MNI ASIA OPEN: Oct FOMC Minutes: Tepid Support Dec Rate Cut

EXECUTIVE SUMMARY

- MNI FED: FOMC Minutes Show Tepid-At-Best Support For December Cut

- MNI US DATA: Fed Should Have Q3 GDP And September PCE Estimates By Its Dec Meeting

- MNI US DATA: Fed Still Unlikely To Have November CPI, Payrolls By Dec Decision Time

- MNI US DATA: China And EU Leading Largest Adjustments In Trade With US

- MNI US DATA: Business Inflation Expectations Ease Further

US

MNI FED: FOMC Minutes Show Tepid-At-Best Support For December Cut

The biggest anticipated focus in the October FOMC meeting minutes (link) was on the degree to which support for a December cut was signaled. In short, the minutes suggest that it may only be a minority of the Committee that is pushing for a follow-up cut.

- That's largely in line with MNI's view that a majority of the broader Committee may be leaning to a December hold based on post-October FOMC commentary, though it doesn't necessarily mean that would-be cutters in December make up a majority of the 12-member voting contingent. (Below is a crib sheet on what "many" vs "several" means in the FOMC minutes - especially useful in this edition - from a guide published by the Fed Board staff).

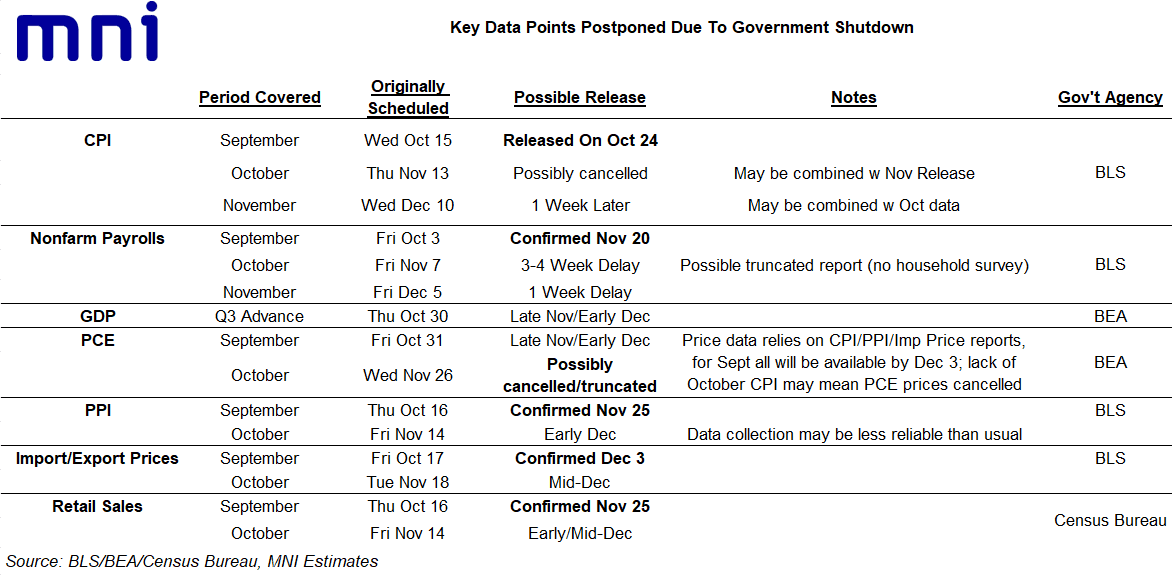

MNI US DATA: Fed Should Have Q3 GDP And September PCE Estimates By Its Dec Meeting

What's notable about the majority of post-shutdown rescheduled economic releases so far is that they are essential to compiling advance Q3 GDP and September PCE, both of which were originally due to be published by the Bureau of Economic Analysis at the end of October.

- That leaves it narrowly possible that we get an advance Q3 GDP release by the end of the month (ie Nov 28) depending on whether the BEA has time to compile and is willing to base their estimate on partial data to a greater degree than is usual, and whether the Thanksgiving holiday on Nov 27 forces a delay into the following week. Certainly we are now confident that the FOMC will have a Q3 GDP estimate and September PCE data in hand by the time of its Dec 9-10 meeting.

