US: Schumer Reiterates That Democrats Won't Accept 'Clean' Funding Extension

Sep-11 13:43

Senate Minority Leader Chuck Schumer (D-NY) told reporters yesterday that partisan Republican funding proposals to avert a government shutdown on October 1, “can’t get our votes.”

- Semafor notes, “Republicans have proposed several short-term funding options running from November to January, but Democrats want Republicans to negotiate with them, especially on extending expiring health care subsidies.”

- Schumer's comment suggests he is maintaining a hardline position that any short-term measure must be negotiated in a partisan manner, rather than a 'clean' extension proposed by Senate Majority Leader John Thune (R-SD) that would keep funding unchanged while the appropriations process continues.

- Senate Appropriations Chair Susan Collins (R-ME) said, “If that’s his position, then he’s calling for a government shutdown. I personally support an extension in some form of those [health care] tax credits. But that doesn’t really have anything to do with the need to keep [the] government funded.”

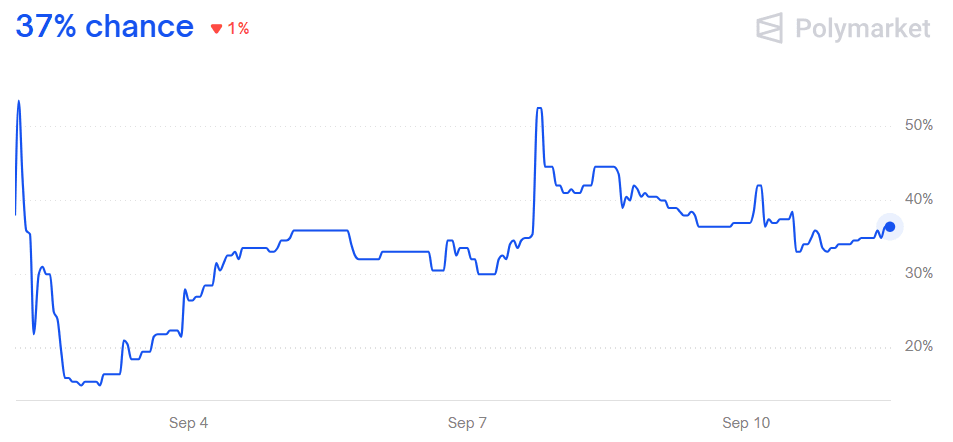

- Despite Schumer’s comments, the implied probability of a government shutdown is largely unchanged, according to data from Polymarket.

Figure 1: Government Shutdown by October 1

Source: Polymarket

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Core CPI Trends Running Below Stubborn Y/Y

Aug-12 13:39

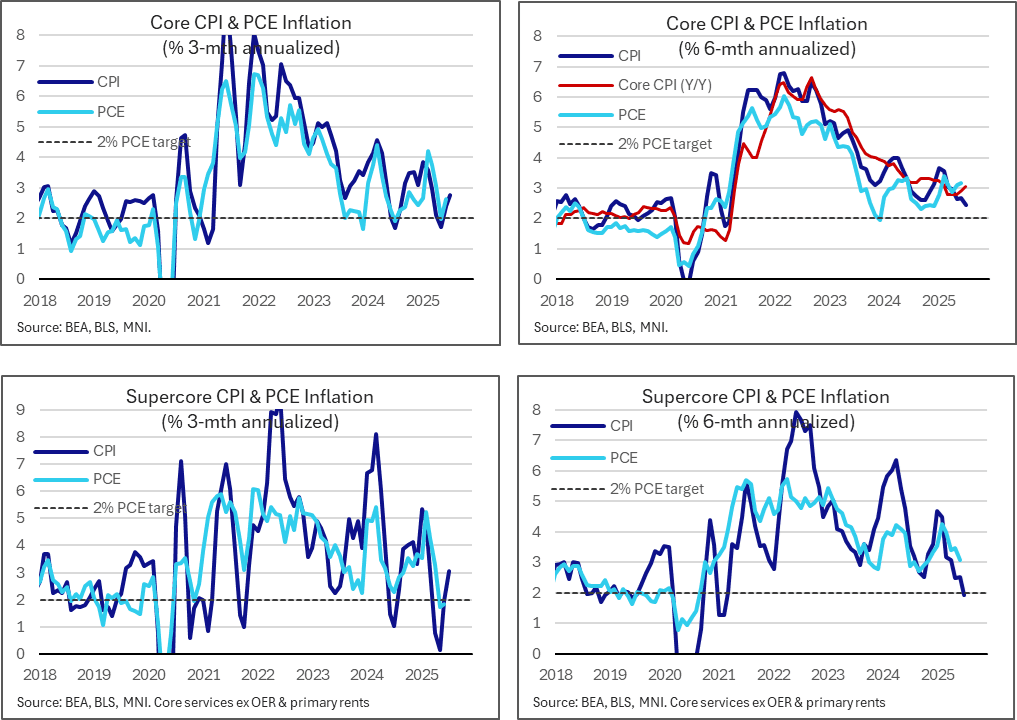

- As the earlier unrounded figures showed, the core CPI Y/Y of 3.06% marginally beat consensus as it rounded up to 3.1% (cons 3.0) after 2.93% Y/Y, despite the M/M being exactly in line with the median unrounded analyst estimate we’d seen of 0.32% M/M.

- A reminder here that the Y/Y is calculated from NSA data whereas the M/M (and subsequent trend rates) is calculated from SA data.

- That’s the fastest Y/Y since Feb 2025 although 3- and 6-mth run rates are softer, albeit moving in different directions.

- The 3-month accelerated from 2.4% to 2.8% annualized whilst the 6-month eased from 2.7% to 2.4% annualized.

- This pattern was echoed in the supercore, with the 3-month accelerating from 2.0% to 3.1% (driven by a strong 0.48% M/M in July) compared to the 6-month easing from 2.5% to 1.9% (on account of the booming 0.76% M/M in Jan dropping out).

- This is the softest 6-month supercore rate since Jan-Feb 2021 although needs to be treated with particular caution owing to larger differences with its PCE counterpart owing to greater reliance on PPI details.

- For instance, CPI airfares were a particular source of strength at 4.0% M/M but won’t feed into PCE and other important inputs for medical care services remain to be seen. As for items that do feed into PCE, there were somewhat offsetting large moves from booming dental services (2.6% M/M, 4.3% of supercore CPI) and further declines in lodging (-1.0% M/M, 6.4% of supercore).

BONDS: Binds are under heavy selling pressure

Aug-12 13:31

- Most Desks have not seen a clear driver for that latest push lower especially in German Govies, which has been led by the German long end, as previously mentioned the 30yr Yield has reached its highest level in 14yrs, since August 2011.

- Volumes did pick up, with 30k Bund sold in the past 56 minutes, and Immediate support for Bund is at 129.12, the August low

- The US Rally has also faded, TYU5 is back to pre CPI levels, with very heavy seeling going through.

BUNDS: German 30yr Yield highest in 14yrs

Aug-12 13:17

- German 30yr Buxl falls towards 115.00, helping push the Yield above the 2023 high of 3.263%, to reach its highest printed level since August 2011.

- The next big upside target would be situated at 3.30%, which today would equate to 114.37.