FOREX: Equity Weakness Halts USDJPY Momentum, EURGBP Highest Since May 2023

- The early part of the Wednesday session saw the greenback on the front foot, highlighted by the extension higher for USDJPY, which broke above 154.50 resistance and briefly printed a fresh 9-month high of 1.5504. The moves came despite additional verbal jawboning by Japanese officials, who remain vigilant to disorderly and speculative moves in the yen.

- However, it was the sensitivity to risk that turned the fortunes for USDJPY, as significant weakness for the major equity benchmarks following the US cash open (Nasdaq declined 1.3% from session highs) stalled the pair’s advance and prompted a move back towards 154.50 in late European trade.

- The trend structure in USDJPY remains bullish and this week’s gains reinforce current conditions. Sights are on 155.53 next, a Fibonacci projection.

- In similar vein, GBPUSD traded lower for most of the session, and briefly slipped back below the 1.3100 handle. However, a larger than usual collection of option expiries stalled the downside momentum and the late turnaround for the USD prompted cable to rise back to 1.3140. Sterling weakness has been more evident via EURGBP, with the cross rising to the strongest level since May 2023. Spot briefly pierced an old high, located at 0.8835.

- Once again, dips have remained very well supported around the prior breakout level at 0.8769, highlighting the dominant uptrend. The next topside target remains at 0.8875, the April 2023 high.

- The Swiss franc extended recent gains amid optimism on a looming trade deal with the US. Details of the deal remain sparse for now, with a "technical agreement" seemingly achieved according to NZZ. EURCHF currently stands just 35 pips from the key medium-term support of 0.9206, while USDCHF has consolidated back below the 0.8000 handle, falling 0.42% today.

- Australian employment data and the preliminary read of UK Q3 GDP highlight Thursday’s economic calendar.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

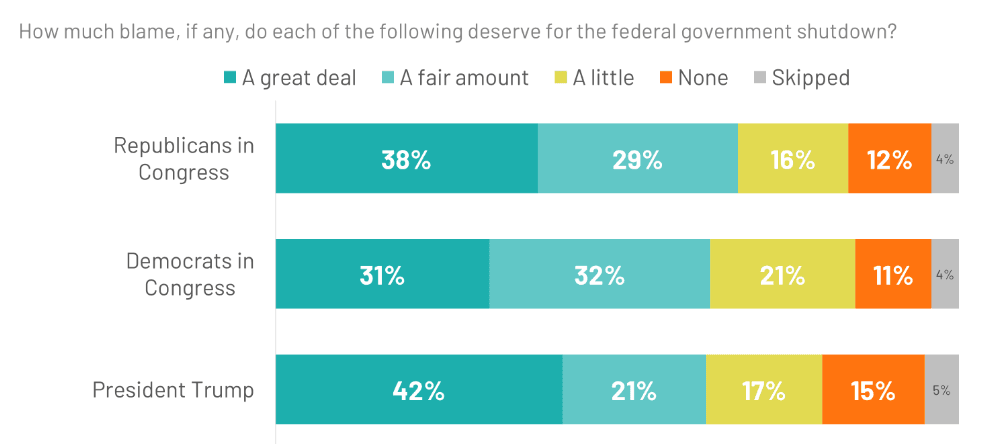

US: GOP/Trump Gets More Blame For Shutdown, Unclear If It Will Help Dems - Ipsos

New polling from Ipsos has suggested that the government shutdown might hurt Republicans and President Donald Trump more than it would hurt Democrats. However, "At the same time, there aren’t any glaring signs that it will help Democrats, who have been struggling with their own lack of popularity. Ultimately, while the fate of this shutdown is uncertain, one thing that seems likely is that this shutdown will only reinforce partisan entrenchment and disillusionment.”

- Ipsos notes, “A majority of Americans are at least somewhat concerned about the government shutdown, though it’s not very concerning to most… No side will leave this shutdown unscathed. Democrats in Congress, Republicans in Congress, and President Trump receive at least some blame in the eyes of the public.”

- Ipsos adds, “How hard do Americans want their side to fight? It depends. Half of America would prefer their leaders stand up for their issue positions at the cost of a shutdown. Independents would rather see a compromise. The most likely end result: more disillusionment.”

Figure 1: Who gets the blame for the government shutdown?

Source: Ipsos

FED: Philadelphia's Paulson: 2 More Cuts This Year, More Uncertainty Over 2026

In her first commentary on monetary policy since becoming Philadelphia Fed president in the summer, Anna Paulson (non-2025 FOMC voter, votes in 2026) said in a speech Monday that with rates " modestly restrictive now", she sees easing through year-end in line with the September SEP median - in other words, two more cuts by year-end. That's in line with MNI's assumption of her view.

- For 2026, when she is an FOMC voter, she sounds far less certain: "But first, what about next year? I see two important questions for monetary policy to grapple with in 2026. The first question is: What is the neutral policy rate? And the second question is: How quickly should policy move to neutral? My short answer to these questions is: I don’t know, and because I don’t know, we should proceed cautiously."

- Her current view on the economy: "The latest available data suggest an economy that is doing pretty well, although inflation remains elevated...Job gains have slowed markedly but labor supply and demand appear to be slowing more or less in tandem, leaving overall conditions in a rough balance...labor market risks do appear to be increasing — not outrageously, but noticeably. And momentum seems to be going in the wrong direction."

- She sees tariffs as largely having a one-off impact on inflation: "My base case is that tariffs will increase the price level, but they won’t leave a lasting imprint on inflation. And, given this base case, monetary policy should look through tariff effects on prices" though "I do still expect some additional goods inflation over the next few quarters, due in part to current tariffs working their way through and also to new tariffs that have been announced."

- Overall, "Given my views on tariffs and inflation, monetary policy should be focused on balancing risks to maximum employment and price stability which means moving policy towards a more neutral stance."

- And on neutral rates and the path ahead: "there are a wide range of plausible estimates of the neutral policy rate, and I think we will need to feel our way there, paying close attention to what economic developments tell us about the stance of policy. The ability to go slowly and assess is particularly valuable as we get closer to neutral. We will be better positioned to go slowly in the future if we adjust policy in the near term in a way that better aligns labor market and inflation risks. I anticipate that 2026 will see growth near potential, and inflation rising and then subsiding as tariffs, together with current and past monetary policy restrictiveness, work their way through. If the economy evolves as I expect, the monetary policy adjustments we make this year and next will be sufficient to keep labor market conditions close to full employment."

EURUSD TECHS: Corrective Bear Leg Intact

- RES 4: 1.1919 High Sep 17 and a bull trigger

- RES 3: 1.1820 High Sep 23

- RES 2: 1.1779 High Oct 1 and a key short-term resistance

- RES 1: 1.1692 20-day EMA

- PRICE: 1.1564 @ 15:47 BST Oct 13

- SUP 1: 1.1542 Low Oct 9

- SUP 2: 1.1516 76.4% retracement of the Aug 1 - Sep 17 bull leg

- SUP 3: 1.1392 Low Aug 1 and bear trigger

- SUP 4: 1.1313 Low May 30

EURUSD is trading closer to its recent lows. A short-term corrective bear cycle remains intact. Last week’s sell-off resulted in a breach of the 50-day EMA and support at 1.1646, the Sep 25 low, exposing 1.1516, a Fibonacci retracement. Note that MA studies are in a bull-mode position. This continues to highlight a dominant medium-term uptrend. Initial firm resistance is 1.1779, the Oct 1 high. A break of this level would signal a bull reversal.