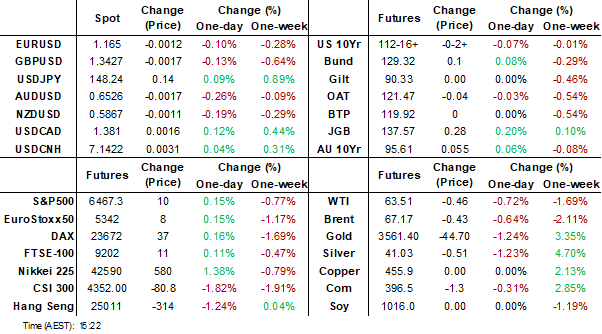

MNI EUROPEAN MARKETS ANALYSIS: JGBs Up Post Solid 30yr Auction

Sep-04 05:23By: Jonathan Cavenagh

Europe

- Regional bond markets have mostly tracked lower in yield terms. A resilient 30yr debt auction in Japan aided JGB futures. Curves are mostly flatter following US trends from Wednesday.

- The USD is up a touch, while China equities have seen sharper losses, unwinding some of the recent strong gains.

- Australia household spending painted a resilient consumption backdrop for July.

MARKETS

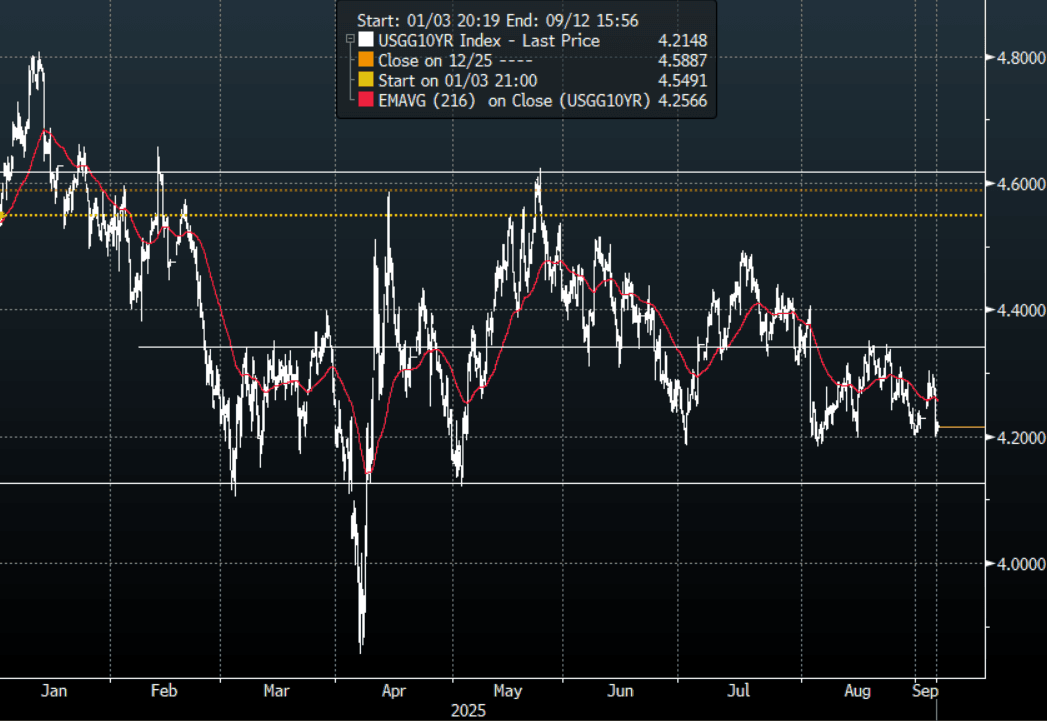

US TSYS: Yields Mixed In a Quiet Session

The TYZ5 range has been 112-16 to 112-19 during the Asia-Pacific session. It last changed hands at 112-18, down 0-01+ from the previous close.

- The US 2-year yield has edged lower trading around 3.61%, down 0.01 from its close.

- The US 10-year yield has is trading around 4.215%.

- 10-Year Yields rejected the 4.30% area on a softer JOLTS report and has moved very quickly back to the 4.20% area. NFP will now take on big significance, a break of the 4.18% support would turn the focus back to 4.10%.

- Bloomberg - “Fed Governor Christopher Waller said the US central bank should begin lowering interest rates this month and make multiple cuts in the coming months, adding that officials could debate the precise pace of reductions.”

- zerohedge on X: "Labor Market Crosses Critical Threshold: For First Time Since 2021 There Are More Unemployed Than Job Openings. Why does this matter? Because the US has never entered a recession when it was labor supply constrained. As of this moment it is no longer supply constrained."

- Robin Brook on X: “Two things are driving the rise in long-term bond yields: (i) much of the G10 has big deficits and debt near 100%; (ii) long-term yields have been kept artificially low by central banks. Best example of the latter is Japan, where 30-year yield is same as Germany. That's bonkers.”

- Data/Events: Challenger Job Cuts, ADP, Initial Jobless Claims, Trade Balance, S&P PMI’s, ISM Services

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: 30yr Yield Down Post Auction, Labour Earnings Data Tomorrow

Futures sit at 137.55, +.26 versus settlement levels. Post lunch break highs were at 137.65. This was close to highs seen at the start of Sep. US tsy futures hold a touch weaker, but have had a quiet session, while cash Tsy yields are down a touch.

