MNI EUROPEAN MARKETS ANALYSIS: Japan Markets Up on Trade Deal

- The NIKKEI is up over +3.5% today on the Trump Headlines that a trade deal has been reached between the US and Japan.

- This comes on reports that the Japanese PM will resign as soon as this month.

- Treasury Secretary Bessent has offered his support to Chairman Powell.

- Canadian PM Carney used very strong language about the likelihood of reaching a trade deal by August 1.

MARKETS

US TSYS: Asia Wrap - Yields Move Higher, Led By The Long-End

The TYU5 range has been 111-06 to 111-10+ during the Asia-Pacific session. It last changed hands at 111-07, down 0-06 from the previous close.

- The US 2-year yield has edged higher trading around 3.844%, up 0.01 from its close.

- The US 10-year yield has moved higher trading around 4.365%, up 0.02 from its close.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, expect supply around 4.30/35% first up. A close back below 4.30% would begin to get the bulls excited once more and the chopfest within the range will continue.

- Nick Timiraos on X: Goldman: "Market participants seem to agree that the risk to Fed independence is rising, as 5-year 5-year forward inflation swaps have recently decoupled higher from their prior close relationship with the 2-year note yield."

- Bloomberg - “Lawrence Summers backed Scott Bessent’s questioning of the Fed’s non-monetary policy activities, saying that there were some areas that are distinct from the broader issue of central bank independence.”

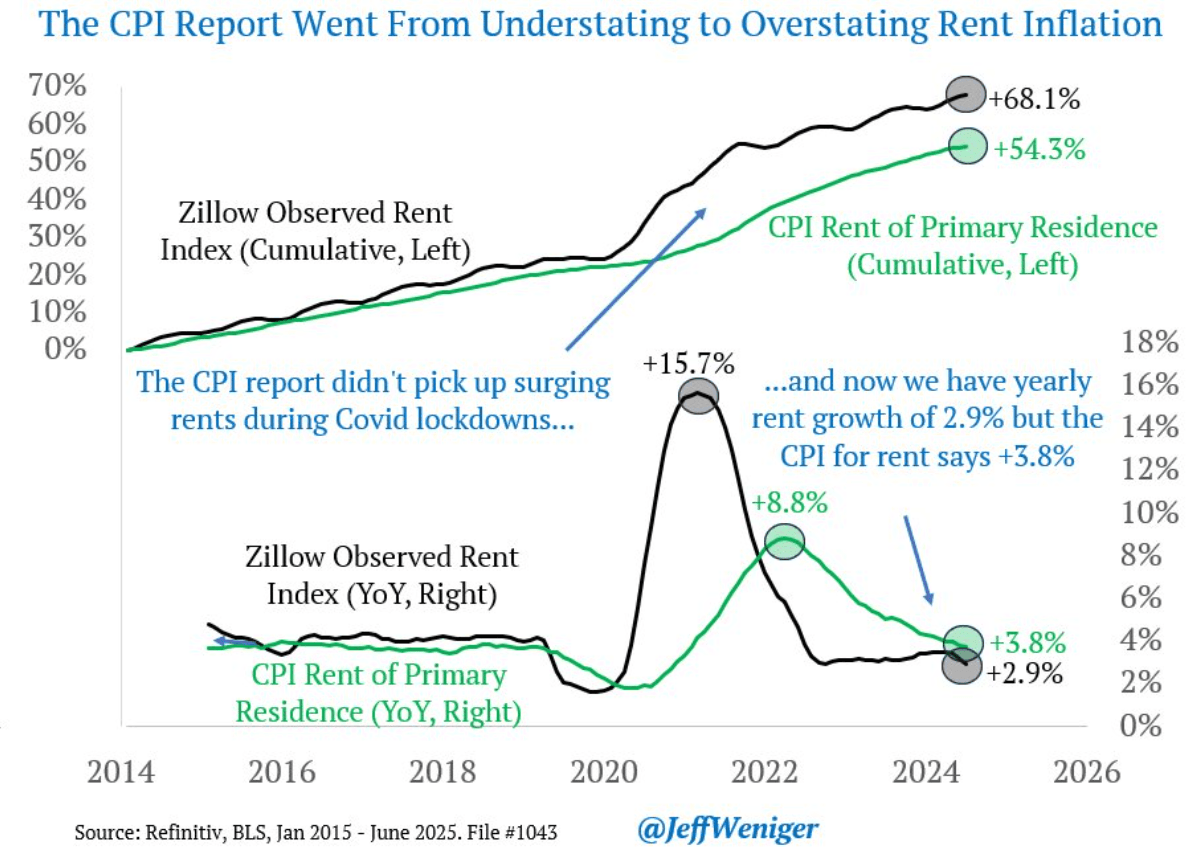

- Jeff Weniger on X: “Understand this and you'll be ahead of 99% of the public on official inflation dynamics. Similar to work by my WisdomTree colleague @JeremyDSchwartz, we see that the CPI for rent is still playing catch-up after the Covid money splash. The CPI reports of 2025 are overstating rent and will continue to do so until the catch-up is complete.” See Graph Below.

Data/Events: MBA Mortgage Applications, Existing Home Sales

Fig 1: CPI Vs CPI For Rent

Source: MNI/@JeffWeniger/Refinitiv

JGBS: 40Y Leads Market Cheaper After Poor Auction

JGB futures are sharply lower, -79 compared to settlement levels, but off the session’s worst levels.

- Today's focus has been on the US-JN trade deal. Japan will pay a 15% reciprocal tariff to the US, which is lower than the 25% rate that had been threatened.

- Kelly Eckhold (Westpac) on LinkedIn: "Trump trade deals progressing. Japan interestingly opens up the rice market in exchange for their tariff being reduced to 15%. That's a huge change for Japan, where rice imports have not been allowed."

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs are 4-8bps cheaper across benchmarks, with the benchmark 40-year yield underperforming after today's supply.

- Demand for today’s 40-year bond issuance was weak, with the high yield clearing well above dealer expectations. According to a Bloomberg survey, the market anticipated a yield of 3.35%, while the actual result came in at 3.375%. The auction’s cover ratio also declined to 2.1273x from 2.2114x at the previous issuance.

- Swap rates are 4-7bps higher, led by the belly of the curve. Swap spreads are mostly wider.

- Tomorrow, the local calendar will see S&P Global PMIs (P).

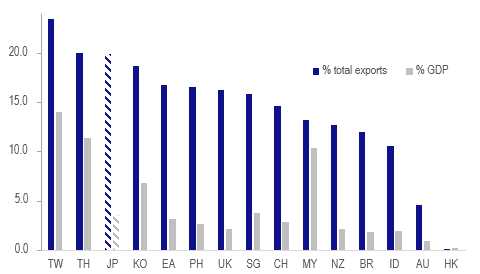

TARIFFS: Trade Deal Relief For Japan’s Vehicle Manufacturers

A trade deal has been reached between the US and Japan ahead of the August 1 deadline, which has been seen as positive by markets with the Nikkei up 2.4% but USDJPY has given up its earlier gains and is little changed at 146.64. Imports from Japan, including autos, will face a 15% tariff down from the 24% announced in April but higher than the current average below 5%. This lower rate is in exchange for $550bn of Japanese investment in the US.

- Japan is a key US ally and so a deal was expected but the US’ 2024 merchandise deficit of $69.4bn with Japan, larger than the deficit with Canada, made it a target of President Trump’s protectionism. 4.5% of 2024 US imports came from Japan, the fifth highest.

- Japan has one of the higher export shares to the US at 19.9% of total goods shipped in 2024 but at only 3.5% of GDP, it has a relatively lower impact on the economy.

Exports to the US (ex NAFTA) 2024 %

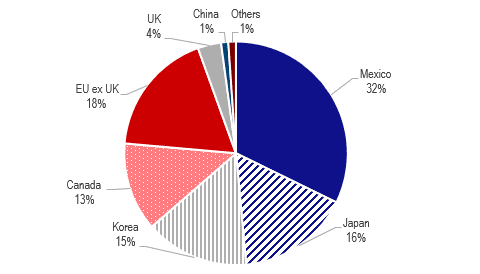

- However, certain sectors are highly exposed, especially autos. Japan is the second largest source of US personal vehicle & light truck imports at 16% of the total only behind Mexico’s 32%, and 8% of parts. Japanese autos will now face the agreed 15% duty below the universal 25% against all vehicle imports and as a result Toyota and Mazda shares have rallied.

US imports personal vehicles & light trucks % total 2024

- Japan frontloaded shipments to the US through Q1 and Bloomberg container ship tracking data signal that continued in June ahead of the earlier July 9 deadline, but vessels departing for the US are down in July. However, the value of exports to the US fell 11.4% y/y in June after rising 10.5% y/y in February.

JAPAN: Local Media States PM Ishiba To Resign In August

Headlines have crossed from local newspaper Mainichi that PM Ishiba will resign by the end of August. Via Rtrs: "Japan's Prime Minister Shigeru Ishiba has made up his mind to resign, Mainichi newspaper reported on Wednesday."

- Earlier PM Ishiba wouldn't be drawn on speculation around his future, stating that he would assess the US-Japan trade deal details before making any decision.

- Still, in the aftermath of the weekend upper house result, which saw the ruling LDP coalition lose its majority, Ishiba's future has been speculated on.

- His removal odds per Polymarket has remained elevated this week, but sub recent highs.

- The market reaction has been for USD/JPY to rise, testing up through 147.00 (highs were at 147.20, but we sit back near 147.00 in latets dealings)Japan equities have also rallied further.

- JGB yields are higher across the curve so far today, with focus on the 40yr debt auction in a little while. Risks around fiscal slippage for Japan will remain elevated if Ishiba resigns.

AUSSIE BONDS: Slightly Richer, New Oct-36 Bond Issued, RBA Gov Speech Tomorrow

ACGBs (YM flat & XM +1.5) are slightly stronger but off Sydney session bests.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's modest rally.

- Cash ACGBs are flat to 2bps richer with the AU-US 10-year yield differential at -8bps.

- The AOFM announced that the issue by syndication of the new 4.25% 21 October 2036 Treasury Bond has been priced at a yield to maturity of 4.36 per cent. The issue size is $16 billion in face value terms. There was a total of $61.9 billion of bids at the final clearing price.

- (Bloomberg) -- Australia's economy will expand 0.5% in 2Q, according to the latest median estimate from a Bloomberg News survey conducted from July 17 to July 22.

- The bills strip is slightly mixed.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in August is given a 100% probability, with a cumulative 65bps of easing priced by year-end.

- Tomorrow, the local calendar will see S&P Global PMIs (P) and a speech by RBA Governor Michele Bullock, titled `The RBA’s Dual Mandate - Inflation and Employment' at the Anika Foundation.

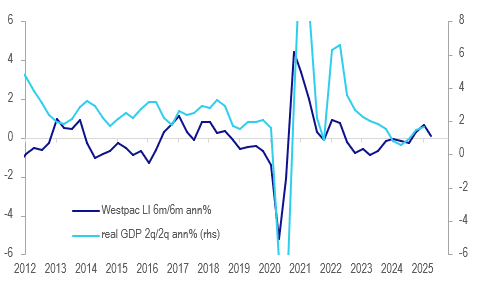

AUSTRALIA DATA: Westpac Lead Indicator Signals Around Trend Growth

The Westpac lead indicator for June fell 0.03% m/m following an upwardly-revised 0.05% rise. The 6-month rate, which leads detrended growth by 3 to 9 months, is hovering just above zero signalling that growth is likely to return to around trend towards year end. Westpac believes that sluggish growth and the Q2 CPI outcome on July 30 will enable the RBA to cut 25bp on August 12 but it will maintain a “gradual easing cycle”.

- The 6m/6m annualised change in the lead indicator printed at 0.03% in June down from 0.11%.

- Weaker commodity prices in AUD, consumer confidence, hours worked drove the moderation from December’s +0.33%. However, the ASX, lower rates and US IP have been supportive.

- Westpac is forecasting GDP growth of 1.7% in 2025 up only slightly from 2024’s 1.3%.

Australia Westpac lead indicator vs real GDP %

BONDS: NZGBS: Closed With A Modest Twist-Flattener

NZGBs closed showing a twist-flattener, with benchmark yields 1bp higher to 2bps lower.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's modest rally.

- Today’s focus has been on the US-JN trade deal. Japan will pay a 15% reciprocal tariff to US Trump notes. This is lower than the 25% rate which had been threatened.

- (Bloomberg) -- RBNZ publishes new residential mortgage lending data for June, on its website. Lending to all borrowers NZ$8.26b, Gains 47% y/y, Increases 3.5% m/m after seasonal adjustment: RBNZ.

- Satish Ranchhod (Westpac) on LinkedIn: "Inflation in New Zealand has picked up to 2.7%, and it's on course to rise back up to around 3% by the end of this year, it's a mixed picture under the surface.”

- Swap rates closed flat to 2bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed little changed across meetings. 21bps of easing is priced for August, with a cumulative 37bps by November 2025.

- Tomorrow, the local calendar will see a speech from the RBNZ's Conway on tariffs and the economy.

- Tomorrow, the NZ Treasury plans to sell NZ$225mn of the 3.0% Apr-29 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 5.0% May-54 bond.

FOREX: Asia FX Wrap - BBDXY Looks Heavy Below 1200

The BBDXY has had a range of 1195.19 - 1197.06 in the Asia-Pac session, it is currently trading around 1196, +0.05%. The USD again fell very easily overnight, aided by the move lower in US yields. The market is much more comfortable selling USD’s, while below 1220 rallies should continue to find supply. What stands out overnight though is the USD could not move higher while the risk of Powell being removed hung over its head, last night both Trump and Bessent pulled back from that scenario and intimated Powell would complete his term. US yields have moved lower as a result taking the USD with it, does that mean the USD now goes down in all scenarios ?

- EUR/USD - Asian range 1.1731 - 1.1749, Asia is currently trading 1.1735. The pair bounced off its first support around the 1.1600 area. The price still looks a little stretched in the short term, first support around 1.1550/1600 then more importantly the 1.1450 area.