MNI US DATA: Fed Still Unlikely To Have November CPI, Payrolls By Dec Decision Time

In our latest MNI FedSpeak podcast we discussed the outlook for economic data releases as the Federal Reserve's December decision looms - we also opined on what the meeting decision and messaging might be. To hear the full episode (recorded Tuesday), click here.

- We update our key data points schedule below. Our FAQ on rescheduled data (Nov 11) remains largely intact, though releases are coming out a little more slowly than we had anticipated, by a few days to about a week - here

- Also see MNI's Data Methodology Cheat Sheet (Nov 13 - including methodologies underlying data releases) - here

NEWS

MNI US: Texas Redistricting And Inflation Concerns Dampen Midterm Outlook For GOP

President Donald Trump’s efforts to gain an edge in the 2026 midterms by redrawing Congressional maps in red states took another hit yesterday, with a federal court in Texas blocking a Republican map due to evidence it is "racially gerrymandered."

US TSYS

MNI US TSYS: Update Post-FOMC Minutes React: Extending Lows

- Treasuries mildly extended session lows in the last few minutes, now drawing some modest buying as participants continue to digest the October FOMC minutes discourse.

- While opinions "differed strongly", the minutes suggest that it may only be a minority of the Committee that is pushing for a follow-up cut.

- Currently, the Dec'25 10Y contract trades -1.5 at 112-23.5 after slipping to 112-22.5 low. Attention is on 112-10+, the 100-DMA and 112-06, the Sep 25 low. Trendline support also lies at 112-06+.

- Curves have unwound this week's steepening, 2s10s -.733 at 53.148, 5s30s -.431 at 104.291.

- Projected rate cut pricing has receded from this morning's levels (*): Dec'25 steady at -12bp, Jan'26 at -21.6bp (-22.1bp), Mar'26 at -32.6bp (-33.4bp), Apr'26 at -40.1bp (-41.1bp).

- Cross asset comparison: Bbg US$ continues to climb: BBDXY +6.33 at 1225.76; stocks generally mixed with SPX eminis +13 at 6653.00 while the DJIA trades down 56.92 points (-0.12%) at 45946.4. Crude weaker: WTI -1.31 at 59.43.

OVERNIGHT DATA

MNI US DATA: Business Inflation Expectations Ease Further

Business unit cost inflation expectations ebbed lower in the Atlanta Fed’s November survey, hitting it lowest since December, whilst realized own price setting reported its lowest for a quarterly question that started in late 2020. The Atlanta Fed’s Business Inflation Expectations survey saw a small dip in year-ahead expectations for unit costs from 2.27% to 2.18% in November.

MNI US DATA: Census Bureau Rescheduled Data Includes Sept Retail Sales For Next Week

We have more updates from the Census Bureau on upcoming data releases:

- August Wholesale Sales And Inventories Nov 21 1000ET (originally due out Oct 9)

- September Advance Retail Sales Nov 25 0830ET (originally due out Oct 16)

- August Manufacturing Inventories And Sales Nov 25 1000ET (originally due out Oct 16)

- September Advance Durable Goods Nov 26 0830ET (originally due out Oct 29)

- This is in line with MNI's expectation that September retail sales would be out by late November.

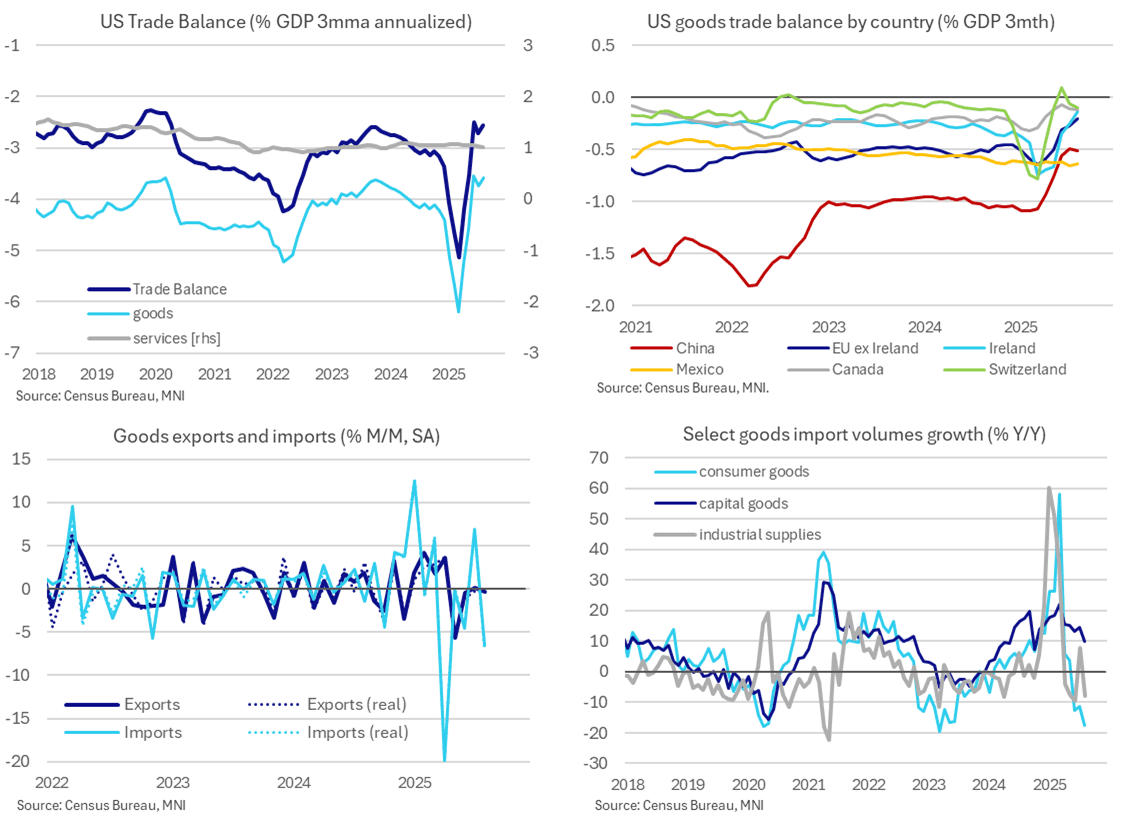

MNI US DATA: China And EU Leading Largest Adjustments In Trade With US

- The goods & services trade deficit was close to expectations in August at $59.6bn (cons $60.4bn) after a marginally revised $78.2bn in July. This is the full August release that was delayed by the government shutdown, after the initial advance covering just goods trade had been reported on Sep 25.

MNI US DATA: Mortgage Applications Reverse Refi Uptick

Mortgage applications last week fully unwound what had been a strong refi-driven increase seen back in late October when rates fell to their lowest in over a year. Rates have only increased modestly in recent weeks whilst mortgage swap spreads have seen a narrowing trend barring a small widening in the latest week.

- MBA composite applications fell a seasonally adjusted -5.2% last week, now fully unwinding a strong increase in late October with its largest single week decline since September.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 31.58 points (0.07%) at 46133.05

S&P E-Mini Future up 26.25 points (0.4%) at 6667.5

Nasdaq up 157.2 points (0.7%) at 22594.52

US 10-Yr yield is up 1.8 bps at 4.1309%

US Dec 10-Yr futures are down 3.5/32 at 112-21.5

EURUSD down 0.0054 (-0.47%) at 1.1528

USDJPY up 1.47 (0.95%) at 156.97

WTI Crude Oil (front-month) down $1.3 (-2.14%) at $59.44

Gold is up $12.59 (0.31%) at $4079.98

European bourses closing levels:

EuroStoxx 50 up 7.34 points (0.13%) at 5542.05

FTSE 100 down 44.89 points (-0.47%) at 9507.41

German DAX down 17.61 points (-0.08%) at 23162.92

French CAC 40 down 14.16 points (-0.18%) at 7953.77

US TREASURY FUTURES CLOSE

3M10Y -0.282, 24.847 (L: 22.331 / H: 26.203)

