BONDS: EGBs-GILTS CASH CLOSE: Yields Fade Early Rise

Oct-01 18:37

European curves steepened Wednesday, with Gilts slightly outperforming Bunds.

- Yields were higher in early trade, amid uncertainty over the U.S. federal government shutdown that started overnight, and supply weighing somewhat (E5B of 10Y Bund).

- However, the tone was lightened as data proved to be on the dovish side: Italian and Spanish PMIs disappointed, while yields saw the biggest move of the day (to the downside) as US ADP private payrolls unexpectedly contracted. Eurozone HICP came in broadly in line with consensus.

- On the day, the German and UK curves both twist steepened.

- Periphery/semi-core EGB spreads closed a little tighter, with BTPs outperforming.

- Thursday's schedule includes French industrial production and Spanish labor market data, with DMP inflation expectations the highlight of the UK docket. There will also be attention on Swiss inflation, as well as appearances by ECB's Makhlouf, Villeroy and de Guindos.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at 2.013%, 5-Yr is down 0.8bps at 2.301%, 10-Yr is up 0.2bps at 2.713%, and 30-Yr is up 1.8bps at 3.298%.

- UK: The 2-Yr yield is down 2bps at 3.965%, 5-Yr is down 1.9bps at 4.117%, 10-Yr is down 0.3bps at 4.696%, and 30-Yr is up 0.5bps at 5.511%.

- Italian BTP spread down 1bps at 81.3bps / French OAT down 0.5bps at 81.7bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

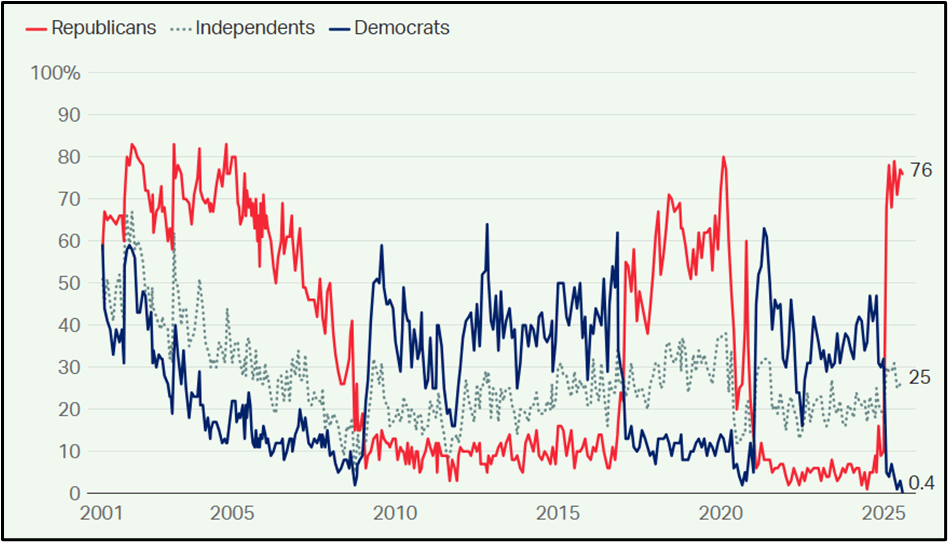

US: Partisan Polarisation Increases, Economic Confidence Index Dips Slightly

Sep-01 17:51

Gallup’s Economic Confidence Index, "which takes into account evaluations of current economic conditions and perceptions of the economy’s direction, is at -20 in August, a bit less negative than the -26 measured in October and -22 in April — but not to the point seen in June, when it rose to -14."

- The Wall Street Journal reports that, “After months of tracking high-income earners’ positive economic outlook, America’s middle-income households appear to be losing confidence”.

- Gallup notes: “Similar to the trend in economic confidence, the 31% of Americans who currently say they are satisfied with the direction of the country is higher than the 26% recorded in late October, as well as the average 22% throughout Biden’s presidency. However, it has waned after reaching 38% in May, the highest of Trump’s second term.”

- Gallup notes: “Partisanship is also at a peak on this metric, with 76% of Republicans saying they are satisfied with the direction of the country versus less than 1% of Democrats. The resulting 76-point gap is the highest Gallup has recorded on this measure, although not substantially different from a 75-point gap in May and 74 points in March and July.”

Figure 1: “In general, are you satisfied or dissatisfied with the way things are going in the United States at this time?”

Source: Gallup

COMMODITIES: Crude Rallies, Precious Metals Extend Gains

Sep-01 17:20

- Crude is trading higher on Monday, with Russian supply concerns and Indian buying in focus. Attention is also turning to the next OPEC+ meeting, scheduled for Sept 7.

- WTI Oct 25 is up by 1.1% at $64.7/bbl.

- Overall, Russian crude exports face pressure, running at a four-week low. However, Indian demand remains firm despite US threats and tariffs.

- From a technical perspective, a bear cycle in WTI futures remains intact and the latest recovery appears corrective.

- Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $66.56, the Aug 4 high.

- Meanwhile, spot gold has risen by 0.8% today to $3,476/oz, amid ongoing questions surrounding Fed independence and focus on the potential for a round of Fed easing.

- Initial US dollar weakness helped the yellow metal rise to a high of $3,490 earlier in the session, before bullion moved away from best levels amid a stabilisation in the greenback.

- The primary trend direction for gold remains up, and sights are on key resistance and the bull trigger at $3,500.1, the Apr 22 all-time high. Clearance of this hurdle would confirm a resumption of the uptrend and open $3,547.9, a Fibonacci projection.

- Elsewhere, silver has outperformed today, with the precious metal up by 2.4% at $40.68/oz.

- Trend signals in silver remain bullish, with sights on $41.064 next, a Fibonacci projection.

US TSYS: Mildly Cheaper At The Labor Day Early Close

Sep-01 17:07

- Treasury futures dealt mildly cheaper at the early close for Labor Day after an unsurprisingly quiet session. There was no cash trading due to the holiday.

- Sell-off cues were taken from some mild weakness in EGBs on supply grounds.

- TYZ5 at 112-11+ (-04+) on cumulative volumes of 208k. An earlier low of 112-09+ saw lows since Aug 27, but as opposed to some support clearance in EGBs it didn’t come close to troubling support at 111-31 (20-day EMA).

- Technicals suggest the trend structure remains bullish with resistance at 112-20+ (Aug 28 high).

- At the front end, Fed Funds futures were mixed for near-term meetings, with Sept cut pricing building very slightly to 22.5bp priced vs a 0.5bp trimming for Dec with a cumulative 55.5bp.

- SOFR futures implied yields were up to 2.5bp higher from Friday’s close, with increases led by the SFRH7 which continues to see a terminal yield of sub-3% at 2.97% for ~135bp of cuts from current levels.

- President Trump’s Truth Social activity has also been light so far today, saying India’s offer to cut tariff rates to zero is getting late, hinting at pushes to tackle crime in Chicago, LA, NY and Baltimore and pushing “Pfizer and others” to show Covid drug success.

- US Tsy Sec Bessent meanwhile suggests that Trump may declare a “national housing emergency” this fall to address rising house prices, something last seen in 2008.

- Tomorrow is headlined by ISM mfg for August before labor data starts to take over in the usual build-up to the nonfarm payrolls report for August on Friday.