- The 30yr debt auction was not as bad as feared from a demand standpoint. The bid to cover ratio was 3.31, versus a 12mth average of 3.38 (per BBG). The tail for the auction was 0.18, versus the early August result of 0.15.

- Cash JGB yields are down led by the back end of the curve. The 30yr last off 4bps to be back near 3.26%. The 10yr is back to 1.615%, off close to 1.5bps. The JGBs 2/30s curve sits a touch flatter at +241bps.

- Earlier headlines crossed, notably: "*HAYASHI: NOT TRUE GOVT DECIDED TO COMPILE ECONOMIC MEASURES" - BBG and *HAYASHI: MANAGE IN WAY THAT AVOIDS SUDDEN RISE IN L-T RATES" - BBG. Extra stimulus/household support remains a focus point, particularly given budget requests for the upcoming financial year are pressured by debt repayments and higher defence spending.

- Also note: "*BOJ TO HOLD MEETING ON MARKET OPERATIONS ON OCT. 16" - BBG.

- Note tomorrow we get July labour cash earnings. Nominal earnings are forecast to rise 3.0%y/y, versus 3.1% in June. Real earnings are expected at -0.6%y/y, which would be an improvement on the June -0.8%y/y outcome.

JAPAN DATA: Japan Offshore Bond Purchases Pick-Up

The highlight of Japan offshore investment flows, in the week ending Aug 29, was the surge in buying of overseas bonds. Just over ¥1.4trln in bonds were purchased, the largest flow into this segment since mid July. This ends a run of modest net selling of offshore bonds by local investors through much of late July/first part of August. Cumulative flows have been strong since May of this year. Global bond returns picked up through late August, but remained sub earlier 2025 highs.

- Japan investors also purchased offshore equities, but trends in this space have been mixed, with 3 out of the last 5 weeks still recording net selling.

- In terms of inflows into Japan assets, we saw net selling by offshore investors of local stocks for the 2nd straight week. This follows a basically un-interrupted run of inflows back to April of this year. Japan stocks have struggled since making fresh record highs in mid August.

- On the bond side, offshore investors were modest net buyers of local bonds.

Table 1: Japan Offshore Weekly Investment Flows

| Billion Yen | Week ending Aug 29 | Prior Week |

| Foreign Buying Japan Stocks | -785.7 | -496.2 |

| Foreign Buying Japan Bonds | 397.4 | -105.8 |

| Japan Buying Foreign Bonds | 1419.8 | -167.2 |

| Japan Buying Foreign Stocks | 481.8 | -306.1 |

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Yields Correct Lower, Household Spending Remains Firm In July

Aussie bond futures are holding gains. The 3yr (YM) last at 96.49.5, just off session highs, while the 10yr (XM) was at 95.61, +5.5bps. Session highs for this benchmark were at 95.62. The cash ACGB curve is 3-6.5bps lower across the benchmarks and like elsewhere has been led by the back end, as curves flatten. The ACGB 3/10s curve is a touch flatter, at +88bps.

- The 3yr yield sits around 3.48%, after testing multi month highs yesterday (around 3.55%). The combination of better than expected Q2 GDP and some hawkish RBA remarks from Governor Bullock yesterday, aided these moves. The 10yr yield was last close to 4.36%.

- An RBA cut remains close to fully priced for the Nov meeting outcome.

- Data today showed July household spending was close to market forecasts. We rose 0.5%m/m, in line with the consensus, although June was revised down a touch to 0.3%, (from 0.5% originally reported). Y/Y spending was still a touch firmer though at 5.1%, versus 5.0% forecast and 4.6% prior. This follows

- Other data for July trade showed the trade surplus at over A$7bn due to weaker imports (off 1.3%m/m), while exports held up at +3.3%m/m. Softer imports reflected a modest decline in consumer related goods (so some caution around the better household spending story).

- We still await details of RBA Deputy Governor's interview with Reuters.

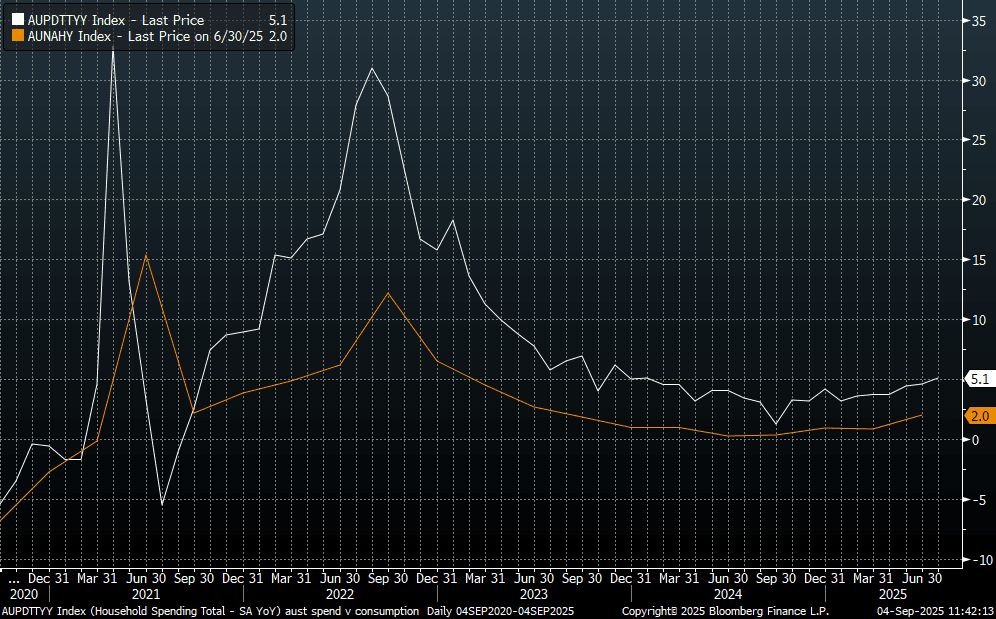

AUSTRALIA DATA: Household Spending +5%y/y, Trade Surplus Up On Lower Imports

Australia July household spending was close to market forecasts. We rose 0.5%m/m, in line with the consensus, although June was revised down a touch to 0.3%, (from 0.5% originally reported). Y/Y spending was still a touch firmer though at 5.1%, versus 5.0% forecast and 4.6% prior.

- The chart below plots the household spending measure against consumption growth (from the national accounts), with both measures in y/y terms. The continued trend improvement in y/y household spending points to further gains in aggregate consumption growth (all else equal).

- The standouts in the month were health spending, +1.8%m/m, along with spending on hotels, cafes and restaurants (+1.4%m/m). Weakness was seen in household equipment and clothing (both down over 1% m/m).

- The ABS noted: "‘In contrast, Goods spending fell 0.3 per cent after mid-year sales boosted spending by 0.9 per cent in June.’"

- Other data for July trade showed the trade surplus at over A$7bn due to weaker imports (off 1.3%m/m), while exports held up at +3.3%m/m. Softer imports reflected a modest decline in consumer related goods (so some caution around the better household spending story).

Fig 1: Australian Household Spending & Consumption Growth Y/Y

Source: Bloomberg Finance L.P./MNI

BONDS: NZGBS: Flatter Curve In Line With Global Moves

NZGB yields sit 3-6bps weaker across the benchmarks, led by the back end. The 2yr remains under 3% last around 2.95% (off 3bps). The 10yr was back close to 4.40%, off nearly 6bps. Markets gaped lower around the open, in yield terms, and price action since then has been fairly muted. The NZ 2/10s curve is slightly flatter at +145bps. These moves largely reflect offshore developments from Wednesday.

- The 2yr swap rate is around 2.75%, off a little over 2bps. Recent lows rest at 2.706%, from late August.

- On the data front, we had Q2 volume of all building work print earlier. This fell 1.8%q/q, against a -1.0% forecast. Q2 was revised higher to a +1.3% gain though, after initially being reported as flat.

- We get more Q2 activity data next week, with manufacturing figures due on Tuesday. Q2 GDP isn't out though until Sep 18.

- Via BBG: "New Zealand sold NZ$225 million ($132.2 million) of bonds due May 15, 2035 on Sept. 4 (bid to cover was 2.96), also " New Zealand sold NZ$225 million ($132.2 million) of bonds due May 15, 2030 on Sept. 4." via BBG (bid to cover was 4.38).

- Tomorrow the data calendar is empty.

