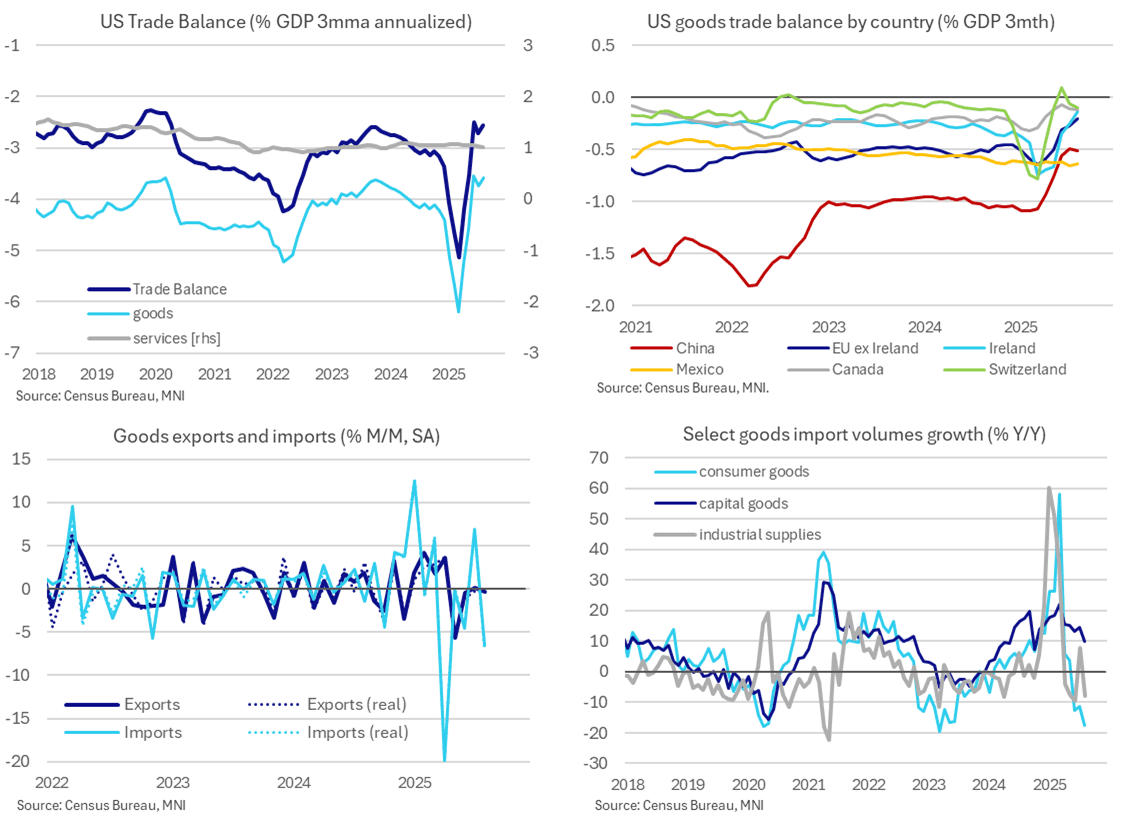

US DATA: China And EU Leading Largest Adjustments In Trade With US [1/2]

Nov-19 14:37

- The goods & services trade deficit was close to expectations in August at $59.6bn (cons $60.4bn) after a marginally revised $78.2bn in July.

- This is the full August release that was delayed by the government shutdown, after the initial advance covering just goods trade had been reported on Sep 25.

- Exports increased 0.1% M/M, with reasonable services growth of 0.8% M/M offsetting softer goods at -0.3% M/M as broadly indicated by the advance release.

- Imports were confirmed to have fallen firmly, with -5.1% M/M after bouncing 5.9% M/M in July, driven primarily by goods (-6.6% after 6.9%) whilst services increased a little further (0.4% after 2.3%). The swing in imports was due to monetary gold – to be discussed in part two.

- The $264.6bn of goods imports poked below the $264.9bn in June for its lowest since Jan 2024 – of note for a nominal series – although the subsequent uplift in services imports saw broader goods & services imports hold above its June recent low.

- Driving these trends, goods imports volumes are currently -4.0% Y/Y for their most negative since mid-2023. Consumer goods have clearly been adversely impacted by tariffs (-18% Y/Y) along with industrial supplies more recently (-8% Y/Y). Capital goods (10% Y/Y) continues to be an important offsetting driver, having been growing strongly since mid-2024 and with 10% Y/Y actually its softest since October.

- It left the goods & services trade deficit at 2.6% GDP on a three-month basis in August vs 5.1% GDP in Q1 on peak tariff front-running and 3.4% GDP in Q4.

- Latest updates on country trade balances vs Dec’24 levels: China -0.6% GDP vs -1.1%, EU -0.4% vs -0.8%, Switz. -0.1% vs -0.3% and then less change for Canada at -0.1% vs -0.2%, UK 0.1% vs 0.0% and Mexico -0.6% vs -0.6%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: BTP/Bund Spread Near Session Lows, Growth Data Key To Further Narrowing

Oct-20 14:31

The 10-year BTP/Bund spread trades close to session lows of ~78.5bps, benefiting from the latest extension higher in global equity futures.

- We highlighted last week that having already tightened by ~35bps this year, the 10-year BTP/Bund spread has struggled to sustainably consolidated below 80bps in recent months.

- Signs of a more resilient domestic growth outlook may be a necessary condition for further narrowing. Although the 2026 draft budget projects the Italian deficit to fall to 2.8% next year, a weak growth trajectory may impede continued improvements in fiscal metrics. Q3 flash GDP is due on October 30.

- Note that EUR 3m10y swaption vol has also moved away from multi-year lows through October, which may be limiting near-term tightening impulses.

- BTP futures are +7 ticks at 121.53, off session lows of 121.58. Initial resistance is Friday’s opening high of 121.94.

- Italy is issuing the new retail-only 7-year Oct-32 BTP Valore this week. Day 1 books are currently E4.9bln. That’s above the E3.7bln raised on the first day of the last BTP Valore issue in May 2024, but currently below the E5.6bln raised on the first day of the BTP Piu issue in February 2025.

BOC: Canada Consumer And Business Inflation Views Soften But Remain Elevated

Oct-20 14:30

- Firms expecting inflation exceeding BOC target rate declined from 74% in Q2 to 69% in Q3.

- Two-thirds of consumers foresee a recession within a year, blaming trade war, yet also see inflation at 3.72% now and 4% a year from now.

- CSCE indicator -0.85 from prior -1.07; remains below historical levels.

- 70% of consumers believe the worst inflation spill-over is yet to come from tariffs.

- Surveys mostly gathered from July through Sept. BOC has said it will remain cautious on interest rates after a return to cutting last month.

MNI: BOC OUTLOOK SURVEY: FUTURE SALES GROWTH BALANCE OF OPINION -2

Oct-20 14:30

- MNI: BOC OUTLOOK SURVEY: FUTURE SALES GROWTH BALANCE OF OPINION -2

- BANK OF CANADA BUSINESS OUTLOOK SURVEY OVERALL INDICATOR -2.28

- BOC: CONSUMERS SEE INFLATION AT 3.72% NOW, 4% IN 1 YEAR