MNI ASIA OPEN: Shutdown Set To Give Way To U.S. Data Deluge

MNI (NEW YORK) -

EXECUTIVE SUMMARY

- MNI BRIEF: Atlanta Fed President Bostic To Step Down In Feb

- MNI INTERVIEW: Fed Will Cut In Dec, More Next Year-Reinhart

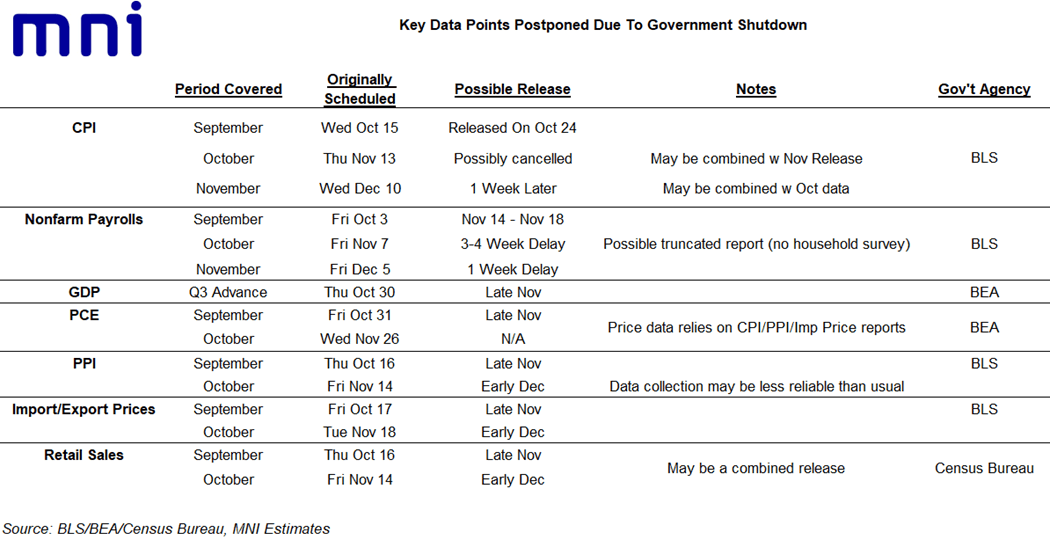

- October jobs data may never be released, White House says (Politico)

- MNI: Bank of Canada Discussed Delaying Oct Rate Cut- Minutes

- MNI INTERVIEW: Carney Job 1 Is Revive US Trade Talks-Foresters

MNI Estimates Of Possible Postponed U.S. Data Releases - Download Full Report Here

NEWS

MNI BRIEF: Atlanta Fed President Bostic To Step Down In Feb

Federal Reserve Bank of Atlanta President Raphael Bostic, the first African American and openly gay president of a regional Fed bank, said Wednesday he intends to retire on February 28, 2026 after nearly nine years in the post.

US Supreme Court to hear Trump's bid to fire Fed's Cook on January 21 (Reuters)

The U.S. Supreme Court announced on Wednesday that it will hear arguments on January 21 in President Donald Trump's attempt to remove Federal Reserve Governor Lisa Cook, a move without precedent that challenges the central bank's independence.

MNI INTERVIEW: Fed Will Cut In Dec, More Next Year-Reinhart

The Federal Reserve is likely to take out additional insurance against further labor market weakness by lowering interest rates again in December, and new leaders at the FOMC could cut borrowing costs more aggressively than the gradual easing likely to be depicted in the Summary of Economic Projections, former Fed Board division of monetary affairs chief Vincent Reinhart told MNI.

October jobs data may never be released, White House says (Politico)

White House Press Secretary Karoline Leavitt said Wednesday that the October jobs report and inflation data will likely not be released even after the government reopens. “Democrats may have permanently damaged the federal statistical system with October CPI and jobs reports likely never being released,” Leavitt told reporters. “All of that economic data released will be permanently impaired, leaving our policy makers at the [Federal Reserve] flying blind at a critical period.”