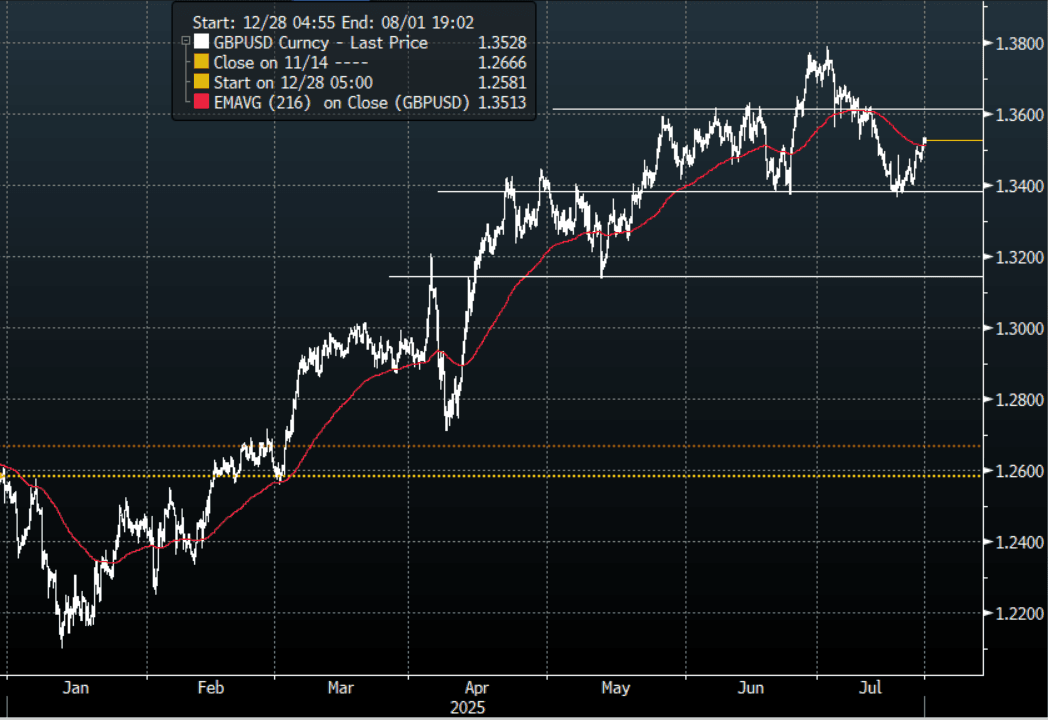

- GBP/USD - Asian range 1.3517 - 1.3535, Asia is currently dealing around 1.3525. The support around 1.3350/1.3400 has proved to be solid first up. Bounces back towards 1.3500/1.3550 should now see offers initially. While the support holds the market will be encouraged to continue to play from the long side.

- USD/CNH - Asian range 7.1592 - 7.1727, the USD/CNY fix printed 7.1414, Asia is currently dealing around 7.1600. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.25%, Gold $3423, US 10-Year 4.364%, BBDXY 1206, Crude oil $65.54

- Data/Events : EZ Consumer Confidence

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

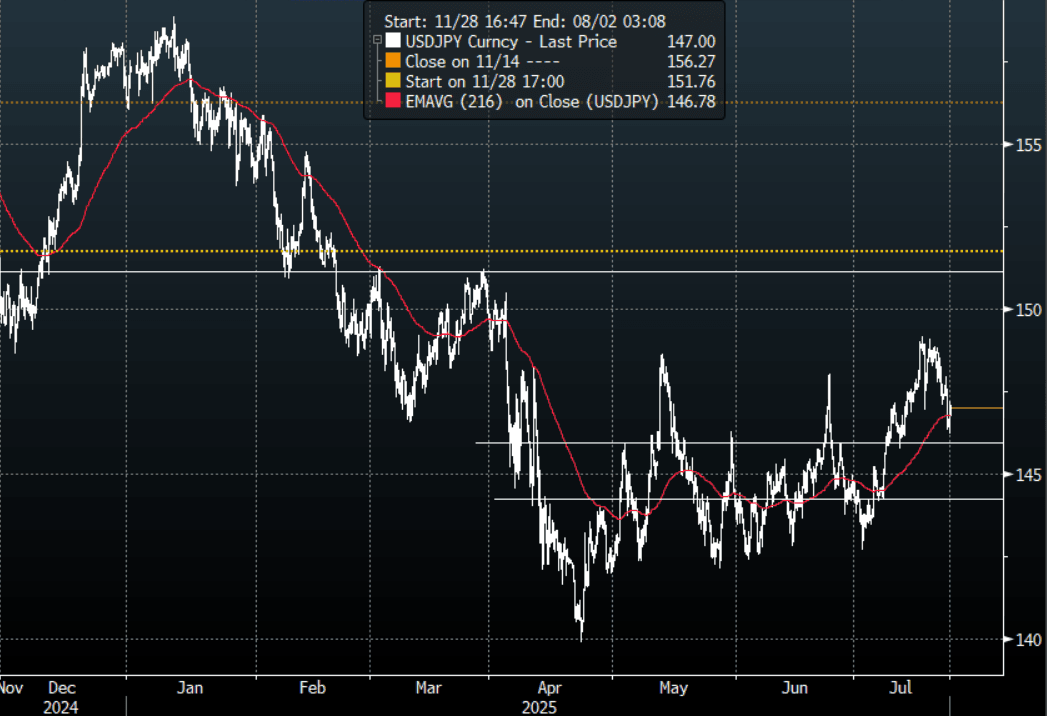

JPY: Asia Wrap - USD/JPY Finds A Base, Probes Above 147.00 On Trade Deal

The Asia-Pac USD/JPY range has been 146.20 - 147.20, Asia is currently trading around 147.00, +0.25%. USD/JPY continues to frustrate the market and has given back a large portion of its recent gains, around 250 points in 2 days. The move lower in US yields is providing serious headwinds for the pair and the USD seems to be floundering in all scenarios. We are probing the first support around 146.50 this morning where some demand should be seen first up as the market digests the trade deal with the US, next level is the pivotal 144.00/145.00 area.

- Kelly Eckhold(Westpac) on LinkedIn: “Trump trade deals progressing. Japan interestingly opens up the rice market in exchange for their tariff being reduced to 15%. That’s a huge change for Japan where rice imports have not been allowed.”

- "ISHIBA: DEAL WON'T SACRIFICE JAPAN AGRICULTURE AT ALL, WILL INCREASE US RICE IMPORTS WITHIN EXISTING BRACKET" - BBG

- MNI: BOJ's Uchida - Gradual Rate Hike, But No Pace Signalling. TOKYO - Bank of Japan Deputy Governor Uchida stated on Wednesday that the central bank will maintain its approach of gradually raising the policy interest rate, citing persistently low real interest rates. However, he offered no guidance on the timing or pace of future rate hikes, citing elevated levels of uncertainty.

- JAPAN Local Media States PM Ishiba To Resign In August : Headlines have crossed from local newspaper Mainichi that PM Ishiba will resign by the end of August. Via Rtrs: "Japan's Prime Minister Shigeru Ishiba has made up his mind to resign, Mainichi newspaper reported on Wednesday." A later headline from the Yomiuri newspaper reported he may announce resignation as soon as this month.

- "JAPAN 40-YEAR BOND BID-COVER RATIO 2.13 VS 12-MONTH AVG 2.48, SALE DRAWS WEAKEST DEMAND RATIO SINCE 2011, BOND FUTURES HOLD LOSS AFTER 40-YEAR DEBT AUCTION" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($734m), 148.00($902m).Upcoming Close Strikes : 147.50($1.5b July 24), 145.00($1.15bm July 25) - BBG.

- CFTC data shows Asset managers starting to reduce JPY longs more aggressively +71610, while leveraged funds have started to build into a new short JPY position -12606.

Fig 1 : USD/JPY Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Moves Higher As Risk Reacts Positively To Trade Deal

The AUD/USD has had a range of 0.6548 - 0.6569 in the Asia- Pac session, it is currently trading around 0.6565, +0.15%. The pair pushed higher in the New York session as the USD came back under pressure with US yields pushing lower. The follow through below 0.6500 was quite disappointing for AUD shorts but with Stocks making new highs and risk outperforming, it makes it a hard environment for AUD/USD to collapse in. The pair looks to be consolidating in a 0.6450 - 0.6600 range as the market awaits a catalyst to provide clearer direction.

- AUSTRALIA DATA: Westpac Lead Indicator Signals Around Trend Growth. The Westpac lead indicator for June fell 0.03% m/m following an upwardly-revised 0.05% rise. The 6-month rate, which leads detrended growth by 3 to 9 months, is hovering just above zero signalling that growth is likely to return to around trend towards year end. Westpac believes that sluggish growth and the Q2 CPI outcome on July 30 will enable the RBA to cut 25bp on August 12 but it will maintain a “gradual easing cycle”.

- (Bloomberg) -- Australia’s economy will expand 0.5% in 2Q, according to the latest median estimate from a Bloomberg News survey conducted from July 17 to July 22.

- "AUSTRALIAN PRUDENTIAL REGULATION AUTHORITY - KEEPS ITS MACROPRUDENTIAL POLICY SETTINGS STEADY" - RTRS

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6525(AUD603m), 0.6500(AUD445m), 0.6580(AUD403m) . Upcoming Close Strikes : none - BBG

- CFTC Data shows Asset managers have maintained their shorts -38267, the Leveraged community added slightly to their shorts to -20048.

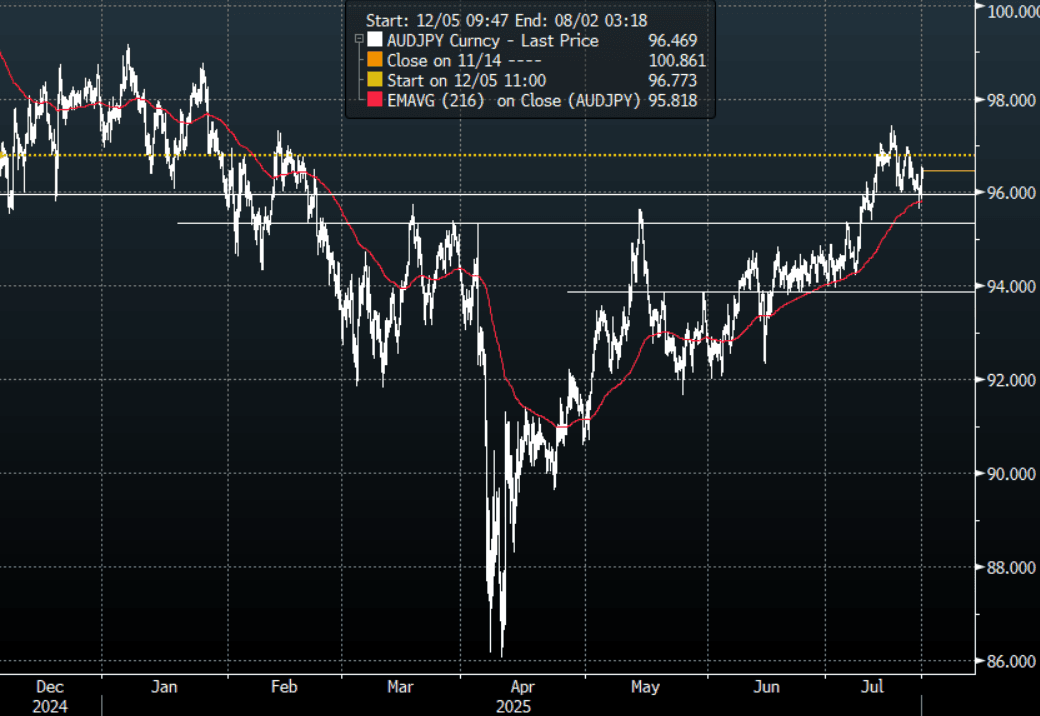

- AUD/JPY - Today's range 95.85 - 96.55, it is trading currently around 96.45, +0.35%. The pair continued to trade heavily overnight. The support has held between 95.00 - 96.00, demand has materialized first up, and the trade deal between the US and Japan should provide it with some tailwinds initially.

