MNI ASIA OPEN: Strong Dovish Reaction to CPI, Weekly Claims

EXECUTIVE SUMMARY

- MNI: Bullard Interviewed By Bessent For Fed Chair Job

- MNI BRIEF: ECB On Hold, Little Change in Inflation Outlook

- MNI US DATA: CPI Inflation Breadth Widened Further In August

- MNI US: Schumer Reiterates That Democrats Won't Accept 'Clean' Funding Extension

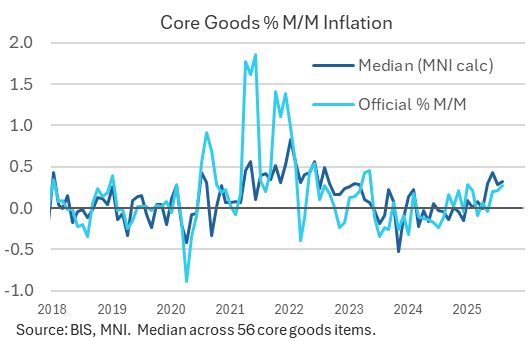

- MNI US DATA: Further Robust CPI Core Goods Details But No Additional Acceleration

- MNI US DATA: Core CPI Categories Mixed Vs Expectations, PCE Looks Benign

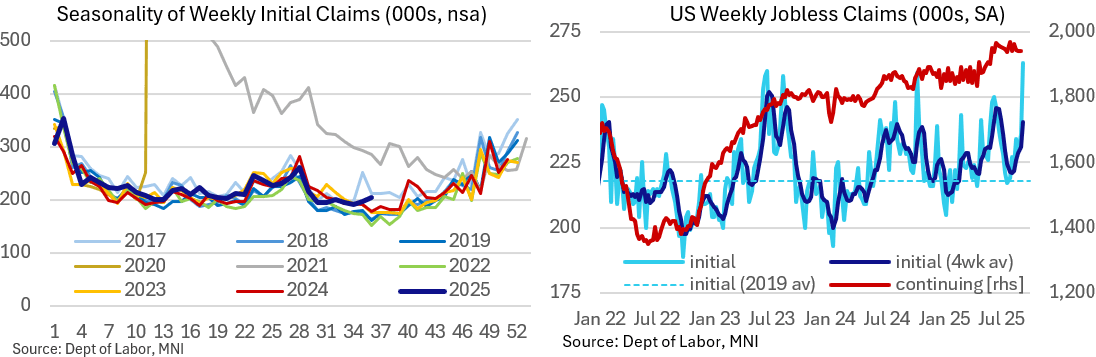

- MNI US DATA: Initial Claims Jump Led By Texas, But Continuing Stabilizing

US

MNI: Bullard Interviewed By Bessent For Fed Chair Job

Federal Reserve Bank of St. Louis President James Bullard told MNI he was interviewed for the position of Fed chair Wednesday, and made the case to Treasury Secretary Scott Bessent that his deep experience serving on the FOMC for 15 years has prepared him well to lead the central bank. "I emphasized that I might be the most experienced person of the people on the list," he said. "It was a good discussion."