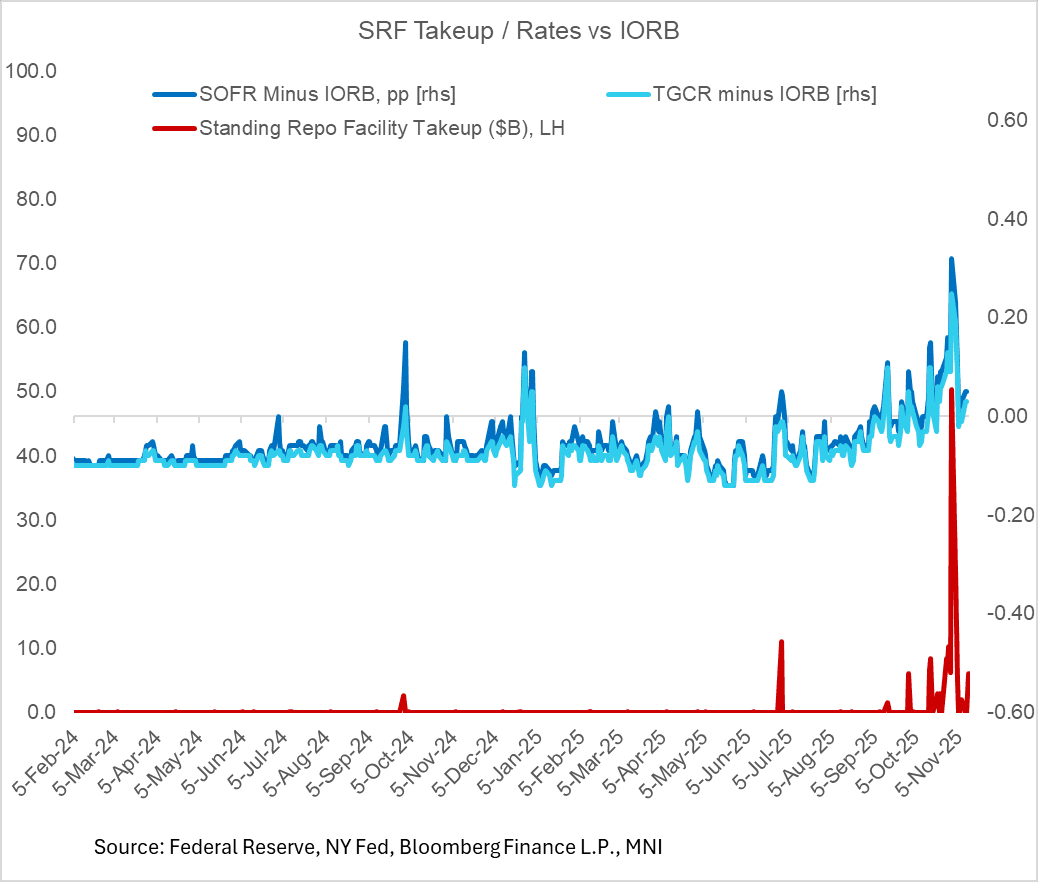

MNI BRIEF: Fed Repo Facility Will Cap Rate Pressures- Williams

The Federal Reserve standing repo facility will effectively cap temporary upward pressure on money market rates as long as primary dealers and banks use it, New York Fed President John Williams said Wednesday, also repeating the Fed is assessing market indicators to decide when to begin gradual expansion of its balance sheet. "The SRF’s effectiveness relies on market participants availing themselves of the SRF based on market conditions, free of worries about stigma or other impediments. I fully expect that the SRF will continue to be actively used in this way and contain upward pressures on money market rates."

MNI INTERVIEW: Carney Job 1 Is Revive US Trade Talks-Foresters

Prime Minister Mark Carney’s top priority must be restoring U.S. trade talks because relief in last week's budget won't come fast enough prevent more lost jobs and investment, Forest Products Association of Canada chief Derek Nighbor told MNI. “Mills are taking time off, reducing shifts, or shutting down temporarily. The sooner we get a deal that works for both Canada and the U.S., the better off both countries will be,” he said. “Until that happens, uncertainty in the marketplace will continue."