Fig 1: AUD/JPY spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

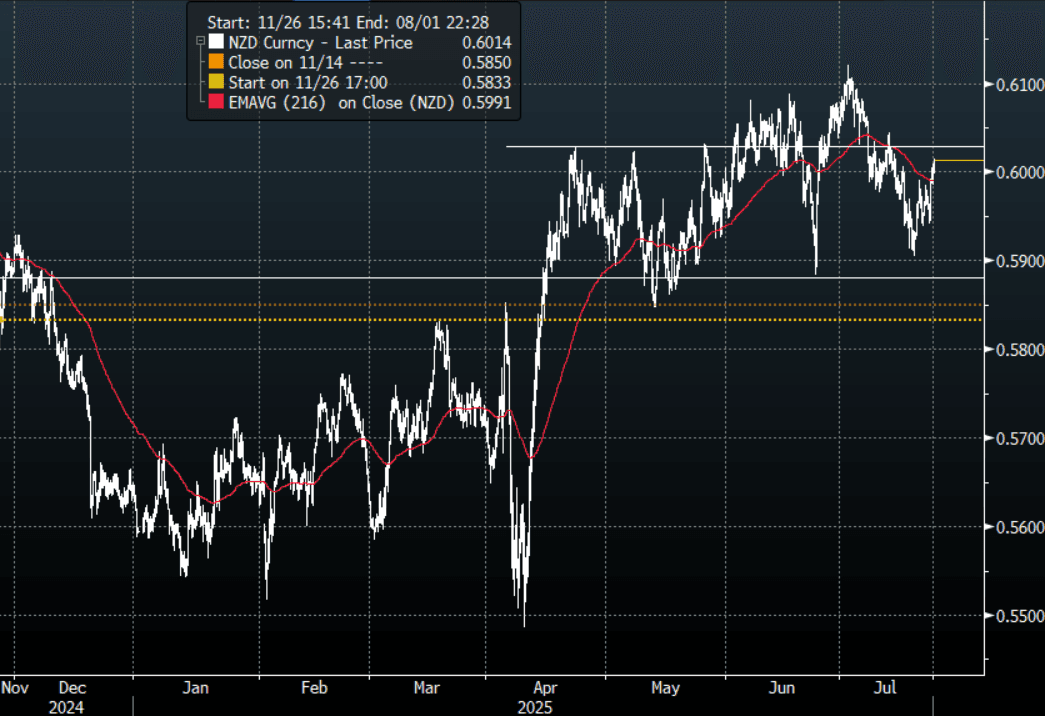

NZD: Asia Wrap - NZD/USD Pushing Back Above 0.6000, Can It Put A Base In?

The NZD/USD had a range of 0.5985 - 0.6014 in the Asia-Pac session, going into the London open trading around 0.6015, +0.20%. The pair had a decent move higher in the New York session as the USD came back under pressure with US yields pushing lower. Depending what your view is this 0.6020/0.6050 area looks an attractive fade, the danger though is the USD which is looking sickly once more and should it capitulate the NZD could build momentum higher again. Price will need a sustained break back above the 0.6025/50 area to signal a potential base might be in place.

- Satish Ranchhod(Westpac) on LinkedIn: “Inflation in New Zealand has picked up to 2.7%, and it’s on course to rise back up to around 3% by the end of this year, it’s a mixed picture under the surface. With softness in demand, we are seeing lower inflation in parts of the domestic economy, especially the housing sector. However, we’re continuing to see large increases in administered prices like council rates and electricity charges. At the same time, import prices are starting to push higher again. We continue to expect another 25bp cut from the RBNZ in August. However, with headline inflation pushing higher, the RBNZ will be cautious about the extent and timing of any further rate cuts.”.

- (Bloomberg) -- RBNZ publishes new residential mortgage lending data for June, on its website. Lending to all borrowers NZ$8.26b, Gains 47% y/y, Increases 3.5% m/m after seasonal adjustment: RBNZ.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6010(NZD302m July 24). - BBG

- CFTC Data shows Asset Managers slightly reduced their newly built longs in NZD +8192, the Leveraged community has continued to reduce their shorts last week -6744.

- AUD/NZD range for the session has been 1.0915 - 1.0940, currently trading 1.0920. The cross moved higher in response to the NZ CPI. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Japan Markets Surge, Led By Autos, On US 15% Tariff Deal

Japan stocks are the standout, as headlines cross of a US-Japan trade deal, which will see the reciprocal tariff rate set at 15%. This includes the important auto sector as well. Benchmark Japan indices were last up +3%. US equity futures have edged higher, but Eminis are only +0.20% firmer at this stage. EU stock futures are doing better, last around 1.15% higher for Euro Stoxx.

- The trade deal is seen as a win for Japan, particularly the 15% auto tariff (after 25% was threatened by US President Trump). Other details include $550bn of Japan investment into the US, although specific projects/timelines for this weren't apparent. Headlines also crossed that PM Ishiba plans to resign in August, which gave markets another leg higher. This could prompt further fiscal support for the economy. The Topix is up over 3%, last above 2925, which is fresh highs back to July last year. The auto and transport sub index is up close to 10%.

- China and Hong Kong stocks continue to rally as well. The HSI is up over 1%, while the CSI 300 has gained close to 0.75%, putting the index near 4150. General positive sentiment around US-China trade/relations is aiding sentiment. US Tsy Secretary Bessent will meet China officials in Stockholm next week, with the aim of extending the trade truce and expanding talks. US President Trump also stated overnight he may meet China President XI in the not too distant future (per BBG).

- Taiwan markets are firmer, the Taiex up over 1.10%, but South Korea's market has struggled for positive momentum as it can't sustain moves above 3200.

- In SEA, Thailand stocks are up strongly, last over +2% firmer, putting the index comfortably above the 1200 level. Indonesian stocks are also higher, along with other bourses in the region.

OIL: Crude Supported By US-Japan Deal But Focus Now On China & EU

While oil markets are off their highs following the announcement of a US-Japan trade deal, they are still up today but continue to range trade. WTI is 0.4% higher at $65.54/bbl after reaching $65.82 earlier, while Brent is +0.3% to $68.77/bbl following a peak of $69.10. The USD index is slightly higher.

- US imports from Japan, including autos, will face a 15% tariff down from the 24% announced in April but higher than the current average below 5%. This lower rate is in exchange for $550bn of Japanese investment in the US.

- Attention remains on negotiations with the EU and China. Treasury Secretary Bessent is scheduled to meet China officials in Stockholm next week with the aim of extending the current hold on tariffs beyond August 12. The talks may also include China’s continued consumption of Russian and Iranian crude.

- Industry-based data showed a small US crude inventory drawdown with a larger one for gasoline but distillate was higher. The official EIA data is out later today and while the supply/demand balance remains a concern is likely to be a focus.

- Malaysia has decided not to cut fuel subsidies and the price of RON95 fuel will actually fall to MYR 1.99/L as part of a package to support households.

- Later June US existing home sales and preliminary July euro area consumer confidence print.

GOLD: US-Japan Trade Deal Boosts Risk Appetite Weighing On Gold

Gold prices have trended moderately lower today following the conclusion of a trade deal between Japan and the US lifting optimism that others, especially the EU and China, may also be able to reach an agreement before August 1. Bullion had a strong start to the week rising almost 2.5% over Monday/Tuesday. Today it is down 0.2% to $3423.6/oz but off the intraday low of $3419.27 with the BBDXY USD index and US yields slightly higher.

- Gold continues to be supported by concerns over Fed independence.

- Silver is also lower at -0.1% to $39.25 after rising to $39.38 but off today’s low of $39.13. It was up almost 3% over Monday/Tuesday.

- US imports from Japan, including autos, will face a 15% tariff down from the 24% announced in April but higher than the current average below 5%. This lower rate is in exchange for $550bn of Japanese investment in the US.

- Treasury Secretary Bessent is scheduled to meet China officials in Stockholm next week with the aim of extending the current hold on tariffs.

- The US-Japan trade deal has driven an improvement in risk appetite with equities higher (Nikkei +3.2%, Hang Seng +1.1% & S&P e-mini +0.2%). Oil prices are higher with WTI +0.3% to $65.48/bbl and copper up 0.9%.

- Later June US existing home sales and preliminary July euro area consumer confidence print.

CHINA: PBOC Provides Update on Foreign Ownership of Bonds

- The PBOC issued a release showing that foreign institutions held CNY4.3 trillion of bonds via the interbank market.

- This accounts for 2.5% of total 'custody volume' of bonds.

- Overseas institutions hold CNY2.1tn of CGBs, CDs CNY1.15tn, Policy Bonds CNY810bn.

- There are over 1,170 of overseas institutions who have access to the interbank market with just over 70% via Bond Connect in Hong Kong.

- The release comes days after a China Daily article suggesting that China will over time move away from investing US Treasuries.

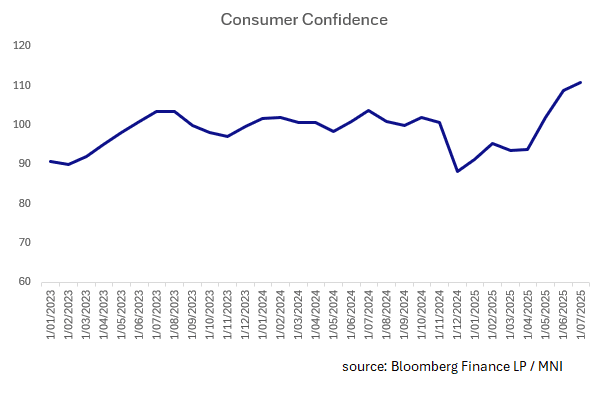

SOUTH KOREA: Koreans Responding to Policy

- South Korea's consumers appear to be responding to the various policy measures implemented in recent weeks.

- A combination of supplementary budgets from the new government, rate cuts, cash handouts known as 'consumption coupons' all the while the KOSPI has performed well up +32.11% year to date and the Won 6% better since the wides of April.

- The Consumer Confidence rose to 110.8 from 108.7 and the highest print since 2017.

- Households’ inflation expectation for next 12 months rose to 2.5%, Bank of Korea says in a statement.

- Survey based on responses from 2,286 households across the nation, conducted between July 8-15: statement

- Households’ inflation expectation for next 12 months rose to 2.5%.

- Over the last few weeks, the bond market has moved to take out interest rate cuts already priced in. Back in March swaps had priced in over 30bps of cuts on a 12 month forward looking basis and those cuts have all but been priced out since.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 23/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 23/07/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/07/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 23/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 23/07/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 23/07/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 24/07/2025 | - | European Central Bank Meeting | ||

| 24/07/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 24/07/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 24/07/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 24/07/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 24/07/2025 | 0700/0900 | ** | PPI | |

| 24/07/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 24/07/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 24/07/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 24/07/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 24/07/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 24/07/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 24/07/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 24/07/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/07/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 24/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/07/2025 | 1230/0830 | ** | Retail Trade | |

| 24/07/2025 | 1230/0830 | ** | Retail Trade | |

| 24/07/2025 | 1245/1445 | ECB Press Conference | ||

| 24/07/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/07/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/07/2025 | 1400/1000 | *** | New Home Sales | |

| 24/07/2025 | 1430/1030 | ** | Natural Gas Stocks |