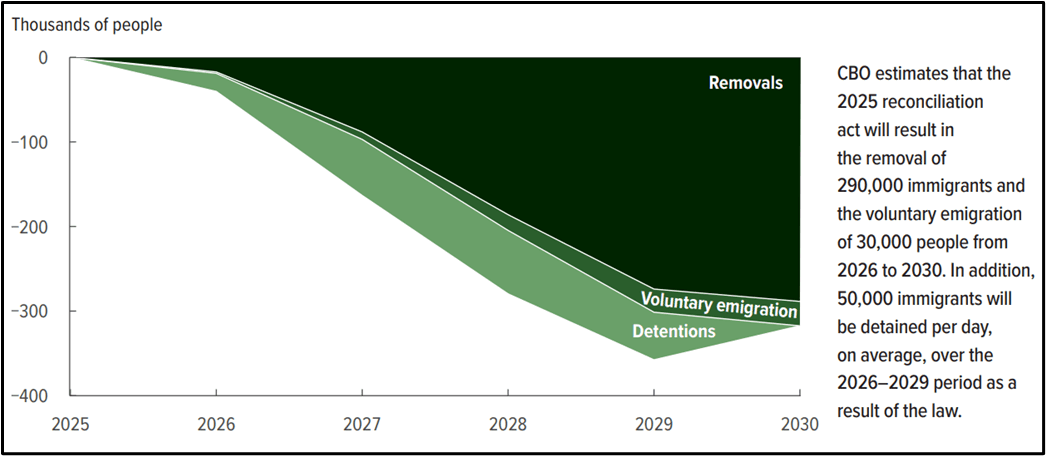

MNI US: 'Big Beautiful Bill' To Reduce US Population Growth - CBO

The Congressional Budget Office estimates in a new report that “as a result of the immigration enforcement provisions of the 2025 reconciliation act ['One Big Beautiful Bill'], the size of the population will decrease relative to CBO’s January 2025 population projections.”

- CBO estimates that altogether, “there will be 320,000 fewer people in the Social Security area population and 280,000 fewer people age 16 or older in the civilian noninstitutionalized population in 2035 than the agency previously estimated there would be.”

Figure 1: Estimated Effects of the 2025 Reconciliation Act on the Population

Source: CBO

NEWS

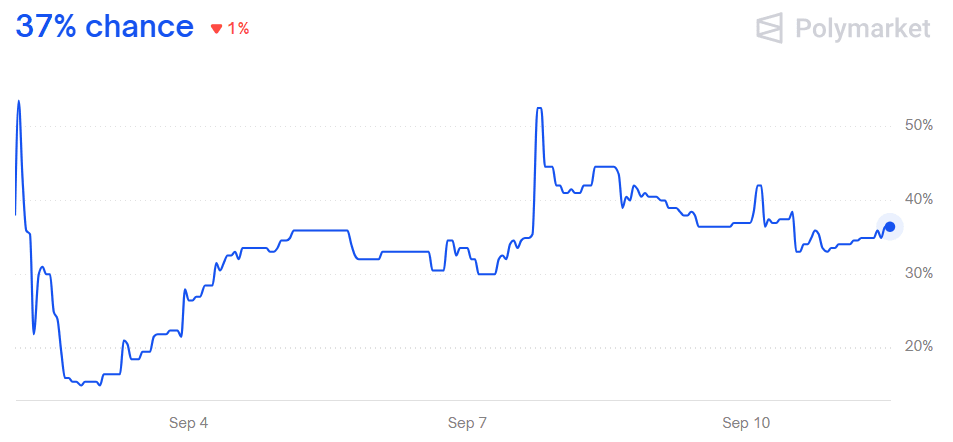

MNI US: Schumer Reiterates That Democrats Won't Accept 'Clean' Funding Extension

Senate Minority Leader Chuck Schumer (D-NY) told reporters yesterday that partisan Republican funding proposals to avert a government shutdown on October 1, “can’t get our votes.” Semafor notes, “Republicans have proposed several short-term funding options running from November to January, but Democrats want Republicans to negotiate with them, especially on extending expiring health care subsidies.”

Figure 1: Government Shutdown by October 1

Source: Polymarket

MNI BRIEF: ECB On Hold, Little Change in Inflation Outlook

The European Central Bank kept its three key interest rates unchanged on Thursday, with staff projections presenting a similar picture of inflation similar to June’s. The deposit facility, main refinancing operations and marginal lending facility remain unchanged at 2.00%, 2.15% and 2.40% respectively, as expected, with policy to be decided on a meeting-to-meeting and data-dependent basis.

- Inflation projections were slightly higher in the near-term and modestly lower over the medium term. Headline inflation is seen averaging 2.1% in 2025, 1.7% in 2026 and 1.9% in 2027. Inflation excluding energy and food is seen at 2.4% in 2025, 1.9% in 2026 and 1.8% in 2027.

MNI ECB WATCH: Lagarde Declares Disinflation Over

The European Central Bank as expected held interest rate for a second consecutive meeting at 2% on Thursday, with President Christine Lagarde saying that the disinflationary process is now over and that risks to economic growth are more balanced. “The disinflationary process is over. And I'm referring here to the causes for inflation that we have experienced in the last few quarters,” Lagarde told the post-meeting news conference, adding that the ECB continued to be in a good place with inflation where it wants it to be.

