTRS]". The last comment around FX to be included in the trade agreement with the US has helped bring USD/KRW lower.

- THB has rallied, we were last close to 32.00 versus the USD. The cabinet choices of new Thai PM Anutin, the third since 2023, have been met by relief. He appears to have chosen experience and continuity which is particularly important given that he promised to hold elections within four months to win the support of the People’s Party who hold the most number of seats in the House of Representatives.

- The Rupiah is up strongly in Monday trading, approaching levels that the Central Bank is targeting (16300). We were last close to 16350, up around 0.40% in IDR terms.

- Moves elsewhere are move modest, with a bias towards USD weakness.

CHINA: Country Wrap: Exports Miss for August

Market Summary: Shenzhen's announcement that it will join Beijing and Shanghai in easing home-buying rules has given China's building shares a boost in Monday's trading. China's key bourses are all higher, with the exception of the CSI 300 which is flat. The Hang Seng is up +0.35%, Shanghai up +0.17% and Shenzhen up +0.45%. The Yuan Reference Rate at 7.1029 Per USD; Estimate 7.1323 and CGB 10-Yr is a touch higher at 1.78%.

- China's August exports missed expectations with growth of +4.4%, down from +7.2% in July. Imports were lower also, expanding just +1.3% following +4.1% in July. The export result was the weakest in six months with exports to the US cratering by over 30%. Shipments to the EU rose 10% and African 26%. With the monthly surplus at $102bn China's annual surplus could touch $1tn if this path is maintained (source MNI)

- The China Securities Journal reports that the likelihood of the PBOC resuming bond purchases is increasing.

INDONESIA: Country Wrap: Foreign Reserves Down in August

Market Summary: The Jakarta Composite had a modest week last week, yet it up strongly today by +0.55% and maintain it's position above all major moving averages. The Rupiah is up strongly in Monday trading, approaching levels that the Central Bank is targeting. Gains of +0.40% sees the IDR at 16,367, near to the 16,300 target set by BI. The gains see the rupiah nearing the 20-day EMA, which it hasn't traded below since late August. Bonds are rallying with the front end outperforming. The 10-Yr is lower by -4bp to 6.35%

- The Jakarta Globe reports that JPMorgan remains confident in the country's financial markets and the ability of the government to restore stability in the face of public unrest.

- Indonesia’s foreign reserves fell to $150.7b in August (from $152bn in July), the lowest since November, due to government external debt payments and rupiah stabilization measures by the central bank, according to a statement on Monday by the Bank Indonesia

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 08/09/2025 | 0600/0800 | ** | Trade Balance | |

| 08/09/2025 | 0600/0800 | ** | Industrial Production | |

| 08/09/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 08/09/2025 | 1900/1500 | * | Consumer Credit | |

| 09/09/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 09/09/2025 | 0645/0845 | * | Industrial Production | |

| 09/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/09/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 09/09/2025 | 1150/1350 | SNB's Schlegel at BIS fireside chat | ||

| 09/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index |