JGBS: 30yr Yield Down Post Auction, Labour Earnings Data Tomorrow

Futures sit at 137.55, +.26 versus settlement levels. Post lunch break highs were at 137.65. This was close to highs seen at the start of Sep. US tsy futures hold a touch weaker, but have had a quiet session, while cash Tsy yields are down a touch.

- The 30yr debt auction was not as bad as feared from a demand standpoint. The bid to cover ratio was 3.31, versus a 12mth average of 3.38 (per BBG). The tail for the auction was 0.18, versus the early August result of 0.15.

- Cash JGB yields are down led by the back end of the curve. The 30yr last off 4bps to be back near 3.26%. The 10yr is back to 1.615%, off close to 1.5bps. The JGBs 2/30s curve sits a touch flatter at +241bps.

- Earlier headlines crossed, notably: "*HAYASHI: NOT TRUE GOVT DECIDED TO COMPILE ECONOMIC MEASURES" - BBG and *HAYASHI: MANAGE IN WAY THAT AVOIDS SUDDEN RISE IN L-T RATES" - BBG. Extra stimulus/household support remains a focus point, particularly given budget requests for the upcoming financial year are pressured by debt repayments and higher defence spending.

- Also note: "*BOJ TO HOLD MEETING ON MARKET OPERATIONS ON OCT. 16" - BBG.

- Note tomorrow we get July labour cash earnings. Nominal earnings are forecast to rise 3.0%y/y, versus 3.1% in June. Real earnings are expected at -0.6%y/y, which would be an improvement on the June -0.8%y/y outcome.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Richer But Off Bests, Mar-36 Supply Tomorrow

ACGBs (YM flat & XM +4.0) are holding richer but well off session bests.

- June household spending printed lower than expected at 0.5% m/m bringing the annual rate to 4.8% up from May’s 4.4% though. Q2 consumption volumes rose 0.7% q/q, third consecutive gain, up from Q1’s 0.5% signalling that private spending in the national accounts on September 3 could be slightly higher than Q1’s 0.4%. This is an area that has disappointed RBA expectations given the growth in real incomes and it is monitoring closely.

- Cash US tsys are flat to 2bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's modest extension of Friday's rally. The highlight of today's US calendar will be the US ISM services index for July.

- Cash ACGBs are 11bps richer after being closed for a bank holiday yesterday, with the AU-US 10-year yield differential at +1bp.

- The bills strip is richer, with pricing flat to +1.

- RBA-dated OIS pricing is giving a 25bp rate cut in August a 100% probability, with a cumulative 65bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from the AOFM planned sale of A$900mn of the 4.25% 21 March 2036 bond. A$1000mn of the 3.00% 21 November 2033 bond is planned for Friday.

GOLD: Bullion Off Today’s High But Holding Onto Post-Payroll Gains

Gold prices are slightly lower in today’s APAC session after rising sharply following the disappointing US July payrolls data and increased pricing of Fed rate cuts. They peaked at $3382.40/oz before trending lower to $3371.33 and are around $3372.0. The higher US dollar and yields put downward pressure on non-interest bearing bullion.

- Silver is down 0.1% to $37.384 after a high of $37.494. It reached a low of $37.371 earlier.

- Equities have followed the US higher with the Nikkei up 0.6%, Hang Seng +0.3%, KOSPI +1.4% and S&P e-mini +0.1%. Oil prices are lower with WTI -0.2% to $66.16/bbl. Copper is up 0.3%.

- Later June US trade, final July S&P Global services/composite PMIs and services ISM print. In Europe, there are July services/composite PMIs and June euro area PPI.

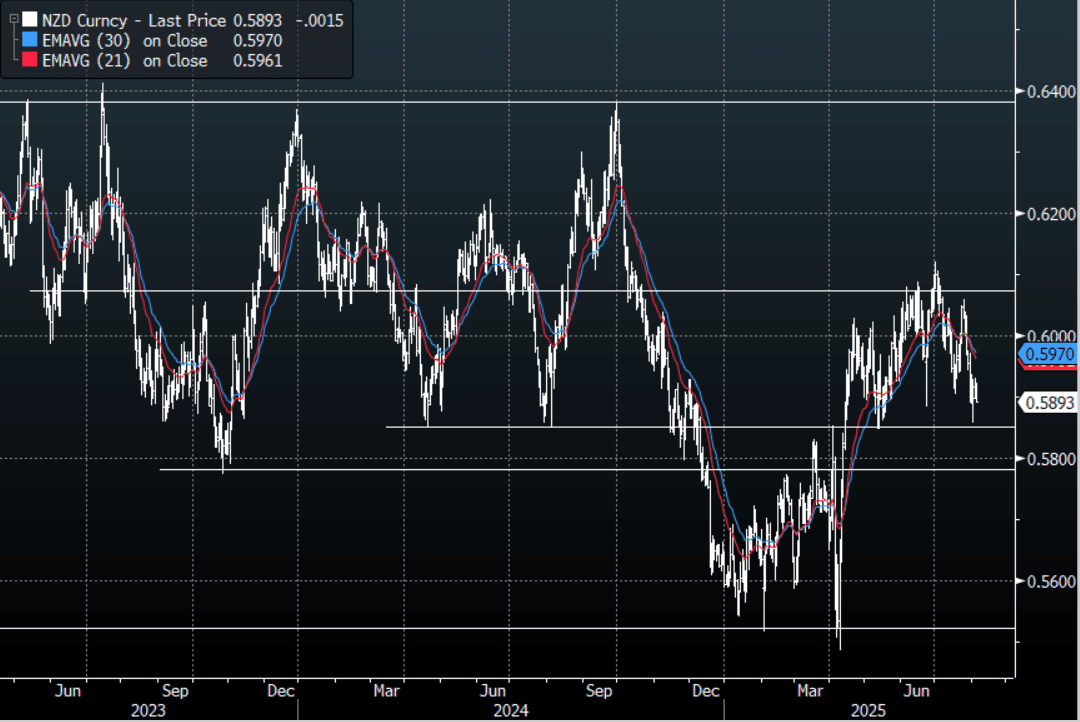

NZD: NZD/USD - Trades Heavy Even With Risk Extending Higher

The NZD/USD had a range of 0.5891 - 0.5923 in the Asia-Pac session, going into the London open trading around 0.5895, -0.25%. US Yields slipped lower again overnight, but stocks came roaring back and the USD went nowhere. NZD/USD bounced nicely off its 0.5850 support but would suspect sellers would return on any bounce back toward 0.6000, it looks like we might consolidate within the 0.5850-0.6100 range while we wait for clearer direction. It has traded heavy in our session after initially trying higher, ignoring the move higher in risk.

- (Bloomberg) -- New Zealand's commodity export prices fell 1.8% m/m in July versus revised -2.4% in June, according to ANZ Bank.

- CHINA PMI Services Records Large Gains: China's S&P Global China PMI (formerly CAIXIN) came in ahead of expectations in July. Up at 52.6, it was a material increase from June's result of +50.6 and estimates of +50.4. The result was the best since May 2024 with the employment index up to +50.9, from June's contraction.

- “The US is exploring ways to equip AI chips with location tracking to curtail exports to China and other restricted countries.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5970(NZD3496m Aug 7). - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD315m). Upcoming Close Strikes : 0.5970(NZD496m Aug 7), 0.6140(NZD364m Aug 7). - BBG

- AUD/NZD range for the session has been 1.0938 - 1.0960, currently trading 1.0955. The Cross continues to consolidate on a 1.09 handle as the pair tries to build some momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P