US TSYS

MNI US TSYS: Strong Dovish Data React Lifts Projected Rate Cut Pricing

- Treasuries look to finish higher Thursday, off early post-data highs on heavier two-way flow. Treasury futures extended lows briefly (TYZ5 113-09) before rebounding / gapping higher post data: slightly higher than expected August CPI MoM inflation, while weekly claims come out much higher than expected.

- Core goods prices accelerated to 0.28% M/M from 0.21% prior, a little shy of expectations of a rise to the low 0.30s. This slight "miss" appears down to used car prices on the soft side of expectations at 1.0% M/M, still a 7-month high but vs expectations of a little above that figure.

- Initial jobless claims surprisingly jumped to 263k (sa, cons 235k) in the week to Sep 6 after a slightly downward revised 236k (initial 237k). Note that in the NSA jobless claims details, national claims increased 7.9k on the week but 15.3k of that came from Texas. Continuing claims on the other hand surprised lower at 1939k (sa, cons 1950k).

- Currently, the Dec'25 10Y trades +4 at 113-22.5 (yld 4.00547% -.0401) vs. 113-29 high - through initial technical resistance at 113-21.5 (High Sep 5) and 113-26.5 (2.764 proj of the Jul 15 - 22 - 28 price swing). Next level round number resistance at 114-00.

- Projected rate cut pricing gained traction vs. morning/pre-data levels (*): Sep'25 at -27.2bp (-27.1bp), Oct'25 at -50.1bp (-46.4bp), Dec'25 at -73.2bp (-68bp), Jan'26 at -86.1bp (-80.4bp).

- Focus Friday shifts to the UK activity data, in which markets expect both industrial and manufacturing production to slow on a monthly and yearly basis - underscoring a slower level of monthly GDP growth into Q3. French and German inflation numbers are also due, but it's the prelim University of Michigan sentiment numbers that should prove more decisive.

OVERNIGHT DATA

MNI US DATA: Initial Claims Jump Led By Texas, But Continuing Stabilizing

Initial jobless claims surprisingly jumped to 263k (sa, cons 235k) in the week to Sep 6 after a slightly downward revised 236k (initial 237k). Note that in the NSA jobless claims details, national claims increased 7.9k on the week but 15.3k of that came from Texas. It clearly stands out compared to recent years (see chart) and thus could be an outlier, but of course it is a major state and so can’t easily be written off.

- There is no explanation in the BLS release, but one theory is that it is a a knock-on effect the heavy Texas flooding in July (albeit that was almost 2 months ago). Keeping that potential idiosyncratic Texas boost in mind, the four-week average pushed 10k higher to 241k for its highest since June.

- Continuing claims on the other hand surprised lower at 1939k (sa, cons 1950k) in the week to Aug 30 after a slightly downward revised 1939k (initial 1940k). Those are the joint-lowest continuing claims since the first week of June, and down from the July high of 1,946k.

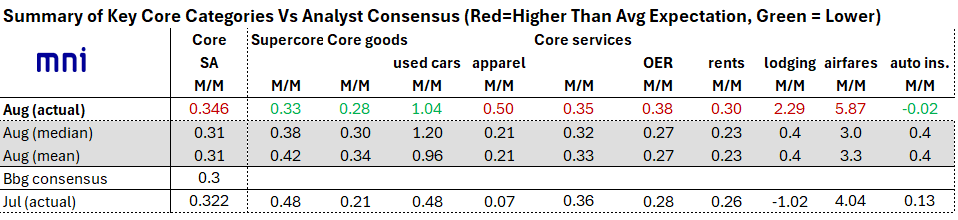

MNI US DATA: Core CPI Categories Mixed Vs Expectations, PCE Looks Benign

Core inflation categories were mixed in August vs expectations. Core goods prices accelerated to 0.28% M/M from 0.21% prior, a little shy of expectations of a rise to the low 0.30s. This slight "miss" appears down to used car prices on the soft side of expectations at 1.0% M/M, still a 7-month high but vs expectations of a little above that figure. New vehicle prices rose 0.3% (0.0% prior), likewise an 8-month high but some had seen higher.

