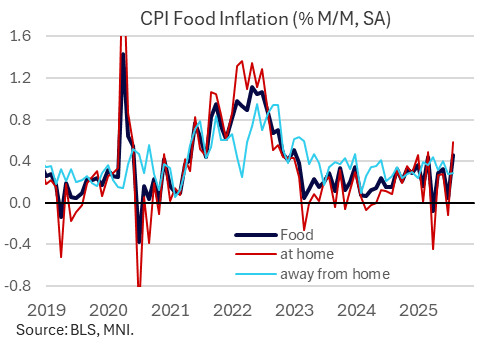

US DATA: 3-Year High In Food-At-Home CPI Fuels Above-Expected Headline

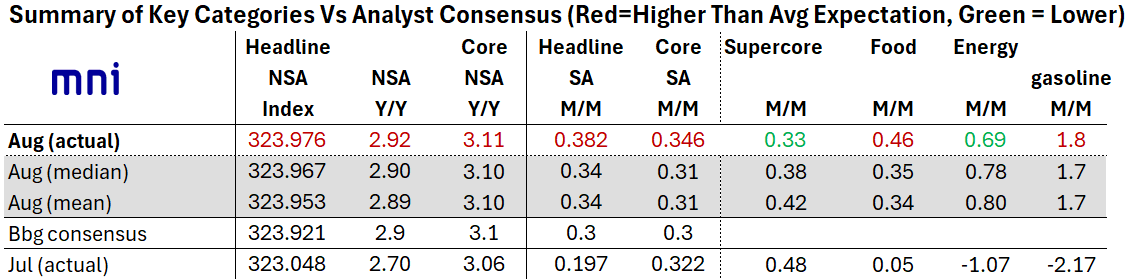

August's headline CPI reading of 0.382% M/M unrounded (0.197% prior) exceeded median expectations of 0.34% M/M for easily the highest print since January. As noted previously, core CPI came in at a slightly-above consensus 0.346% unrounded (0.322% prior, 0.32% MNI unrounded median).

- The Y/Y prints were marginally above-expected at 2.92% for headline (2.70% prior) and 3.11% for core (3.06% prior), respectively 7-month and 6-month highs.

- The headline "beat" came in spite of a slightly cooler rise in energy CPI (0.7% vs around 0.8% expected, -1.1% prior). While motor fuel prices rose basically as expected (1.8% after -2.2%), electricity prices appeared to be on the moderate side (0.2% vs -0.1% prior, no consensus) with gas utility CPI falling 1.6% after a 0.9% fall in the previous month.

- Food prices however were on the high side of expectations: the 0.46% M/M rise was a 31-month high, marking a sharp acceleration from under 0.1% prior and was about 0.1pp higher than the MNI median expectation.

- While food away from home continued to print solidly (0.3%, same as July), food at home jumped to 0.6% from -0.1% - the unrounded 0.58% rise was the biggest in 36 months.

- There was a noticeable pickup in the meats/poultry/fish/eggs (1.0% after 0.2%) and fruits and vegetables (1.6%, highest since early 2022 after 0.0%) categories, which combined make up 3% of the total CPI basket.

- Beef and veal prices are rising at some of their fastest rates in years (2.70% M/M), while tomato prices jumped 5.1% M/M, fastest since December 2017. We suspect there will be speculation that tariffs may be helping fuel the rise in these categories, either directly or indirectly.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Fed Gov Nominee Miran: No Tariff Inflation; Service Disinflation Imminent

Fed Governor nominee (and current CEA head) Miran on CNBC says he "just can't comment on current monetary policy at the moment" due to his impending Senate nomination. However he reiterates his view that there's little to no evidence of tariffs translating into stronger inflation, and he also makes the case that domestic services inflation will pull back "profoundly" due to reduced net immigration.

- "At the aggregate level, when you look holistically across the inflation data, there's just no evidence of [tariffs] whatsoever."