MNI: Bank of Canada Discussed Delaying Oct Rate Cut- Minutes

Bank of Canada officials discussed delaying cutting interest rates before agreeing to go ahead according to minutes of the Oct. 29 decision published Wednesday. "While members agreed that a cut to the policy interest rate would be needed, they had a range of views about the timing of the cut," according to the Summary of Deliberations.

MNI INTERVIEW: CNB Likely Done At 3.5% - Ex-Governor Singer

The Czech National Bank has likely reached its terminal rate with the two-week rate at 3.5%, former governor Miroslav Singer told MNI in an interview, but more expansionary fiscal policy under incoming Prime Minister Andrej Babis is unlikely to add significantly to inflation pressures and force a hike.

MNI BRIEF:ECB Warns Brussels On Synthetic Securitisation Scale

The ECB has warned the European Commission that the continued growth of "synthetic" securitisation deals poses financial stability risks and says that the EU's prudential rules should discourage such transactions.

MNI BRIEF: BOE Urges Ongoing Engagement With Gilt Repo Consult

The Bank of England's consultation on potential reforms to improve the resilience of the gilt repo market has stressed the risk of the unintended consequences of reforms aiming to maximise leverage and enhance market resilience, the Bank's Director of Financial Stability Strategy said on Wednesday.

MNI BRIEF: BCB Rates Restrictive Amid High Inflation-Galipolo

Central Bank of Brazil Governor Gabriel Galipolo said Wednesday it is clear why the board has to keep interest rates restrictive, as inflation has remained above the 3% target for 11 months and expectations are no longer anchored. “We’ve been outside the target for 11 months. Not in a single one of those months have we been within it. All projections indicate that inflation will remain above the target for a large part of my term,” Galipolo said at a press conference in São Paulo when asked about government criticism of the high interest rate policy.

US TSYS: Futures Flat, Cash Bull Flatter As Post-Shutdown Data Deluge Beckons

Cash Treasuries caught up with Tuesday's futures rally in the return to cash trade Wednesday, with TY futures hovering around the week's best levels.

- The curve bull flattened on the day, with Tuesday's poor weekly ADP data continuing to reverberate as we await "official" data following the conclusion of the government shutdown.

- The 10Y Note auction brought a tail (0.6bp) for a second consecutive month, but Treasuries were little moved in the aftermath. The Refunding week concludes with the 30Y auction Thursday.

- Atlanta Fed's Bostic announced his retirement at the end of his term in February 2026, and delivered a speech showing support for holding rates until there were clearer signs that inflation wasn't going to be a threat. NY's Williams repeated previous comments on Fed balance sheet policy, while Tsy Sec Bessent effectively recapped the conclusions from last week's Refunding announcement.

- Latest levels: The 2-Yr yield is down 2.7bps at 3.5638%, 5-Yr is down 4.5bps at 3.6682%, 10-Yr is down 4.9bps at 4.0674%, and 30-Yr is down 4.1bps at 4.6646%. Dec 10-Yr futures (TY) were down 1/32 at 113-00 (L: 112-27 / H: 113-2.5) - having tested key near-term resistance at 113-02, highs seen Nov 5, 7, and 11.

- Attention turns to the House vote expected at 7pm to end the government shutdown. White House's Leavitt said that it was likely October CPI and employment data would never be released - we go over prospects for those and other data releases here.

- With the expected return of government workers to their posts Thursday, we expect to soon get word on rescheduled data. However note that in 2013 we only got the BLS's updated release schedule at 4:30pm on the first day of reopening, so we won't be expecting an announcement on Thursday morning.

- However we are assured of getting some alternative data points Thursday including Chicago CARTS retail sales for October and the Dallas Fed's weekly economic index. We may also get the Department of Labor's official calculation of weekly jobless claims for the first time since the end of September, but either way we will be able to make our own estimates based on state-level data. We also hear from SF's Daly, Minneapolis's Kashkari, St Louis's Musalem and Cleveland's Hammack.

