BONDS: EGBs-GILTS CASH CLOSE: Soft Close Cements Bear Flattening For The Week

Sep-12 17:15

Gilts underperformed Bunds across respective curves Friday.

- Gilts picked up where Bunds left off post-ECB with some bear flattening early, with oil prices ticking up and BOE/TNS inflation expectations coming in on the high side (UK GDP data was largely in line but brought little reaction).

- BTPs underperformed across periphery/semi-core EGBs, but OATs lead a selloff in afternoon trade, amid concerns about a possible ratings downgrade from Fitch after the cash close.

- Final inflation data for France / Spain / Germany was uneventful. Multiple ECB speakers appearing Friday didn't have much market impact, largely echoing Thursday's hawkish-leaning tone from Lagarde (with the usual exception of Villeroy).

- For the week, there was bear flattening in both the UK (2Y +7.4bp, 10Y +2.5bp) and German (2Y +8.9bp, 10Y +5.3bp) curves.

- UK developments highlight next week's calendar, including labour market and inflation data, and the BOE meeting.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.2bps at 2.018%, 5-Yr is up 5bps at 2.307%, 10-Yr is up 5.8bps at 2.715%, and 30-Yr is up 4.3bps at 3.298%.

- UK: The 2-Yr yield is up 5.3bps at 3.984%, 5-Yr is up 5.3bps at 4.096%, 10-Yr is up 6.5bps at 4.671%, and 30-Yr is up 5.8bps at 5.496%.

- Italian BTP spread up 1.3bps at 80.8bps / French OAT up 0.5bps at 79.3bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURUSD TECHS: Bullish Daily Candle

Aug-13 17:00

- RES 4: 1.1851 High Sep 10 2021

- RES 3: 1.1829 High Jul 01 and the bull trigger

- RES 2: 1.1789 High Jul 24

- RES 1: 1.1730 High Aug 13

- PRICE: 1.1723 @ 15:40 BST Aug 13

- SUP 1: 1.1401 Low Jul 30 and a bear trigger

- SUP 2: 1.1373 Low Jun 10

- SUP 3: 1.1313 Low May 30

- SUP 4: 1.1184 38.2% retracement of the Feb 3 - Jul 1 bull cycle

EUR/USD edged higher Tuesday and is firm again to start the Wednesday session. Prices are extending gains on the clearance of the post-NFP high - keeping the recovery off the late July pullback low intact. This works against the bearish backdrop that had dominated the pullback from 1.1829. The break of firm resistance into 20-day EMA, now at 1.1624, is signaling greater odds of a further reversal higher. Major support below rests at 1.1373 next, the Jun 10 low.

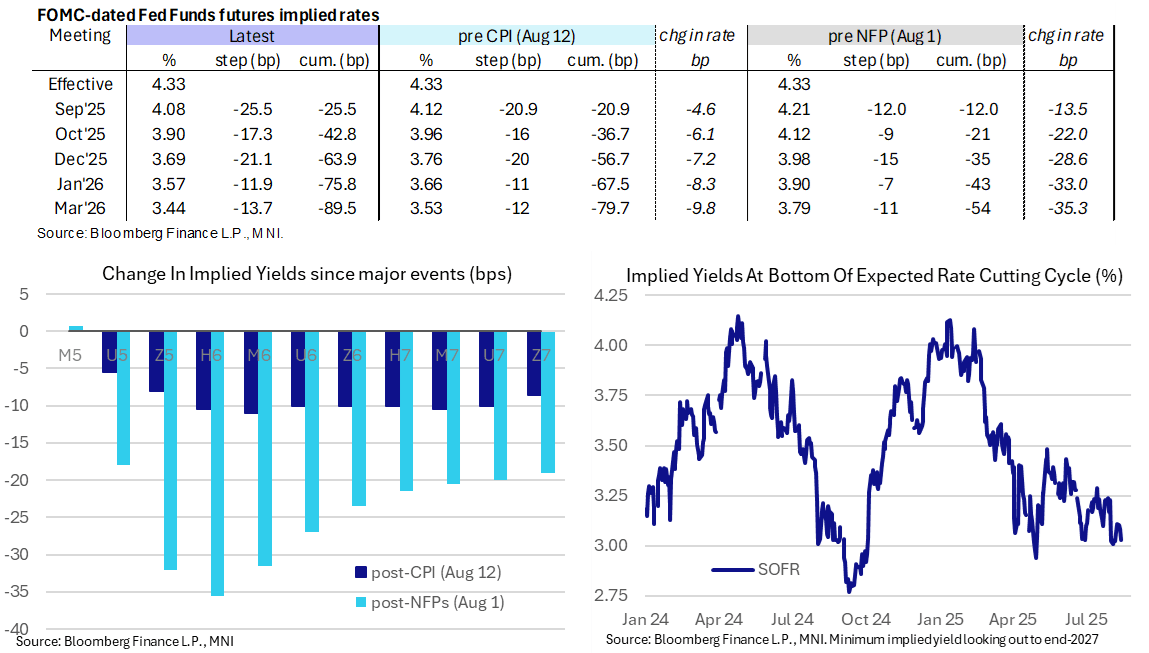

STIR: Up To 64bp Of Fed Cuts By Year-End, Fedspeak Up Shortly

Aug-13 16:58

- Fed Funds implied rates are holding sizeable declines seen on a day with no notable data releases, with the Dec’25 rate 3.5bp lower and Mar’26 5bp lower.

- The 64bp of cuts to year-end is close to recent dovish extremes of 65bp briefly in thin Asia trade after payrolls.

- Tsy Secretary Bessent earlier reiterated his call for a 50bp cut in September, along with stressing that the Fed Funds target range should be 150-175bp lower than it currently is (pointing to the potential for a "series" of rate cuts). He also added to the growing list of candidates to succeed Fed Chair Powell although Trump has since said he sees three or four candidates.

- Cumulative cuts from 4.33% effective: 25.5bp Sep, 43bp Oct, 64bp Dec, 76bp Jan and 89.5bp Mar.

- The SOFR implied terminal yield of 3.03% (SFRH7) is 4.5bp lower on the day, at what would be its lowest close since Aug 6 as it starts to re-approach recent lows.

- Context for upcoming Fedspeak:

- 1300ET - Goolsbee ('25 voter, dove) speaks at a monetary policy luncheon. It's been an unusually long time since Goolsbee last spoke, on Jul 11 saying that he has seen "surprisingly little" impact from tariffs but that new tariff threats (at the time) could delay rate cuts.

- 1330ET - Bostic (non-voter) speaks on the economic outlook (Q&A only). This should be a useful update from Bostic, who said after the July nonfarm payrolls report that he still saw only one rate cut this year. He wants to see how things evolve over the coming months and warned that it might take twelve months for businesses to adjust their prices.

US TSYS: Modestly Off Highs, TYA Yet To Test Resistance

Aug-13 16:52

- Treasuries hold gains seen after rallying through London hours until ~1100ET, before little net impact from Trump’s remarks at The Kennedy Center.

- TYU5 trades at 112-07 (+13) off a latest high of 112-09, although it stopped short of resistance at 112-15 (Aug 5 high). Clearance could open 112-23 (May 1 high).

- Cash yields are 5-6bp lower across the curve, with Treasuries underperforming EGBs throughout the session.

- 2YY currently at 3.681% off a session low of 3.664% vs 3.655% in Monday’s Asia trading in CPI follow through.

- Curves broadly consolidate yesterday’s CPI-driven steepening, with 5s30s at 106bps off yesterday’s 107.6bps having come close to ytd highs of 108.5bps.

- Trump will ask for a “small amount” of money for DC, may have a second meeting with Putin that will also include Zelensky if Friday’s bilateral meeting with Putin is a success, and he sees three or four picks for Fed chair with his pick possibly named a little bit early.

- Fedspeak to come from Goolsbee (1300ET) and Bostic (1330ET) shortly before Trump signs an executive order at 1600ET. Tomorrow then sees PPI and jobless claims data.

Trending Top

Jun-26 16:22