2Y10Y -0.362, 53.519 (L: 52.649 / H: 55.053)

2Y30Y -0.315, 115.507 (L: 114.777 / H: 117.386)

5Y30Y -0.481, 104.241 (L: 103.891 / H: 105.52)

Current futures levels:

Dec 2-Yr futures down 1/32 at 104-3.625 (L: 104-03.375 / H: 104-06.125)

Dec 5-Yr futures down 2.25/32 at 109-7.25 (L: 109-06.75 / H: 109-13.25)

Dec 10-Yr futures down 3.5/32 at 112-21.5 (L: 112-21 / H: 112-30.5)

Dec 30-Yr futures down 4/32 at 116-19 (L: 116-17 / H: 117-02)

Dec Ultra futures down 6/32 at 119-24 (L: 119-22 / H: 120-11)

MNI US 10YR FUTURE TECHS: (Z5) Resistance Remains Intact

- RES 4: 114-02 High Oct 17 and the bull trigger

- RES 3: 113-29 High Oct 22

- RES 2: 113-18+ High Oct 28

- RES 1: 113-04+ High Nov 14

- PRICE: 112-27+ @ 1100 ET Nov 19

- SUP 1: 112-10/06+ 100-dma / Trendline drawn from the May 22 low

- SUP 2: 112-06 Low Sep 25 /

- SUP 3: 111-31 Low Sep 2

- SUP 4: 111-23 50.0% retracement of the May 22 - Oct 17 bull leg

Resistance at the 113-02 level in Treasuries, an area of congestion since Nov 5, remains intact. A clear breach of this hurdle would be a bullish signal and suggest scope for a climb towards 113-18+, the Oct 28 high. A breach would also cancel a short-term bearish theme. For bears, attention is on 112-10+, the 100-DMA and 112-06, the Sep 25 low. Trendline support also lies at 112-06+.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 -0.023 at 96.168

Mar 26 -0.020 at 96.390

Jun 26 -0.020 at 96.640

Sep 26 -0.015 at 96.815

Red Pack (Dec 26-Sep 27) -0.01 to -0.005

Green Pack (Dec 27-Sep 28) -0.015 to -0.005

Blue Pack (Dec 28-Sep 29) -0.015 to -0.01

Gold Pack (Dec 29-Sep 30) -0.015 to -0.005

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.94% (-0.06), volume: $3.220T

- Broad General Collateral Rate (BGCR): 3.90% (-0.06), volume: $1.278T

- Tri-Party General Collateral Rate (TCR): 3.90% (-0.06), volume: $1.256T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.88% (+0.00), volume: $78B

- Daily Overnight Bank Funding Rate: 3.88% (+0.00), volume: $164B

FED Reverse Repo Operation

RRP usage inches up to $1.129B with 8 counterparties this afternoon from yesterday's $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: $6.35B to Price Wednesday

- Date $MM Issuer (Priced *, Launch #)

- 11/19 $2B #Baxter $300M 3Y +90, $700M 5Y +125, $1B 10Y +155

- 11/19 $1.1B #Bangkok Bank $500M 5Y +82, $600M 10Y +97

- 11/19 $1B #EOG Resources $750M +5Y +73, $250M 30Y tap +105

- 11/19 $500M #VSP Optical WNG 10Y +135

- 11/19 $500M #Element Fleet 5Y +95

- 11/19 $750M #SMBC Aviation 10Y +115

- 11/19 $500M #FIBRA Prologis WNG 10Y +145

- 11/19 $Benchmark First Abu Dhabi Bank (FAB) investor calls

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform Again Despite Soft UK CPI

Gilts underperformed for a second consecutive session Wednesday.

- The short end outperformed on the UK curve as October CPI data on the soft side (headline, services, food inflation below BOE forecasts) appeared to open the door to a December BOE cut slightly wider.

- Gilts initially rallied though global dynamics and local fiscal/political concerns weighed and there was clear underperformance further down the curve. 10Y Gilt yields hit the highest levels in a month.

- A revived bid in equities about 2 hours before the European cash close saw core FI pull back, reversing nascent gains for Bunds.

- On the day the UK curve bear steepened, with Germany's twist steepening. Periphery/semi-core EGB spreads closed slightly tighter.

- Thursday's global focus will be the delayed US September nonfarm payrolls report, though we get varied European data as well including German PPI and Eurozone and UK (GfK) consumer confidence. We also get appearances by BOE's Mann and Dhingra.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.1bps at 2.018%, 5-Yr is up 0.1bps at 2.294%, 10-Yr is up 0.5bps at 2.711%, and 30-Yr is up 1.3bps at 3.332%.

- UK: The 2-Yr yield is up 0.6bps at 3.806%, 5-Yr is up 2.8bps at 4.001%, 10-Yr is up 4.8bps at 4.602%, and 30-Yr is up 6.2bps at 5.448%.

- Italian BTP spread down 0.9bps at 74.2bps / French OAT down 0.5bps at 75bps

MNI FOREX: USD Index Rally Extends, Narrows Gap to Recovery Highs

- The ongoing concerns related to AI valuations and the associated shaky risk sentiment continue to provide a safe haven bid for the greenback, with the USD index significantly extending higher on Wednesday. Gains have been exacerbated in late trade by the confirmation that the Fed will not receive any additional jobs reports before the December meeting.

- On data fog grounds, front-end rates now price a smaller chance of a December cut (around 9bps), cementing the bullish intra-day theme for the greenback. Overall, the short-term DXY uptrend remains intact, having been well supported by the 50-day EMA since early October. The index has notably risen back above the 100 mark, and hovers within 30 pips of the recovery highs at 100.36. A break above 100.48 (May 29 high) would be a broader bullish development for the dollar.

- The consistent declines for the likes of AUD and NZD today highlight a pessimistic backdrop as market participants await the release of Nvidia earnings after the close tonight. NZDUSD continues to exhibit clear underperformance, with the pair falling over 1% and trading below 0.5600, the lowest level for the pair since April. Support appears scant until the year’s lows at 0.5486.

- Importantly, dollar gains today have been broad based, with the advances of USDJPY (+0.85%) and USDCHF (0.70%) reflective of this dynamic. USDJPY has now surpassed meaningful resistance at 156.75, the Jan 23 high.

- The Japanese yen has been proving immune to the recent equity weakness and the more forceful verbal FX warnings from Japanese officials. Furthermore, the ongoing tensions between Japan/China, disappointing Q3 GDP data and fiscal related uncertainty continue to provide a pessimistic domestic backdrop.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 20/11/2025 | 0700/0800 | ** | PPI | |

| 20/11/2025 | 1000/1100 | ** | EZ Construction Output | |

| 20/11/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 20/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 20/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 20/11/2025 | 1330/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/11/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1345/0845 | Cleveland Fed's Beth Hammack | ||

| 20/11/2025 | 1430/0930 | Fed Governor Michael Barr | ||

| 20/11/2025 | 1500/1000 | *** | NAR existing home sales | |

| 20/11/2025 | 1500/1000 | * | Services Revenues | |

| 20/11/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 20/11/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 20/11/2025 | 1600/1100 | Fed Governor Lisa Cook | ||

| 20/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 20/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 20/11/2025 | 1740/1240 | Chicago Fed's Austan Goolsbee | ||

| 20/11/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 20/11/2025 | 1830/1830 | BOE Dhingra Speech on Trade and Tariffs | ||

| 20/11/2025 | 2100/2100 | BOE Mann at IMF Statistical Forum | ||

| 21/11/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 20/11/2025 | 2315/1815 | Fed Governor Stephen Miran | ||

| 21/11/2025 | 2330/0830 | *** | CPI | |

| 20/11/2025 | 2345/1845 | Philly Fed's Anna Paulson | ||

| 21/11/2025 | 0001/0001 | ** | Gfk Monthly Consumer Confidence | |

| 21/11/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI |