US DATA: Fed Should Have Q3 GDP And September PCE Estimates By Its Dec Meeting

Nov-19 14:50

What's notable about the majority of post-shutdown rescheduled economic releases so far is that they are essential to compiling advance Q3 GDP and September PCE, both of which were originally due to be published by the Bureau of Economic Analysis at the end of October.

- That leaves it narrowly possible that we get an advance Q3 GDP release by the end of the month (ie Nov 28) depending on whether the BEA has time to compile and is willing to base their estimate on partial data to a greater degree than is usual, and whether the Thanksgiving holiday on Nov 27 forces a delay into the following week. Certainly we are now confident that the FOMC will have a Q3 GDP estimate and September PCE data in hand by the time of its Dec 9-10 meeting.

- September international price indices used in the GDP calculation are now due out by BLS on Dec 3, and September advance goods trade and business inventories data haven't yet been rescheduled (it was originally due out Oct 29, the day before advance GDP), but aside from these the BEA should have enough data to compile an initial Q3 estimate.

- With PPI and CPI data for September all out by Nov 25, BEA's got pretty much all it needs to produce a monthly PCE price estimate for that month, absent a narrow sliver that it gets from import prices. Just conjecture but it's possible that it could get the import prices it needs on an inter-agency basis ahead of Dec 3.

- As for the consumption and income portions of the September PCE report: the September payrolls data (Nov 20) will provide the underlying estimates for wages and salaries needed for the income estimates, while the retail sales data is the lion's share of the consumption data and much of the services consumption is either estimated anyway or derived from September nonfarm payrolls.

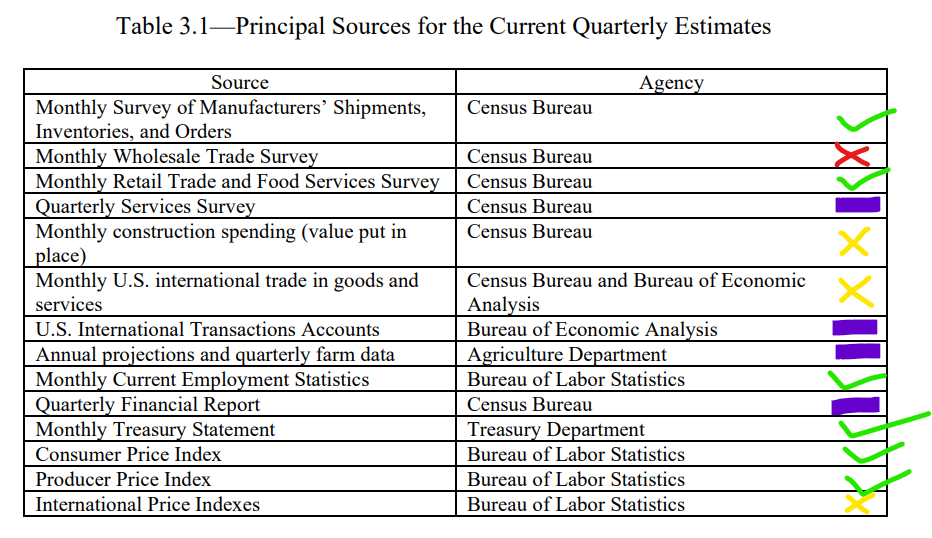

- For the quarterly GDP estimates, the image below shows the major reports used (from the BEA's methodology document) - the green checkmarks are those data that will be in hand by Wednesday Nov 26; the red X (wholesale trade) won't be available, the yellow X's will either likely be partly available or wouldn't have been available anyway by the original GDP release data; and the purple bars represent series that are used more for Gross Domestic Income and future revisions rather than the advance estimate.

- We've only had updates on this morning's trade data rescheduling from the BEA so far, but as we have been saying, they depend heavily on other agencies to compile the source data for their own series. As such we will hopefully hear from them soon as to the PCE and GDP reschedulings.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: SFIH6 1x2 Call Spread Buyer

Oct-20 14:49

SFIH6 96.30/50 1x2 call spread, paper pays 2.25 in +4.5k (bought the 1 leg)

EGBS: BTP/Bund Spread Near Session Lows, Growth Data Key To Further Narrowing

Oct-20 14:31

The 10-year BTP/Bund spread trades close to session lows of ~78.5bps, benefiting from the latest extension higher in global equity futures.

- We highlighted last week that having already tightened by ~35bps this year, the 10-year BTP/Bund spread has struggled to sustainably consolidated below 80bps in recent months.

- Signs of a more resilient domestic growth outlook may be a necessary condition for further narrowing. Although the 2026 draft budget projects the Italian deficit to fall to 2.8% next year, a weak growth trajectory may impede continued improvements in fiscal metrics. Q3 flash GDP is due on October 30.

- Note that EUR 3m10y swaption vol has also moved away from multi-year lows through October, which may be limiting near-term tightening impulses.

- BTP futures are +7 ticks at 121.53, off session lows of 121.58. Initial resistance is Friday’s opening high of 121.94.

- Italy is issuing the new retail-only 7-year Oct-32 BTP Valore this week. Day 1 books are currently E4.9bln. That’s above the E3.7bln raised on the first day of the last BTP Valore issue in May 2024, but currently below the E5.6bln raised on the first day of the BTP Piu issue in February 2025.

BOC: Canada Consumer And Business Inflation Views Soften But Remain Elevated

Oct-20 14:30

- Firms expecting inflation exceeding BOC target rate declined from 74% in Q2 to 69% in Q3.

- Two-thirds of consumers foresee a recession within a year, blaming trade war, yet also see inflation at 3.72% now and 4% a year from now.

- CSCE indicator -0.85 from prior -1.07; remains below historical levels.

- 70% of consumers believe the worst inflation spill-over is yet to come from tariffs.

- Surveys mostly gathered from July through Sept. BOC has said it will remain cautious on interest rates after a return to cutting last month.