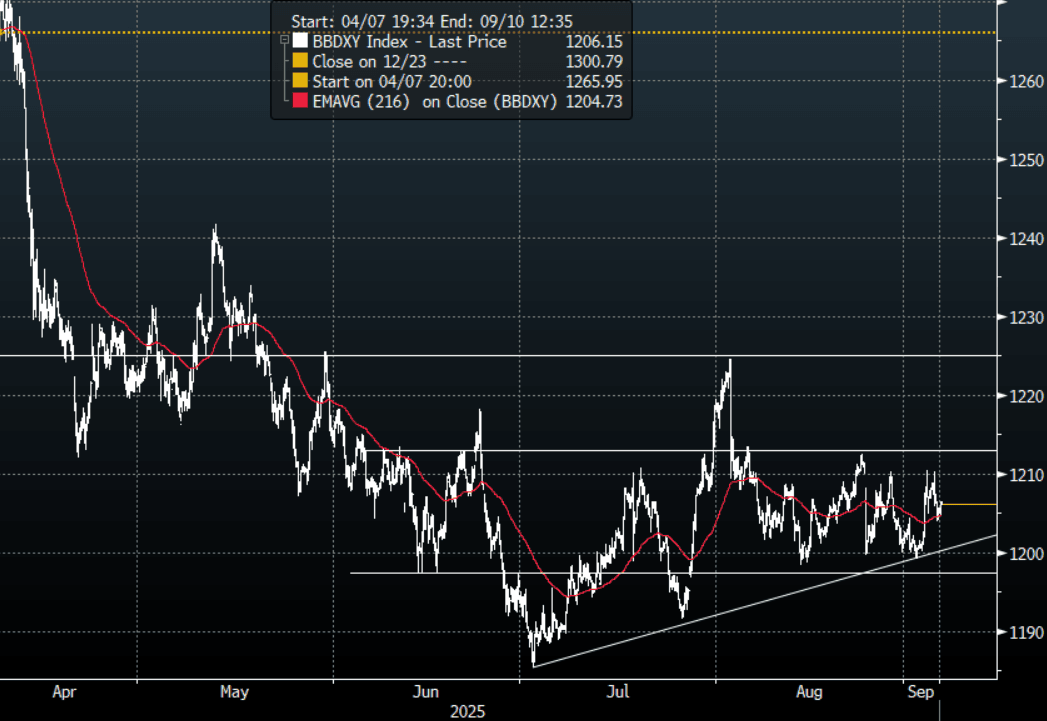

FOREX: Asia Wrap - USD Stabilised After Overnight Fall

The BBDXY has had a range of 1204.59 - 1206.37 in the Asia-Pac session, it is currently trading around 1206, +0.07%. The USD topped out above 1210 and reversed lower with US yields in response to a softer JOLTS report. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. The USD is looking comfortable for the moment above this support, not sure we get any clear direction though until the market sees what the NFP print is.

- EUR/USD - Asian range 1.1651 - 1.1669, Asia is currently trading 1.1655. The pair is drifting back towards its first support around 1.1550, firmly within its wider 1.1350-1.1850 range.

- GBP/USD - Asian range 1.3426 - 1.3450, Asia is currently dealing around 1.3430. The pair collapsed in response to moves in UK bonds. Price bounced off its support around 1.3350, though I suspect offers should now find supply on rallies back towards 1.3500. A sustained break below 1.3350 would open up a move back to 1.3100.

- USD/CNH - Asian range 7.1362 - 7.1450, the USD/CNY fix printed 7.1052, Asia is currently dealing around 7.1420. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3530, US 10-Year 4.217%, BBDXY 1206, Crude Oil $63.52

- Data/Events : EZ Retails Sales, Germany HCOB Construction PMI

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

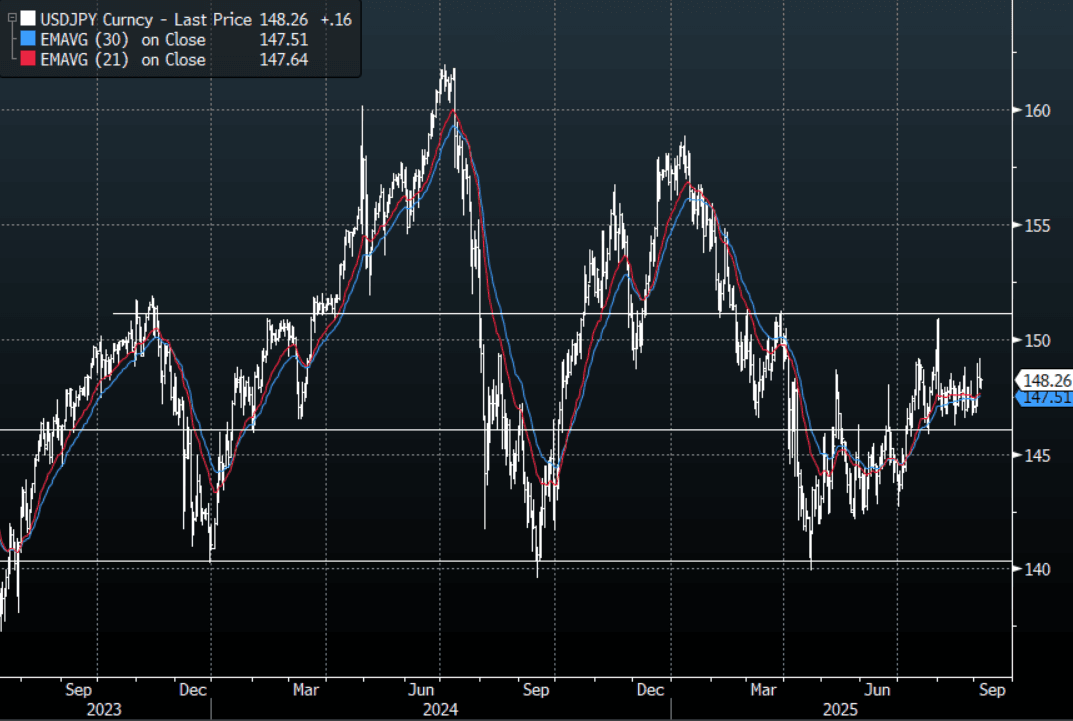

JPY: Asia Wrap - USD/JPY Consolidates Around 148.00

The Asia-Pac USD/JPY range has been 147.80-148.28, Asia is currently trading around 148.25, +0.10%. USD/JPY again rejected the 149.00 area overnight, helped by a softer JOLTS report which saw US yields move quickly lower. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. The price action looks pretty constructive but I would not be expecting any major extensions until the market has had a look at the NFP on Friday, which given the reaction to JOLTS could be a key driver.

- MNI POLICY: Risk Of Weaker Inflation Expectations Concern BOJ. BOJ Officials are monitoring risks that households inflation expectations could weaken as food-price rises ease and some firms lower retail prices, MNI understands, though high living costs and wage hikes are still seen as supporting underlying inflation.

- The 30yr debt auction was not as bad as feared from a demand standpoint. The bid to cover ratio was 3.31, versus a 12mth average of 3.38 (per BBG). The tail for the auction was 0.18, versus the early August result of 0.15.

