ASIA STOCKS: The Period of Big Inflows Appears to have Stalled

After an exceptional period of inflows into the major markets, it appears that this trend has stalled for now as constant daily flows are interrupted with outflows.

- South Korea: Recorded outflows of -$57m yesterday, bringing the 5-day total to -$16m. 2025 to date flows are -$11,527. The 5-day average is -$3m, the 20-day average is +$76m and the 100-day average of -$115m.

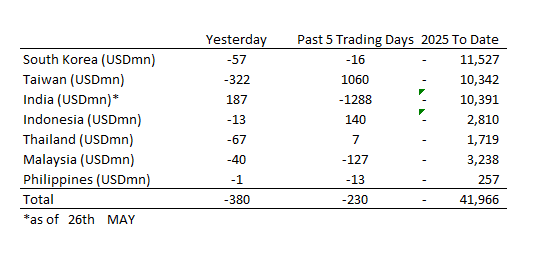

- Taiwan: Had outflows of -$322m as yesterday, with total inflows of +$1,060m over the past 5 days. YTD flows are negative at -$10,342. The 5-day average is +$212m, the 20-day average of +$414m and the 100-day average of -$115m.

- India: Had inflows of +$187m as of the 26th, with total outflows of -$1,288m over the past 5 days. YTD flows are negative -$10,391m. The 5-day average is -$258m, the 20-day average of +$153m and the 100-day average of -$115m.

- Indonesia: Had outflows of -$13m as of yesterday, with total inflows of +$140m over the prior five days. YTD flows are negative -$2,810m. The 5-day average is +$28m, the 20-day average +$13m and the 100-day average -$31m.

- Thailand: Recorded outflows of -$67m as of yesterday, inflows totaling +$7m over the past 5 days. YTD flows are negative at -$1,719m. The 5-day average is +$1m, the 20-day average of -$4m and the 100-day average of -$17m.

- Malaysia: Recorded outflows of -$40m as of yesterday, totaling -$127m over the past 5 days. YTD flows are negative at -$3,238m. The 5-day average is -$28m, the 20-day average of +$27m and the 100-day average of -$22m.

- Philippines: Saw outflows of -$1m yesterday, with net outflows of -$13m over the past 5 days. YTD flows are negative at -$257m. The 5-day average is -$3m, the 20-day average of +$2m the 100-day average of -$3m.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Quiet Start

TYM5 has traded a little higher with a range of 111-18 to 111.22+ during the Asia-Pacific session. It last changed hands at 111-19, up 0.03 from the previous close.

- The US 10-year yield is a little higher, dealing around 4.24%, up from its close around 4.23%

- The US 2-year yield is up, dealing around 3.75%, up from its close around 3.748%.

- Risk has struggled to hold onto its gains leaking lower in Asia as the market gives back some of its gains made on Friday night.

- Bloomberg - “ Big tech earnings earnings estimates may be way too high, with analysts projecting an average of 15% profit growth for the magnificent Seven in 2025, despite recent market turmoil. Any hint of a shortfall in Microsoft, Apple, Meta and Amazon’s results this week will probably “cause a further selloff”.”

- US TSY: Block - Sell TYM5, SELL 3020 of TYM5 traded at 111-19+, post-time 01:36:55 BST (DV01 $193,162).

- The 10-year Yield, has put in a lower high around 4.40% and is attempting to break through the recent support around 4.25%. Should this give way the next support is towards the 4.10 area which should find supply once more as the market will continue to look for higher term premium while uncertainty remains elevated.

- Data/Events : US GDP, ISM Manufacturing, NFM payrolls the main events this week. Trump’s first 100 days in office speech tomorrow.

JGBS: Subdued Data-Light Session, BoJ Policy Decision Thursday

At the Tokyo lunch break, JGB futures are stronger and Tokyo session highs, +16 compared to the settlement levels.

- (MNI) The BoJ board is expected to keep its 0.5% policy rate unchanged at the two-day meeting ending May 1, as policymakers monitor the economic and inflationary impact of recent U.S. trade policies and volatile markets.

- Uncertainty about the severity of the economic downturn caused by tariffs, along with the impact of the dollar/yen exchange rate, is making it difficult for bank officials to draft the likely scenarios they will present at the board meeting.

- Greater clarity on the economic outlook – particularly regarding the U.S. economy and Fed policy – is expected by July, when the BOJ releases its updated medium- to long-term growth and inflation forecasts. Should the U.S. fall into recession, it would likely remove any chance of a BOJ rate hike this year.

- Cash US tsys are flat to 1bp cheaper, with a flattening bias, in today’s Asia-Pac session after Friday’s solid gains.

- Cash JGBs are flat to 2bps richer out to the 20-year benchmark and 1-2bps cheaper beyond. The benchmark 10-year yield is 2.0bps lower at 1.322% versus the cycle high of 1.596%.

- Swap rates are 1-3bps lower. Swap spreads are mixed.

CNH: USD/CNH Ticks Up, PBoC Vows To Keep Yuan Basically Stable

USD/CNH is holding close to session highs (7.2986), last near 7.2950/50. We are modestly higher, in line with a tick up in USD index levels. The broader USD index though, USD/CNH remains within recent ranges. Support remains evident in the low 7.2800 region, while recent highs remain intact close to 7.3350.

- The headlines crossing from the press conference aimed at stabilizing the economy and supporting the jobs market haven't shifted market sentiment greatly. It still appears more monetary stimulus is on the way, but the authorities will enact such moves in a timely manner. Contingency plans will also be put in place.

- No doubt the authorizes are waiting to see how the trade/tariff conflict with the US unfolds. The NRDC stated it was still confident of hitting this year's growth target.

- On the yuan, the PBOC vowed to keep the currency basically stable.

- the bias for the currency is likely to remain for any fresh depreciation pressures to remain gradual/steady, with focus on where tariff levels end up. A higher average tariff rate for China compared to the rest of the world is still likely to bias CNH weaker on key crosses like EUR and CNH.

- In the equity space today, trends have been very steady as has been the case in the past few weeks. The CSI 300 remains close to 3800 in latest dealings.