OVERNIGHT DATA

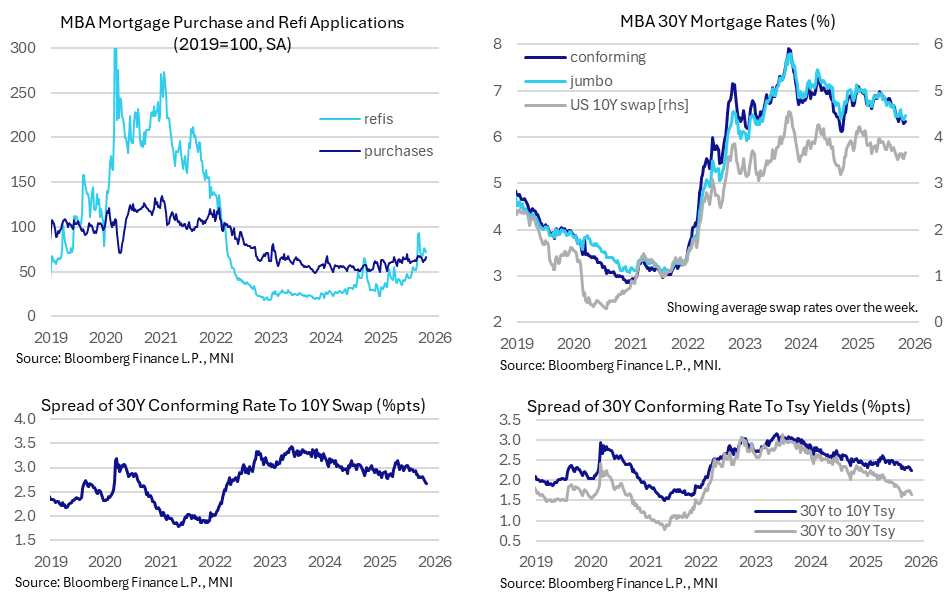

US DATA: Mortgage Rates Steady As Swap Spread Narrows Further

Mortgage applications were essentially unchanged last week even if it masked a strong uptick in new purchase applications. Mortgage rates have been steady in recent weeks, benefiting from a sizeable tightening in spreads to swap rates.

- MBA composite mortgage applications inched 0.6% higher last week (sa) after -1.9% and 7.1% in the previous two weeks.

- The details were a little more interesting than that suggests though, with new purchase applications increasing 5.8% (largest since early Sept and before that early June) compared to refi applications slipping -3.4%.

- Levels relative to 2019 average for context: composite 71%, new purchases 67%, refis 72%.

- The flatlining in overall activity came as the 30Y conforming rate ticked up 3bps to 6.34% after the 6.30% two weeks prior had been the lowest since Sep 2024.

- The relative stability in mortgages rates in the latest few weeks has come with a further tightening in spreads to swap rates.

- The 30Y mortgage rate to the average 10Y swap rate through the week fell further to 267bps, a fresh low since Apr 2022, compared to an average 285bp in Q1 and a rough range of 300 +/-5bp for some months after reciprocal tariff announcements in April prompted some additional caution in lending standards.

- This narrowing in spreads will be well received by the Trump administration.

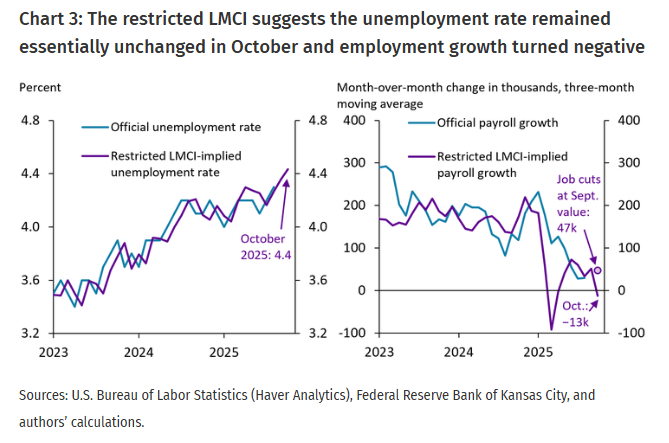

US DATA: KC Fed’s Alternative Labor Index Echoes Steady U/E Rate Increase

- Updated for October two days ago, we add the “Alternative Version” of the KC Fed’s Labor Market Conditions Index (LMCI) to the broad list of labor indicators we have focused on for labor market clues under the government shutdown. Atlanta Fed's Bostic today described it as one of his favorite gauges of the labor market.

- This Alternative Version, which excludes delayed government series, “suggests little change in the labor market, but a deceleration in labor market momentum caused by a high number of announced job cuts [in the Challenger report]. This has pushed down our model's forecast of payroll employment growth for October.”

- This restricted model points to an unemployment rate of 4.4% in October, broadly chiming with the 4.36% from the Chicago Fed’s unemployment rate nowcast for a very mild deterioration from the 4.32% reported in latest BLS data for August.

- It also sees the economy losing an average of 13k jobs per month from Aug-Oct, “driven entirely by the aforementioned announced job cuts in October”.

- We see a high likelihood of the delayed September payrolls report being released between Friday to early next week although the White House has called into question whether the October jobs report will be published.

- See the MNI US Shadow Employment Report here, noting that it was published prior to Tuesday’s slide in the weekly ADP series (see US DATA: Weekly ADP Series Rolls Over – Nov 11, 1016ET).

CANADA DATA: Building Permits Pick Up, But Still Negative For The Quarter

Building permits rose more quickly than anticipated in September at 4.5% M/M SA (0.9% expected), but this was largely offset by a downward revision to prior (-4.0%, vs -1.2%) in this volatile series.

- Residential permitting rose 4.8% to a 5-month high level, with non-residential up 4.0% rising for the first time in 5 months.

- However note these figures are in value and not volume terms, making the 11.2% Y/Y overall drop particularly poor. The real rise in September was 4.2% M/M. But for Q3 as a whole, the value of housing permits in constant terms fell to the lowest in series history back to 2018.

- For the 3rd quarter, permits fell 5.4% in nominal terms for a 2nd consecutive quarterly decline, with Ontario non-residential permitting driving the Q3 decrease (after jumping in Q2).

- Overall despite the September pickup, the softness in broader permits bodes for some softer readings ahead in housing starts and overall construction.

- The BOC's latest Monetary Policy Report notes "Residential investment is anticipated to grow modestly over the projection horizon. Housing starts are anticipated to remain elevated and grow modestly" though for business capex "Tariffs and trade policy uncertainty are expected to remain a significant headwind to investment into 2026."

US 10YR FUTURE TECHS: (Z5) Breaks Through Clustered Resistance

- RES 4: 114-02 High Oct 17 and the bull trigger

- RES 3: 113-29 High Oct 22

- RES 2: 113-18+ High Oct 28

- RES 1: 113-02+ High Nov 5& 7 and a key near-term resistance

- PRICE: 113-02 @ 17:27 GMT Nov 12

- SUP 1: 112-09+ Low Nov 5

- SUP 2: 112-09/06 100-dma / Low Sep 25 and a reversal trigger

- SUP 3: 112-03 Trendline support drawn from the May 22 low

- SUP 4: 111-23 50.0% retracement of the May 22 - Oct 17 bull leg

Prices rallied Wednesday, topping clustered resistance at 113-02 in the process. Clearance and a close above this mark is a bullish signal and will shift focus to the next notable resistance into 113-18+ and above. This cancels the S/T bear theme present at the beginning of the week, meaning markets need to challenge 112-06 to the downside, the Sep 25 low, and the 100-DMA, at 112-09 to weaken the outlook. Trendline support then undercuts at 112-03.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

US TSYS/OVERNIGHT REPO: Secured Rates Ticked Up Monday, Set To Stay Elevated

Secured rates ticked up on Monday Nov 10 (data was published this morning by the NY Fed which alongside rate markets was closed Tuesday due to the Veterans Day holiday).

- SOFR rose 2bp (3.95%) with TGCR up 4bp (3.93%), marking the highest both in absolute terms and relative to the Fed's administered rates (notably IORB which is 3.90%) since Nov 4 when October month-end pressures looked to have been dissipating.

- We also note that takeup of the Fed's Standing Repo Facility came in at $6.05B in this morning's operation, already the highest for a full day since Nov 3.