- "JAPAN TRADE NEGOTIATOR AKAZAWA: WILL CONTINUE TO PUSH FOR PRESIDENTIAL ORDER FOR WHAT HAS BEEN AGREED ON TARIFFS, ISHIBA ADMINISTRATION SHOULD CONTINUE TO CARRY OUT IMMINENT TASKS, NO NEED FOR EARLY LDP LEADERSHIP ELECTION - [RTRS]"

- "HAYASHI: TO MANAGE ECONOMY, FINANCES ENSURING MKT CONFIDENCE, MANAGE IN WAY THAT AVOIDS SUDDEN RISE IN L-T RATES" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.10($970m), 146.50($673m).Upcoming Close Strikes : 146.00($2.16b Sept 5), 147.00($1.09b Sept 5), 146.00($103b Sept 8 ) - BBG.

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +76761( Last +71379), leveraged funds though again used the dip to add slightly to their newly built short JPY position -52275(Last -50848). One of them is going to be wrong.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

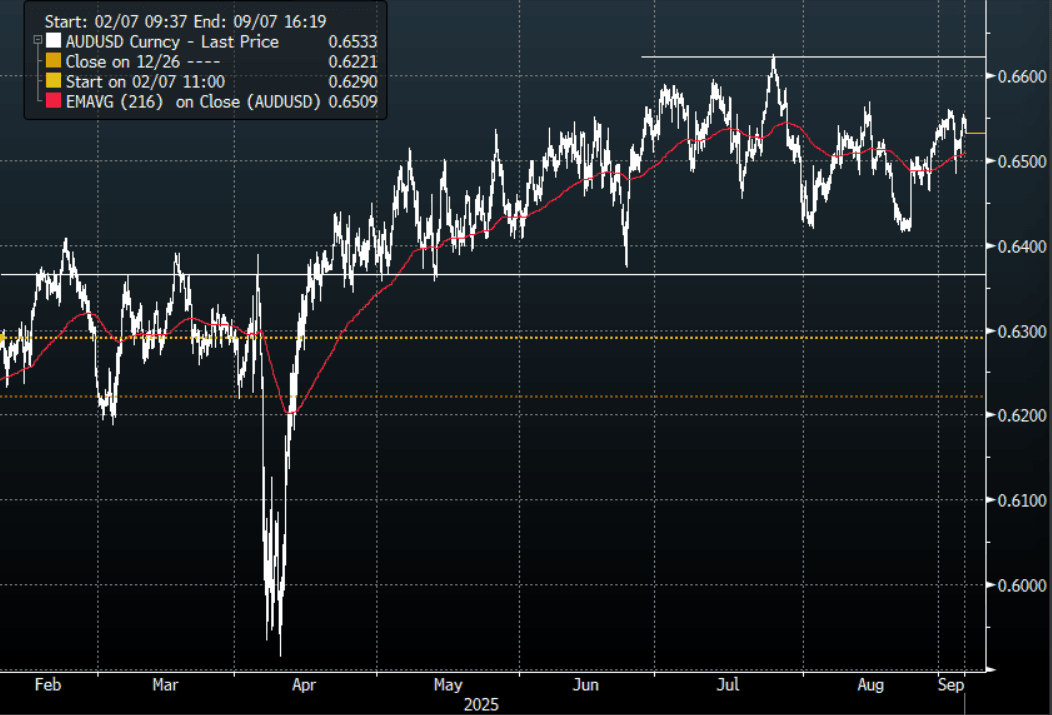

AUD: Asia Wrap - AUD/USD Drifts Lower As China Looks To Curb Speculation

The AUD/USD has had a range of 0.6534 - 0.6550 in the Asia- Pac session, it is currently trading around 0.6535, -0.15%. The AUD has drifted lower as Chinese authorities contemplate options to rein in speculative trading. The AUD remains in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction. The market will be looking towards NFP at the end of the week to hopefully be a catalyst.

- “Chinese Authorities are contemplating options to rein in speculative trading on concern a sharp reversal might inflict heavy losses on retail investors." - BBG

- Household Spending +5%y/y, Trade Surplus Up On Lower Imports: Australia July household spending was close to market forecasts. We rose 0.5%m/m, in line with the consensus, although June was revised down a touch to 0.3%, (from 0.5% originally reported). Y/Y spending was still a touch firmer though at 5.1%, versus 5.0% forecast and 4.6% prior.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6445(AUD945m), 0.6595(AUD867m), 0.6600(AUD967m). Upcoming Close Strikes : 0.6400(AUD1.12b Sept 5), 0.6500(AUD1.08b Sept 5), 0.6600(AUD1.02b Sept 5) - BBG

- CFTC Data last week shows Asset managers continue to add to their shorts -78758(Last -72904), the Leveraged community though again reduced their own shorts -6447(Last -7818).

- AUD/JPY - Asia-Pac range 96.75 - 97.01, Asia is trading around 96.85. The pair has broken back above 96.50 which starts to negate the downward direction, a sustained break above 97.50 is needed to reignite the upward trend. Until then looks to be 94.50 - 97.50.

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

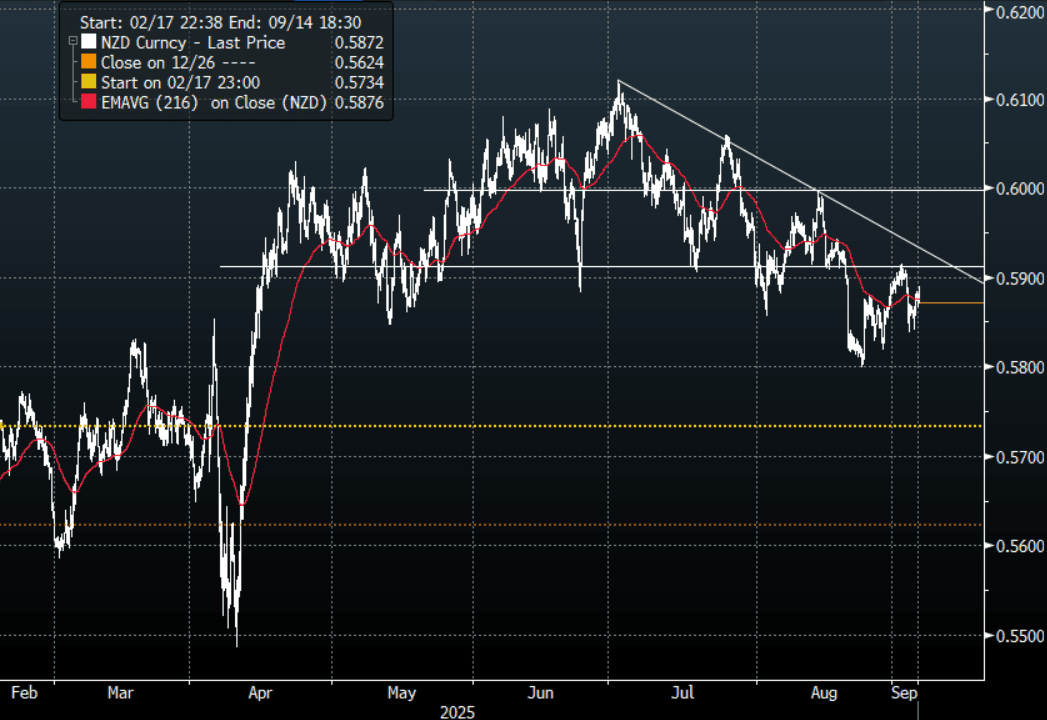

NZD: Asia Wrap - NZD/USD Drifts Lower

The NZD/USD had a range of 0.5867 - 0.5890 in the Asia-Pac session, going into the London open trading around 0.5875, -0.10%. The NZD found some demand again just under 0.5850 overnight and bounced higher from there as the USD got sold in response to the softer JOLTS data. The NZD sellers should continue to be around looking to fade any bounce back towards the 0.5950 area initially, NFP’s will be an important input.

- "NZ 2Q CONSTRUCTION WORK FALLS 1.8% Q/Q; EST. -1.0%, NZ 2Q RESIDENTIAL CONSTRUCTION FALLS 2.9% Q/Q, NZ 2Q NON-RESIDENTIAL CONSTRUCTION FALLS 0.4% Q/Q" -BBG

- “Chinese Authorities are contemplating options to rein in speculative trading on concern a sharp reversal might inflict heavy losses on retail investors." - BBG

- "RBNZ GOVERNOR CHRISTIAN HAWKESBY WILL SPEAK ON SEPT. 11": The Governor will discuss the August Monetary Policy Statement (MPS) and the Capital Review consultation which opened on 25 August. No new information will be provided regarding economic conditions or the August MPS. The remarks will be followed by a question and answer session with conference attendees. - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none - BBG

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -4743(Last -3198), the Leveraged community have almost completely exited their short -225(Last -4004).

- AUD/NZD range for the session has been 1.1116 - 1.1139, currently trading 1.1125. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now.

Fig 1: NZD/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China's Markets Lead the Decline

China equity benchmarks were lower for the third straight session as BBG reported that potential measures were being considered to curb market sentiment. "The measures proposed to top policymakers in recent weeks include the removal of some short selling curbs. Authorities are also contemplating options to rein in speculative trading on concern a sharp reversal might inflict heavy losses on retail investors." (per BBG). Fear has been growing among investors that Chinese regulators will intervene to rein in the excessive stock gains, with measures including acceleration of new stock supply, restrictions on margin accounts and selling of large stakes held by state buyers.

- The Hang Seng is down -1.21% today, the CSI 300 down -2.47%, Shanghai Comp -1.97% and Shenzhen down -1.55% as returns over the last five trading days turn negative.

- The NIKKEI recovered from yesterday's falls and is up +1.45% today

- The TAIEX in Taiwan is up for a second successive day, by +0.55%

- The KOSPI has delivered three days of gains for the first time in a month, up +0.15% today.

- The FTSE Malay KLCI has done very little ahead of the central bank later, down -0.09%.

- The Jakarta Composite is lower by -0.21% as markets appear to be calmer than earlier in the week.

- The NIFTY 50 is up for a third day, by +0.15%. After a week start Monday, the gains have seen it edge over into positive territory week to date.

