AUSSIE BONDS: Modest Bear-Flattener On A Data-Light Session

ACGBs (YM -1.5& XM -0.5) are slightly weaker after another subdued data-light session.

- Cash US tsys are slightly mixed in today's Asia-Pac session after yesterday's modest sell-off.

- Cash ACGBs have bear-flattened, with yields flat to 2bps higher and the AU-US 10-year yield differential at flat.

- Bloomberg - The slump in the US dollar is convincing Australia's individual investors to seek protection for their American investments. Retail investors have poured a record $320 million into BlackRock's Australian-dollar hedged S&P 500 Index exchange-traded fund this year. Damien McIntyre, chief executive of GSFM Pty, said Australian investors are "positioning themselves for US dollar weakness".

- The bills strip has bear-steepened, with pricing -1 to -4 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in August is given a 98% probability, with a cumulative 62bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- On Monday, the local calendar will be empty.

- Next week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 2.75% 2 1 November 2029 bond on Friday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Asia FX Wrap - The USD Edges Higher

The BBDXY has had a range of 1196.17 - 1198.60 in the Asia-Pac session, it is currently trading around 1197. The USD has edged higher back towards the overnight highs in a quiet Asia-Pac session, +0.15%. CHINA CPI and PPI Weak Trend Continues: The decline in PPI entered its 33th month as June PPI declined -3.6%. This was the lowest print since July 2023. Manufactured goods prices declined further along with food and mining products. CPI in June inched up by +0.1% YoY as Core CPI rose +0.7% YoY. “With positioning so one-sided, Brent Donnelly says that even a modest pause in foreign hedging or a string of good US headlines could unleash a classic squeeze, dragging EURUSD back toward the 1.14–1.15 “pain zone” and lifting the DXY to its 50- and 100-day moving averages.” - BBG. "DONALD TRUMP DEAL TO LEAVE EU FACING HIGHER TARIFFS THAN UK- FT

- EUR/USD - Asian range 1.1702 - 1.1729, Asia is currently trading 1.1710. The pair failed to hold onto the gains it made on news of a proposed deal with the US, demand seen again just below the 1.1700 area. The price is starting to look a little stretched in the short term and is vulnerable to any correction in the USD, first support is back towards 1.1600 then more importantly the 1.1450 area.

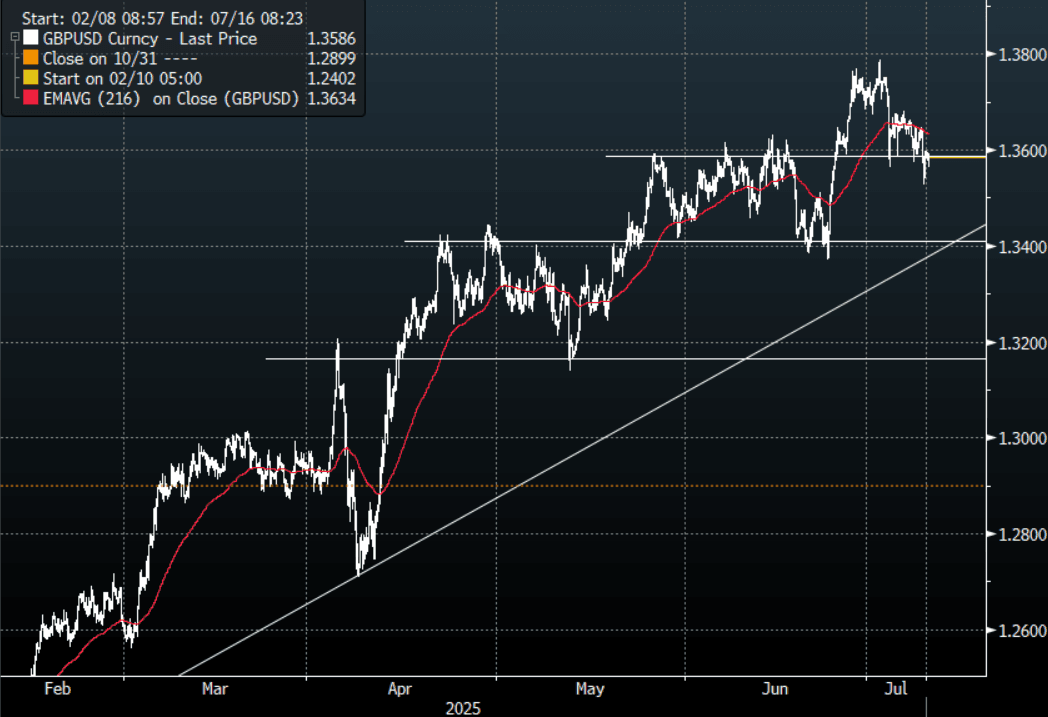

- GBP/USD - Asian range 1.3565 - 1.3595, Asia is currently dealing around 1.3585. Strong demand was again seen on a 1.3500 handle. Price has rejected the move higher and with the USD looking constructive the risk for GBP/USD points to further downside in the short-term. First support around 1.3500 and then more importantly the 1.3350/1.3400 area.

- USD/CNH - Asian range 7.1794 - 7.1866, the USD/CNY fix printed 7.1541, Asia is currently dealing around 7.1850. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.06%, Gold $3295, US 10-Year 4.41%, BBDXY 1197, Crude oil $68.17

Data/Events : Germany CPI, Italy Industrial Production

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Post-RBA Sell-Off Extends

ACGBs (YM -7.0 & XM -9.5) are weaker and near session cheaps as the fall-out from yesterday's surprising RBA decision continued.

- (Bloomberg) Former RBA Assistant Governor Luci Ellis said episodes of the RBA surprising market pricing "will be more common" due to fewer inter-meeting speeches and a reliance on post-decision briefings.

- (AFR, Stephen Miller) “Certainly, the July decision was “cautious” even if the bond market might not have found it “predictable”. However, there is an argument that the certainty with which the bond market regarded a policy rate reduction in July was a reflection of an unbalanced assessment of the evidence. Certainly, the labour market looks to be in robust good health.”

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's modest sell-off.

- Cash ACGBs are 7-9bps with the AU-US 10-year yield differential at -6bps.

- The bills strip are 3-7bps cheaper and steeper.

- RBA-dated OIS pricing is modestly firmer across meetings today after shunting higher yesterday. Currently, pricing across meetings is 10-20bps firmer than yesterday's pre-RBA levels. A cumulative 60bps of easing is priced by year-end versus 75bps before the RBA decision.

- Tomorrow, the local calendar will be empty.

- The AOFM plans to sell A$1000mn of the 2.75% 21 November 2029 bond on Friday.

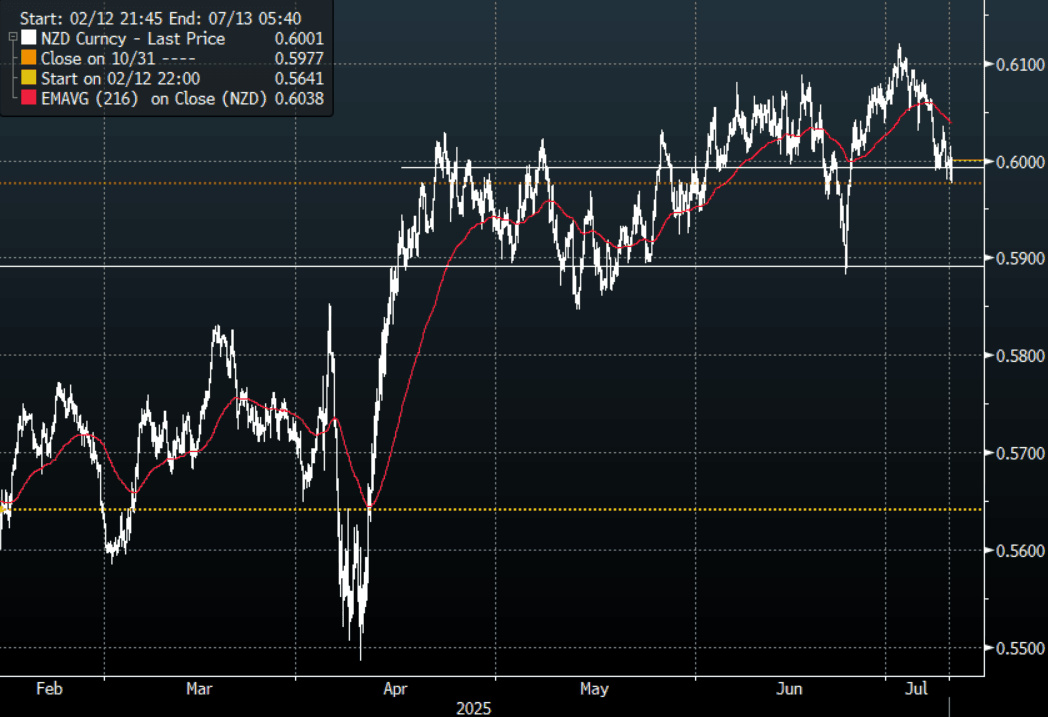

NZD: Asia Wrap - NZD/USD Tests Below 0.6000 Finds Bids As RBNZ Considered A Cut

The NZD/USD had a range of 0.5976 - 0.6014 in the Asia-Pac session, going into the London open trading around 0.6000, +0.03%. The pair was muted after the RBNZ left the benchmark rate unchanged, it initially tested higher but when the RBNZ said it had considered a cut the NZD dropped quickly in response. If there is a deeper correction in risk and the USD can squeeze higher then the risk to the NZD is a move back towards the 0.5850/0.5900 area, the bulls will be hoping the support just below 0.6000 continues to hold.

- RBNZ On Hold, Considered Cutting Rates By 25bps, Awaiting More Information : As widely expected, the RBNZ held the policy rate steady at 3.25%. This was in line with the sell-side consensus (although some forecasters saw risks of a 25bps cut), while market pricing only gave a very small chance to a cut today.

- The RBNZ considered two options at this meeting, to cut by 25bps or hold policy steady. The case to ease largely reflected concerns around faltering economic momentum. The case to hold won out, amid high uncertainty: The RBNZ noted: "Some members emphasized that waiting would allow the Committee to assess whether weakness in the domestic economy persists, and how inflation and inflation expectations evolve."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6075(NZD519m). Upcoming Close Strikes : 0.6000(NZD407m July 10), 0.6025(NZD373m July10).

- CFTC Data shows Asset Managers have reduced their newly built longs in NZD +8515, the Leveraged community reduced their short last week -8424.

- AUD/NZD range for the session has been 1.0868 - 1.0900, currently trading 1.0895. The cross has broken out of its recent range and focus will now turn to the more pivotal 1.0900/50 area.

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P