MNI EUROPEAN MARKETS ANALYSIS: JGBs Down Sharply Post Auction

- The RBNZ delivered a hawkish 25bps cut. RBNZ-dated OIS pricing closed 6-10bps firmer across meetings versus pre-RBNZ levels. In Japan, JGB futures are sharply weaker and at Tokyo session lows, -68 compared to settlement levels, after today’s 40-year auction displayed poor demand metrics.

- NZD outperformed in the G10 space, but the USD is mostly finding support as we approach month end.

- In the equity space, ahead of tomorrow’s decision by the BOK, the Kospi in South Korea was the regional outperformer as it achieves new highs for 2025 as large cap chipmakers join value stocks in the run up to next week’s election.

- Later the Fed’s Kashkari speaks as well as the May FOMC meeting minutes are released. US May Richmond & Dallas Fed indices as well as German April unemployment and French April consumption are released. BoE’s Pill also speaks.

MARKETS

US TSYS: Asia Wrap - 2s10s Steepens

The TYM5 range has been 110-09 to 110-15 during the Asia-Pacific session. It last changed hands at 110-09, down 0-07 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.965%, down 0.02 from its close.

- The US 10-year yield has edged higher, dealing around 4.467%, up 0.02 from its close.

- This has seen the yield curve steepen in Asia - 2s10s +3.73 at 49.583.

- (Bloomberg) “The JGB 40-year sale has come in weak after all. The bid-to-cover dropped back to 2.21, the weakest since July. And the yield of 3.135% is above the poll estimate of 3.085%. That global bond bounce may fade.”

- “The Fed’s Tom Barkin said elevated uncertainty has led businesses to freeze hiring and hold off on future investment decisions. Neel Kashkari said there’s a “healthy debate” among policymakers about whether to look through the inflation effect of tariffs as a transitory shock, or a lasting issue.”(BBG)

- " FED'S WILLIAMS: WE HAVE TO BE VERY AWARE THAT INFLATION EXPECTATIONS COULD SHIFT IN ANY WAYS THAT COULD BE DETRIMENTAL - [RTRS]

- The 10-year look likely to see supply on any dips in yield in the short-term, should yields hold above 4.35/40% the target looks to be the 4.75% area. Watch for any announcements though relating to the SLR, this could have an impact on a market that is already quite short.

JGBS: Aggressive Bear-Steepener After Poor 40Y Auction

JGB futures are sharply weaker and at Tokyo session lows, -68 compared to settlement levels, after today’s 40-year auction displayed poor demand metrics.

- Demand for today’s 40-year bond issuance was notably weak, with the high yield clearing well above dealer expectations. According to a Bloomberg survey, the market anticipated a yield of 3.085%, while the actual result came in at 3.135%.

- The auction’s cover ratio declined sharply to 2.2114x, down from 2.9203x at the previous issuance and marking the weakest demand since July 2024.

- Given the combination of elevated yield and weak demand metrics, today’s result is likely to be regarded as very poor. In afternoon trading, the 40-year yield is dealing 8bps higher versus pre-auction levels.

- Cash US tsys have modestly bear-steepened in today's Asia-Pac session, with yields flat to 3bps higher.

- Cash JGBs are 2-8bps cheaper, with a steeper curve.

- The swaps curve has bear-steepened, with rates 3-8bps higher. Swap spreads are wider.

- Tomorrow, the local calendar will see International Investment Flow and Consumer Confidence data alongside BoJ Rinban Operations covering 3-25-year JGBs.

AUSSIE BONDS: Cheaper But Limited Reaction To CPI Data

ACGBs (YM -4.0 & XM -3.0) are modestly mixed after the release of April CPI data.

- April headline inflation was unchanged at 2.4% y/y, slightly higher than expected, while the trimmed mean picked up 0.1pp to 2.8% y/y. The focus is on the latter as the headline is likely to be impacted by government electricity rebates until year-end. Underlying inflation has been sitting around 2.7/2.8% since December, and the RBA expects 2.6% for Q2, which is released on July 30.

- Cash US tsys have bear-steepened in today's Asia-Pac session, with yields flat to 3bps higher.

- Cash ACGBs are 3bps cheaper on the day, with the AU-US 10-year yield differential at -14bps.

