US DATA: Slight, Uneven Improvement In Manufacturing ISM Amid Soft Demand

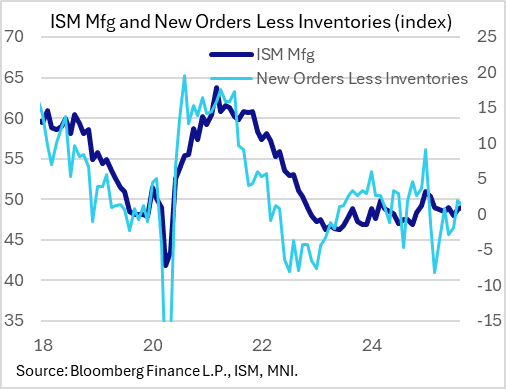

September's ISM Manufacturing Report showed a slight if uneven improvement in sectoral activity, with the headline index improving as expected but sub-categories coming in mixed. This is indicative of a manufacturing sector contracting, albeit at a slightly slower rate - though as the ISM report reminds, this doesn't mean that the broader economy is contracting (a manufacturing above 42.3 "over a period of time, generally indicates an expansion of the overall economy.")

- The headline PMI of 49.1 edged expectations of an improvement to 49.0 (48.7 prior), and marked a 7-month high.

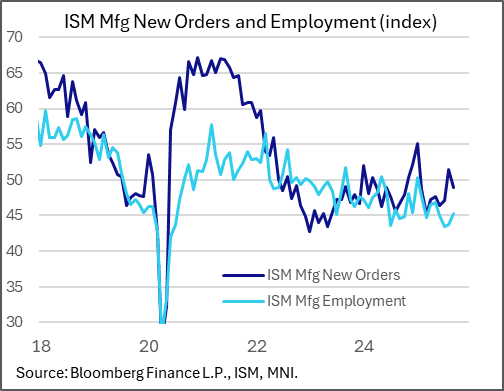

- New orders fell back into contraction for the 7th month in 8 at 48.9 (50.0 expected, 51.4 prior). Employment picked up more than expected, however, to a 4-month high 45.3 (44.3 expected, 43.8 prior). And Production rose 3.2 points to 51.0, while Backlog of Orders rose 1.5 to 46.2.

- The sequence here is described by the ISM: the prior "increase in new orders (an index gain of 4.3 percentage points from July to August) seems to have flowed through to production but does not appear to be sustainable given the subsequent drop in new orders in September." That said, new orders still slightly exceed inventories (47.7), which historically has been suggestive that future production is in the pipeline.

- New Export Orders fell 4.6 points to 43.0, for a 7th consecutive contraction, with imports down 1.3 points to 44.7. Both were 4-month lows.

- Even so, the two "output" (Production and Employment) indices improved. But just 1 of 4 "demand" indicators (Backlog of Orders) improved, vs faster contractions in New Orders, New Export Orders, and Customers' Inventories. And "inputs" (supplier deliveries, inventories, prices, imports) on total moved into contractionary territory (supplier deliveries slowed, which contributes to a higher ISM index).

- On that note, though, Prices Paid fell more than anticipated, to an 8-month low 61.9 (62.7 expected, 63.7 prior), suggesting that largely tariff-related inflationary pressures peaked this summer but remain at an elevated rate.

- More broadly, the anecdotes were overwhelmingly negative, with several complaints about tariff and interest rate policy, as well as citing weaker demand.

- On the Employment front, the weaker headline reading came with some color suggestive of a low-hiring, low-firing environment: "64 percent of panelists’ comments still indicated that managing head count is still the norm at their companies, as opposed to hiring...Of the six big manufacturing sectors, none reported higher levels of employment in September. For every comment on hiring, there were three on reducing head counts as companies continued to focus on accelerating staff reductions due to uncertain near- to mid-term demand."

- On New Orders, “Of the six largest manufacturing sectors, none reported increased new orders. For every positive comment about new orders, there were 1.6 comments expressing concern about near-term demand, primarily driven by tariff costs and uncertainty."

- On Prices Paid: "The Prices Index reading continues to be driven by increases in steel and aluminum prices that impact the entire value chain, as well as tariffs applied to many imported goods."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SEK: Most notable move in EURSEK

- Today is the most notable single move in the EURSEK in a Month, since 1st August ~9 big figures range.

- For now the cross seems to be finding some support at the Psychological 11.0000 level.

- The early chart to watch was the USDSEK, now close to testing the 2025 low.

EGBS: Limited Benefit To Bunds From OAT Weakness

Goldman Sachs note that “although French assets have been under pressure, spillovers to the rest of Europe - and to EGBs in particular – have been contained. Ongoing declines in rates volatility help to contain risks to other sovereign spread markets. And there has been limited richening in Bunds vs. swaps compared to last year’s snap elections”.

- They provide two possible explanations:

- “Uncertainty in France has not reached the same level as last year, with parliamentary elections likely not yet widely expected and less speculation about President Macron resigning. In the same vein, markets may be drawing some comfort from having witnessed the relatively smooth transition from the Barnier to the Bayrou government last November”.

- “With the ECB cutting cycle now over, German fiscal easing underway, and a more challenging duration backdrop globally, the prospect of substantial Bund outperformance is dimmer”.

- Ultimately, Goldman continue to “expect Bunds to cheapen, both in outright terms and against swaps. That said, to the extent that we expect the cheapening in Bunds vs. swaps to be gradual, the increased tail risk in France and lack of reaction in swap spreads so far diminish the risk reward for tighteners, in our view”.

US: Trump Says India Offers 0% Tariffs, But Getting Late

U.S. President Trump posts the following to Truth Social "What few people understand is that we do very little business with India, but they do a tremendous amount of business with us. In other words, they sell us massive amounts of goods, their biggest “client,” but we sell them very little - Until now a totally one sided relationship, and it has been for many decades. The reason is that India has charged us, until now, such high Tariffs, the most of any country, that our businesses are unable to sell into India. It has been a totally one sided disaster! Also, India buys most of its oil and military products from Russia, very little from the U.S. They have now offered to cut their Tariffs to nothing, but it’s getting late. They should have done so years ago. Just some simple facts for people to ponder!!!"