- Additionally, Treasury bill settlement will raise $14B in new cash today and $23B Thursday, applying some upside pressure to funding rates.

- As such it doesn't look like there will be much relief in rates today.

- Effective Fed funds were unchanged at 3.87% Monday.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 3.95%, 0.02%, $3135B

* Broad General Collateral Rate (BGCR): 3.93%, 0.04%, $1234B

* Tri-Party General Collateral Rate (TGCR): 3.93%, 0.04%, $1214B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 3.87%, no change, volume: $77B

* Daily Overnight Bank Funding Rate: 3.87%, no change, volume: $161B

OPTIONS: US Options Roundup - Nov 12 2025

Wednesday's US rates/bond options flow included:

- TYZ5 111.50 puts paper paid 0-02 on 4K

- TYF6 114c, bought for '27 in 28k (was bought in 100k Tuesday)

- adding to this: TYF6 114c, bought for '27 in 40k vs 112.28 (29del)

- SFRX5 96.18/96.31^^, traded half in 5k

- SFRX5 96.25/96.12ps, traded 1.75 in 2k

- SFRZ5 96.18/96.31/96.50/96.62c condor, traded for 6 in 5k

- SFRZ5 96.12/96.25/96.50/96.62c condor, traded for 6.75 in 6k

- SFRF6 96.37/96.18ps vs 0QF6 96.68p, bought the front for half in 2.5k (on screen).

- SFRF6 96.50/96.68/96.81c fly, bought for 3 in 15k (5k done on Block).

- SFRH6 96.37/96.25ps 1x2, traded half in 5k

- SFRM6 96.25/96.12/96.00p ladder, bought for flat in 2.5k.

- 0QX5 97.12/97.06/96.87/96.75p condor, traded 5 in 5k

- 0QU6 97.25/97.50cs, sold at 5.5 in 4k.

- 2QX5 96.75/96.68ps strip, bought for half in 4k

- 3QM6 96.87c, bought for 13.5 in 2k

BONDS: EGBs-GILTS CASH CLOSE: OATs Outperform On Political Progress

OATs outperformed the broader space Wednesday, with Gilts underperforming.

- EGBs and Gilts weakened on early trade. UK instruments led the broader sell-off after having outperformed Tuesday, suffering in part from rumours surrounding a potential leadership challenge in the ruling Labour Party. The high in yields was hit in late morning trade.

- But French Finance MInister Lescure's comments that he was "fairly confident" parliament would approve the contentious budget saw EGBs gain, and the national assembly's passing a suspension of the pension age rise, boosted perceptions of political stability and saw OATs extend outperformance.

- Weaker oil prices (an OPEC+ report showed price-negative supply-demand dynamics) also helped keep a lid on yields through the session.

- On the day, the German curve bull flattened, with Gilts bear steepening. Periphery spreads tightened alongside the OAT gains.

- Thursday's schedule includes UK Q3 / September GDP and monthly activity data, along with French labour market and Eurozone industrial production. In central bank communications, the BOE's Greene and ECB's Villeroy and Elderson make appearances, while we also get the ECB's latest Economic Bulletin release.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.3bps at 1.998%, 5-Yr is down 1.2bps at 2.247%, 10-Yr is down 1.5bps at 2.643%, and 30-Yr is down 2.6bps at 3.228%.

- UK: The 2-Yr yield is up 0.4bps at 3.728%, 5-Yr is up 1bps at 3.867%, 10-Yr is up 1.1bps at 4.398%, and 30-Yr is up 1.9bps at 5.191%.

- Italian BTP spread down 1.7bps at 72.8bps / French OAT down 2.8bps at 73.6bps

FOREX: Equity Weakness Halts USDJPY Momentum, EURGBP Highest Since May 2023

- The early part of the Wednesday session saw the greenback on the front foot, highlighted by the extension higher for USDJPY, which broke above 154.50 resistance and briefly printed a fresh 9-month high of 1.5504. The moves came despite additional verbal jawboning by Japanese officials, who remain vigilant to disorderly and speculative moves in the yen.