- Swap rates are 1-3bps higher after the CPI data.

- The bills strip has cheapened after the data, leaving pricing -3 to -6 across contracts.

- RBA-dated OIS pricing is 1-4bps firmer across meetings after the data. A 25bp rate cut in July is given a 64% probability (70% pre-data), with a cumulative 73bps (70bps pre-data) of easing priced by year-end.

- Tomorrow, the local calendar will see Q1 Private Capital Expenditure data.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Friday.

AUSTRALIA DATA: April Underlying Inflation Measures Higher

April headline inflation was unchanged at 2.4% y/y, slightly higher than expected, while the trimmed mean picked up 0.1pp to 2.8% y/y. The focus is on the latter as headline is likely to be impacted by government electricity rebates until year end. Underlying inflation has been sitting around 2.7/2.8% since December and the RBA expects 2.6% for Q2, which is released on July 30.

- CPI ex volatile items & holiday travel rose 0.3% m/m seasonally adjusted to be up 2.8% y/y after 2.6% y/y in March. Seasonally adjusted headline rose 0.2% m/m and both showed a moderation in 3-month momentum but it remains above 3.5% annualised.

- Disinflation continues to be driven by goods & tradeables with annual inflation moderating to 0.9% y/y and 0.3% y/y respectively, as fuel prices fell further in April. Domestically-driven services & non-tradeables inflation picked up though to 4.1%, highest since November, and 3.6%, highest since August.

- Food & non-alcoholic beverage inflation moderated to 0.3pp to 3.1% y/y in April but housing rose 0.4pp to 2.2% y/y due to new dwellings. Rents eased to 5.0% y/y from 5.2%, the lowest since February 2023.

- Electricity fell 6.5% y/y in April after -9.6% y/y, as rebates in Queensland and WA have been used. Without all government subsidies, prices would have been up 1.5% y/y, according to the ABS.

Australia CPI y/y%

BONDS: NZGBS: Bear-Flatter After RBNZ Hawkish Cut

NZGBs closed 4-9bps cheaper, with a flatter curve.

- The RBNZ cut rates 25bp to 3.25% following a vote that included an option to leave rates unchanged. The vote wasn’t unanimous, with one dissenter. Despite this, the OCR path was revised down to show a trough 25bp below February’s at 2.85%.

- In his first press conference as Governor, Hawkesby noted that this was the first vote on the direction of rates in two years—something that typically occurs at inflection points and highlights the current high level of uncertainty. With policy rates now in the “neutral zone,” he emphasised that the MPC is positioned to “respond to developments as they occur,” indicating that further easing is not guaranteed and future moves will depend on incoming data and the evolving outlook.

- Swap rates closed 7-10bps higher.

- RBNZ-dated OIS pricing closed 6-10bps firmer across meetings versus pre-RBNZ levels. Markets had fully priced in today’s 25bp cut ahead of the decision. A total of 32bps of easing is now expected by November 2025.

- Tomorrow, the local calendar will see the RBNZ Governor in front of the Parliament Select Committee on MPS. ANZ Business Confidence is also scheduled for release.

- The NZ Treasury also plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-36 bond.

RBNZ: 3.25% OCR Is In the “Neutral Zone”

Governor Hawkesby held his first press conference and noted that the vote on the direction of rates was the first in two years and usually occurs at inflexion points and also reflects the high degree of uncertainty at the moment. With rates now in the “neutral zone” the MPC “can now respond to developments as they occur”, thus further easing isn’t a given and future decisions will remain data and outlook dependent.

- There was a consensus around the updated projections but not whether there needed to be a rate cut in May.

- Chief Economist Conway said that the central bank sees neutral as between 2.5% and 3.5% and now that rates are at 3.25% and in that range, it becomes more difficult to talk about restrictive or stimulatory policy and communication will mention ‘neutral’ less. The RBNZ is now focussed on the effect of rates on the economy.

- The central case remains that inflation returns to the 1-3% mid-point as core trends lower, but risks remain especially as inflation printed at 2.5% in Q1. This may also have contributed to the pickup in Q2 inflation expectations, which can respond to higher inflation in the short-term. Tariff news may have also boosted them.

