MNI ASIA OPEN: Weeky Claims, Employ Data Suspended on Shutdown

EXECUTIVE SUMMARY

- MNI FED: Gov Cook To Stay In Post Until At Least January Supreme Court Arguments

- MNI US: Speaker Johnson-House To Return Next Week, But Nothing To Negotiate w/Dems

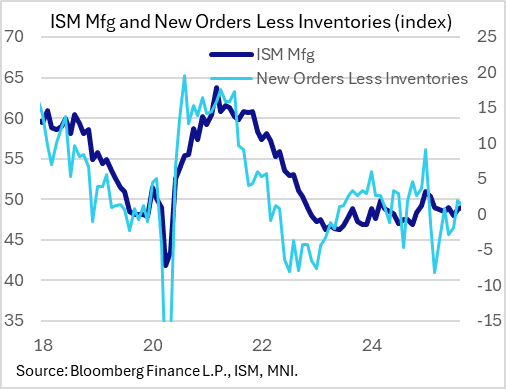

- MNI US DATA: Slight, Uneven Improvement In Manufacturing ISM Amid Soft Demand

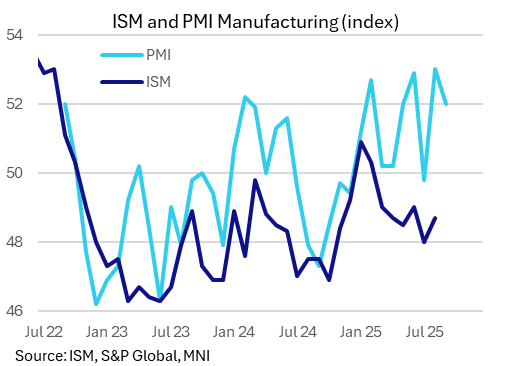

- MNI US DATA: Final Manufacturing PMI Unchanged From Flash, Still Shows Modest Growth

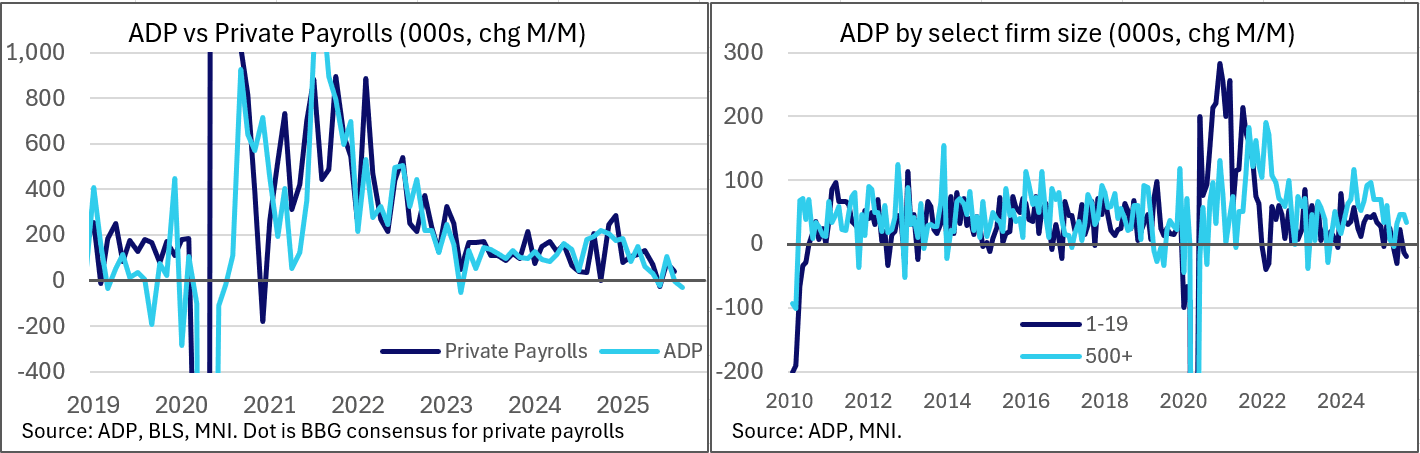

- MNI US DATA: ADP Re-Benchmarking Aside, Weak Private Payrolls Trends Continue

US

MNI FED: Gov Cook To Stay In Post Until At Least January Supreme Court Arguments

The Supreme Court files a notice in "TRUMP, PRESIDENT OF U.S., ET AL. V. COOK, LISA D." that Gov Cook will be allowed to stay in her position (and not "fired" by the White House) until at least an oral argument on the case is heard in January 2026: "The application for stay presented to The Chief Justice and by him referred to the Court is deferred pending oral argument in January 2026. The Clerk is directed to establish a briefing schedule for amici curiae and any supplemental briefs responding to amici."

