MNI ASIA OPEN: Ylds Rise, U.Michigan Sentiment Slips, Pre-FOMC

EXECUTIVE SUMMARY

- MNI INTERVIEW: Powell Won't Signal String Of Fed Cuts-Lockhart

- MNI US: Trump Says Patience Running Out With Putin, Offers Vague Threat Of Sanctions

- MNI SECURITY: NATO Launches Eastern Sentry To Bolster Defence Of Border With Russia

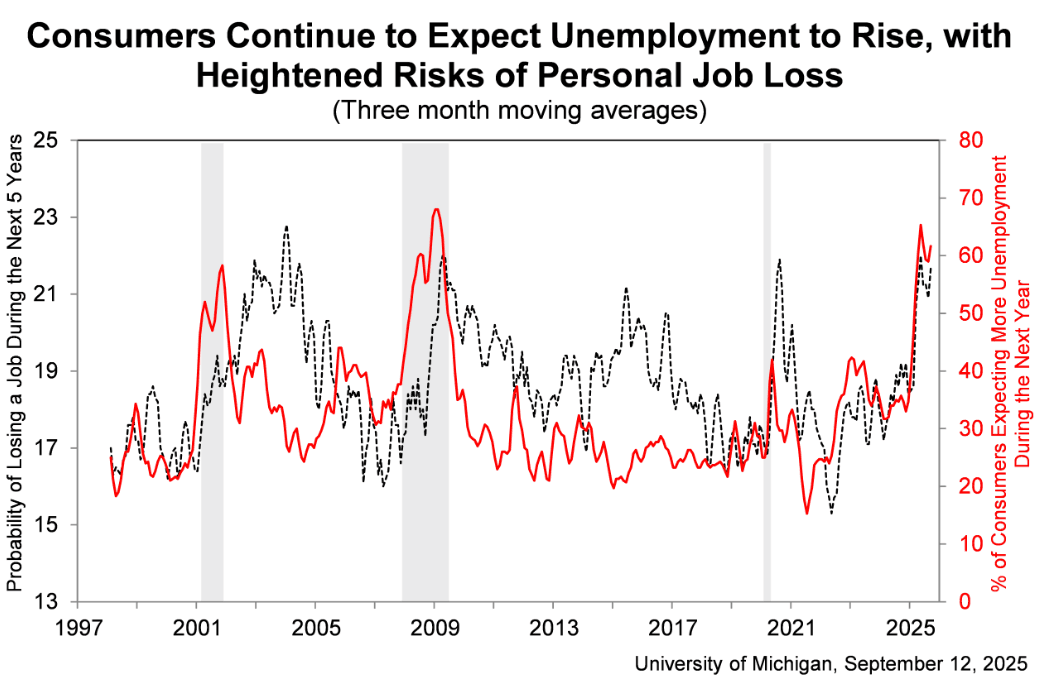

- MNI US DATA: U.Mich Consumer Sentiment Slips With High Likelihood Of Job Losses

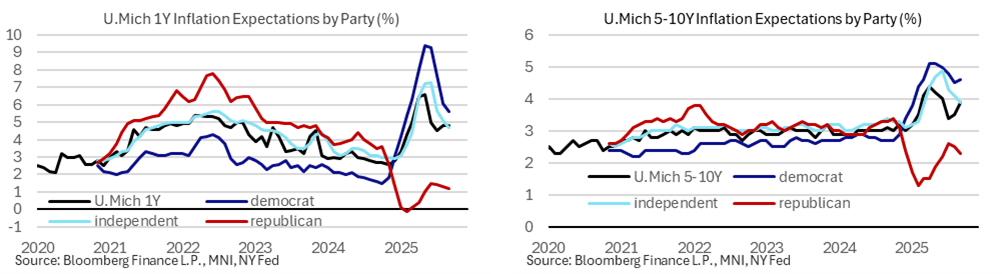

- MNI US DATA: Little Reaction To Stronger Preliminary U.Mich 5-10Y Inflation Expectations

US

MNI INTERVIEW: Powell Won't Signal String Of Fed Cuts-Lockhart

Federal Reserve Chair Jerome Powell will justify next week’s widely expected interest rate cut by citing rising downside risks to employment but refrain from signaling a string of cuts beyond September because the Fed must also contend with inflation heading in the wrong direction, former Atlanta Fed President Dennis Lockhart told MNI. "A 25 bp cut would be a nod to the weakening employment picture, and temporarily at least subordinating the fight against elevated inflation to shoring up support for the employment side of the mandate," he said in an interview.

NEWS

MNI US: Trump Says Patience Running Out With Putin, Offers Vague Threat Of Sanctions

President Donald Trump told Fox News he will be ‘clamping down’ on Russia as his patience is “running out fast” with Russian President Vladimir Putin. Asked what ‘clamping down’ entails, Trump said, “it’ll be hitting very hard with sanctions to banks and having to do with oil and tariffs also.” Trump added, “I’ve done a lot. Look, India was their biggest customer. I put a 50% tariff on India because they are buying oil from Russia. That’s not an easy thing to do.”

MNI SECURITY: NATO Launches Eastern Sentry To Bolster Defence Of Border With Russia

NATO Secretary General Mark Rutte and Supreme Allied Commander Europe General Alexus G. Grynkewich have delivered a joint press conference on the Russian drone incursion at NATO HQ in Brussels, announcing the launch of ‘Eastern Sentry”, a security initiative to bolster defensive posture on NATO's Eastern flank with assets from Denmark, France, the UK, Germany, and others.

MNI SECURITY: Kremlin Says Negotiations With Ukraine Have Been 'Paused'

Kremlin spokesperson Dmitri Peskov told reporters, “There's a pause in Russia-Ukraine negotiations.” Peskov added Russia “remains open to talks,” but European countries are “holding back efforts to find peace in Ukraine,” per Reuters. The comments come amid European efforts to fortify NATO's Eastern flank in response to a Russian drone incursion into Poland that resulted in NATO engaging Russian aircraft in NATO airspace for the first time.

US TSYS

MNI US TSYS: Treasury Yields Rise, Focus on FOMC Rate Decision Next Week

- Treasuries look to finish lower Friday, off lows after tracking a decline in German Bunds heading into the European close. Rates held near lows (TYZ5 113-08) after UoM data - a muted reaction to lower than expected sentiment, 1Y inflation steady while 5-10Y inflation expectation rose: 3.9% (cons 3.4) in Sep prelim after 3.5% in Aug.

- Previously, such an upside for long-term inflation expectations would have sparked a market reaction but not this time. We suspect that’s after August and less so July preliminary readings were marked lower in the final.

- Consumer sentiment surprised lower in the U.Michigan preliminary September report, at 55.4 (cons 58) after 58.2 in Aug. The press release (https://www.sca.isr.umich.edu/) notes more pronounced easing in lower and middle income consumers along with unprompted comments about tariffs.

- Currently, the Dec'25 10Y trades -12 at 113-09 (yld 4.0586% +.0380) vs. 113-04 low - briefly testing initial technical support at 113-05.5/112-215 (Low Sep 10 / 20-day EMA); resistance above at 113-29 (High Sep 5). Curves are mixed: 2s10s +2.595 at 49.879, 5s30s -.898 at 104.744.

- USD fades slightly on the back of the weaker headline - stalling the fade in EUR/USD through early US hours. GBP/USD similarly improves, rising back above 1.3550 to 1.3564.

- Focus in the coming week shifts to the Fed rate decision. A 25bps rate cut remains fully priced, with not insignificant pricing for a 50bps step. This week's inflation data endorsed easing at this juncture, but there remains uncertainty around the magnitude of this rate cut step. Either way, the FOMC will be well aware of the scrutiny over their decision in the Oval Office.

OVERNIGHT DATA

MNI US DATA: U.Mich Consumer Sentiment Slips With High Likelihood Of Job Losses

- Consumer sentiment surprised lower in the U.Michigan preliminary September report, at 55.4 (cons 58) after 58.2 in Aug. The press release (https://www.sca.isr.umich.edu/) notes more pronounced easing in lower and middle income consumers along with unprompted comments about tariffs.

- "This month’s easing in economic views was particularly strong among lower and middle income consumers. Buying conditions for durables improved, while all other index components fell. Consumers continue to note multiple vulnerabilities in the economy, with rising risks to business conditions, labor markets, and inflation. Likewise, consumers perceive risks to their pocketbooks as well; current and expected personal finances both eased about 8% this month.

- Trade policy remains highly salient to consumers, with about 60% of consumers providing unprompted comments about tariffs during interviews, little changed from last month. Still, sentiment remains above April and May 2025 readings, immediately after the initial announcement of reciprocal tariffs."

- Also of note, the featured chart shows still high perceived probability of losing a job:

MNI US DATA: Little Reaction To Stronger Preliminary U.Mich 5-10Y Inflation Expectations

- 1Y inflation expectations: 4.8% (cons 4.8) in Sep prelim after 4.8% in Aug.

- 5-10Y inflation expectations: 3.9% (cons 3.4) in Sep prelim after 3.5% in Aug.

- Previously, such an upside for long-term inflation expectations would have sparked a market reaction but not this time. We suspect that’s after August and less so July preliminary readings were marked lower in the final.

- This could be down to relatively higher responses from Democrat-leaning respondents early in collection period (pure conjecture with no way of knowing from public data) with a still sizeable split by party affiliation: 4.6% Democrat, 3.9% Independent and 2.3% Republican.

- The August report jumped from 3.4% to 3.9% in the preliminary reading before revised down to 3.5%

- The July report wasn’t the same situation but still saw a downward revision with the final reading. It was initially reported at 3.6% before being revised down to 3.4%.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 273.78 points (-0.59%) at 45834.22

S&P E-Mini Future down 5 points (-0.08%) at 6587.75

Nasdaq up 98 points (0.4%) at 22141.1

US 10-Yr yield is up 4 bps at 4.0605%

US Dec 10-Yr futures are down 13/32 at 113-8

EURUSD up 0.0002 (0.02%) at 1.1736

USDJPY up 0.37 (0.25%) at 147.59

WTI Crude Oil (front-month) up $0.15 (0.24%) at $62.52

Gold is up $10.37 (0.29%) at $3644.68

European bourses closing levels:

EuroStoxx 50 up 3.94 points (0.07%) at 5390.71

FTSE 100 down 14.29 points (-0.15%) at 9283.29

German DAX down 5.5 points (-0.02%) at 23698.15

French CAC 40 up 1.72 points (0.02%) at 7825.24

US TREASURY FUTURES CLOSE

3M10Y +4.382, 2.995 (L: -1.869 / H: 5.101)

2Y10Y +2.994, 50.278 (L: 47.378 / H: 51.251)

2Y30Y +1.315, 111.889 (L: 108.982 / H: 114.716)

5Y30Y -0.878, 104.764 (L: 103.452 / H: 107.842)

Current futures levels:

Dec 2-Yr futures down 2.25/32 at 104-11.625 (L: 104-10.625 / H: 104-13.25)

Dec 5-Yr futures down 7.25/32 at 109-21.5 (L: 109-19.5 / H: 109-27)

Dec 10-Yr futures down 13/32 at 113-8 (L: 113-04 / H: 113-18)

Dec 30-Yr futures down 19/32 at 117-12 (L: 117-00 / H: 117-28)

Dec Ultra futures down 17/32 at 121-5 (L: 120-19 / H: 121-25)

MNI US 10YR FUTURE TECHS: (Z5) Bulls Remain In The Driver’s Seat

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-05 1.0% 10-dma envelope

- RES 2: 114-00 Round number resistance

- RES 1: 113-29 High Sep 5

- PRICE: 113-09 @ 1516 ET Sep 12

- SUP 1: 113-04+/112-21+ Low Sep 12 / 20-day EMA

- SUP 2: 112-00+ 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

Treasury futures rallied to a fresh cycle high Thursday, allowing the contract to build on the bulk of its latest gains. Note that the recent impulsive rally highlights an acceleration of the uptrend. Also, moving average studies are in a bull-mode position, highlighting a dominant uptrend. This suggests scope for an extension through 114-00 next and a test of 114-10, the Apr 7 high (cont). Initial firm support to watch is 112-21+, the 20-day EMA.

SOFR FUTURES CLOSE

Current White pack (Sep 25-Jun 26):

Sep 25 -0.028 at 95.960

Dec 25 -0.030 at 96.360

Mar 26 -0.030 at 96.595

Jun 26 -0.035 at 96.820

Red Pack (Sep 26-Jun 27) -0.045 to -0.035

Green Pack (Sep 27-Jun 28) -0.045 to -0.045

Blue Pack (Sep 28-Jun 29) -0.05 to -0.045

Gold Pack (Sep 29-Jun 30) -0.055 to -0.045

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.41% (+0.02), volume: $2.828T

- Broad General Collateral Rate (BGCR): 4.38% (+0.01), volume: $1.147T

- Tri-Party General Collateral Rate (TCR): 4.38% (+0.01), volume: $1.120T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $117B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $214B

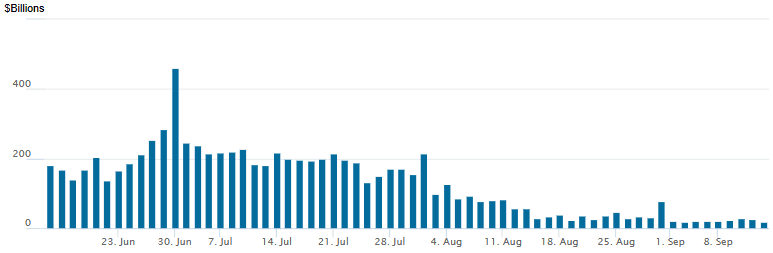

FED Reverse Repo Operation

RRP usage retreats to new lowest levels since early April 2021: $17.331B with 16 counterparties this afternoon from $26.897B Thursday. Compares to prior low of $17.923B on Wednesday, Sep 3. This year's high usage of $460.731B occurred on June 30.

MNI BONDS: EGBs-GILTS CASH CLOSE: Soft Close Cements Bear Flattening For The Week

Gilts underperformed Bunds across respective curves Friday.

- Gilts picked up where Bunds left off post-ECB with some bear flattening early, with oil prices ticking up and BOE/TNS inflation expectations coming in on the high side (UK GDP data was largely in line but brought little reaction).

- BTPs underperformed across periphery/semi-core EGBs, but OATs lead a selloff in afternoon trade, amid concerns about a possible ratings downgrade from Fitch after the cash close.

- Final inflation data for France / Spain / Germany was uneventful. Multiple ECB speakers appearing Friday didn't have much market impact, largely echoing Thursday's hawkish-leaning tone from Lagarde (with the usual exception of Villeroy).

- For the week, there was bear flattening in both the UK (2Y +7.4bp, 10Y +2.5bp) and German (2Y +8.9bp, 10Y +5.3bp) curves.

- UK developments highlight next week's calendar, including labour market and inflation data, and the BOE meeting.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.2bps at 2.018%, 5-Yr is up 5bps at 2.307%, 10-Yr is up 5.8bps at 2.715%, and 30-Yr is up 4.3bps at 3.298%.

- UK: The 2-Yr yield is up 5.3bps at 3.984%, 5-Yr is up 5.3bps at 4.096%, 10-Yr is up 6.5bps at 4.671%, and 30-Yr is up 5.8bps at 5.496%.

- Italian BTP spread up 1.3bps at 80.8bps / French OAT up 0.5bps at 79.3bps

MNI FOREX: USD Rally Backed Up by Yields, But Conviction Low into Fed Meeting

- The USD rallied against all others Friday as markets backtracked a small part of the spell of weakness that followed Thursday's weekly jobless claims print. While equity markets were generally stable outside of a phase of selling through the European open, Treasuries faltered throughout Friday trade, providing a further tailwind to the greenback.

- That said, EUR/USD weakness failed to make any headway back below the 1.1700 handle as markets saw the first ECB governing council members speak after the Thursday rate decision. The divide among the council was clear, with Villeroy raising the possibility of further easing measures ahead, while both Kazaks and Simkus were less convictive in their approach.

- USD/JPY rallied well, while EUR/JPY remained inside the broader uptrend. A Kyodo news poll showed Thatcherite MP Takaichi leading opinion polling for the leadership race in the LDP (and thereby next PM of Japan). Her well known stance for fiscal spending as well as her recent criticism of the BoJ's rate hiking plans worked against the currency, keeping resistance into 173.91-97 intact for the EUR/JPY cross.

- Focus in the coming week shifts to the Fed rate decision. A 25bps rate cut remains fully priced, with not insignificant pricing for a 50bps step. This week's inflation data endorsed easing at this juncture, but there remains uncertainty around the magnitude of this rate cut step. Either way, the FOMC will be well aware of the scrutiny over their decision in the Oval Office.

- Outside of the Fed decision, UK inflation data and the Bank of England rate decision cross. Markets expect CPI to remain stubborn - keeping the MPC on hold into year-end. Just 9bps of easing are now priced through December, a series low, which is helping GBP/USD hold above the 1.35 handle. Horizontal resistance is seen layered between 1.3590-00, clearance above which will conclude the early September corrective move lower.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 15/09/2025 | 0900/1100 | * | Trade Balance | |

| 15/09/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/09/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/09/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/09/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 15/09/2025 | 1810/2010 | ECB Lagarde at Institut Montaigne Paris | ||

| 15/09/2025 | - | FOMC Meetings with S.E.P. |