- As reflected in the downward revisions to its growth and inflation projections, the RBNZ sees increased trade protectionism as a negative demand shock for NZ after looking at the channels the developments will feed through.

- The May budget had little effect on RBNZ projections and thinking.

RBNZ: Global Events Suggest Policy Could Become Stimulatory

The RBNZ cut rates 25bp to 3.25% following a vote that included an option to leave rates unchanged. The vote wasn’t unanimous with one dissenter. There appears to be some disagreement over the impact of increased trade protectionism on NZ inflation. Despite this, the OCR path was revised down to show a trough 25bp below February’s at 2.85%, which signals that the impact of current global developments would require stimulatory policy by end-2025.

- The arguments to cut rates included inflation is within the 1-3% target band, core and wage inflation are moderating, significant spare capacity persists, domestic inflation is impacted by higher administered prices, and growth and inflation are projected to be lower due to global events.

- In terms of staying on hold, the MPC considered that it would have more time to assess the impact of elevated uncertainty on behaviour, will help inflation expectations to return to the band mid-point, and “guard against” risk of higher inflation from a tariff-related supply chain shock.

- Given the outcome of US trade negotiations remains highly uncertain, the RBNZ ran two scenarios with different impacts on NZ inflation – significant rise in global production costs increasing imported inflation and weaker global growth & trade diversion reduces imported inflation.

- Global developments drive the RBNZ’s downward revision to growth and inflation. GDP is revised lower in 2025 but then is expected to be higher in 2026. The economy is still assumed to recover with end-2025 growth at 1.8% y/y and 2.9% Q4 2026 after -1.1% in Q4 2024. It believes that it continues to be “well placed” to respond to events.

- Q2 2025 inflation was revised up 0.2pp to 2.6% y/y but Q4 is 0.1pp lower at 2.4% and Q4 2026 at 2.1%.

- The OCR troughs at 2.85% in Q1 2026 with 25-50bp of easing in Q3 2025. Rates are assumed to return to around ‘neutral’ in 2027.

NEW ZEALAND: Jobs Market Still Soft But Stabilising

The deterioration in the labour market appears to have stabilised but a recovery is yet to begin. Filled jobs in April fell 0.1% m/m to be down 1.7% y/y after a 0.1% m/m rise in March but it was also down 1.7% y/y. Vacancies are off their 2024 lows but remain depressed despite rising in March & April. The RBNZ is widely expected to cut rates 25bp today but the focus will be on the updated OCR trajectory and if it signals a possibility of policy going stimulatory.

- Primary industries saw a 0.1% m/m rise in filled jobs, a sector that has seen strong external demand lately. However, goods-producing sectors fell 0.3% m/m and services -0.1% m/m.

- In annual terms, construction jobs are down 6.5% y/y and admin services -6.7% y/y. Retail is down 1.5% y/y.

- Young people have felt the brunt of labour shedding with filled jobs for 15-19 year olds down 10% y/y and 20-24 years -3.9% y/y.

- April SEEK job ads rose 1.1% m/m but are still down 9.6% y/y. 3-month momentum though has been positive this year. Labour supply remains robust with applicants per job ad up 17.5% y/y but the ratio down 3.1% m/m in March, the sharpest monthly drop in over 2 years as migration eases.

NZ job ads vs filled jobs

NZD: Asia Wrap - NZD Bounces On A Hawkish Cut

The NZD/USD had a range of 0.5924 - 0.5980 in the Asia-Pac session, going into the London open trading around 0.5960. The NZD has bounced pretty hard with the RBNZ being surprisingly hawkish suggesting that they are pretty close to neutral now.

- The RBNZ decision, has aided NZD, with the 25bps cut and lowered OCR projection offset by the non-unanimous decision. This hints further cuts may be harder to come by, while Governor Hawkesby wouldn't be drawn on the policy bias at the next meeting, with central bank well placed to respond to developments. RBNZ officials also note the new OCR of 3.25% is in the neutral zone.

- "RBNZ GOV HAWKESBY: HAVE LOWERED RATES A CONSIDERABLE WAY, STILL WORKING WAY THROUGH - [RTRS]"

- "RBNZ'S CONWAY: OCR AT 3.25% IS `INTO NEUTRAL ZONE'" - BBG.

- The NZD has bounced across the board on the back of this and expect this price action to continue as shorts that had been added to hoping for a more dovish outcome are pared back.

- The NZD continues to trade in a 0.5850/0.6050 range, another failure above 0.6000 and with corporate month-end in play be on the lookout for more demand of USD’s over the next day or 2.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break here could provide the spark for the next leg higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5725(NZD1.09b). Upcoming Close Strikes : 0.5975(NZD400m May 29)

AUD/NZD range for the session has been 1.0779 - 1.0851, currently trading 1.0790. A sustained break above 1.0930 is needed to turn the focus higher, until then expect supply on bounces. It traded up to a high around 1.0851 just before the RBNZ, but has subsequently dropped lower as the RBNZ suggests they are close to neutral. A top looks in place now just above 1.0900, the market will have been looking for a more dovish tone today and AUD/NZD should now see supply on bounces. The first target is around 1.0650.

Fig 1: AUD/NZD Spot Daily Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - AUD Stays Under Pressure

The AUD/USD has had a tight range of 0.6426 - 0.6454 in the Asia- Pac session, it is currently trading around 0.6430 drifting down back towards the days lows.

- April headline inflation was unchanged at 2.4% y/y, slightly higher than expected, while the trimmed mean picked up 0.1pp to 2.8% y/y. The focus is on the latter as headline is likely to be impacted by government electricity rebates until year end.

- We head into the corporate month-end and this could see more demand for USD’s over the next day or 2.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6325(AUD430m). Upcoming Close Strikes : 0.6400(AUD 556m June 2), 0.6500(AUD 532m May 30)

AUD/JPY - Today's range 92.75 - 93.23, it is trading currently around 93.00. The pair has again found supply above the 93.00 area in today's session, a break back above 93.50 could see the focus return once more to the 95/96 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg

JPY: Asia Wrap USD/JPY - A Whippy Session With An Underlying Bid

The Asia-Pac USD/JPY range has been 143.85 - 144.77, Asia is currently trading around 144.35. USD/JPY has had a very whippy session with a big spike seen into the Japanese Fix, it drifted lower from there but bounced again in our afternoon to make a new high around 144.77.

- " Regarding a recent spike in super-long yields on government debt, market participants cited the unwinding of existing positions and a drop in demand, Bank of Japan Governor Kazuo Ueda says. Moves in short- and long-term yields tend to affect the economy more than those in super long-term yields. Will monitor market developments closely along with their economic impact by keeping in mind that major moves in super long-term yields can affect shorter-term yields." (per BBG)

- "A Japanese government advisory panel is urging authorities to intensify fiscal consolidation efforts, according to Bloomberg News on Tuesday, citing a proposal submitted to Finance Minister Katsunobu Kato on the same day. This comes as the Bank of Japan's ongoing monetary tightening increases the risk of higher debt-servicing costs for the nation, said the news wire." (per MTN)

- (Bloomberg) - “The JGB 40-year sale has come in weak after all. The bid-to-cover dropped back to 2.21, the weakest since July. And the yield of 3.135% is above the poll estimate of 3.085%. That global bond bounce may fade.”

- This move yesterday would have caught out a few shorts, but we are approaching resistance back towards 145.00/146.00 which should see some sellers emerge.

- It is worth noting though we are heading into the corporate month-end and this could see some USD demand over the next day or 2 making it uncomfortable for the considerable JPY longs that have been built up.

- The market has been very confident of a move lower in USD/JPY but with positioning quite large now the risk of pullbacks does increase. Resistance is now back towards 145.00/146.00 area first up.

Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($2.14b), 143.00($1.98b), 144.00($1.67b). Upcoming Close Strikes : 143.00($3.34b May 30), 140.00($2.78b May 30).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

FOREX: Asia FX Wrap - USD Keeps Its Bid Tone

The BBDXY has had a range of 1215.25 - 1219.21 in the Asia-Pac session, it is currently trading around 1218. “The Fed’s John Williams said policymakers should focus on anchoring not just long-term price expectations, but “the whole curve” to prevent inflation from becoming persistent or permanent”(BBG). “The ECB’s Philip Lane said inflation will hover around 2% for the rest of the year. The impact of US tariffs on medium-term price pressures will determine monetary policy, he told the FAZ.”(BBG)

- EUR/USD - Asian range 1.1301 - 1.1345, Asia is currently trading 1.1305. EUR has drifted lower for most of the Asian session. It is worth noting that we are heading into the corporate month-end and this could see some USD demand over the next day or 2. Dips back to 1.1200 are expected to be supported.

- GBP/USD - Asian range 1.3473 - 1.3522, Asia is currently dealing around 1.3470. The GBP is struggling to hold above the pivotal 1.3500 area for now, looking for support to return back towards the 13300/3400 area which could be seen if the corporate USD demand materializes.

- USD/CNH - Asian range 7.1868 - 7.1993, the USD/CNY fix printed 7.1894. Asia is currently dealing around 7.1950. Sellers should be found on a bounce back towards the 7.2200 area again. Andreas Steno Larsen on X : The elephant in the room. USDCNH needs to go to 6.80 at least. https://x.com/AndreasSteno/status/1926115935200440525

- Cross asset : SPX -0.10%, Gold $3297, US 10-Year 4.47%, BBDXY 1218, Crude oil $61.19

Data/Events : Fra GDP & PPI, Ger Unemployment, ECB CPI Expectations

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: KOSPI Leads the Way whilst Others are in Holding Pattern

Ahead of tomorrow’s decision by the BOK, the Kospi in South Korea was the regional outperformer as it achieves new highs for 2025 as large cap chipmakers join value stocks in the run up to next week’s election. Shares of holding companies continue to perform as pushes to reform the corporate structure grow louder.

Chinese bourses did very little today as volatility remains low in the region's largest economy as investors wait for the next update on tariff discussions. BYD fell in Hong Kong for a third day straight on concerns of discounting. BYD is down over -2.00% today and down over 12% for the week, weighing heavy on the Hang Seng and other EV related stocks.

- The Hang Seng is down today by -0.55% and trading very heavy for the week. The CSI 300 is up a mere +0.09%, Shanghai Comp +0.07% and Shenzhen down -0.12%.

- The KOSPI is the regional outperformer today, rising +1.66% easily wiping out yesterday's modest losses.

- The fact that the FTSE Malaysia KLCI was flat today will come as welcome relief given falling nine of the last 12 trading days.

- The Jakarta Composite did very little today also yet remains up over 6% month to date making it the best performer of the major markets.

- In Singapore the Straits Times is up +0.50% whilst the PSEi in the Philippines is up +1.40%.

- The NIFTY 50 closed lower by -0.70% yesterday and carried that over to today and is currently down -0.25%

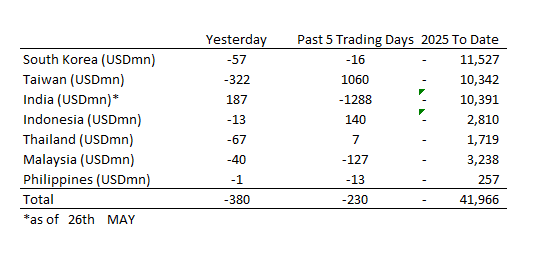

ASIA STOCKS: The Period of Big Inflows Appears to have Stalled

After an exceptional period of inflows into the major markets, it appears that this trend has stalled for now as constant daily flows are interrupted with outflows.

- South Korea: Recorded outflows of -$57m yesterday, bringing the 5-day total to -$16m. 2025 to date flows are -$11,527. The 5-day average is -$3m, the 20-day average is +$76m and the 100-day average of -$115m.

- Taiwan: Had outflows of -$322m as yesterday, with total inflows of +$1,060m over the past 5 days. YTD flows are negative at -$10,342. The 5-day average is +$212m, the 20-day average of +$414m and the 100-day average of -$115m.

- India: Had inflows of +$187m as of the 26th, with total outflows of -$1,288m over the past 5 days. YTD flows are negative -$10,391m. The 5-day average is -$258m, the 20-day average of +$153m and the 100-day average of -$115m.

- Indonesia: Had outflows of -$13m as of yesterday, with total inflows of +$140m over the prior five days. YTD flows are negative -$2,810m. The 5-day average is +$28m, the 20-day average +$13m and the 100-day average -$31m.

- Thailand: Recorded outflows of -$67m as of yesterday, inflows totaling +$7m over the past 5 days. YTD flows are negative at -$1,719m. The 5-day average is +$1m, the 20-day average of -$4m and the 100-day average of -$17m.

- Malaysia: Recorded outflows of -$40m as of yesterday, totaling -$127m over the past 5 days. YTD flows are negative at -$3,238m. The 5-day average is -$28m, the 20-day average of +$27m and the 100-day average of -$22m.

- Philippines: Saw outflows of -$1m yesterday, with net outflows of -$13m over the past 5 days. YTD flows are negative at -$257m. The 5-day average is -$3m, the 20-day average of +$2m the 100-day average of -$3m.

OIL: Crude Range Trading Ahead Of Key Events, FOMC Minutes Later

Oil prices are moderately higher today after falling around 0.7% on Tuesday. They are range trading as the market waits for key US data on Friday and the outcome of OPEC’s May 31 meeting. WTI is up 0.5% to $61.20/bbl after a high of $61.43, while Brent is 0.5% higher at $64.40/bbl off the intraday low of $64.32. The US dollar continues to strengthen with the USD index up 0.15%.

- With OPEC expected to increase output again in July adding to global excess supply, attention will remain on US inventory data with industry-based figures out later today and the official EIA report on Friday, delayed because of Monday’s US holiday which marked the start of the driving season. Gasoline demand will be especially monitored during this time.

- OPEC’s Joint Ministerial Monitoring Committee meets virtually today to discuss quotas for July and then a smaller group led by Saudi Arabia will decide on May 31.

- It seems that sanctions on Russia’s fossil fuel exports are not only going to stay but may tighten with Europe already increasing restrictions and considering others, while the US is also seriously thinking about adding to its list. Russian attacks on Ukraine have intensified despite calls for a truce.

- Later the Fed’s Williams and Kashkari speak as well as the May FOMC meeting minutes are released. US May Richmond & Dallas Fed indices as well as German April unemployment and French April consumption are released. BoE’s Pill also speaks.

GOLD: Stronger Greenback Continues To Pressure Gold

Gold prices are down slightly during today’s APAC trading after falling 1.3% on Tuesday. They are down 0.1% to $3296.60 as the strengthening US dollar continues to weigh (USD BBDXY +0.1%) while equity and commodity prices are mixed. Bullion rose to $3315.81 early in the session before falling to $3291.79.

- Gold is trading in a narrow range as markets wait for news on the progress of trade negotiations and key US data out on Friday, especially PCE prices. US April durable orders were better than expected and the Dallas Fed manufacturing index improved substantially. It is also sensitive to geopolitical developments that may shift safe-haven flows.

- Equities have been mixed with the S&P e-mini down 0.1% and Hang Seng -0.6% but Nikkei up 0.3% and Kospi +1.7%. Oil prices are higher with the WTI +0.6% to $61.24. Copper is down 0.6% though. Silver is little changed at around $33.26.

- Later the Fed’s Williams and Kashkari speak as well as the May FOMC meeting minutes are released. US May Richmond & Dallas Fed indices as well as German April unemployment and French April consumption are released. BoE’s Pill also speaks.

SOUTH KOREA: Country Wrap: BOK to Cut Rates by 25bps

- MNI BOK Preview - May 2025: BOK to Cut. The BOK to cut rates by 25bps this week whilst tempering expectations for further cuts given contraction in Q1 GDP, • CPI manageable and in line with target with expectations it could moderate further, whilst exports have rebounded, ongoing tariff concerns cloud the outlook and the currency and equity markets have rebounded strongly providing good back drop for rates move. (source MNI Market News)

- Presidential frontrunner Lee Jae-myung’s liberal Democratic Party publishes pledge book on Wednesday ahead of June 3 election. These include: To appoint chief AI officer in presidential office, To introduce online platform bill to prevent power abuse by local and international big platform cos, To expand the duty of loyalty for corporate boards to include safeguarding the interests of shareholders, To reduce small merchants’ burden via debt adjustments or forgiveness, To consider institutionalization of treasury stock cancelation of listed companies, To allow crypto spot ETFs; to prepare measures on using won-based stablecoin, To seek 4.5-day workweek (source BBG)

- The KOSPI is the regional outperformer today, rising +1.66% easily wiping out yesterday's modest losses.

- The Won is in a holding pattern as the economy awaits the BOK decision tomorrow, trading at 1,376.40

- Bonds are stronger with yields lower across the curve by up to -2.5bps. KTB 10YR 2.71%

CHINA: Country Wrap: BBG Survey Sees GPD at 4.5%

- Country is vying for global leadership in strategic sectors including artificial intelligence, robotics and high-performance computing chips. China has unveiled a detailed plan to upgrade its information technology (IT) manufacturers as it doubles down on achieving self-sufficiency in technologies including semiconductors, batteries, satellite navigation and artificial intelligence (AI), and sidestepping US tech curbs. The 18-point action plan calls for the deepening of AI integration and the fostering of a new class of industry service providers by 2027. It aims to see more than 85 per cent of manufacturers using computer numerical control - in which computer programs automate machining - in key processes in the next two years, and to cultivate at least 100 specialized service providers for the sector. (source SCMP)

- BBG's May economic survey for China suggests GDP will expand +4.5% in 2025 and +4.2% in 2026. 2025 CPI forecast at +0.3% y/y versus prior survey +0.4%. PBOC 1 Year medium-term lending facilities rate seen at 1.90% by end-2Q25, current rate is 2.00% (source BBG)

- The Hang Seng is down today by -0.55% and trading very heavy for the week. The CSI 300 is up a mere +0.09%, Shanghai Comp +0.07% and Shenzhen down -0.12%.

- Yuan Reference Rate at 7.1894 Per USD; Estimate 7.2014

- Bond market activity remains subdued with the 10YR marginally higher in yield at 1.70%

ASIA FX: USD/CNH Drifts Higher, KRW & TWD Modestly Outperform

In North East Asia FX, aggregate FX moves have been very modest in Wednesday trade to date. USD/CNH is a little higher, and supported on dips so far, while KRW and TWD are little changed, outperforming firmer USD trends elsewhere but only at the margin.

- USD/CNH was last near 7.1950, unable to test above 7.2000 but supported under 7.1900. The pair continues the recent pattern since Monday of higher highs and lows. We remain well within recent ranges, and appear to mostly be following broader USD trends, albeit with a low beta. A move above 7.2000 may bring more selling interest into play.

- Spot USD/KRW was last near 1376, little changed for the session. At the start of the session we did dip briefly under 1370, before buying interest emerged. Local equities were up +2% at one stage, we now sit at +1.5%. Optimism around potential corporate value up from a new South Korean President (elections are held June 3), along with a strong offshore tech lead have been clear positives. Earlier data showed an improvement in manufacturing sentiment, albeit from a low base.

- Spot USD/TWD is holding under 30.00 at this stage, little changed for the session. The Taiex is around flat, while alter on Q1 Taiwan GDP prints. The market expects a 5.4%y/y outcome, versus 5.37% prior.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 28/05/2025 | 0600/0800 | ** | Retail Sales | |

| 28/05/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 28/05/2025 | 0645/0845 | ** | PPI | |

| 28/05/2025 | 0645/0845 | *** | GDP (f) | |

| 28/05/2025 | 0645/0845 | ** | Consumer Spending | |

| 28/05/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/05/2025 | 0755/0955 | ** | Unemployment | |

| 28/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kahkari | ||

| 28/05/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 28/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 28/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/05/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/05/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/05/2025 | 1500/1600 | BOE's Pill on monetary policy panel at Austria National Bank / SUERF | ||

| 28/05/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 28/05/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/05/2025 | 1800/1400 | FOMC Minutes | ||

| 28/05/2025 | 1800/1400 | *** | FOMC Minutes | |

| 28/05/2025 | 0000/2000 | New York Fed's John Williams | ||

| 29/05/2025 | 0130/1130 | * | Private New Capex and Expected Expenditure | |

| 29/05/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 29/05/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 29/05/2025 | 0900/1000 | BOE's Breeden opening remarks at conference on non-bank financial sector and financial stability | ||

| 29/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 29/05/2025 | 1230/0830 | * | Current account | |

| 29/05/2025 | 1230/0830 | * | Payroll employment | |

| 29/05/2025 | 1230/0830 | *** | GDP | |

| 29/05/2025 | 1230/0830 | Richmond Fed's Tom Barkin |