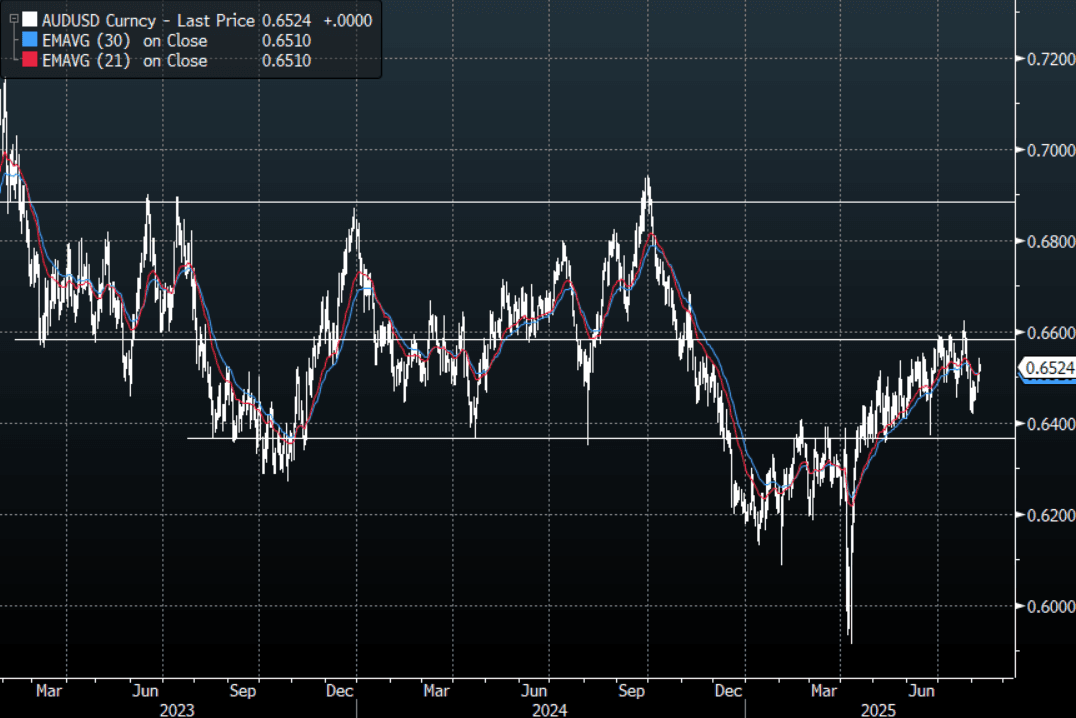

AUD: Asia Wrap - AUD/USD Unchanged In A Quiet Session

The AUD/USD has had a range of 0.6511 - 0.6528 in the Asia- Pac session, it is currently trading around 0.6520, -0.05%. The headline that Trump is set to nominate Miran to the short-term Fed Board vacancy saw a late move lower in the USD across the board. The market is very quick to use any excuse to sell the USD, Miran’s views on the USD are well publicised but at most he will add 1 more dovish vote to a board that seems to already be turning that way. Can he actually alter the policy on the USD from this position ? Risk has traded a little higher as a result of this, E-minis +20%, NQU5 +0.20% but the AUD ends our session unchanged after initially probing higher.

- Depending on what your view is 0.6550 still offers good risk/reward to fade initially. I feel the performance of US equities over August/September will be crucial as seasonality points to some strong headwinds approaching.

- Bloomberg - The slump in the US dollar is convincing Australia’s individual investors to seek protection for their American investments.Retail investors have poured a record $320 million into BlackRock’s Australian-dollar hedged S&P 500 Index exchange-traded fund this year. Damien McIntyre, chief executive of GSFM Pty, said Australian investors are "positioning themselves for US dollar weakness".

- Stephen Miran At Hudson Bay Capital : ”The root of the economic imbalance lies in persistent dollar overvaluation that prevents the balancing of international trade, and this overvaluation is driven by inelastic demand for reserve assets. As global GDP grows, it becomes increasingly burdensome for the United States to finance the provision of reserve assets and the defense umbrella as the manufacturing and tradeable sectors bear the brunt of the costs."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD4.42b), 0.6400(AUD1.32b). Upcoming Close Strikes : 0.6565(AUD783m Aug 12) - BBG

- AUD/JPY - Asia-Pac range 95.76 - 96.06, Asia is trading around 96.00. The pair has bounced to test its first resistance around the 96.00/96.50 area. There should be sellers around here initially, a sustained break below 94.50/95.00 is needed to signal a deeper move lower.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Cheaper As Post-RBA Fallout Continues

ACGBs (YM -7.0 & XM -8.0) are weaker and near session cheaps as the fall-out from yesterday’s surprising RBA decision continued.

- (AFR) At least two Labor appointees to the Reserve Bank of Australia monetary policy board, Jenny Wilkinson and Iain Ross, almost certainly voted for an interest rate cut on Tuesday, according to former RBA insiders. Wilkinson is Treasury secretary to Jim Chalmers and Ross is a former union-aligned pay setter. But the identity of the third dissenter in the shock 6-3 decision to hold the cash rate unchanged at 3.85 per cent is more of a mystery.

- Cash US tsys are ~1bp cheaper in today’s Asia-Pac session after yesterday’s modest sell-off.

- Cash ACGBs are 6-8bps with the AU-US 10-year yield differential at -7bps.

- The bills strip are 3-5bps cheaper.

- RBA-dated OIS pricing is modestly firmer across meetings today after shunting higher yesterday. A 25bp rate cut yesterday was given a 92% probability by the market ahead of the decision. Currently, pricing across meetings is 10-19bps firmer than yesterday’s pre-RBA levels. A cumulative 60bps of easing is priced by year-end (based on an effective cash rate of 3.84%) versus 75bps before the RBA decision.

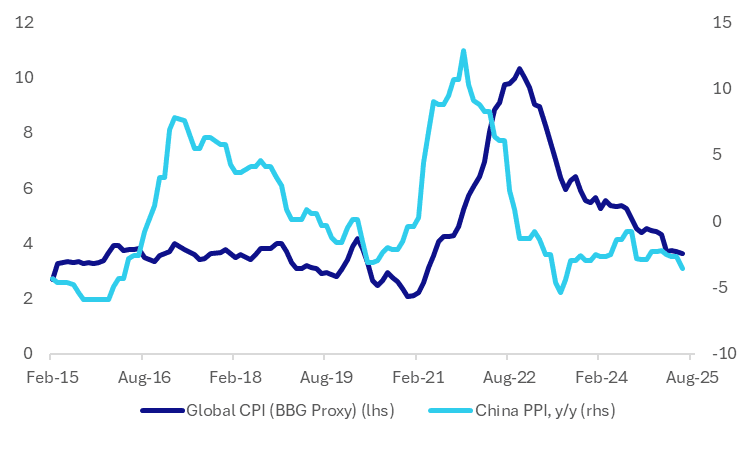

CHINA DATA: Low PPI May Help Global Inflation Pressures, Commodity Prices A Risk

China's PPI downside momentum remained firmly in place for June. We printed -3.6%y/y, the weakest outcome since July 2023.

- The chart below overlays the China PPI, in y/y terms, versus a Global CPI proxy from Bloomberg (see WOININFL <Index> on BGB for more details). At a time when global inflationary pressures are still elevated, particularly given higher tariff threats, the continued downward momentum in China PPI may provide some further support to downside global CPI momentum.

- The relationship is by no means perfect, but the correlation in the last 3 years is still running at over 53%.

- There of course caveats around whether the relationship will continue to hold, given tariff shifts may drive shifting trade patterns. Still, such shifts can take a while to play out, so weaken upstream price pressures in China should, all else equal, help alleviate upside global inflation pressures.

Fig 1: China PPI Y/Y & World CPI Y/Y

Source: Bloomberg Finance L.P./MNI

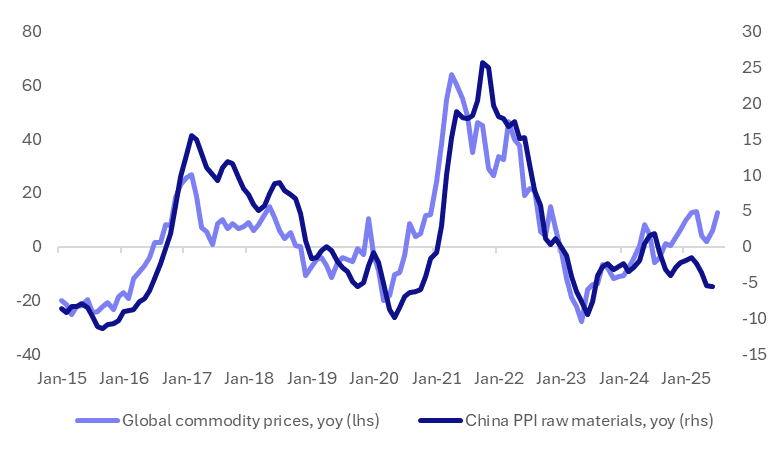

- The other caveat is the extent to which upstream price pressures rebound in China. The second chart overlays the PPI raw materials sub index against spot global commodity prices (in y/y terms).

- The firmer global spot price backdrop is yet to translate into firmer raw materials prices in China. Historically, these two series have moved reasonably closely with each other.

- Again tariffs (threats or otherwise) are at play, given copper surging in Tuesday trade as US President Trump threatened high tariffs on imports of the metal.

Fig 2: China PPI Raw Materials Y/Y & Spot Commodity Prices Y/Y

Source: Bloomberg Finance L.P./MNI

JGBS: Modest Twist-Flattener For Cash Bonds

At the Tokyo lunch break, JGB futures are weaker, -14 compared to the settlement levels.

- (MT Newswires) A newly appointed member of the Bank of Japan's board, Junko Koeda, has indicated a possible upward revision to the central bank's inflation forecast this month, Bloomberg News reported Wednesday.

- Cash US tsys are ~1bp cheaper in today’s Asia-Pac session after yesterday’s modest sell-off.

- The cash JGB curve has twist-flattened, with yields 1bp higher to 1bp lower, pivoting at the 10-year.

- (Bloomberg) There’s little sign that longer-dated JGBs will rebound given concerns the July 20 upper house election will lead to a surge in government spending. That’s also spurring traders to pare back beta on BOJ rate hikes, as the rapid steepening of the yield curve acts to tighten monetary conditions.

- Swap rates flat to 1bp lower. Swap spreads are mostly tighter.