- However, it was the sensitivity to risk that turned the fortunes for USDJPY, as significant weakness for the major equity benchmarks following the US cash open (Nasdaq declined 1.3% from session highs) stalled the pair’s advance and prompted a move back towards 154.50 in late European trade.

- The trend structure in USDJPY remains bullish and this week’s gains reinforce current conditions. Sights are on 155.53 next, a Fibonacci projection.

- In similar vein, GBPUSD traded lower for most of the session, and briefly slipped back below the 1.3100 handle. However, a larger than usual collection of option expiries stalled the downside momentum and the late turnaround for the USD prompted cable to rise back to 1.3140. Sterling weakness has been more evident via EURGBP, with the cross rising to the strongest level since May 2023. Spot briefly pierced an old high, located at 0.8835.

- Once again, dips have remained very well supported around the prior breakout level at 0.8769, highlighting the dominant uptrend. The next topside target remains at 0.8875, the April 2023 high.

- The Swiss franc extended recent gains amid optimism on a looming trade deal with the US. Details of the deal remain sparse for now, with a "technical agreement" seemingly achieved according to NZZ. EURCHF currently stands just 35 pips from the key medium-term support of 0.9206, while USDCHF has consolidated back below the 0.8000 handle, falling 0.42% today.

- Australian employment data and the preliminary read of UK Q3 GDP highlight Thursday’s economic calendar.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 12/11/2025 | 2100/1600 | Boston Fed's Susan Collins | ||

| 13/11/2025 | 0030/1130 | *** | Labor Force Survey | |

| 13/11/2025 | 0700/0700 | *** | UK Monthly GDP | |

| 13/11/2025 | 0700/0800 | *** | Final Inflation Report | |

| 13/11/2025 | 0700/0700 | ** | Trade Balance | |

| 13/11/2025 | 0700/0700 | ** | Index of Services | |

| 13/11/2025 | 0700/0700 | ** | Index of Production | |

| 13/11/2025 | 0700/0700 | ** | Output in the Construction Industry | |

| 13/11/2025 | 0700/0700 | *** | GDP First Estimate | |

| 13/11/2025 | 0700/0800 | *** | Final Inflation Report | |

| 13/11/2025 | 0730/0730 | BOE MPG Minutes Released | ||

| 13/11/2025 | 0930/0930 | Productivity Flash Estimates | ||

| 13/11/2025 | 1000/1100 | ** | EZ Industrial Production | |

| 13/11/2025 | 1200/1200 | BOE Greene in Panel on Central Bank Independence | ||

| 13/11/2025 | - | *** | Money Supply | |

| 13/11/2025 | - | *** | New Loans | |

| 13/11/2025 | - | *** | Social Financing | |

| 13/11/2025 | - | ECB de Guindos at ECOFIN Meeting in Brussels | ||

| 13/11/2025 | 1300/1400 | ECB Elderson Moderates Climate and Banks Panel | ||

| 13/11/2025 | 1300/0800 | San Francisco Fed's Mary Daly | ||

| 13/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 13/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 13/11/2025 | 1330/0830 | *** | CPI | |

| 13/11/2025 | 1330/0830 | *** | CPI | |

| 13/11/2025 | 1330/0830 | *** | CPI | |

| 13/11/2025 | 1530/1030 | Minneapolis Fed's Neel Kashkari | ||

| 13/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 13/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 13/11/2025 | 1700/1200 | ** | DOE Weekly Crude Oil Stocks | |

| 13/11/2025 | 1700/1200 | ** | US DOE Petroleum Supply | |

| 13/11/2025 | 1715/1215 | St. Louis Fed's Alberto Musalem | ||

| 13/11/2025 | 1720/1220 | Cleveland Fed's Beth Hammack | ||

| 13/11/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 13/11/2025 | 1900/1400 | ** | Treasury Budget | |

| 14/11/2025 | 0001/0001 | KPMG/REC Report on Jobs | ||

| 14/11/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 14/11/2025 | 0200/1000 | *** | Retail Sales | |

| 14/11/2025 | 0200/1000 | *** | Industrial Output | |

| 14/11/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M |