OIL: Oil Caps off Poor Week with Further Falls

- Oil prices have found new lows for the week today, as prices dropped for a seventh consecutive day.

- WTI is down -0.14% at US$63.79 in the Asia trading day, and down -5.3% for the week.

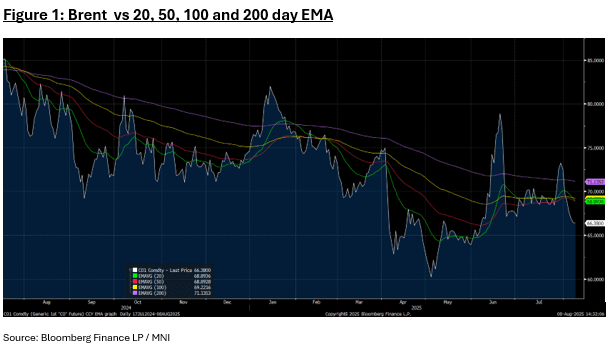

- Brent is down -0.11% at $66.36 and -4.7% for the week. Brent is trading below all major moving averages, the nearest being the converged 20-day and 50-day EMA of $68.89. All major moving averages are beginning to trend downwards, pointing to the bearish trend starting to become entrenched.

- This week the President announced a doubling of tariffs on all Indian imports to 50% as a penalty for the ongoing purchase of Russian oil, prompting local state-owned oil refiners to pull back from purchases and look elsewhere. Treasury Secretary Scott Bessent, meanwhile, said the US may also impose tariffs on China at some point, when asked about targeting countries that buy Moscow’s energy.

August sees the OPEC+ supply increase kick in, which could further suppress prices.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: Asia Wrap - AUD/USD Trades Sideways Above 0.6500, AUD/JPY Breaking ?

The AUD/USD has had a range of 0.6510 - 0.6537 in the Asia- Pac session, it is currently trading around 0.6530, -0.03%. The pair has traded sideways in a tight range today as it consolidates the reaction to the RBA yesterday. The AUD needs to hold above its 0.6480/0.6500 support as a sustained move below there would see a deeper correction back to 0.6350/0.6400.

- MNI RBA Review - July 2025: Easing Bias Still Intact: The RBA surprised the market by keeping rates on hold at 3.85%. The central bank wants to see more evidence of inflation sustainably trending towards the 2-3% target before easing more.

- RBA Governor Bullock stated the central bank still has an easing bias, and the split vote decision (6 in favor of the hold, 3 in favor or a cut) reflected the timing of further easing rather than the direction of rates.

- AUSSIE BONDS ACGB Dec-35 Supply Digested But Less Demand: Expectations of sustained strong pricing at auctions proved accurate, with the latest round of ACGB Dec-35 supply seeing the weighted average yield print 0.58bp through prevailing mids (per Yieldbroker). Today's cover ratio fell to 2.6500x from 3.1042x.

- The AUD/USD bounced strongly off its support around 0.6500 overnight, looks like it's back to the 0.6500 - 0.6600 range and it should now take its cues from the USD. Watching to see if the support continues to hold as a move through there signals a deeper correction.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6425(AUD700m), 0.6550(AUD 607m). Upcoming Close Strikes : 0.6650(AUD857m July 10), 0.6600(AUD634m July 10), 0.6650(AUD599m July 11)

- CFTC Data shows Asset managers pared back their shorts slightly -35992, the Leveraged community maintained their shorts -22903..

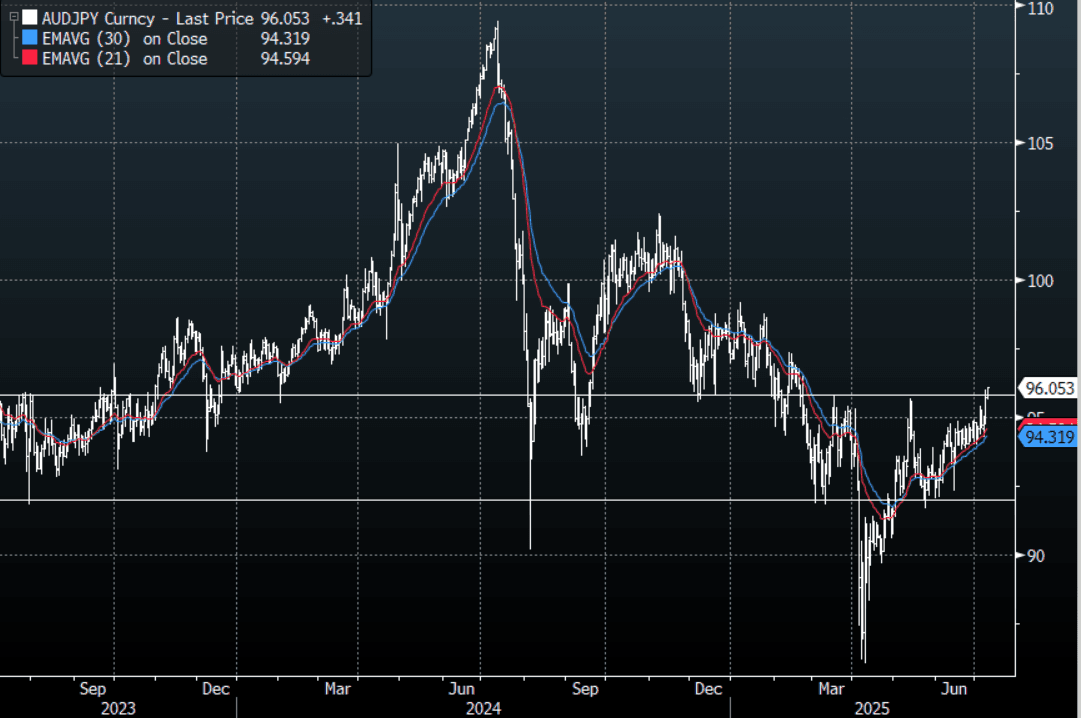

- AUD/JPY - Today's range 95.62 - 96.05, it is trading currently around 96.04, +0.34%. The pair is attempting to break above 96.00, with the market positioned both short AUD and long JPY. A sustained break above this level could see another tranche of these shorts pared back and provide a tailwind to probe higher.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Asia Wrap - Yields Edge Higher

The TYU5 range has been 110-24+ to 110-28 during the Asia-Pacific session. It last changed hands at 111-25, up unchanged from the previous close.

- The US 2-year yield has edged higher trading around 3.90%, up 0.01 from its close.

- The US 10-year yield has edged higher trading around 4.413%, up 0.01 from its close.

- The 10-year yield saw a strong bounce in reaction to the better NFP print. This 4.40% area offers those who would like to express a long the opportunity to fade. A sustained close back above the 4.45/50% area though would not be great for the bulls and could see more of the longs pared back.

- MNI FED: FOMC Minutes: Analysts Eye Discussion Of July Cut, Tariff Inflation. The minutes of the June 17-18 FOMC meeting (released Wednesday Jul 9 at 2pm ET) should underline the Committee's patience in making its next rate move amid heightened tariff-related economic uncertainty, as encapsulated in the meeting's Dot Plot which showed participants largely divided between no cuts and 2 cuts by year-end.

- "Two Kevins Battle to Be Next Fed Chair in Trump's 'Apprentice'-Style Contest -- WSJ". "Two Republicans named Kevin are vying to be the next chairman of the Federal Reserve. One is rising to the top of the list of potential candidates, while the other is facing skepticism from President Trump's allies." - BBG

- Data/Events: Bond investors will be focusing on the Fed Minutes tonight and the demand for 10 & 30-year maturities this week.

AUSSIE BONDS: Cheaper As Post-RBA Fallout Continues

ACGBs (YM -7.0 & XM -8.0) are weaker and near session cheaps as the fall-out from yesterday’s surprising RBA decision continued.

- (AFR) At least two Labor appointees to the Reserve Bank of Australia monetary policy board, Jenny Wilkinson and Iain Ross, almost certainly voted for an interest rate cut on Tuesday, according to former RBA insiders. Wilkinson is Treasury secretary to Jim Chalmers and Ross is a former union-aligned pay setter. But the identity of the third dissenter in the shock 6-3 decision to hold the cash rate unchanged at 3.85 per cent is more of a mystery.

- Cash US tsys are ~1bp cheaper in today’s Asia-Pac session after yesterday’s modest sell-off.

- Cash ACGBs are 6-8bps with the AU-US 10-year yield differential at -7bps.

- The bills strip are 3-5bps cheaper.

- RBA-dated OIS pricing is modestly firmer across meetings today after shunting higher yesterday. A 25bp rate cut yesterday was given a 92% probability by the market ahead of the decision. Currently, pricing across meetings is 10-19bps firmer than yesterday’s pre-RBA levels. A cumulative 60bps of easing is priced by year-end (based on an effective cash rate of 3.84%) versus 75bps before the RBA decision.