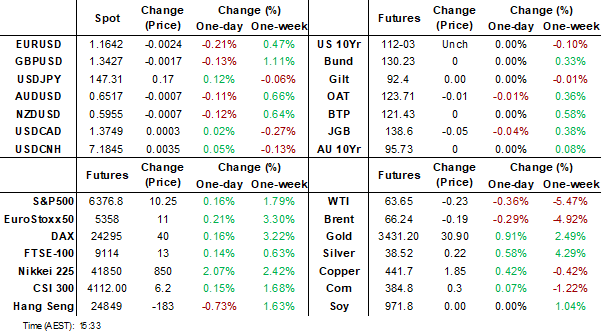

MNI EUROPEAN MARKETS ANALYSIS: BoJ Watching Inflation Risks

- Japan equities were supported by news the US will end so-called stacking tariffs. Data on real household spending for June was positive in y/y terms, but below market forecasts. The BoJ Summary of Opinions from the July meeting noted inflation risks but any shift from wait and see mode by the central bank is only likely towards year end.

- Macro trends were fairly steady elsewhere, with some focus on gold moves in light of recent US tariffs on Switzerland.

- Looking ahead, we have BoE speak, along with Canadian jobs data in a quiet end to the week.

MARKETS

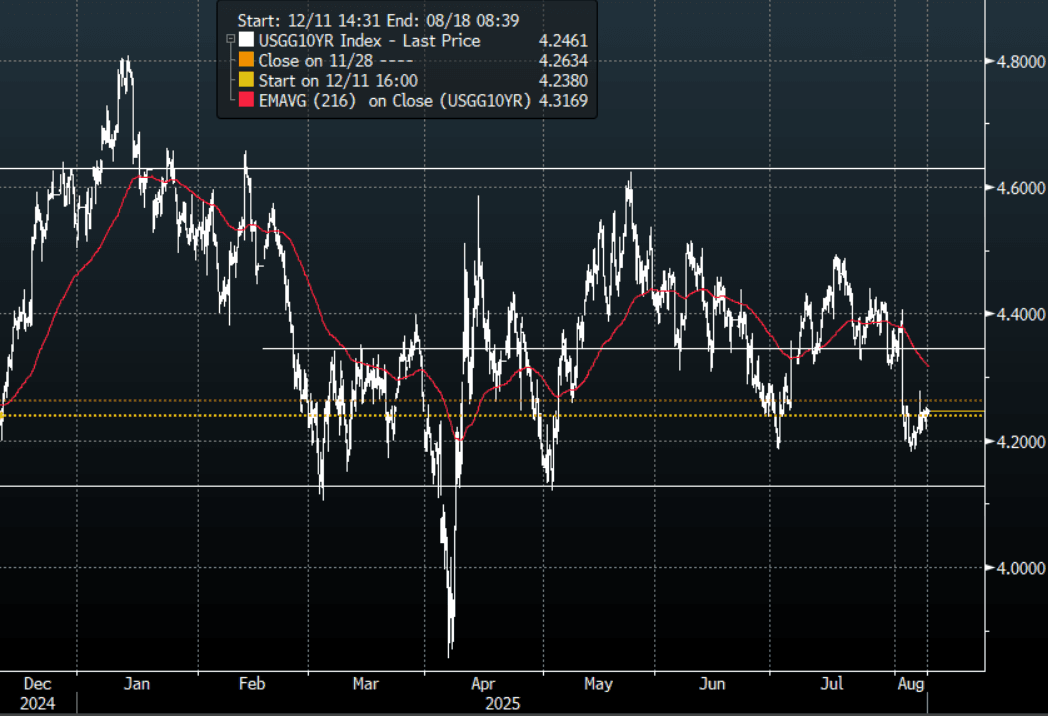

US TSYS: Asia Wrap - Yields End Mixed, The Curve Flattens

The TYU5 range has been 112-01+ to 112-04 during the Asia-Pacific session. It last changed hands at 112-02+, down 0-00+ from the previous close.

- The US 2-year yield has edged higher trading around 3.736%, up 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.244%, down 0.01 from its close.

- This has seen the yield curve flatten in Asia - 2s10s -1.00 at 50.601, 5s30s -0.98 at 102.413.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area.

- Mohamed A. El-Erian on X: “If the Administration were to secure exceptionally rapid Congressional approval for its nominee ahead of the September Fed meeting—and its a big if—the dynamics at the meeting could be fascinating. It’s not totally out of the question, for example, that at least three committee members would dissent from a decision to cut rates by 25 basis points, arguing instead for a more aggressive 50 basis point reduction. After all, last year, the Fed hesitated to cut rates in July, only to opt for a 50 basis point cut at the September meeting.

- RenMac on X: ”According to latest data from Conference Board, more CEOs see a net reduction in workforce. Percent seeing net reduction jumped to 34% in Q3, highest since Q4 2020. Percent seeing at least 1% growth in workforce slid to a low of 27%."