MNI US DATA: Further Robust CPI Core Goods Details But No Additional Acceleration

Median core goods CPI inflation continued to track a little stronger than the published core goods series in August, albeit with its smallest overshoot since this median first accelerated strongly in May. With three of the past four months at 0.3% M/M plus June at 0.44% M/M, it continues to run at a strong monthly pace but of note when thinking about tariff passthrough lags, June has been the peak for monthly price increases for now. Core goods CPI inflation was reasonably close to analyst expectations in August at 0.28% M/M vs expectations for the low 0.30s, which the small ‘miss’ in part to a softer than expected 1.0% M/M increase in used car prices.

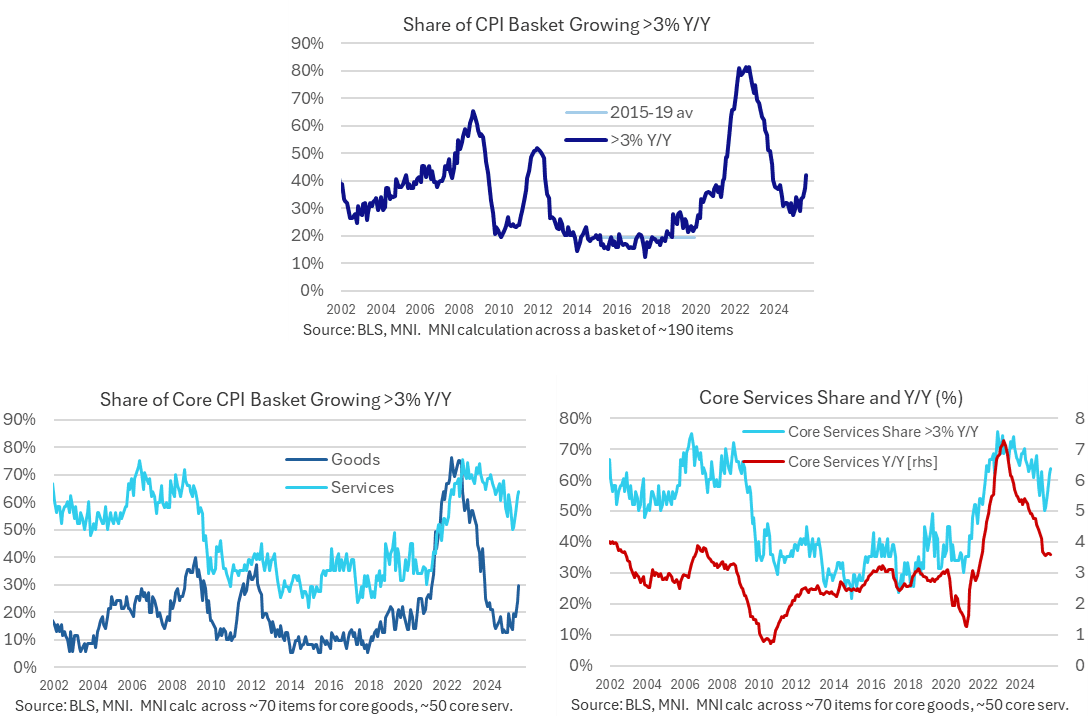

MNI US DATA: CPI Inflation Breadth Widened Further In August

Our calculations show a further widening in inflationary pressures in August, on a headline but also notably both core goods and core services basis. 42% of approximately 190 items across the entire CPI basket saw inflation in excess of 3% Y/Y in August, the highest share since Nov 2023.

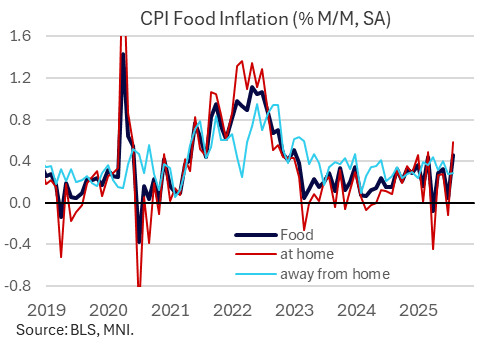

MNI US DATA: 3-Year High In Food-At-Home CPI Fuels Above-Expected Headline

August's headline CPI reading of 0.382% M/M unrounded (0.197% prior) exceeded median expectations of 0.34% M/M for easily the highest print since January. As noted previously, core CPI came in at a slightly-above consensus 0.346% unrounded (0.322% prior, 0.32% MNI unrounded median). The Y/Y prints were marginally above-expected at 2.92% for headline (2.70% prior) and 3.11% for core (3.06% prior), respectively 7-month and 6-month highs.

