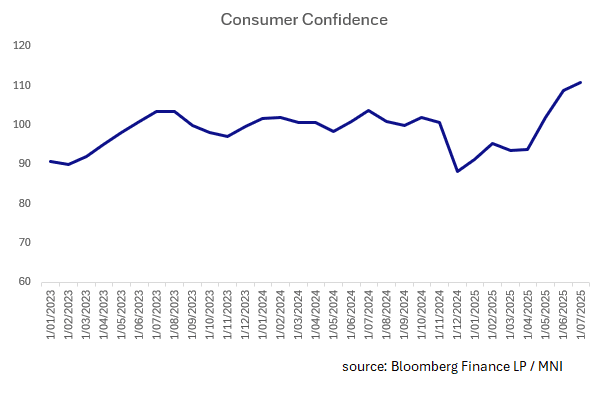

SOUTH KOREA: Koreans Responding to Policy

- South Korea's consumers appear to be responding to the various policy measures implemented in recent weeks.

- A combination of supplementary budgets from the new government, rate cuts, cash handouts known as 'consumption coupons' all the while the KOSPI has performed well up +32.11% year to date and the Won 6% better since the wides of April.

- The Consumer Confidence rose to 110.8 from 108.7 and the highest print since 2017.

- Households’ inflation expectation for next 12 months rose to 2.5%, Bank of Korea says in a statement.

- Survey based on responses from 2,286 households across the nation, conducted between July 8-15: statement

- Households’ inflation expectation for next 12 months rose to 2.5%.

- Over the last few weeks, the bond market has moved to take out interest rate cuts already priced in. Back in March swaps had priced in over 30bps of cuts on a 12 month forward looking basis and those cuts have all but been priced out since.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Modestly Richer After US Strikes Iran's Nuclear Sites

ACGBs (YM +2.0 & XM +0.5) are modestly higher following the weekend's US bombing of Iran’s nuclear sites.

- The US said that it destroyed the Fordow, Natanz and Isfahan nuclear sites. US President Trump said that Iran must now agree to peace but Iran’s President Pezeshkian threatened the US and said it “must receive a response for their aggression” while others officials said that there had not been “any irreversible damage” and that knowledge “can’t be destroyed by bombing”.

- Oil prices have begun today’s trading sharply higher following US strikes on Iranian nuclear sites yesterday.

- S&P Global PMIs(P) for June have printed: Manf Index unchanged at 51 from May; Services Index rises to 51.3 from 50.6 in May; and Composite Index rises to 51.2 from 50.5 in May.

- Cash ACGBs are flat to 2bps richer with the AU-US 10-year yield differential -20bps.

- The bills strip has richened slightly, with pricing flat to +2.

- RBA-dated OIS pricing is modestly softer across meetings today. A 25bp rate cut in July is given an 83% probability, with a cumulative 76bps of easing priced by year-end.

- This week, AOFM plans to sell A$1000mn of the 1.75% 21 November 2032 bond today and A$1000mn of the 3.50% 21 December 2034 bond on Wednesday.

BONDS: NZGBS: Richer After US’s Weekend Bombing Of Iran

In local morning trade, NZGBs are 3-4bps richer after the long weekend and following the weekend's US bombing of Iran’s nuclear sites.

- President Trump has followed up with comments this morning that could see the US look for a regime change in Iran. "TRUMP ON IRAN: WHY WOULDN'T THERE BE A REGIME CHANGE, IF THE CURRENT REGIME CAN'T MAKE IRAN GREAT, WHY NO CHANGE?"(BBG). This would imply a longer and more sustained US involvement in the conflict.

- Oil prices have begun today’s trading sharply higher following yesterday's US strikes on Iranian nuclear sites. Following this development, concerns have escalated that oil supplies from the region will be impacted by the conflict. WTI is up 2.5% to $75.70/bbl after the initial high of $78.40, above the $75.74 initial resistance.

- "Among Group-of-10 commodity currencies, the Kiwi "is the only energy importer and most vulnerable if Middle East oil supply is impacted more severely," wrote Bank of America. "Being a large oil importer, the Asia region remains most vulnerable to such a shock," the BofA team notes."

- Swap rates are 3bps lower.

- RBNZ dated OIS pricing is little changed across meetings. 4bps of easing is priced for July, with a cumulative 26bps by November 2025.

- Today, the local calendar will be empty.

JPY: USD/JPY - The Move In Oil Is Challenging The Long JPY Trade

USDJPY - Struggles To Hold Gains, Testing 145.00 Support

The overnight range was 145.25 - 146.22, Asia is currently trading around 146.40. USD/JPY is attempting to break through the 146.50 area this morning in reaction to the US bombing and the implications of potential extended US involvement in the conflict. The Market is caught long JPY and the implications of a higher oil price is challenging their conviction, as this is overriding the safe haven status the JPY would normally be enjoying when risk turns lower.

- (Bloomberg) - “A geopolitically driven, supply-side shock to oil prices presents a key risk to a short squeeze in USD given its consensus nature – perhaps 2% or more,” analysts at Morgan Stanley. A supply-driven oil price increase could trigger a short squeeze to consensus USD shorts but medium-term fundamentals still suggest fading this dollar strength.”

- "Asian currencies are likely to see further downside in the near-term, amid rising vulnerability to oil prices"(BBG).

- USD/JPY price action continues to point to a market that is positioned long JPY.

- Having broken above 146.50 this morning the market will be closely watching the oil price for short-term clues.

- The market is positioned for a move lower in USD/JPY and with this positioning at extremes we have seen the risk of pullbacks increase. A sustained break above 146.50/147.00 would begin to challenge the conviction of these shorts and focus will return to the 150.00/151.00 area.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.50($323m).Upcoming Close Strikes : 144.50($1.34b June 25)

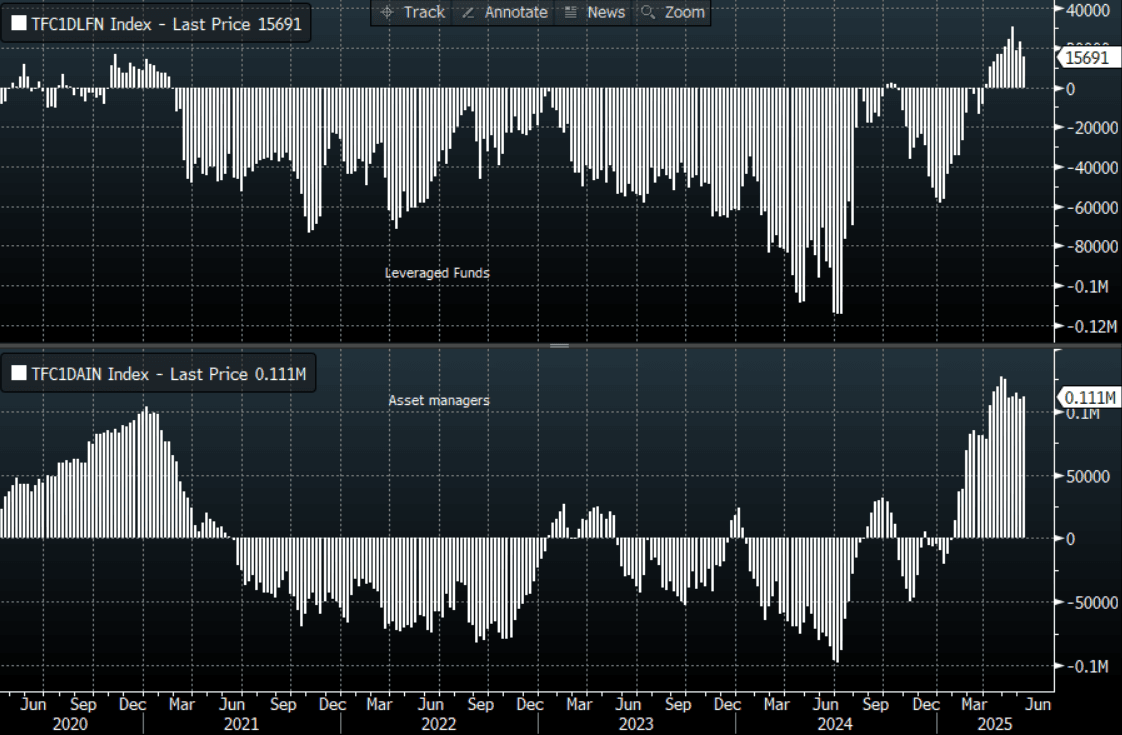

- CFTC data shows Asset managers maintained their already extensive JPY longs, while leveraged funds have pared back their own longs that had just begun to be rebuilt.

- Data/Event : Jibun Bank Japan PMI’s, Tokyo Condominiums for Sale

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P