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

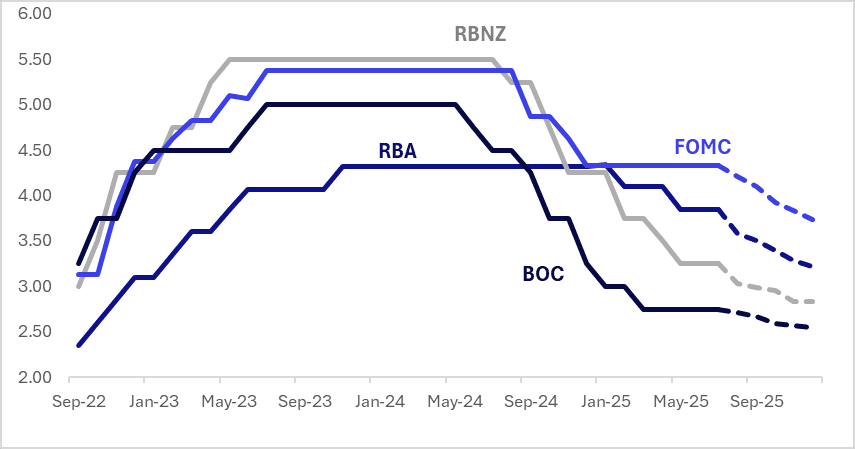

STIR: US Leads Bloc Markets Rates Lower Over Past Week

Interest rate expectations across the $-bloc eased over the past week, led by the U.S., where year-end implied rates fell 26bps. Canada, Australia, and New Zealand saw more modest declines of around 5bps each

- Last Friday, US nonfarm payrolls growth underwhelmed at 73k in July (cons 104k) but the major headline was the -258k two-month downward revision, of which -139k came from the private sector and -119k from the public sector. Outside of April 2020, that’s the largest two-month downward revision in at least forty-five years.

- We caution however that whilst jobs growth has soured sharply, it’s doing so along with a significant slowing in labour supply under immigration curbs.

- As such, the unemployment rate may have technically ticked up to a new cycle high of 4.248% (exceeding the 4.244% in May) but it continues to roughly plateau in the 4.0-4.25% range seen since last July.

- Looking ahead, the next key regional event is the RBA decision on August 12. After last week’s Q2 underlying CPI undershoot, the market is assigning a 97% probability to a 25bp rate cut at the upcoming meeting.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.74%, -59bps; Canada (BOC): 2.54%, -21bps; Australia (RBA): 3.21%, -64bps; and New Zealand (RBNZ): 2.83%, -42bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JGBS: 5Y Leads Yields Higher, Relatively Subdued Session

JGB futures are weaker but off session lows, -7 compared to settlement levels.

- (MNI) Some Bank of Japan board members acknowledged upside risks to prices but saw no need to rush a rate hike at the July 30-31 meeting, the summary of opinions showed Friday. But one member noted that it would take at least two-to-three more months to gauge the effects of U.S. tariff policy.

- MNI Interview - The Bank of Japan will likely raise its policy interest rate 25 basis points to 0.75% as early as December, though the Board could delay the move to January depending on evolving economic and price conditions, a former BOJ chief economist told MNI.

- Cash US tsys are slightly mixed in today's Asia-Pac session after yesterday's modest sell-off.

- Cash JGBs are flat to 2bps cheaper across benchmarks out to the 30-year, with the 5-year underperforming and the 40-year outperforming (-3bps). The benchmark 10-year yield is 0.3bps higher at 1.491% versus the cycle high of 1.616%.

- Swap rates are 1-2bps higher.

- On Monday, the local calendar will be closed.