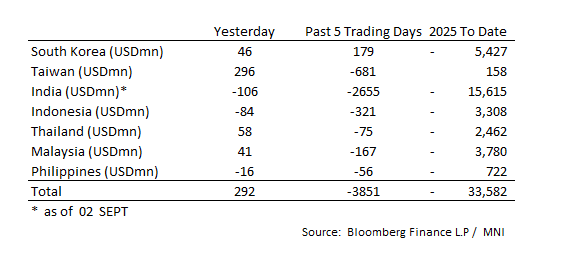

ASIA STOCKS: Equity Flow Update for Major Regional Bourses

Outflows from India continue, as Taiwan has another day of inflows.

- South Korea: Recorded inflows of +$46m yesterday, bringing the 5-day total to +$179m. 2025 to date flows are -$5,427. The 5-day average is +$36m, the 20-day average is -$25m and the 100-day average of +$59m.

- Taiwan: Had inflows of +$296m yesterday, with total outflows of -$681 m over the past 5 days. YTD flows are positive at +$158. The 5-day average is -$136m, the 20-day average of -$145m and the 100-day average of +$185m.

- India: Had outflows of -$106m as of the 2nd, with total outflows of -$2,655m over the past 5 days. YTD flows are negative -$15,615m. The 5-day average is -$531m, the 20-day average of -$222m and the 100-day average of -$12m.

- Indonesia: Had outflows of -$84m yesterday, with total outflows of -$321m over the prior five days. YTD flows are negative -$3,308m. The 5-day average is -$64m, the 20-day average +$24m and the 100-day average -$13m.

- Thailand: Recorded inflows of +$58m yesterday, with outflows totaling -$75m over the past 5 days. YTD flows are negative at -$2,462m. The 5-day average is -$15m, the 20-day average of -$32m and the 100-day average of -$13m.

- Malaysia: Recorded inflows yesterday of +$41m, totaling -$167m over the past 5 days. YTD flows are negative at -$3,780m. The 5-day average is -$33m, the 20-day average of -$35m and the 100-day average of -$10m.

- Philippines: Recorded outflows of -$16m yesterday, with net outflows of -$56m over the past 5 days. YTD flows are negative at -$722m. The 5-day average is -$11m, the 20-day average of -$5m the 100-day average of -$5m.

- Oil declined further in the Asia trading day, after heavy falls overnight on supply concerns

- At an upcoming meeting this weekend, OPEC+ is set to consider options for production and according to some, could be set for a further increase in capacity.

- Already they have approved the increase of 2.5mn barrels a day back in April, a previous supply increase that had been paused.

- In August alone, an additional 400,000 bbls a day was released with the majority coming from Saudi output.

- Production data from Canada showed that Alberta's oil production rose to a record 4.32 million barrels a day in July as oil sands companies boosted output from well sites to fill the expanded Trans Mountain pipeline.

- Asia has increased US crude buying due to cheaper prices and a desire for favor with President Donald Trump. South Korea, Japan, and India have boosted their US crude purchases, with South Korea almost doubling its purchased oil volumes for November.

- An industry estimate showed that crude inventories at the Cushing, Oklahoma, storage hub expanded by 2.1 million barrels last week, which would be the biggest increase since March if confirmed by official data.

- Goldman Sachs Group Inc. reaffirmed a bearish outlook, citing expectations for output to top consumption, with a forecast for Brent to drop to the low $50s in late 2026 (per BBG)

- WTI fell -0.70% today to US$63.52 bbl, following yesterday's large falls.

- Brent fell further also today, down -0.65% to US$67.16 bbl.

Gold Backs off from All Time Highs

- Following yesterday's rally which saw a new all time high close of US$3,559.42, gold finally snapped it's seven day rally in the Asia trading day.

- Down -0.82% despite China's major equity markets falling, suggests that profit taking could be the driver for the daily declines.

- Gold had rallied over 3% in the first few days of the month, before today's declines.

- Up over 35% this year points to a structural shift in demand for gold as Central Banks such as the PBOC diversify their reserves away from the US, whilst increasing their allocation to bullion.

- Goldman Sach's research suggest that if the Federal Reserve's independence was challenged, gold could touch US$5,000.

- Last night during the US trading day, weaker than expected data gave gold a boost on hopes of an upcoming rate cut.

- As the week ends with Non-Farm payrolls, gold investors will be watching closely as a guide for the next move from the Fed.

CHINA: Country Wrap: New Consumption Boosting Policies Come into Effect

- China's subsidized personal consumption loan policy came into effect on Monday, with multiple banks racing to roll out the measures as part of the government's broader push to spur domestic spending. The plan, unveiled on Aug 12, marks the first time the central government has offered interest subsidies for qualifying personal consumption loans. The program runs from Sept 1, 2025 to Aug 31, 2026, and applies to the portion of personal consumption loans — excluding credit card borrowing — used directly for consumption which is verifiable through borrowers' transaction records via loan disbursement accounts. (source China Daily)

- Foreign investors are increasing their investment in Chinese assets, buoyed by optimism. The latest data from the China Securities Regulatory Commission (CSRC) shows that by the end of July, the number of qualified foreign institutional investors (QFIIs) had reached 900, with 40 new additions this year. The CSRC stated that it will introduce further reform measures to optimize the QFII system, effectively promoting high-level institutional opening of the capital market. Market analysts believe that the policy signals revealed at the recent symposium of experts and scholars on the 15th Five-Year Plan for the Capital Market held by the China Securities Regulatory Commission (CSRC) indicate that a new round of capital market reform and opening-up is expected to accelerate. Further improvements to cross-border investment and financing facilities, as well as optimization of market access management and investment operations, are highly anticipated. Foreign institutions are expected to cast a greater vote of confidence in the Chinese market. (source China Securities)

- The Hang Seng is down -1.21% today, the CSI 300 down -2.47%, Shanghai Comp -1.97% and Shenzhen down -1.55% as returns over the last five trading days turn negative.

- Yuan Reference Rate at 7.1052 Per USD; Estimate 7.1405

- Bonds are stronger today with the 10-Yr down at 1.74%

INDONESIA: Country Wrap: Government Data Challenged Again

- Indonesia's central bank said it had agreed on a "burden sharing" arrangement with the government where it will raise the interest rates it pays on government deposits as a way to help the government fund its programmes. In a statement on Thursday, a Bank Indonesia spokesperson said the arrangement was intended to help the government cover the cost of raising funds through the bond market for programmes such as affordable housing and setting up cooperatives in villages. (source Reuters)

- An analyst urged Wednesday that the government should be transparent with the economic data that they publish, saying that inaccuracy can diminish public trust. "The government has to provide accurate data, not cover it up with misleading and manipulated information," Nailul Huda, a director at the think-tank Celios, told a talkshow broadcasted on Beritasatu TV on Wednesday. Nailul looked back on when the statistics bureau BPS reported that Indonesia's economy had grown 5.12 percent year-on-year (yoy) in the second quarter. Economists at the time had even questioned its credibility. Nailul told BeritaSatu TV that the situation on the ground showed that people were struggling to find jobs. Food prices also soared, not to mention the declining purchasing power, thus a stark contrast to the growth that had beat analysts' expectations. (source Jakarta Globe)

- The Jakarta Composite is lower by -0.21% as markets appear to be calmer than earlier in the week.

- USDIDR is weaker by -0.15% today at 16,442, having closed last night at 16,416. Early this week, the BI Governor confirmed that Central Bank had been in markets to stabilize the rupiah with a target level of 16,300.

- Government bonds are doing very little with the 10-Yr at 6.39%.

ASIA FX: USD/KRW Recoups Wednesday Losses, USD/CNH Above 7.1400

In North East Asia FX, won weakness is the standout in the first part of Thursday trade. CNH and HKD are little changed, while TWD is up modestly.

- For USD/CNH we are holding above 7.1400 in latest dealings. The USD/CNY fixing moved lower but remains just above 2025 to date lows. Some USD gains emerged after onshore equities faltered notable. The CSI 300 is off close to 2.5%, with BBG reporting that the authorities are considering measures to calm market sentiment.

- Spot USD/KRW has recouped yesterday's losses. The pair back around 1394 in latest dealings, up +0.30% for the session. Local equities are up a touch, but the Kospi remains sub 3200. Rtrs reported: "SOUTH KOREA VICE FIN MIN: CLOSELY MONITORING FX MARKETS, WILL ACT TO STABILIZE FX MARKETS IF NEEDED, SOUTH KOREA VICE FIN MIN: DISCUSSING FX WITH THE U.S." This may keep selling interest on moves towards 1400.

- Spot USD/TWD is down a touch to 30.67, against recent highs of 30.75. USD/HKD is close to 7.8000.

In South East Asia, moves have been modest. USD/IDR is a touch higher last around 16440. More student protests are planned for today, but BI is likely to remain proactive on any attempts to move above 16500.

- USD/PHP sits slightly lower, last around 57.20, while USD/MYR is a touch higher, last close to 4.2300.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 04/09/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/09/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/09/2025 | 0630/0830 | *** | CPI | |

| 04/09/2025 | 0700/0900 | ** | Unemployment | |

| 04/09/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/09/2025 | 0830/0930 | Decision Maker Panel data | ||

| 04/09/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/09/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 04/09/2025 | 0900/1100 | ** | EZ Retail Sales | |

| 04/09/2025 | 0930/1130 | ECB Cipollone Speaks at Digital Euro Hearing, European Parliament | ||

| 04/09/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 04/09/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 04/09/2025 | 1230/0830 | ** | Trade Balance | |

| 04/09/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/09/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/09/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/09/2025 | 1400/1000 | Fed nominee Stephen Miran | ||

| 04/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 04/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/09/2025 | 1600/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 04/09/2025 | 1600/1200 | ** | US DOE Petroleum Supply | |

| 04/09/2025 | 1605/1205 | New York Fed's John Williams | ||

| 04/09/2025 | 2300/1900 | Chicago Fed's Austan Goolsbee | ||

| 05/09/2025 | 2330/0830 | ** | average wages (p) | |

| 05/09/2025 | 2330/0830 | ** | Household spending | |

| 05/09/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/09/2025 | 0600/0700 | *** | Retail Sales | |

| 05/09/2025 | 0645/0845 | * | Foreign Trade | |

| 05/09/2025 | 0800/1000 | * | Retail Sales | |

| 05/09/2025 | 0900/1100 | * | Employment | |

| 05/09/2025 | 0900/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/09/2025 | 1230/0830 | *** | USDA Crop Estimates - WASDE | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Employment Report | |

| 05/09/2025 | 1230/0830 | *** | Labour Force Survey |