ASIA STOCKS: China's Markets Lead the Decline

China equity benchmarks were lower for the third straight session as BBG reported that potential measures were being considered to curb market sentiment. "The measures proposed to top policymakers in recent weeks include the removal of some short selling curbs. Authorities are also contemplating options to rein in speculative trading on concern a sharp reversal might inflict heavy losses on retail investors." (per BBG). Fear has been growing among investors that Chinese regulators will intervene to rein in the excessive stock gains, with measures including acceleration of new stock supply, restrictions on margin accounts and selling of large stakes held by state buyers.

- The Hang Seng is down -1.21% today, the CSI 300 down -2.47%, Shanghai Comp -1.97% and Shenzhen down -1.55% as returns over the last five trading days turn negative.

- The NIKKEI recovered from yesterday's falls and is up +1.45% today

- The TAIEX in Taiwan is up for a second successive day, by +0.55%

- The KOSPI has delivered three days of gains for the first time in a month, up +0.15% today.

- The FTSE Malay KLCI has done very little ahead of the central bank later, down -0.09%.

- The Jakarta Composite is lower by -0.21% as markets appear to be calmer than earlier in the week.

- The NIFTY 50 is up for a third day, by +0.15%. After a week start Monday, the gains have seen it edge over into positive territory week to date.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Richer But Off Bests, Mar-36 Supply Tomorrow

ACGBs (YM flat & XM +4.0) are holding richer but well off session bests.

- June household spending printed lower than expected at 0.5% m/m bringing the annual rate to 4.8% up from May’s 4.4% though. Q2 consumption volumes rose 0.7% q/q, third consecutive gain, up from Q1’s 0.5% signalling that private spending in the national accounts on September 3 could be slightly higher than Q1’s 0.4%. This is an area that has disappointed RBA expectations given the growth in real incomes and it is monitoring closely.

- Cash US tsys are flat to 2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's modest extension of Friday's rally. The highlight of today's US calendar will be the US ISM services index for July.

- Cash ACGBs are 11bps richer after being closed for a bank holiday yesterday, with the AU-US 10-year yield differential at +1bp.

- The bills strip is richer, with pricing flat to +1.

- RBA-dated OIS pricing is giving a 25bp rate cut in August a 100% probability, with a cumulative 65bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from the AOFM planned sale of A$900mn of the 4.25% 21 March 2036 bond. A$1000mn of the 3.00% 21 November 2033 bond is planned for Friday.

GOLD: Bullion Off Today’s High But Holding Onto Post-Payroll Gains

Gold prices are slightly lower in today’s APAC session after rising sharply following the disappointing US July payrolls data and increased pricing of Fed rate cuts. They peaked at $3382.40/oz before trending lower to $3371.33 and are around $3372.0. The higher US dollar and yields put downward pressure on non-interest bearing bullion.

- Silver is down 0.1% to $37.384 after a high of $37.494. It reached a low of $37.371 earlier.

- Equities have followed the US higher with the Nikkei up 0.6%, Hang Seng +0.3%, KOSPI +1.4% and S&P e-mini +0.1%. Oil prices are lower with WTI -0.2% to $66.16/bbl. Copper is up 0.3%.

- Later June US trade, final July S&P Global services/composite PMIs and services ISM print. In Europe, there are July services/composite PMIs and June euro area PPI.

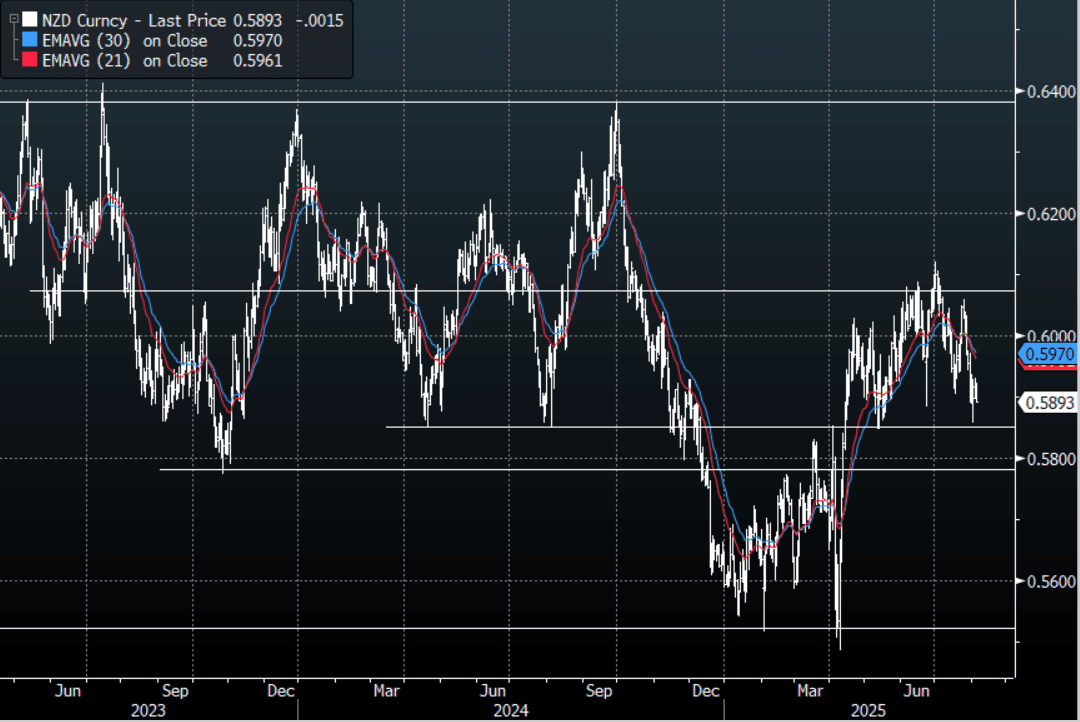

NZD: NZD/USD - Trades Heavy Even With Risk Extending Higher

The NZD/USD had a range of 0.5891 - 0.5923 in the Asia-Pac session, going into the London open trading around 0.5895, -0.25%. US Yields slipped lower again overnight, but stocks came roaring back and the USD went nowhere. NZD/USD bounced nicely off its 0.5850 support but would suspect sellers would return on any bounce back toward 0.6000, it looks like we might consolidate within the 0.5850-0.6100 range while we wait for clearer direction. It has traded heavy in our session after initially trying higher, ignoring the move higher in risk.

- (Bloomberg) -- New Zealand's commodity export prices fell 1.8% m/m in July versus revised -2.4% in June, according to ANZ Bank.

- CHINA PMI Services Records Large Gains: China's S&P Global China PMI (formerly CAIXIN) came in ahead of expectations in July. Up at 52.6, it was a material increase from June's result of +50.6 and estimates of +50.4. The result was the best since May 2024 with the employment index up to +50.9, from June's contraction.

- “The US is exploring ways to equip AI chips with location tracking to curtail exports to China and other restricted countries.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5970(NZD3496m Aug 7). - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD315m). Upcoming Close Strikes : 0.5970(NZD496m Aug 7), 0.6140(NZD364m Aug 7). - BBG

- AUD/NZD range for the session has been 1.0938 - 1.0960, currently trading 1.0955. The Cross continues to consolidate on a 1.09 handle as the pair tries to build some momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P