US DATA: Core CPI Categories Mixed Vs Expectations, PCE Looks Benign

Sep-11 13:48

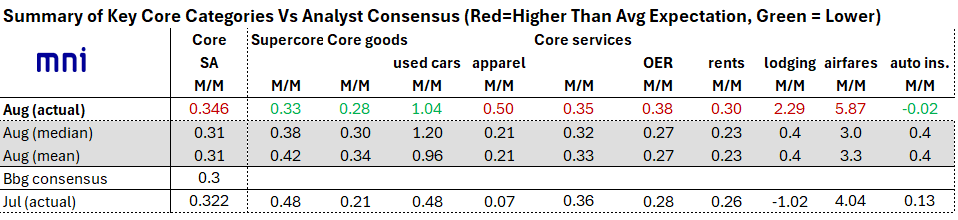

Core inflation categories were mixed in August vs expectations.

- Core goods prices accelerated to 0.28% M/M from 0.21% prior, a little shy of expectations of a rise to the low 0.30s. This slight "miss" appears down to used car prices on the soft side of expectations at 1.0% M/M, still a 7-month high but vs expectations of a little above that figure. New vehicle prices rose 0.3% (0.0% prior), likewise an 8-month high but some had seen higher.

- Additionally, medical care commodities were notably weak at -0.3% M/M (+0.1% prior). Conversely, there was some upside in tariff-related core goods categories including apparel (jumped to 0.5% from 0.1% and vs 0.2% expected). But overall core goods ex-used vehicle inflation was exactly the same in August (0.17% M/M) as in July, suggesting limited pressure on this front.

- In services, Supercore came in a little soft at 0.33% M/M vs closer to 0.40% expected (though again there was a wide range of estimates from 0.3-0.6%).

- Breaking that down, rents/OER were above expected at 0.30% and 0.38% respectively (prior: 0.26% / 0.28%). That's a 5-month high for OER and 4-month high for rents, both of which have accelerated since recent lows set in May. Lodging meanwhile rebounded way more than expected at 2.3% M/M (0.4% expected) after 5 consecutive monthly contractions.

- Ex-shelter services prices decelerated to 0.26% M/M from 0.54% prior for a 3-month low. One downside surprise of note here is medical care printed a 29-month low -0.14%. This had been expected to see downward payback after +0.79% in July was a 34-month high, but the reversal appears to have gone further than expected.

- PCE implications look benign. When we look at PCE-related categories that come from PPI and not CPI such as airfares (5.9% rise, around double the expected rate and vs 4.0% prior) and auto insurance (flat, vs +0.4% expected), those are probably on net a boost for core CPI vs expectations - so the PCE readthrough from these is a little softer than the core print would suggest. We would also point to dental services inflation which fell 0.7% M/M after +2.6%, marking the weakest month for this category since 2018 - this feeds into core PCE and looks likely to keep post-CPI estimates contained at or perhaps slightly below the core CPI reading.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Trump Says Considering Allowing a "Major Lawsuit" Against Powell to Proceed

Aug-12 13:46

Trump on Truth Social: "Jerome “Too Late” Powell must NOW lower the rate. Steve “Manouychin” really gave me a “beauty”when he pushed this loser. The damage he has done by always being Too Late is incalculable. Fortunately, the economy is sooo good that we’ve blown through Powell and the complacent Board. I am, though, considering allowing a major lawsuit against Powell to proceed because of the horrible, and grossly incompetent, job he has done in managing the construction of the Fed Buildings. Three Billion Dollars for a job that should have been a $50 Million Dollar fix up. Not good!"

US DATA: Core CPI Trends Running Below Stubborn Y/Y

Aug-12 13:39

- As the earlier unrounded figures showed, the core CPI Y/Y of 3.06% marginally beat consensus as it rounded up to 3.1% (cons 3.0) after 2.93% Y/Y, despite the M/M being exactly in line with the median unrounded analyst estimate we’d seen of 0.32% M/M.

- A reminder here that the Y/Y is calculated from NSA data whereas the M/M (and subsequent trend rates) is calculated from SA data.

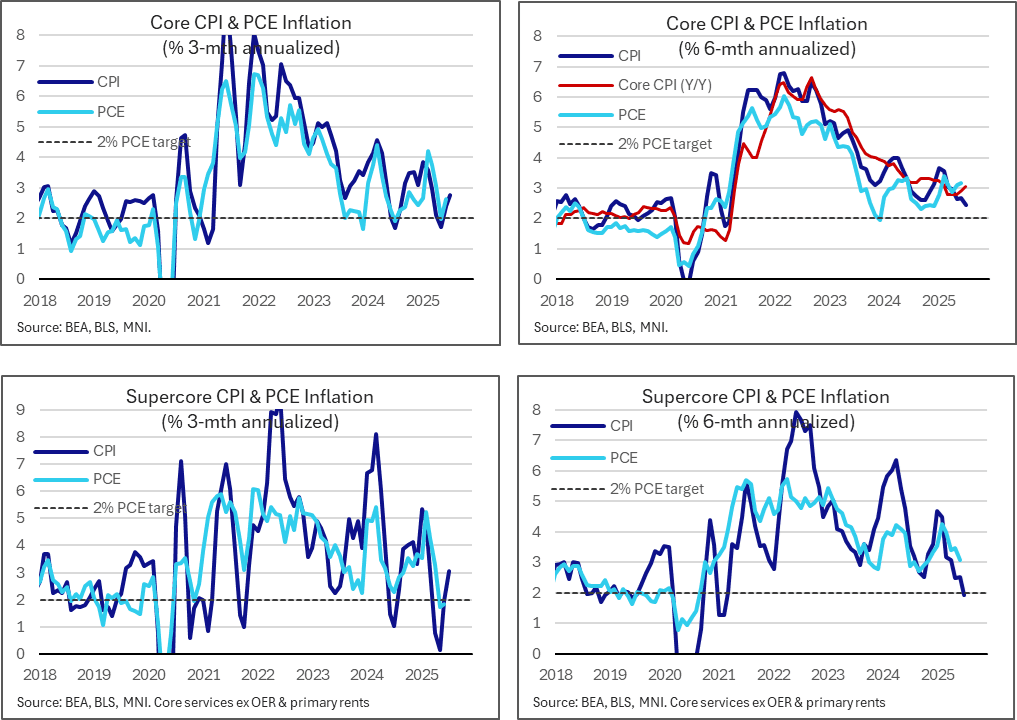

- That’s the fastest Y/Y since Feb 2025 although 3- and 6-mth run rates are softer, albeit moving in different directions.

- The 3-month accelerated from 2.4% to 2.8% annualized whilst the 6-month eased from 2.7% to 2.4% annualized.

- This pattern was echoed in the supercore, with the 3-month accelerating from 2.0% to 3.1% (driven by a strong 0.48% M/M in July) compared to the 6-month easing from 2.5% to 1.9% (on account of the booming 0.76% M/M in Jan dropping out).

- This is the softest 6-month supercore rate since Jan-Feb 2021 although needs to be treated with particular caution owing to larger differences with its PCE counterpart owing to greater reliance on PPI details.

- For instance, CPI airfares were a particular source of strength at 4.0% M/M but won’t feed into PCE and other important inputs for medical care services remain to be seen. As for items that do feed into PCE, there were somewhat offsetting large moves from booming dental services (2.6% M/M, 4.3% of supercore CPI) and further declines in lodging (-1.0% M/M, 6.4% of supercore).

BONDS: Binds are under heavy selling pressure

Aug-12 13:31

- Most Desks have not seen a clear driver for that latest push lower especially in German Govies, which has been led by the German long end, as previously mentioned the 30yr Yield has reached its highest level in 14yrs, since August 2011.

- Volumes did pick up, with 30k Bund sold in the past 56 minutes, and Immediate support for Bund is at 129.12, the August low

- The US Rally has also faded, TYU5 is back to pre CPI levels, with very heavy seeling going through.