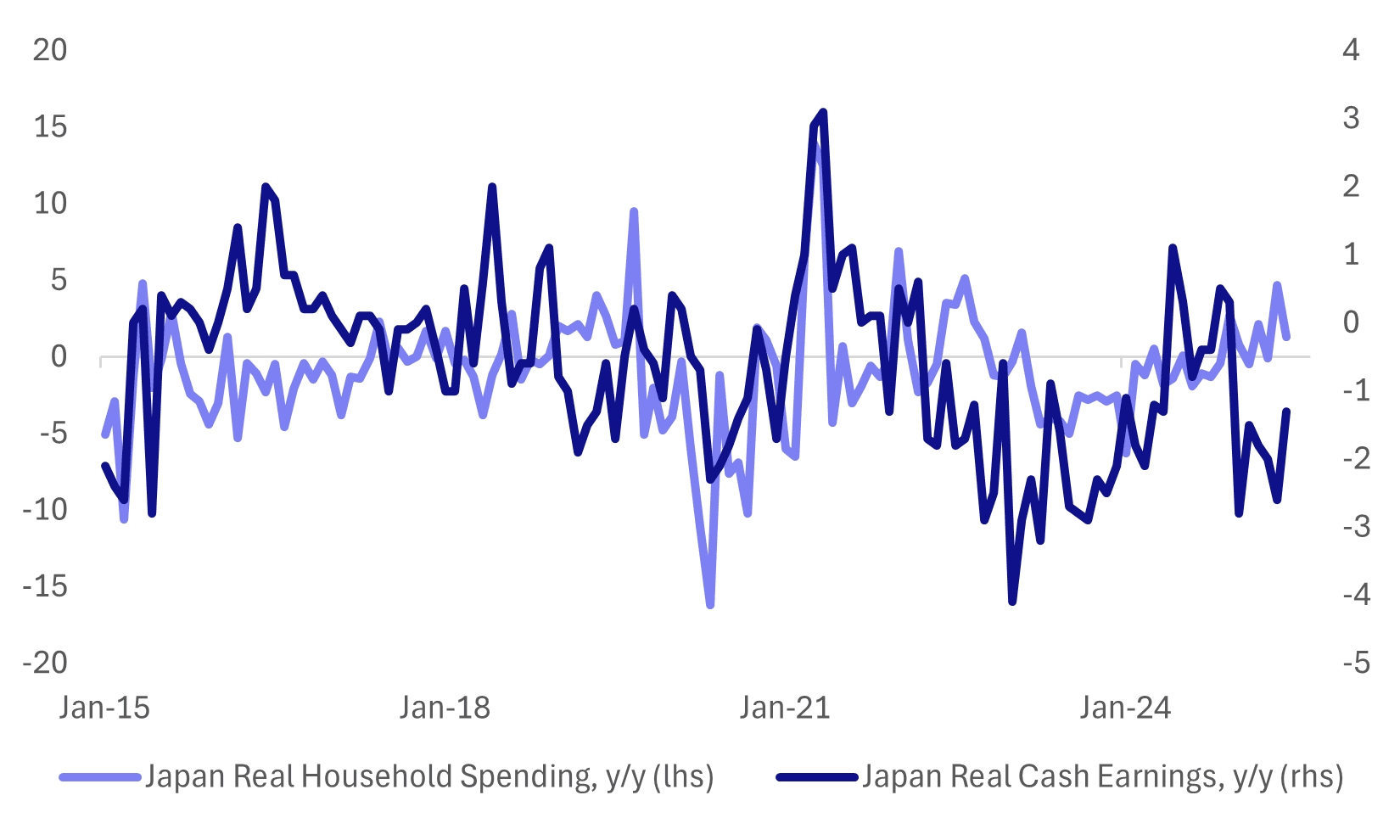

JAPAN DATA: June Real Household Spending Below Expectations

Japan's June real household spending outcome was below market expectations. In y/y terms we rose 1.3%, against a 2.7% forecast and 4.7% rise in May. In m/m terms spending was down 5.2%.

- This outcome brings the spending and real earnings trends somewhat back closer together, see the chart below. The two series diverged notably in May when spending was much stronger than the pace implied by a still negative real earnings backdrop. Earlier this week we saw June earnings data print below market expectations, with real earnings remaining in negative territory.

- This remains a key policy focus point in terms of driving positive real outcomes in this space, which would underpin a sustained rise in real household spending.

- In terms of the detail, food was down 2.1%y/y, along with furniture (-5.0%), clothing (-6.6%) and culture and recreation (-1.0%). Positives were seen in transport, and housing.

Fig 1: Japan Real Household Spending & Real Earnings Y/Y

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Modest Bear-Flattener On A Data-Light Session

ACGBs (YM -1.5& XM -0.5) are slightly weaker after another subdued data-light session.

- Cash US tsys are slightly mixed in today's Asia-Pac session after yesterday's modest sell-off.

- Cash ACGBs have bear-flattened, with yields flat to 2bps higher and the AU-US 10-year yield differential at flat.

- Bloomberg - The slump in the US dollar is convincing Australia's individual investors to seek protection for their American investments. Retail investors have poured a record $320 million into BlackRock's Australian-dollar hedged S&P 500 Index exchange-traded fund this year. Damien McIntyre, chief executive of GSFM Pty, said Australian investors are "positioning themselves for US dollar weakness".

- The bills strip has bear-steepened, with pricing -1 to -4 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in August is given a 98% probability, with a cumulative 62bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- On Monday, the local calendar will be empty.

- Next week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 2.75% 2 1 November 2029 bond on Friday.

BONDS: NZGBS: Closed Slightly Stronger, Subdued End To The Week

NZGBs closed 1bp richer across benchmarks after a subdued end to the trading week.

- The NZ 10-year outperformed its $-bloc counterparts slightly, with the NZ-US and NZ-AU yield differentials 1-2bps tighter on the day.

- Cash US tsys are slightly mixed in today's Asia-Pac session after yesterday's modest sell-off.

- Swaps closed showing a modest bull-flattening, with rates flat to 2bps lower.

- “Inflation expectations remain contained in New Zealand, and don't pose a threat to further easing by the Reserve Bank. The main inflation risk lies offshore - domestically driven price pressures appear muted, with expectations for wage growth pulling back. We see a disconnect between expectations and reality in the labor market, and believe the unemployment rate is likely to surprise to the upside over the coming quarters. That should see the RBNZ deliver more rate cuts than it projects. We expect a 25-basis-point rate cut at its next meeting on Aug. 20.” (BBG)

- RBNZ dated OIS pricing closed little changed across meetings. 23bps of easing is priced for August, with a cumulative 41bps by November 2025.

- On Monday, the local calendar will be empty. The next release will be Card Spending data on Wednesday.

FOREX: Asia FX Wrap - BBDXY Finds Demand Back Towards 1200

The BBDXY has had a range of 1201.73 - 1204.04 in the Asia-Pac session, it is currently trading around 1203, -0.02%. The USD attempted a bounce overnight, but Miran’s appointment to the Fed board has seen that quickly reversed. The market is again very quick to pounce onto anything that potentially justifies selling the USD and Stephen Miran has been very vocal about the USD’s overvaluation being the root of the US’s economic imbalances. Personally I struggle to see how he changes the structural demand for USD’s from inside the Fed other than adding to a dovish tilt within it. Lets see if the market is able to follow through with this initial wave of selling, the 1200 area seems to be holding pretty well for now.

- EUR/USD - Asian range 1.1655 - 1.1679, Asia is currently trading 1.1660. The pair has bounced nicely off the important 1.1300/1.1400 area. The market stalled at its first attempt to challenge the resistance around the 1.1700 area, let's see if it can do better the second time round.

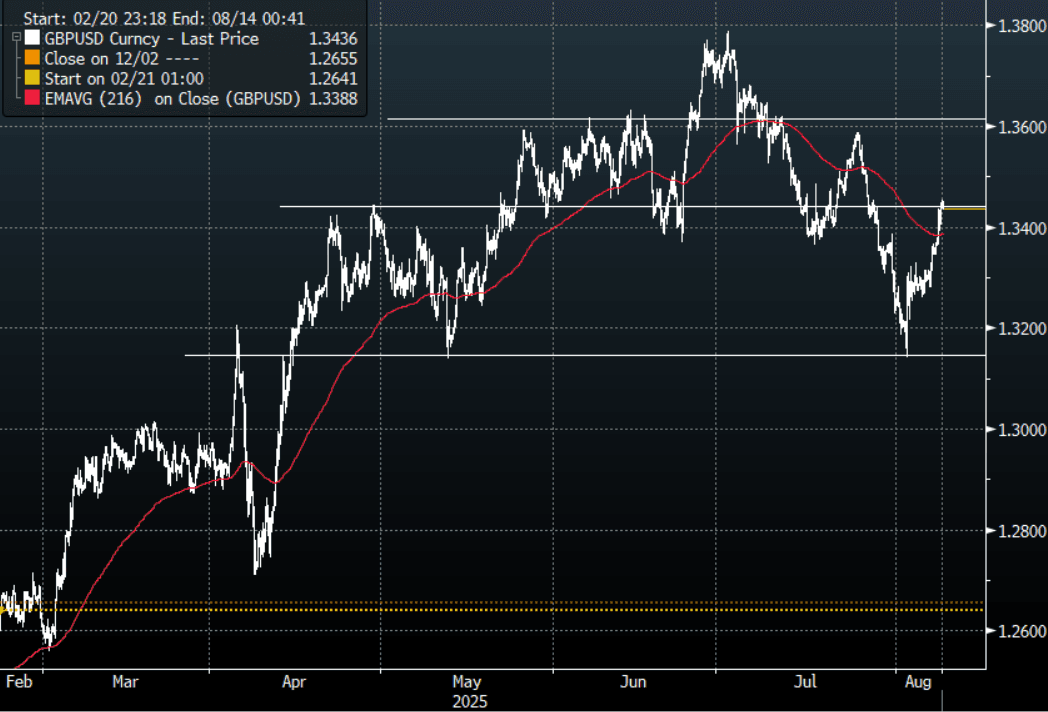

- GBP/USD - Asian range 1.3438 - 1.3453, Asia is currently dealing around 1.3435. The pair bounced nicely off the 1.3100/1.3200 support area. I would suspect sellers could be around on this bounce back towards 1.3450 initially looking to fade this bounce.

- USD/CNH - Asian range 7.1784 - 7.1870, the USD/CNY fix printed 7.1382, Asia is currently dealing around 7.1840. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.20%, Gold $3398, US 10-Year 4.244%, BBDXY 1203, Crude Oil $63.77

- Data/Events : France ILO Unemployment rate

Fig 1: GBP/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

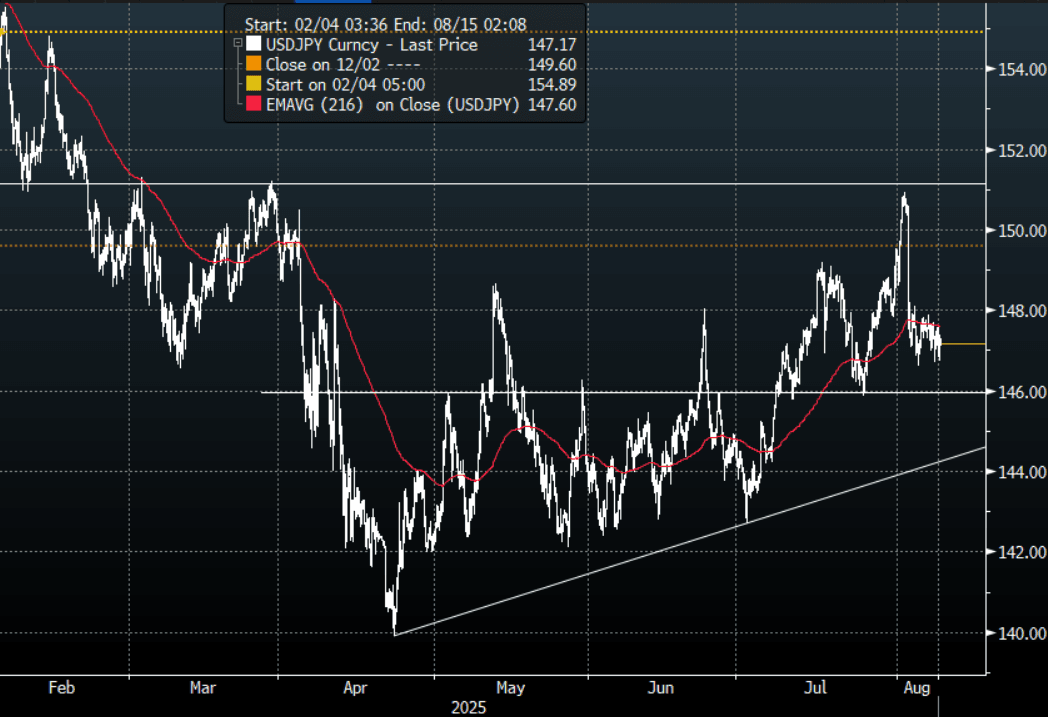

JPY: Asia Wrap - USD/JPY Finds Demand Sub 147.00 Again

The Asia-Pac USD/JPY range has been 146.72 - 147.37, Asia is currently trading around 147.15, +0.01%. USD/JPY is consolidating within a 146.50-148.00 range. Price has moved very quickly away from the pivotal 151/152 area much to the relief of Institutional Yen longs and the BOJ. CFTC Data shows leveraged accounts had started to aggressively build Yen shorts last week so this quick move lower would have been frustrating. Price is holding above the support area between 146.00/147.00, a move sub 145.00 is needed to turn momentum lower once more, until then the 145.00-151-00 range should dominate.

- (Bloomberg) -- “Japanese stocks rose after Japan’s chief trade negotiator said the US agreed to end so-called stacking on universal tariffs and cut car levies at the same time. Optimism about rate cuts in the US also helped lift the mood.”

- MNI Interview - The Bank of Japan will likely raise its policy interest rate 25 basis points to 0.75% as early as December, though the Board could delay the move to January depending on evolving economic and price conditions, a former BOJ chief economist told MNI.

- (MNI) Some Bank of Japan board members acknowledged upside risks to prices but saw no need to rush a rate hike at the July 30-31 meeting, the summary of opinions showed Friday. But one member noted that it would take at least two-to-three more months to gauge the effects of U.S. tariff policy. "If the U.S. economy is able to withstand the impact to a greater extent than expected, the downward effects on Japan's economy are likely to remain minimal. In that case, it may be possible for the Bank to exit from its current wait-and-see stance, perhaps as early as the end of this year."

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($671m), 147.50($501m), 148.20($400m).Upcoming Close Strikes : 147.30($878m Aug 12), 147.00($841m Aug 13) - BBG.

- CFTC data shows asset managers surprisingly added slightly to their JPY longs +75119( Last +72326), while leveraged funds aggressively added to their newly built short JPY position -31280(Last -11571).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

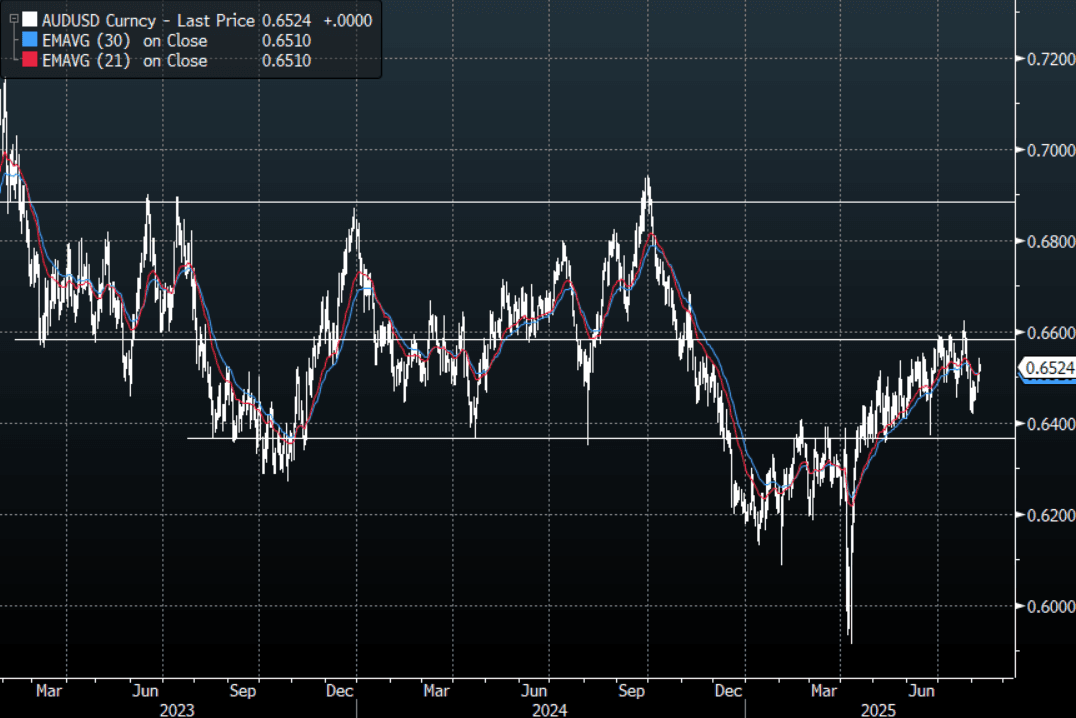

AUD: Asia Wrap - AUD/USD Unchanged In A Quiet Session

The AUD/USD has had a range of 0.6511 - 0.6528 in the Asia- Pac session, it is currently trading around 0.6520, -0.05%. The headline that Trump is set to nominate Miran to the short-term Fed Board vacancy saw a late move lower in the USD across the board. The market is very quick to use any excuse to sell the USD, Miran’s views on the USD are well publicised but at most he will add 1 more dovish vote to a board that seems to already be turning that way. Can he actually alter the policy on the USD from this position ? Risk has traded a little higher as a result of this, E-minis +20%, NQU5 +0.20% but the AUD ends our session unchanged after initially probing higher.

- Depending on what your view is 0.6550 still offers good risk/reward to fade initially. I feel the performance of US equities over August/September will be crucial as seasonality points to some strong headwinds approaching.

- Bloomberg - The slump in the US dollar is convincing Australia’s individual investors to seek protection for their American investments.Retail investors have poured a record $320 million into BlackRock’s Australian-dollar hedged S&P 500 Index exchange-traded fund this year. Damien McIntyre, chief executive of GSFM Pty, said Australian investors are "positioning themselves for US dollar weakness".

- Stephen Miran At Hudson Bay Capital : ”The root of the economic imbalance lies in persistent dollar overvaluation that prevents the balancing of international trade, and this overvaluation is driven by inelastic demand for reserve assets. As global GDP grows, it becomes increasingly burdensome for the United States to finance the provision of reserve assets and the defense umbrella as the manufacturing and tradeable sectors bear the brunt of the costs."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD4.42b), 0.6400(AUD1.32b). Upcoming Close Strikes : 0.6565(AUD783m Aug 12) - BBG

- AUD/JPY - Asia-Pac range 95.76 - 96.06, Asia is trading around 96.00. The pair has bounced to test its first resistance around the 96.00/96.50 area. There should be sellers around here initially, a sustained break below 94.50/95.00 is needed to signal a deeper move lower.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