- The headline "beat" came in spite of a slightly cooler rise in energy CPI (0.7% vs around 0.8% expected, -1.1% prior). While motor fuel prices rose basically as expected (1.8% after -2.2%), electricity prices appeared to be on the moderate side (0.2% vs -0.1% prior, no consensus) with gas utility CPI falling 1.6% after a 0.9% fall in the previous month.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 615.68 points (1.35%) at 46108.48

S&P E-Mini Future up 55.25 points (0.84%) at 6595.5

Nasdaq up 164.2 points (0.8%) at 22051.7

US 10-Yr yield is down 3.1 bps at 4.0149%

US Dec 10-Yr futures are up 1/32 at 113-19.5

EURUSD up 0.0043 (0.37%) at 1.1737

USDJPY down 0.32 (-0.22%) at 147.15

WTI Crude Oil (front-month) down $1.41 (-2.21%) at $62.26

Gold is down $3.56 (-0.1%) at $3637.22

European bourses closing levels:

EuroStoxx 50 up 25.3 points (0.47%) at 5386.77

FTSE 100 up 72.19 points (0.78%) at 9297.58

German DAX up 70.7 points (0.3%) at 23703.65

French CAC 40 up 62.2 points (0.8%) at 7823.52

US TREASURY FUTURES CLOSE

3M10Y -2.044, -1.509 (L: -4.825 / H: 1.843)

2Y10Y -2.212, 47.939 (L: 46.96 / H: 52.112)

2Y30Y -3.795, 111.225 (L: 110.922 / H: 119.042)

5Y30Y -3.77, 105.949 (L: 105.949 / H: 113.789)

Current futures levels:

Dec 2-Yr futures down 0.25/32 at 104-13.25 (L: 104-10.5 / H: 104-17.375)

Dec 5-Yr futures down 1.5/32 at 109-27.5 (L: 109-22.5 / H: 110-04.75)

Dec 10-Yr futures up 0.5/32 at 113-19 (L: 113-09 / H: 113-29)

Dec 30-Yr futures up 7/32 at 117-29 (L: 117-05 / H: 118-06)

Dec Ultra futures up 15/32 at 121-22 (L: 120-16 / H: 121-30)

MNI US 10YR FUTURE TECHS: (Z5) Bull Cycle Remains In Play

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-26+ 2.764 proj of the Jul 15 - 22 - 28 price swing

- RES 1: 113-21+ High Sep 5

- PRICE: 113-15+ @ 11:24 BST Sep 15

- SUP 1: 112-28+/112-18 Low Sep 5 / 20-day EMA

- SUP 2: 111-30+ 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

Treasury futures are unchanged and the contract is holding on to the bulk of its latest gains. Recent impulsive gains highlight an acceleration of the uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. This paves the way for an extension through 113-21 next (pierced), the 2.618 projection of the Jul 15 - 22 - 28 price swing. Initial firm support to watch is 112-18, the 20-day EMA.

SOFR FUTURES CLOSE

Current White pack (Sep 25-Jun 26):

Sep 25 +0.010 at 95.985

Dec 25 +0.030 at 96.380

Mar 26 +0.020 at 96.615

Jun 26 +0.005 at 96.850

Red Pack (Sep 26-Jun 27) -0.025 to -0.015

Green Pack (Sep 27-Jun 28) -0.025 to -0.02

Blue Pack (Sep 28-Jun 29) -0.015 to -0.01

Gold Pack (Sep 29-Jun 30) -0.005 to +0.005

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (-0.01), volume: $2.800T

- Broad General Collateral Rate (BGCR): 4.37% (-0.01), volume: $1.145T

- Tri-Party General Collateral Rate (TCR): 4.37% (-0.01), volume: $1.118T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $111B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $209B

FED Reverse Repo Operation

RRP usage slips to $26.897B with 15 counterparties this afternoon from $29.400B Wednesday. Compares to $17.923B on Wednesday, Sep 3 - the lowest levels since early April 2021. This year's high usage of $460.731B occurred on June 30.

MNI PIPELINE: Corporate Bond Roundup: Sidelined Post-Data

- Corporate issuance looks rather subdued today, sidelined pre/post this morning's headline CPI inflation data.

- Date $MM Issuer (Priced *, Launch #)

- 09/11 $900M K Hovnanian $4.5B each: 5.5NC2.5 8%a, 8NC3 8.375%a

- 09/11 $725M CFE FIBRA 15Y +220

- 09/11 $575M #American Tower 5Y +95a, 10Y +105a

- 09/11 $1.5B Directv 8.875% 2030 Tap investor calls

- $12.5B Priced Wednesday, $57.45B/wk

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Underperform With ECB Seen Slightly Hawkish

European curves flattened Thursday.

- US CPI data came in on the slightly high side of expectations, but with relatively benign PCE inflation details combined with above-expected jobless claims released simultaneously, global core FI gained ground.

- The main event of the European session was the ECB meeting - MNI's review is here (PDF).

- In short, the bar to cuts was seen to have been raised a little: Lagarde's press conference sparked a hawkish reaction with growth risks deemed more balanced and the disinflationary process over.

- Later in the session, ECB sources from Bloomberg suggested further shocks are needed to see rate cuts. Reuters sources said the debate on a rate cut was not over just yet with October too soon but December eyed.

- On net, the German curve closed with twist flattening on the day as the short-end was notably weaker; Gilts easily outperformed, with bull flattening in the UK curve.

- Periphery/semi-core EGBs tightened amid the weakness in Bunds, with BTPs and OATs outperforming.

- UK activity data features first thing Friday, while multiple ECB speakers make appaearances (Rehn, Nagel, Kocher).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.4bps at 1.986%, 5-Yr is up 3.2bps at 2.257%, 10-Yr is up 0.5bps at 2.657%, and 30-Yr is down 1.8bps at 3.255%.

- UK: The 2-Yr yield is down 0.9bps at 3.931%, 5-Yr is down 1.2bps at 4.043%, 10-Yr is down 2.7bps at 4.606%, and 30-Yr is down 4.4bps at 5.438%.

- Italian BTP spread down 2bps at 79.5bps / French OAT down 2.1bps at 78.8bps

MNI FOREX: EUR/USD Surges on Soft US Jobs, Hesitant Lagarde

- The USD Index traded weaker into the Thursday close. While August CPI data came in alongside expectations, it was the particularly poor weekly jobless claims numbers that drove the price lower. The USD Index sales came across several phases through Thursday trade, with price action getting a further boost on the core equity rally.

- The e-mini S&P rallied alongside spot gold prices - both gaining as markets cemented expectations for outsized easing at the September FOMC meeting. OIS markets retain full pricing for a 25bps rate cut next week, with partial pricing still pointing to a decent chance of a 50bps move.

- EURUSD gained ground throughout the ECB press conference, breaking the Thursday highs at 1.1738 amid a hawkish-leaning Lagarde as well as the soft jobs data. Lagarde's key press conference signals include her statement that the risks to Eurozone economic growth have become "more balanced" (she previously had noted downside risks), as well as the phrase that "the disinflationary process in Europe is over". These underpinned a hawkish adjustment in EUR STIR.

- Focus Friday shifts to the UK activity data, in which markets expect both industrial and manufacturing production to slow on a monthly and yearly basis - underscoring a slower level of monthly GDP growth into Q3.

- French and German inflation numbers are also due, but it's the prelim University of Michigan sentiment numbers that should prove more decisive. Markets expect the one- and 5-10 year inflation expectation metrics to slow by 0.1 ppts apiece ahead of next week's FOMC decision.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 12/09/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 12/09/2025 | 0600/0700 | ** | Trade Balance | |

| 12/09/2025 | 0600/0700 | ** | Index of Services | |

| 12/09/2025 | 0600/0700 | ** | Index of Production | |

| 12/09/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 12/09/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 12/09/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 12/09/2025 | 0645/0845 | *** | HICP (f) | |

| 12/09/2025 | 0700/0900 | *** | HICP (f) | |

| 12/09/2025 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 12/09/2025 | 0900/1100 | Labour Market Quarterly Statistics | ||

| 12/09/2025 | - | *** | Money Supply | |

| 12/09/2025 | - | *** | New Loans | |

| 12/09/2025 | - | *** | Social Financing | |

| 12/09/2025 | 1230/0830 | * | Building Permits | |

| 12/09/2025 | 1400/1000 | * | Services Revenues | |

| 12/09/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 12/09/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 12/09/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 12/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |