OIL: Oil Continues to Decline

- Oil declined further in the Asia trading day, after heavy falls overnight on supply concerns

- At an upcoming meeting this weekend, OPEC+ is set to consider options for production and according to some, could be set for a further increase in capacity.

- Already they have approved the increase of 2.5mn barrels a day back in April, a previous supply increase that had been paused.

- In August alone, an additional 400,000 bbls a day was released with the majority coming from Saudi output.

- Production data from Canada showed that Alberta's oil production rose to a record 4.32 million barrels a day in July as oil sands companies boosted output from well sites to fill the expanded Trans Mountain pipeline.

- Asia has increased US crude buying due to cheaper prices and a desire for favor with President Donald Trump. South Korea, Japan, and India have boosted their US crude purchases, with South Korea almost doubling its purchased oil volumes for November.

- An industry estimate showed that crude inventories at the Cushing, Oklahoma, storage hub expanded by 2.1 million barrels last week, which would be the biggest increase since March if confirmed by official data.

- Goldman Sachs Group Inc. reaffirmed a bearish outlook, citing expectations for output to top consumption, with a forecast for Brent to drop to the low $50s in late 2026 (per BBG)

- WTI fell -0.70% today to US$63.52 bbl, following yesterday's large falls.

- Brent fell further also today, down -0.65% to US$67.16 bbl.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

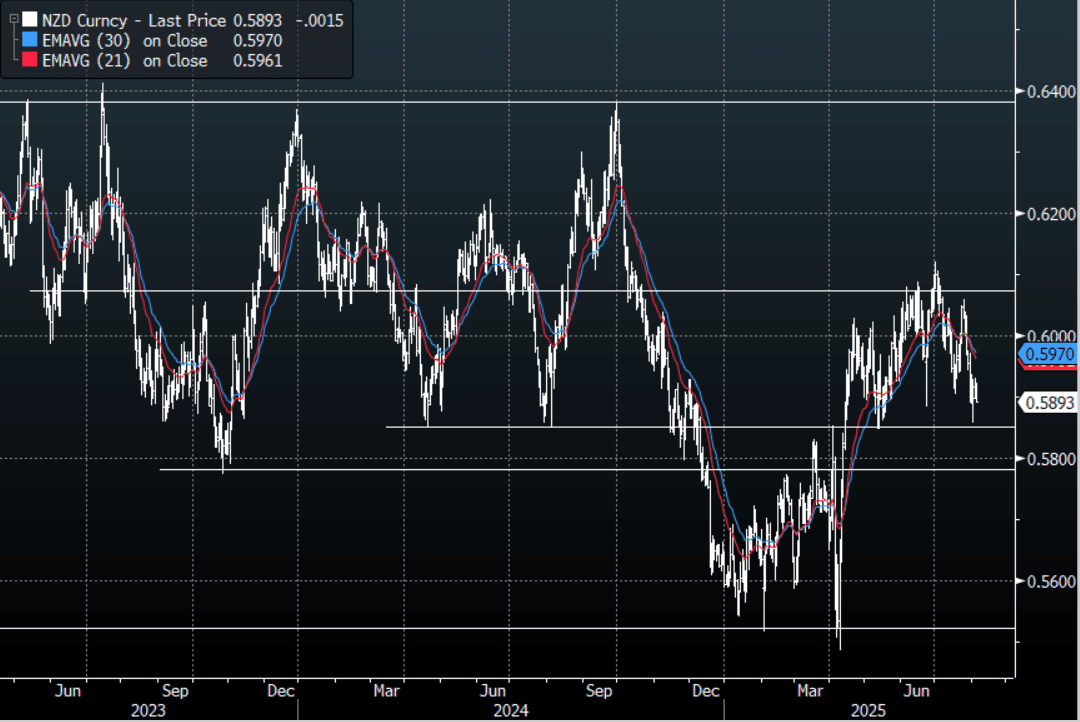

NZD: NZD/USD - Trades Heavy Even With Risk Extending Higher

The NZD/USD had a range of 0.5891 - 0.5923 in the Asia-Pac session, going into the London open trading around 0.5895, -0.25%. US Yields slipped lower again overnight, but stocks came roaring back and the USD went nowhere. NZD/USD bounced nicely off its 0.5850 support but would suspect sellers would return on any bounce back toward 0.6000, it looks like we might consolidate within the 0.5850-0.6100 range while we wait for clearer direction. It has traded heavy in our session after initially trying higher, ignoring the move higher in risk.

- (Bloomberg) -- New Zealand's commodity export prices fell 1.8% m/m in July versus revised -2.4% in June, according to ANZ Bank.

- CHINA PMI Services Records Large Gains: China's S&P Global China PMI (formerly CAIXIN) came in ahead of expectations in July. Up at 52.6, it was a material increase from June's result of +50.6 and estimates of +50.4. The result was the best since May 2024 with the employment index up to +50.9, from June's contraction.

- “The US is exploring ways to equip AI chips with location tracking to curtail exports to China and other restricted countries.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5970(NZD3496m Aug 7). - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD315m). Upcoming Close Strikes : 0.5970(NZD496m Aug 7), 0.6140(NZD364m Aug 7). - BBG

- AUD/NZD range for the session has been 1.0938 - 1.0960, currently trading 1.0955. The Cross continues to consolidate on a 1.09 handle as the pair tries to build some momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Richer & At Session Bests, Q2 Employment Data Tomorrow

NZGBs closed at session bests, 4-5bps richer.

- Cash US tsys are flat to 2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's modest extension of Friday's rally. The highlight of today’s US calendar will be the US ISM services index for July.

- ANZ commodity export prices fell 1.8% m/m in July versus a revised -2.4% in June.

- Tomorrow, the local calendar will see Q2 labour market data. It is expected to show that it weakened in the quarter after some signs of stabilisation in Q1. The unemployment rate is forecast to rise 0.2pp to 5.3% more than the RBNZ's 5.2% May projection. If the data print is as weak as or weaker than the Bloomberg consensus, then a rate cut on August 20 is likely.

- RBNZ dated OIS pricing closed showing 23bps of easing is priced for August, with a cumulative 42bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

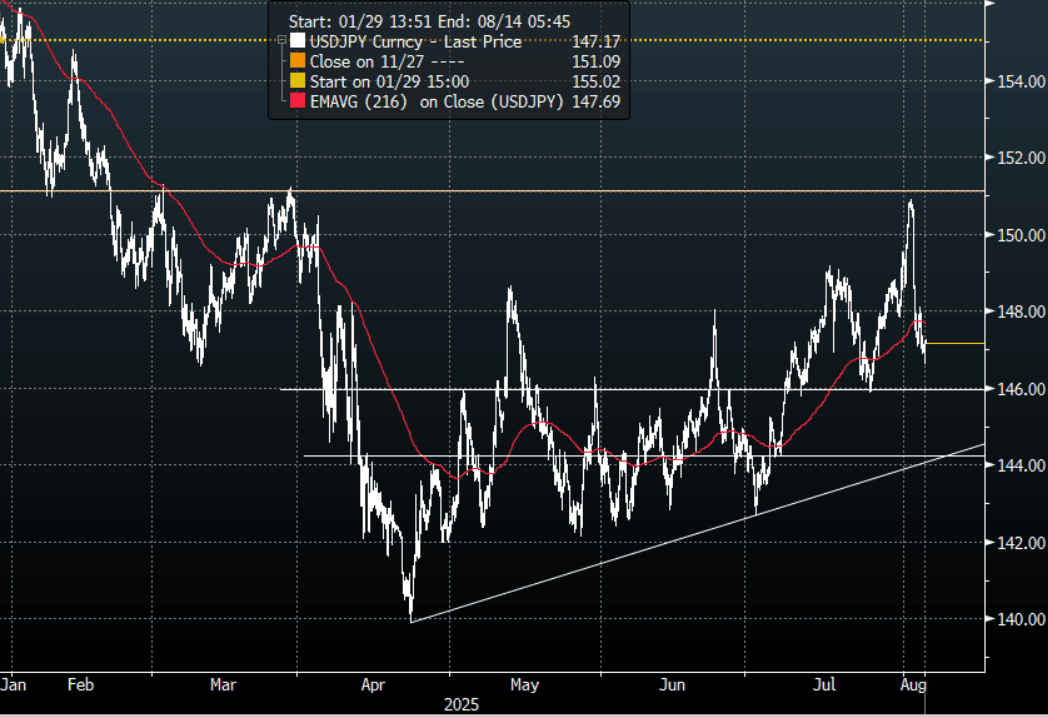

JPY: USD/JPY - Finds Some Demand Sub 147.00

The Asia-Pac USD/JPY range has been 146.62 - 147.26, Asia is currently trading around 147.20, +0.05%. USD/JPY was capped by decent supply around 148.00 overnight and traded heavy into our open ignoring the big bounce in US Equities. Price has moved very quickly away from the pivotal 151/152 area much to the relief of Institutional JPY longs and the BOJ. CFTC Data shows leveraged accounts had started to aggressively build Yen shorts last week so this quick move lower would be a bitter pill to swallow. Price is tested the first support area around 146.50/147.00 where it found good demand this morning, a move sub 145.00 is needed to turn momentum lower once more, until then the 145.00-151-00 range should dominate.

- "AKAZAWA: WILL MULL COLLABORATION WITH US ON PHARMA SUPPLY, WILL WORK CLOSELY WITH US ON CHIP MANUFACTURING. CHIP, PHARMA ARE IMPORTANT FOR ECONOMIC SECURITY. WILL ALSO AIM TO BOOST INWARD DIRECT INVESTMENT" - BBG - BBG

- "ISHIBA: BELIEVE TRADE DEAL DAMAGE TO AUTO INDUSTRY MINIMAL, DEAL IS WIN-WIN BASED ON JAPAN'S TECH, US LABOR AND MKT. LIMITING IMPACT OF TRADE DEAL ON JAPAN FARMERS CRITICAL, TRADE DEAL DOESN'T AFFECT JAPAN'S RICE FARMERS" - BBG

- Bloomberg - “MUFG CEO Hironori Kamezawa called on the BOJ to raise its policy rate as early as the next meeting to combat strong inflation.”

- “Japan is set to shift its policy on rice to focus on boosting production, moving away from adjusting output to maintain price stability, Nikkei reported.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($1.13b).Upcoming Close Strikes : 147.00($1.31b Aug 6), 148.50($1.24b Aug 7) - BBG.

- CFTC data shows asset managers surprisingly added slightly to their JPY longs +75119( Last +72326), while leveraged funds aggressively added to their newly built short JPY position -31280(Last -11571).

Fig 1 : USD/JPY Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P