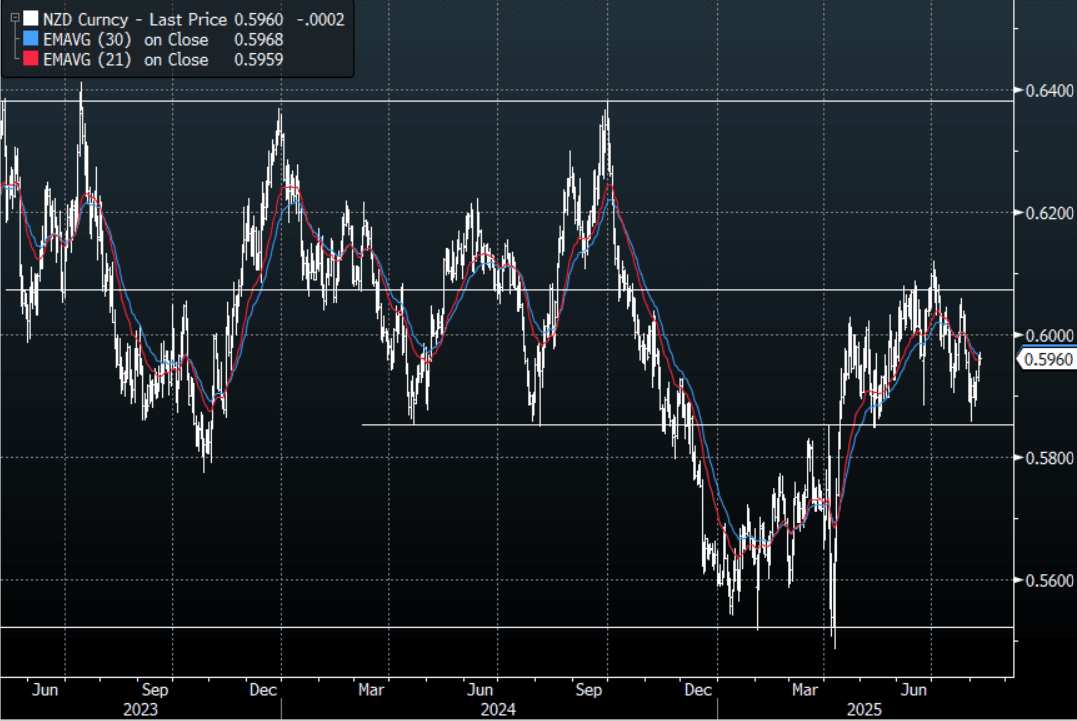

NZD: Asia Wrap - NZD/USD Unchanged After Probing Higher

The NZD/USD had a range of 0.5948 - 0.5972 in the Asia-Pac session, going into the London open trading around 0.5960, -0.03%. The market is very quick to use any excuse to sell the USD, Miran’s views on the USD are well publicised but at most he will add 1 more dovish vote to a board that seems to already be turning that way. Can he actually alter the policy on the USD from this position ? Risk has traded a little higher in response to this, E-minis +25%, NQU5 +0.25%.

- NZD/USD bounced nicely off its 0.5850 support but depending on your view I would suspect sellers could return on any bounce back toward 0.6000/0.6050 first up. For the moment back in the 0.5850-0.6100 range looking for a catalyst to break and give clearer direction.

- Kelly Eckhold(Westpac NZ) on LinkedIn - “The RBNZ data on actual lending rates applied to mortgage loans shows significant pass through in June. This was a big month for refinancing. Effective paid rates are down 73 bp from their peak now. Effective rate is back to October 2023 levels.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5920(NZD583m Aug 11), 0.5930(NZD646m Aug 11). - BBG

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +3903(Last +5034), the Leveraged community reduced their shorts slightly -6250(Last -7328).

- AUD/NZD range for the session has been 1.0929 - 1.0960, currently trading 1.0940. The Cross continues to trade sideways after stalling towards the 1.1000 area once more. The range looks to be 1.0850-1.1000 for now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Japan Firmer On US Trade News, Mixed Trends Elsewhere

Asian equity market trends are mixed as we approach the end of the week. The stand out performer has been Japan stocks, aiding by US-Japan trade talks, which appeared to clarify tariff stacking concerns favorably for Japan. trends elsewhere have been mixed. US equity futures are modestly higher, with Eminis and Nasdaq futures both a little over 0.20% firmer at this stage. Trends are positive for these indices, but we remain off late July highs.

- The Topix is up around 1.5%, the NKY 225 up around 2.2%. For the Topix we are consolidating the recent break above 3000, and tracking at fresh record highs. The NKY 225 is just short of fresh highs. Sentiment has been aided by earlier headlines around US-Japan trade talks, which appeared to clarify the issue around stacking tariffs. Japan's top trade negotiator, Ryosei Akazawa, stated the US will end tariff stacking and cut car tariffs at the same time. There wasn't a timeline on when this would take place, but it is not expected to stretch beyond 6 months.

- Elsewhere we had weaker than forecast Japan real household spending for June. The BoJ Summary Of Opinions recognized inflation risk but exiting the current wait and see approach may not happen until the end of this year.

- Trends are mixed elsewhere, with the HSI off around 0.65% in Hong Kong, while the CSI 300 is little changed, last near the 4117 level.

- The Kospi is also weaker, but still above 3200, while Taiwan's Taiex is around flat. This comes after yesterday's strong outperformance as TSMC rallied to record highs on views the company will avoid the US's 100% chip tariff. Offshore investor inflows were also very strong.

- In South East Asia, trends are relative steady outside of Singapore stocks, which are down around 0.50%. Indonesian markets have performed better, up close to 0.80% at this stage.

- Indian markets remain under pressure, with the benchmark Nifty and Sensex indices both down around 0.40% at this stage. We are up from recent lows, but the downtrend looks firmly entrenched at this stage, amid heightened US tariff risks.

ASIA STOCKS: Taiwan Inflows Surge On TSMC Gains, India Outflows Persist

Surging inflows into Taiwan stocks from offshore investors was the standout EM Asia equity flow from yesterday. The nearly $1.5bn added was the strongest daily inflow since the start of July this year. This came as onshore tech bellwether TSMC surged to fresh record highs. The Taiwan authorities stated chip sales from the company would be exempt from Trump's 100% chip tariff import (presumably as the company has invested in local US manufacturing in Arizona). This brings YTD inflows to just over $4.5bn. The Taiex ended yesterday's session above 24000, fresh highs back to mid last year.

- Elsewhere, South Korea saw modest outflows, leaving a softer trend for the past 5 trading days intact.

- For Wednesday's outflows from India were notably at just over $500mn. The extra tariff hike due to Indian oil imports from Russia is a headwind for local equity market sentiment.

- In South East Asia, Indonesian flows have stabilized somewhat in the past 5 days, while Malaysian momentum remains negative.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -53 | -127 | -4977 |

| Taiwan (USDmn) | 1495 | 2209 | 4554 |

| India (USDmn)* | -502 | -1417 | -11721 |

| Indonesia (USDmn) | 41 | 34 | -3714 |

| Thailand (USDmn) | -9 | 138 | -1700 |

| Malaysia (USDmn) | -69 | -237 | -3186 |

| Philippines (USDmn) | 3 | -2 | -625 |

| Total (USDmn) | 906 | 599 | -21369 |

| * Data Up To Aug 6 |

Source: Bloomberg Finance L.P./MNI

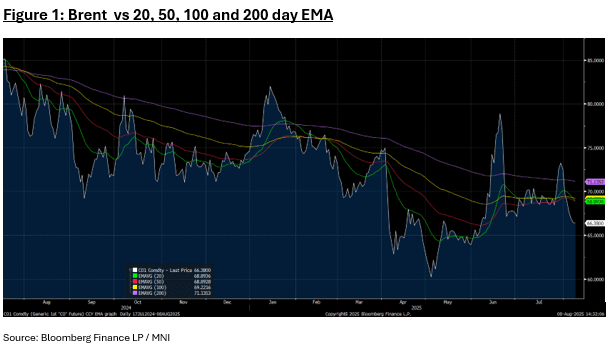

Oil Caps off Poor Week with Further Falls

- Oil prices have found new lows for the week today, as prices dropped for a seventh consecutive day.

- WTI is down -0.14% at US$63.79 in the Asia trading day, and down -5.3% for the week.

- Brent is down -0.11% at $66.36 and -4.7% for the week. Brent is trading below all major moving averages, the nearest being the converged 20-day and 50-day EMA of $68.89. All major moving averages are beginning to trend downwards, pointing to the bearish trend starting to become entrenched.

- This week the President announced a doubling of tariffs on all Indian imports to 50% as a penalty for the ongoing purchase of Russian oil, prompting local state-owned oil refiners to pull back from purchases and look elsewhere. Treasury Secretary Scott Bessent, meanwhile, said the US may also impose tariffs on China at some point, when asked about targeting countries that buy Moscow’s energy.

- August sees the OPEC+ supply increase kick in, which could further suppress prices.

Gold Fails To Hold Above US$3,400

- Gold traded briefly in the Asia morning above US$3,400 before retreating to around $3,396.70 and flat to the US close. Despite this gold remains up 1% for the week on renewed hopes of interest rate cuts in the US.

- Investors are grappling with the FT headline and implications from the US slapping tariffs specifically on 1kg gold bars, seemingly aimed specifically at Switzerland. Whilst gold has long been seen as a 'safe-haven' in the trade war it is now caught up in it.

- The PBOC added 60,000 ounces of gold in July according to data released. As the Central Bank continues to diversify away from the USD it ia adding to its gold reserves, now up to its eight consecutive month of additions.

- Despite the tariff news on bars, Citi upgraded its three month gold forecast to $3,500 per ounce, citing U.S. economic weakness, dollar softness, geopolitical risk, and robust investor appetite for the metal.

- Gold remains above all major moving averages again this week, sitting above the 20-day EMA of $3,356.96. All major moving averages remain modestly upward sloping, a sign that the bullish momentum could continue.

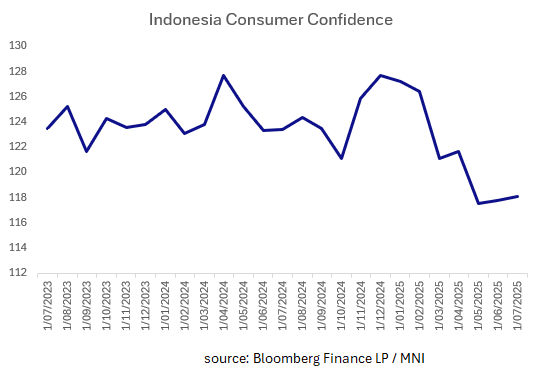

INDONESIA: Consumer Confidence Remains Subdued

- The Subianto government has introduced multiple policy adjustments aimed at boosting the consumer and July's Consumer Confidence Index indicates that the impacts are failing to flow through to consumer confidence.

- The government launched several targeted stimulus packages centered o which included transport subsidies, food and cash handouts and wage subsidies for eligible workers, tax incentives and utility discounts as well as tax relief for labour intensive industries.

- Free school lunch program has been developed to encourage better nutrition.

- Loans aiming for further expansion to support MSMEs in agriculture, trade, manufacturing, and digital sectors.

- Reform of the LPG subsidy distribution system to support households.

- Having hit lows in early April when tariffs were first announced, the Jakarta Composite has been a strong regional performer since up over 25% but with the general population having limited savings, this doesn't impact broader sentiment.

CHINA: Country Wrap: US Threaten China Tariffs for Russian Oil

- Treasury Secretary Scott Bessent says the US may impose tariffs on China at some point, when asked about President Trump’s promise to impose tariffs on countries that buy Russian oil. (source BBG)

- China's foreign trade will remain resilient in the second half of 2025, fueled by strong growth in high-tech exports, vibrant private sector activity and closer ties with emerging markets, government officials and exporters said on Thursday. They noted that China's steady export performance, particularly driven by private companies, underscores robust global demand for the country's high-tech mechanical and electrical products, and facilitates its deeper integration into regional and global industrial chains. (source China Daily)

- Buoyed by stronger-than-expected economic performance and steered by policy continuity and certainty, China is accelerating through the home stretch of the 14th Five-Year Plan (2021-2025) to lay a solid foundation for future high-quality development. The first half of 2025 highlighted China's economic resilience, with GDP rising 5.3 percent -- surpassing expectations -- while employment remained stable, foreign trade volumes reached record highs, and stronger investor confidence pushed stock market indices upward. (source XINHUA)

- The HSI is down in Friday's trade by -0.66%, whilst onshore bourses hold onto modest gains of +0.05 -00.10%. All major bourses remain positive for the week with the Shenzhen Comp the outperformer with gains of +2.3%.

- Yuan Reference Rate at 7.1382 Per USD; Estimate 7.1774

- Government bond yields remain steady with the 10yr at 1.68%, marginally lower for the week.

MALAYSIA: Country Wrap: Malaysia Grapples with Chip Tariffs

- A portion of Malaysia’s semiconductor exports may qualify for exemption from President Donald Trump’s proposed 100% tariff on chip imports, according to CIMB Group Holdings Bhd. This is given the presence of US firms and multinational companies that have ongoing or planned capital expenditure in the US, analysts wrote in a research note on Thursday. About 65% of Malaysia’s semiconductor exports to the US originate from American firms operating locally. If tariff implementation is worse than the base case of 65% exemptions, every additional 10% of semiconductor exports affected could translate to a 0.29% drag on Malaysia’s gross domestic product. Over the longer term, companies may be compelled to relocate production, potentially impacting investment decisions in the future. (source BBG)

- Foreign reserves amounted to 512.8b ringgit ($121.3b) as of July 31, according to Bank Negara Malaysia in Kuala Lumpur.

- Construction and materials stocks are set to benefit from the upcoming Budget 2026 to be announced in October following the tabling of the 13th Malaysian Plan (13MP) spanning 2026 to 2030 that saw an allocation of RM430bil for development expenditure over the period. (source The Star)

- Despite some regional peers experiencing strong inward foreign flows into their equity markets, Malaysia's remain subdued with outflows over the last five trading days. The FTSE Malay KLCI is up +0.25% today and over +1.3% for the week

- The Ringgit is little changed in the morning session Friday, trading at 4.2360 and nearing a 1% gain over the last five days of trading.

- Bond yields are stronger for the week, despite MGS issuance. The 10yr is at 3.38%, down -4bps for the week.

SOUTH KOREA: Country Wrap: Food Prices up Sharply According to Govt

- Food prices are climbing sharply in Korea as supply struggles to keep pace with rising demand, government officials and market observers said Thursday. While extreme weather conditions this summer — including torrential rains and heat waves — have disrupted the production of agricultural, livestock and fishery products, demand has surged following the distribution of government-issued voucher-based cash handouts, they added. (source Korea Times)

- The government will host large-scale domestic tourism and consumption events every month through the end of the year, aiming to turn the recent boost in spending driven by consumption vouchers into “real growth,” Finance Minister Koo Yun-cheol said Thursday. Koo, who also serves as deputy prime minister for economic affairs, added that the government will unveil a new economic growth strategy later this month, which will include key policy directions focused on artificial intelligence (AI) and other future growth engines. (source Korea Times)

- The Kospi is weaker today, but still above 3200 and one of the few regional bourses to poste losses of over 1% for the week.

- The Won is weaker today and failed to follow the strong week of gains of regional peers, only managing modest gains to be near 1,387.85

- Bonds have had a strong week with the KTB 10yr lower by -7bps for the week at 2.76% whilst the 2s10s curve remains at +40bps

Asia FX Softer In NEA, KRW Lagging Better Global Tech Equities

In North East Asia FX, the bias has been for USD gains in the first part of Friday trade. Moves are fairly modest, but evident across the region. USD/CNH remains supported sub 7.1800 for now (last near 7.1835). It remains a very low beta play to overall USD trends, with implied vols just up from recent cycle lows. The USD/CNY fixing rose, but in line with market estimates, leaving the fixing error little changed. Tomorrow we get July CPI and PPI prints. CPI headline is expected to dip back into negative territory (-0.1%y/y, versus 0.1% prior).

- Spot USD/KRW has been supported on dips, the pair last near 1388. Recent ranges continue to hold for the pair, although we look to be lagging better tech global equity trends at this stage. Upside focus will rest close to 1400, which markets the 200-day EMA resistance point. Thursday intra-session lows were just under 1380.

- USD/TWD is up to 29.84, following yesterday's sharp pull back. Equities onshore are up modestly, following yesterday's +2% gain. Later on we get July trade data, with exports projected at 29.6%y/y (from 33.7% in June).

- USD/HKD spot sits just under the top end of the peg band (near 7.8500).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 08/08/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 08/08/2025 | 1115/1215 | BOE Pill At National MPC Agency Briefing | ||

| 08/08/2025 | 1230/0830 | *** | Labour Force Survey | |

| 08/08/2025 | 1230/0830 | *** | Labour Force Survey | |

| 08/08/2025 | 1420/1020 | St. Louis Fed's Alberto Musalem | ||

| 08/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 08/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 09/08/2025 | 0130/0930 | *** | CPI | |

| 09/08/2025 | 0130/0930 | *** | Producer Price Index |