- "If you look at core... two of the strongest categories this month in terms of inflation were used cars and airfares. And neither of those have anything to do with tariffs. We don't import used cars from from abroad in large scale. And airfares are on domestic services... we've been doing a lot of thinking about just how much of this inflation is due to the illegal immigration that's occurred... Our calculations are that the massive in surge of renters into an only sluggishly adjusting housing supply probably boosted rents by about 4-5%. And that's a significant contribution to overall inflation at a time when the housing stock adjusts only slowly... we think that there's a very strong reason for thinking of very profound service disinflation coming up in the near future, as net migration has come to zero because the President's strong border policies."

- On the BLS jobs data, he says there's an element of "noise, uncertainty" that has "increased in recent years", including the birth-death model. "So this is a degradation in the quality of the statistics that has occurred. And I think the President is dead right when he says, we need to fix this. We need to make these statistics reliable. We need to make them believable. We need to make them credible. And I'm really delighted we're shaping up to be able to do."

- He says that re economic surveys, the BLS should consider "incentive schemes to drive response rates higher. I think that we can start thinking about ways to optimize the collection system, optimize the survey system, optimize the timing of responses. I think that we should be thinking critically about these questions."

BUNDS: German 10yr Yield is eyeing the July high

- This is the biggest single move in German Yields since the US NFP, the 10yr Yield could be set to test 2.769%, this was the July high, and highest printed level since late March.

Today reference 129.09:

- 2.769% = 128.88 (not far).

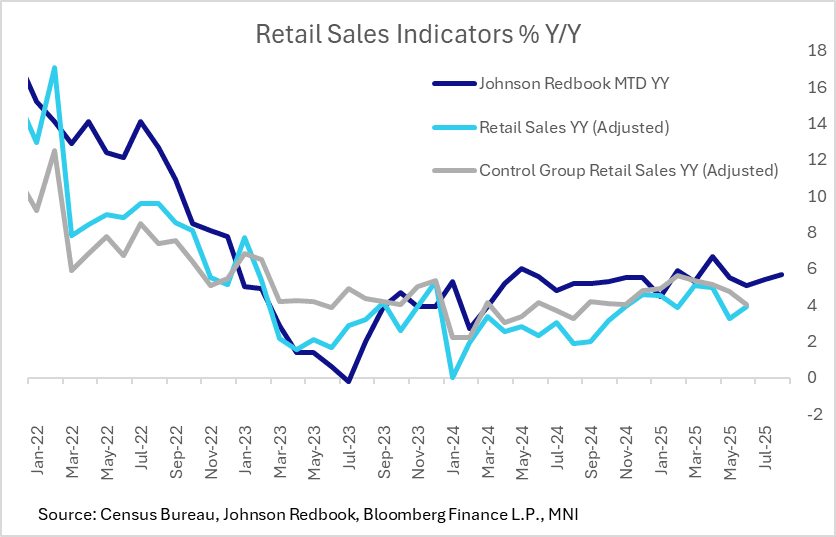

US DATA: Redbook Retail Sales Remain Solid, Sellers Eye Tariff Price Increases

Retail sales have maintained their solid growth pace through the summer, with the Johnson Redbook Retail Sales Index rising 5.7% Y/Y for the week ending Aug 9 (the first retail week of August). That's light vs a targeted 6.2% gain but still robust overall.

- The report notes in the anecdotal section that retailers are planning price increases due to tariffs: "August, much like July, is a transitional month marked by final summer clearance sales and a shift in inventories toward back-to-school merchandise and fall apparel. Sales have benefited from back-to-school sales tax holidays in several states, including Arkansas, Florida, Maryland, Massachusetts, Ohio, Oklahoma, South Carolina, Texas, Virginia, and West Virginia. As retailers begin to report their second-quarter earnings in the coming weeks, they are approaching the second half of the year with caution. They anticipate higher costs due to tariffs and are planning price increases to offset these adjustments. Currently, back-to-school sales have not yet made a significant impact, but this is expected to change as the month progresses."

- If sustained, a reading of 5.7% Y/Y would mean the fastest growth since April. While the Redbook index's growth has typically been higher than the "official" Census Bureau series, current levels would be consistent with Y/Y growth in the latter above 3.5%. We get the July report on Friday, with consensus for overall retail sales at 0.3% M/M (roughly 3.3-3.5% Y/Y).