NEWS

MNI US: Speaker Johnson-House To Return Next Week, But Nothing To Negotiate w/Dems

Speaker of the House of Representatives Mike Johnson (R-LA) confirms that the House will "definitely" return next week, but until that point, “there is nothing truly that we can do much on the floor while the lights are almost literally out here.” Claims House Republicans “would have been here [in Washington, D.C.,] this week, except that we did our work.”

MNI US: Vought Freezes NY City Infrastructure Funds, Applies Pressure On Dem Leaders

White House Office of Management and Budget Director Russell Vought announced on X he is freezing roughly USD$18 billion in funding for infrastructure projects in New York City. Vought wrote, "Roughly $18 billion in New York City infrastructure projects have been put on hold to ensure funding is not flowing based on unconstitutional DEI principles," adding later, "specifically, the Hudson Tunnel Project and the Second Ave Subway."

MNI EU-RUSSIA: More Leaders Support Ukraine 'Reparations Loan', But Obstacles Remain

A growing number of EU leaders are voicing their support for mooted EU plans that could see EUR140bln of frozen Russian assets held in the Union utilised as a zero-interest "reparations loan" for Kyiv. The loan would then only have to be repaid once Russia has, in turn, repaid Ukraine for war damage. European Commission President Ursula von der Leyen said in late September that “We will strengthen our own defence industry by ensuring that part of the loan is used for procurement in Europe and with Europe.”

US TSYS

MNI US TSYS: Taking Delayed/Suspended Data In Stride As Shutdown Gets Underway

- Treasuries look to finish higher - off first half highs after September's ISM Manufacturing Report showed a slight if uneven improvement in sectoral activity. Rates initially gapped higher after much lower than estimated private ADP employment numbers.

- The ADP release for September was weak, showing the biggest private payrolls drop (-32k) since March 2023 and before that, Jun 2020. And the prior 54k was revised down to -3k, so the first back-to-back drops since the pandemic. This was a significant miss for private payrolls versus +51k expected.

- ADP was re-benchmarked, however, resulting in a reduction of 43,000 jobs in September compared to pre-benchmarked data. The trend was unchanged; job creation continued to lose momentum across most sectors."

- Underlying futures climbing again after paring back from late morning highs. Projected rate cut pricing gaining vs. late Tuesday levels (*): Oct'25 at -25.3bp (-24.2bp), Dec'25 at -46.9bp (-44.2bp), Jan'26 at -58.8bp (-53.7bp), Mar'26 at -70.0bp (-64.7bp).

- Thursday's scheduled economic data largely delayed/suspended due to the shutdown - weekly jobless/continuing claims as well as Factory New Orders will not be released

- In other news: Supreme Court rejects Pres Trump's firing of Fed Gov Cook - until at least an oral argument on the case is heard in January 2026. VP Vance expects federal layoffs to start in the next one to two days.

OVERNIGHT DATA

MNI US DATA: Slight, Uneven Improvement In Manufacturing ISM Amid Soft Demand

September's ISM Manufacturing Report showed a slight if uneven improvement in sectoral activity, with the headline index improving as expected but sub-categories coming in mixed. This is indicative of a manufacturing sector contracting, albeit at a slightly slower rate - though as the ISM report reminds, this doesn't mean that the broader economy is contracting (a manufacturing above 42.3 "over a period of time, generally indicates an expansion of the overall economy.")

- The headline PMI of 49.1 edged expectations of an improvement to 49.0 (48.7 prior), and marked a 7-month high.

- New orders fell back into contraction for the 7th month in 8 at 48.9 (50.0 expected, 51.4 prior). Employment picked up more than expected, however, to a 4-month high 45.3 (44.3 expected, 43.8 prior). And Production rose 3.2 points to 51.0, while Backlog of Orders rose 1.5 to 46.2.

MNI US DATA: Final Manufacturing PMI Unchanged From Flash, Still Shows Modest Growth

The final September manufacturing PMI reading was unchanged from the flash report at 52.0 (53.0 prior). The initial reading had been in line with consensus and both suggest a manufacturing sector in modest if slightly weaker expansion in the month, alongside elevated if somewhat softening price pressures. The sustained +50 readings have been cited by some analysts as reason for optimism on upcoming ISM reports (which have been lagging PMI readings for several months).

MNI US DATA: ADP Re-Benchmarking Aside, Weak Private Payrolls Trends Continue

The ADP release for September was weak, showing the biggest private payrolls drop (-32k) since March 2023 and before that, Jun 2020. And the prior 54k was revised down to -3k, so the first back-to-back drops since the pandemic. This was a significant miss for private payrolls versus +51k expected.

- HOWEVER, this should be taken with caution since the ADP re-benchmarked in line with the BLS's QCEW re-benchmarking: "ADP conducted its annual preliminary re-benchmarking of the National Employment Report in September based on the full-year 2024 results of the Quarterly Census of Employment and Wages. This recalibration resulted in a reduction of 43,000 jobs in September compared to pre-benchmarked data. The trend was unchanged; job creation continued to lose momentum across most sectors."

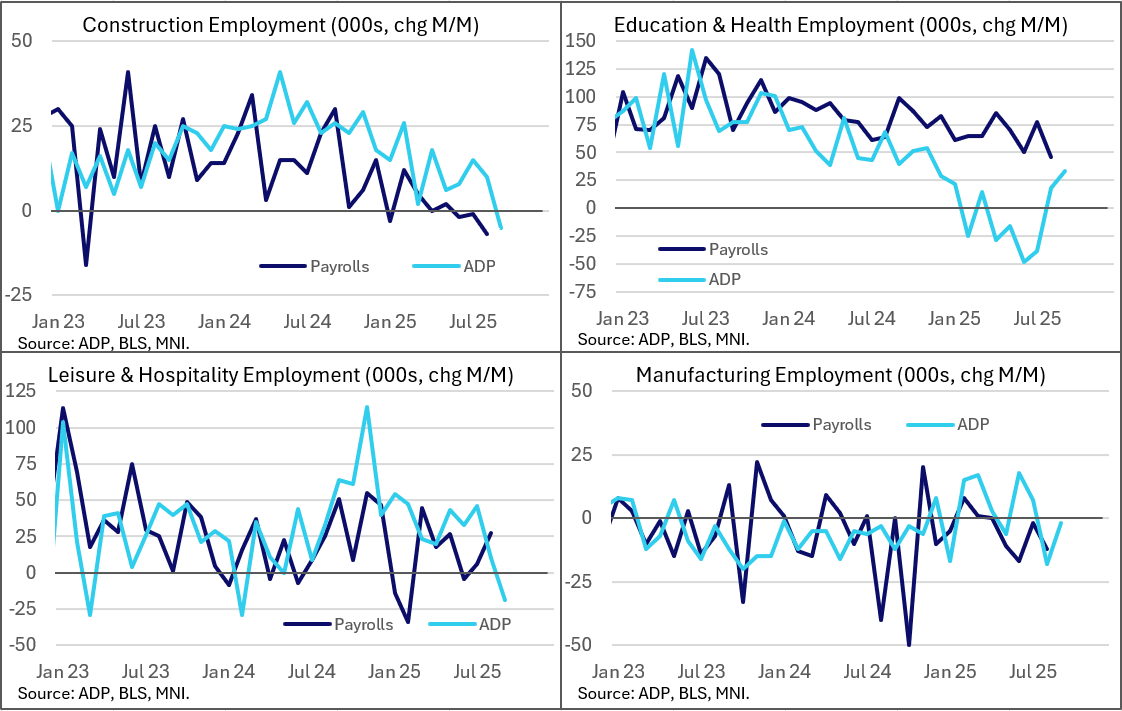

MNI US DATA: ADP Shows Pay, Cyclical Sector Employment Deteriorating

While we take the magnitude of the drop in September's ADP payrolls with a grain of salt given the re-benchmarking impact on the overall sequential change, the data showed widespread weakness across multiple sectors. Goods payrolls fell 3k for the first contraction in 4 months, with services down 28k, worst in 3 months and now marking a third drop in 4. Of 10 covered sectors, just three (natural resources +4k, info tech +3k, education and health +33k) were positive.

MNI US DATA: Final Manufacturing PMI Unchanged From Flash, Still Shows Modest Growth

The final September manufacturing PMI reading was unchanged from the flash report at 52.0 (53.0 prior). The initial reading had been in line with consensus and both suggest a manufacturing sector in modest if slightly weaker expansion in the month, alongside elevated if somewhat softening price pressures. The sustained +50 readings have been cited by some analysts as reason for optimism on upcoming ISM reports (which have been lagging PMI readings for several months).

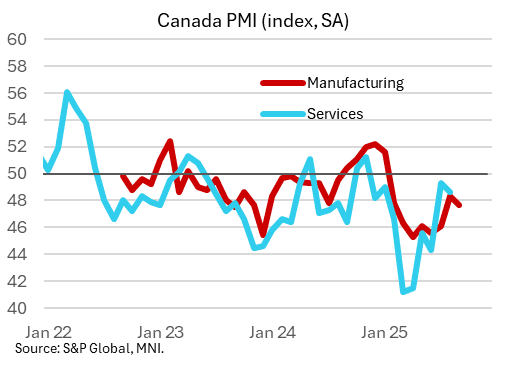

MNI CANADA DATA: Manufacturing PMI Suggests Poor Activity, Softer Price Pressures

Canadian Manufacturing PMI softened in September, to 47.7 (no consensus) from 48.3 prior in what was an overall weak report. August had marked a 7-month high for the index, with the latest move lower keeping it below the 50 mark for an 8th consecutive month. The report showed poor demand, production, exports, and employment in the month, suggesting that a nascent pickup in activity over the summer (highlighted by better-than-expected GDP in July followed by anticipated flat growth in August) lacks momentum, at least in the beleaguered manufacturing sector. Per the S&P Global report:

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 88.12 points (0.19%) at 46484.66

S&P E-Mini Future up 28 points (0.42%) at 6766.5

Nasdaq up 110.1 points (0.5%) at 22769.88

US 10-Yr yield is down 4.1 bps at 4.1097%

US Dec 10-Yr futures are up 9.5/32 at 112-25.5

EURUSD down 0.0001 (-0.01%) at 1.1733

USDJPY down 0.76 (-0.51%) at 147.14

WTI Crude Oil (front-month) down $0.35 (-0.56%) at $62.02

Gold is up $5.78 (0.15%) at $3865.14

European bourses closing levels:

EuroStoxx 50 up 51.25 points (0.93%) at 5581.21

FTSE 100 up 96 points (1.03%) at 9446.43

German DAX up 232.9 points (0.98%) at 24113.62

French CAC 40 up 71.01 points (0.9%) at 7966.95

US TREASURY FUTURES CLOSE

3M10Y -3.501, 17 (L: 14.171 / H: 20.757)

2Y10Y +2.279, 56.27 (L: 53.033 / H: 56.475)

2Y30Y +5.068, 117.131 (L: 111.654 / H: 117.443)

5Y30Y +4.44, 103.288 (L: 99.074 / H: 103.837)

Current futures levels:

Dec 2-Yr futures up 3.375/32 at 104-9.75 (L: 104-05.25 / H: 104-10.5)

Dec 5-Yr futures up 7/32 at 109-13.25 (L: 109-03.75 / H: 109-16.5)

Dec 10-Yr futures up 9.5/32 at 112-25.5 (L: 112-12 / H: 112-31)

Dec 30-Yr futures up 10/32 at 116-29 (L: 116-07 / H: 117-12)

Dec Ultra futures up 7/32 at 120-9 (L: 119-20 / H: 120-30)

MNI US 10YR FUTURE TECHS: (Z5) Bounces Off Support At The 50-Day EMA

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-12/29 High Sep 18 / High Sep 11 and the bull trigger

- RES 1: 112-31/113-00 High Oct 01 / High Sep 24

- PRICE: 112-22+ @ 16:41 BST Oct 1

- SUP 1: 112-01 50.0% retracement of the Jul 15 - Sep 11 bull phase

- SUP 2: 111-26 Low Aug 26

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 111-01+ 76.4% retracement of the Jul 15 - Sep 11 bull phase

Prices bounced Wednesday, despite the short-term bear cycle. Recent weakness has resulted in a print below the 50-day EMA, currently at 112-10+. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13+, the Aug 18 low and the next key support. On the upside, initial firm resistance to watch is unchanged, at 113-00, the Sep 24 high.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 +0.040 at 96.355

Mar 26 +0.060 at 96.565

Jun 26 +0.070 at 96.785

Sep 26 +0.065 at 96.915

Red Pack (Dec 26-Sep 27) +0.050 to +0.065

Green Pack (Dec 27-Sep 28) +0.045 to +0.050

Blue Pack (Dec 28-Sep 29) +0.040 to +0.040

Gold Pack (Dec 29-Sep 30) +0.030 to +0.035

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.24% (+0.11), volume: $3.148T

- Broad General Collateral Rate (BGCR): 4.20% (+0.08), volume: $1.140T

- Tri-Party General Collateral Rate (TCR): 4.20% (+0.08), volume: $1.101T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $155B

FED Reverse Repo Operation - New Multi Year Low

With October underway - RRP usage falls to the lowest level since early April 2021 this afternoon: $10.179B with 15 counterparties, down from $49.071B Tuesday. Compares to the year's high usage of $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: $2B Vistra Operations 2Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 10/01 $2.5B #Bahrain $1.5B +8Y Sukuk 5.875%, $1B 12Y 6.625%

- 10/01 $2B #Vistra Operations $750M 3Y +75, $500M 5Y +93, $750M 10Y +118

- 10/01 $750M Alpha Generation $750M 8.25NC3 6.375%

- 10/01 $500M #Convatec Group 10Y +125

- 10/01 $500M Jane Street Grp 2033 tap

- 10/01 $Benchmark IFC 5Y SOFR+38

MNI BONDS: EGBs-GILTS CASH CLOSE: Yields Fade Early Rise

European curves steepened Wednesday, with Gilts slightly outperforming Bunds.

- Yields were higher in early trade, amid uncertainty over the U.S. federal government shutdown that started overnight, and supply weighing somewhat (E5B of 10Y Bund).

- However, the tone was lightened as data proved to be on the dovish side: Italian and Spanish PMIs disappointed, while yields saw the biggest move of the day (to the downside) as US ADP private payrolls unexpectedly contracted. Eurozone HICP came in broadly in line with consensus.

- On the day, the German and UK curves both twist steepened.

- Periphery/semi-core EGB spreads closed a little tighter, with BTPs outperforming.

- Thursday's schedule includes French industrial production and Spanish labor market data, with DMP inflation expectations the highlight of the UK docket. There will also be attention on Swiss inflation, as well as appearances by ECB's Makhlouf, Villeroy and de Guindos.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at 2.013%, 5-Yr is down 0.8bps at 2.301%, 10-Yr is up 0.2bps at 2.713%, and 30-Yr is up 1.8bps at 3.298%.

- UK: The 2-Yr yield is down 2bps at 3.965%, 5-Yr is down 1.9bps at 4.117%, 10-Yr is down 0.3bps at 4.696%, and 30-Yr is up 0.5bps at 5.511%.

- Italian BTP spread down 1bps at 81.3bps / French OAT down 0.5bps at 81.7bps

MNI FOREX: JPY Strength Extends Amid US Shutdown, Soft ADP Jobs Data

- Wednesday’s session was dominated by the appreciating Japanese Yen, with several factors contributing to the extension of strength this week. First of all, ongoing concerns surrounding the US Government shutdown and uncertainty regarding upcoming data releases have weighed on USDJPY. Secondly, Tankan survey indicated solid business sentiment and earnings in September, likely to increase the odds of an October BOJ rate hike. Thirdly, weaker-than-expected US ADP employment data prompted a bump lower for US yields, providing an additional yen tailwind.

- USDJPY dipped to a low of 146.59 following the US data, extending the pullback from last week’s highs to 2.25%. Subsequently, the pair has found some support and risen back above the 147 handle as we approach the APAC crossover. Potentially assisting the bounce was comments by US speaker Johnson stating he hopes for a shutdown breakthrough today.

- The New Zealand dollar has also been an outperformer across G10, with NZDUSD notably rising back above the significant 0.5800 pivot point. Kiwi’s outperformance has helped stall the topside momentum of AUDNZD, which registered a fresh 3-year high of 1.1418 yesterday. The cross has moved back to 1.1365 today, and support is not seen until 1.1250, the 20-day EMA.

- The Canadian Dollar is among the worst performers in G10 today as USDCAD holds close to recent highs. A breach of 1.3959 would place the pair at four-month highs. Additionally, a number of CAD crosses are at notable technical levels, with CADJPY breaching an important cluster of support and AUDCAD threatening to break above trendline resistance, drawn from the 2021 highs.

- The Swiss Franc also weakened by 0.25% Wednesday ahead of September CPI data due on Thursday. Despite this, EURCHF remains in consolidation mode, respecting the well established and familiar range between 0.93-0.94.

- US jobless claims would be in focus Thursday ahead of NFP on Friday, although the release of the data remains unlikely owing to the current government shutdown.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 02/10/2025 | 0630/0830 | *** | CPI | |

| 02/10/2025 | 0830/0930 | Decision Maker Panel data | ||

| 02/10/2025 | 0900/1100 | ** | EZ Unemployment | |

| 02/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 02/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 02/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 02/10/2025 | 1430/1030 | Dallas Fed's Lorie Logan | ||

| 02/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 02/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 02/10/2025 | 1700/1900 | ECB de Guindos Fireside Chat at ESADE Madrid | ||

| 02/10/2025 | 1725/1325 | BOC Deputy Mendes speaks at Western University | ||

| 03/10/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/10/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/10/2025 | 2330/0830 | * | Labor Force Survey | |

| 03/10/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/10/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI |