US TSYS: Update Post-FOMC Minutes React: Extending Lows

Nov-19 19:57

- Treasuries mildly extended session lows in the last few minutes, now drawing some modest buying as participants continue to digest the October FOMC minutes discourse.

- While opinions "differed strongly", the minutes suggest that it may only be a minority of the Committee that is pushing for a follow-up cut.

- Currently, the Dec'25 10Y contract trades -1.5 at 112-23.5 after slipping to 112-22.5 low. Attention is on 112-10+, the 100-DMA and 112-06, the Sep 25 low. Trendline support also lies at 112-06+.

- Curves have unwound this week's steepening, 2s10s -.733 at 53.148, 5s30s -.431 at 104.291.

- Projected rate cut pricing has receded from this morning's levels (*): Dec'25 steady at -12bp, Jan'26 at -21.6bp (-22.1bp), Mar'26 at -32.6bp (-33.4bp), Apr'26 at -40.1bp (-41.1bp).

- Cross asset comparison: Bbg US$ continues to climb: BBDXY +6.33 at 1225.76; stocks generally mixed with SPX eminis +13 at 6653.00 while the DJIA trades down 56.92 points (-0.12%) at 45946.4. Crude weaker: WTI -1.31 at 59.43.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Candle Pattern Highlight Potential Reversal

Oct-20 19:30

- RES 4: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6660/6707 High Sep 18 / 17 and a bull trigger

- RES 2: 0.6629 High Sep 30 & Oct 01 and key short-term resistance

- RES 1: 0.6549 50-day EMA

- PRICE: 0.6518 @ 17:19 BST Oct 20

- SUP 1: 0.6440 Low Oct 14

- SUP 2: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 3: 0.6373 Low Jun 23

- SUP 4: 0.6357 Low May 12

A recovery in AUDUSD on Oct 144 continues to highlight a possible reversal pattern - a hammer candle formation. If correct, it signals the end of the bear cycle that started Sep 17. Note that moving average studies have remained in a bull-mode position during the latest bear leg, highlighting a dominant M/T uptrend. Initial resistance is 0.6549, the 50-day EMA. A breach of 0.6440, the Oct 14 low, would cancel the reversal signal and reinstate a bear threat.

US TSYS: Treasuries Inch Higher As US Enters Shutdown Day 19

Oct-20 19:29

- Treasuries extended the top end of the range late Monday on relatively modest volumes (TYZ5 just over 1M) as the US Gov enters shutdown day 19, no data & the Federal Reserve in policy blackout through October 30.

- The Dec'25 10Y futures contract trades +4 at 113-19, 113-10.5 low / 113-20 high. MA studies are in a bull-mode position and this set-up continues to highlight a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance.

- Speaking at a bilateral meeting with Australian PM Anthony Albanese, US President Donald Trump confirms that he intends to meet Chinese President Xi Jinping in South Korea during the Asia Pacific Economic Cooperation annual summit at the end of the month.

- Expected corporate earnings announcements after the close include: Cleveland-Cliffs, Crown Holdings, Steel Dynamics, AGNC Investment Corp and Zions Bancorp - the regional bank in the spotlight last week after it "disclosed a $50 million charge-off for a loan underwritten by its wholly-owned subsidiary, California Bank & Trust," Bbg reported.

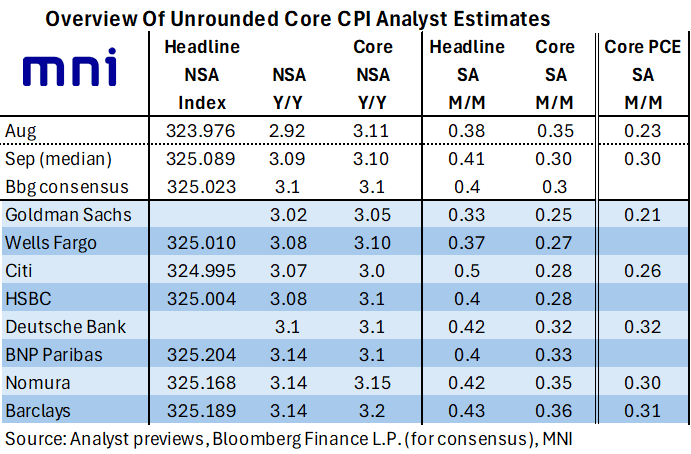

- Looking ahead, UK fiscal data will be published ahead of Canada CPI on Tuesday, while markets will remain focused on Friday’s US inflation data. An early look at analyst unrounded core CPI estimates for Friday’s delayed September release sees a median estimate of 0.30% M/M, with a reasonably wide range of 0.25-0.36% M/M.

US OUTLOOK/OPINION: Core CPI and Early PCE Estimates Eye 0.30% M/M For Sept

Oct-20 19:05

- An early look at analyst unrounded core CPI estimates for Friday’s delayed September release sees a median estimate of 0.30% M/M, with a reasonably wide range of 0.25-0.36% M/M.

- As such, core CPI inflation is mostly expected to moderate from the 0.35% in August although it would be a third consecutive strong month after the 0.32% in July as well.

- Indeed, if accurate, it would leave there having been only two months in the past twelve with a monthly rate equivalent to less than 2% annualized (March and May). That sets it up for a more clearly cut 3.1% Y/Y after accelerating to 3.06% in August.

- Of course, the Fed targets PCE inflation, with a median of the five forecasts for core PCE also at 0.30% M/M for September. In contrast to core CPI, this would be an acceleration after 0.23% M/M in August and 0.24% in July (prior to revisions, which should be more extensive being part of the annual update).

- It's still only seen two months in the past twelve with monthly inflation below 2% annualized (March and November) whilst annual core PCE inflation was still elevated at 2.9% Y/Y in August. The median FOMC member sees this accelerating further to an average 3.1% Y/Y in Q4 before moderating to 2.6% Y/Y in 4Q26 and 2.1% Y/Y in 4Q27.