MNI ASIA OPEN: Neutral PPI, Beige Book Inflation Rising

EXECUTIVE SUMMARY

- MNI FED: Beige Book: Inflation Seen Rising More Rapidly By Late Summer

- MNI FED: Beige Book: Hiring Looking Solid Despite Lingering Uncertainty

- MNI FED: Beige Book: Economic Activity Improved, But Pessimism Persists

- MNI US DATA: Core PCE Estimates Could Be Trimmed Following Neutral PPI Readthrough

- MNI US DATA: PPI Suggests Tariffed Pipeline Price Pressures Less Acute Than Feared

US

MNI FED: Beige Book: Inflation Seen Rising More Rapidly By Late Summer

The July Beige Book's description of inflation suggested relatively steady price pressures compared with the June report, though it seems that what were previously "plans" to pass through tariff-related costs to customers have begun to materialize. In probably the most important finding for the FOMC, the biggest price increases are yet to come: "Contacts in a wide range of industries expected cost pressures to remain elevated in the coming months, increasing the likelihood that consumer prices will start to rise more rapidly by late summer."

MNI FED: Beige Book: Hiring Looking Solid Despite Lingering Uncertainty

The July Beige Book characterizes the labor market in fairly mixed fashion, though generally stable to slightly-positive across most Fed Districts compared with the June beige book. Arguably this is the most solid Beige Book on the employment front since the start of the year, though businesses continued to report holding off on hiring plans "until uncertainty diminished" . Wages were seen as flat-to-moderate.

MNI FED: Beige Book: Economic Activity Improved, But Pessimism Persists

July's Beige Book notes that "economic activity increased slightly from late May through early July." Most Fed Districts reported flat growth: 7 were in that category (Boston, Cleveland, Atlanta, St Louis, Minneapolis, Kansas City, San Francisco), with 3 reporting slight/modest growth (Richmond, Chicago, Dallas) and 2 seeing modest declines (New York, Philadelphia). See table below for summary of current conditions.

NEWS

MNI US: Trump Rejects Reports Of Firing Powell, Keeps Door Open For 'Fraud' Reasons

President Donald Trump has addressed recent reporting that he could fire Fed Chair Jerome Powell, ahead of a bilateral meeting with the Crown Prince of Bahrain. Asked if he could fire Powell, Trump says: "He's always been too late... he should have cut interest rates a long time ago... The only time he cut them was to [benefit Democrats]... I think he does a terrible job..."

MNI US: Odds Of Trump Firing Powell Spikes After CBS Highlights White House Meeting

The implied probability of President Donald Trump firing Fed Chair Jerome Powell spiked to 30% in the last few minutes, after CBS highlighted comments made during a closed-door meeting yesterday. While Trump has repeatedly applied pressure on Powell, in an apparent effort to force him to resign, there hasn't been an obvious route for removing Powell from office before May 2026. AP notes the Supreme Court signaled Trump doesn’t have the authority to remove Powell over an interest rate disagreement.

US TSYS

MNI US TSYS: Curves Steepen to New 4+ Year Highs, Pres Trump Trolls Chair Powell

- Treasuries look to finish near moderate late session highs, early support after lower than expected PPI inflation measures leavened by up-revisions to May reads. The main headline reading was flat PPI % M/M (0.01% unrounded), vs expectations of a 0.2% rise (though this was offset by an upward revision to May, to 0.30% from 0.13%). That left Y/Y PPI at the softest level (2.3%) since September 2024, and down from 2.7% in May.

- Industrial production rose by 0.3% M/M in June (0.1% expected), a figure that looks even more solid when considering the upward revision to prior (May 0.0%, albeit very slightly negative unrounded at -0.03%, rev from -0.2%). Capacity utilization unexpectedly rose to 77.6% (expected unchanged at 77.4%, rev up to 77.5% in May).

- Tsys pared gains after headlines that Pre Trump asked GOP lawmakers if he should fire Fed Chairman Powell now - before the end of his term in May 2026. US$ and equities reacted more sharply, both selling off on the chatter before rebounding late morning after Trump denied reports of an imminent termination of the Fed Chair (unless cause found under pretense of funds misuse for Fed headquarter renovation).

- Currently, Sep'25 10Y contract trades +11 at 110-20 vs. 110-21.5 high. Initial technical resistance above at 111-01 (20-day EMA). Support below at 110-08.5 (Low Jul 14). Curves bounced off lows on wide ranges: 2s10s +2.641 at 56.381; 5s30s +4.649 at 102.55p vs. 107.895 high - highest intraday level since October 2021.

- Focus turns to Thursday's weekly jobless claims, Retail Sales, Import/Export Prices and TIC flows as well as several Fed speakers ahead the start of late Friday's policy Blackout.

OVERNIGHT DATA

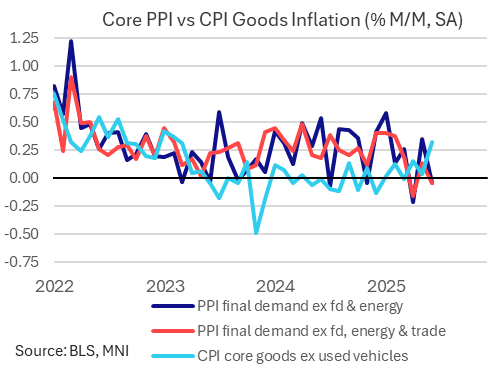

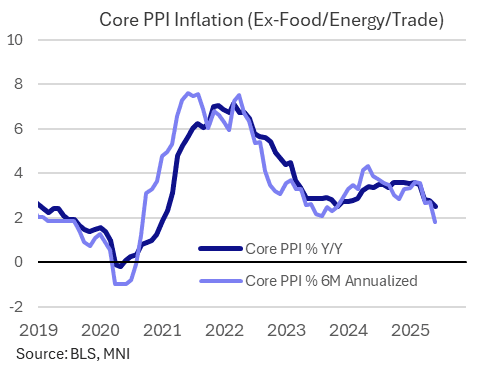

MNI US DATA: PPI Suggests Tariffed Pipeline Price Pressures Less Acute Than Feared

The June Producer Price Index report was roundly softer than expected - and certainly than feared given the context of rising tariffs - despite some upward revisions to prior. While core goods prices did indeed advance, the rise was consistent with the increases seen over the last 6 months rather than a sudden surge.

- The main headline reading was flat PPI % M/M (0.01% unrounded), vs expectations of a 0.2% rise (though this was offset by an upward revision to May, to 0.30% from 0.13%). That left Y/Y PPI at the softest level (2.3%) since September 2024, and down from 2.7% in May. Ex-food and energy final demand inflation unexpectedly fell, by 0.04% M/M (+0.2% was expected), though again May's upward revision must be considered (0.35%, upward rev from 0.14%).

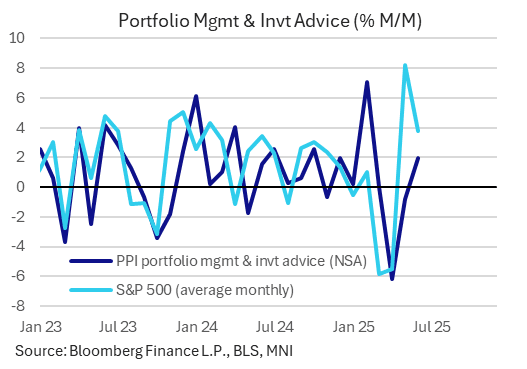

MNI US DATA: PPI Portfolio Services Lift With More Likely To Come

Adding to what looks like roughly a neutral contribution to core PCE from PPI details at first glance. Portfolio-related costs look somewhat in the ballpark of limited expectations we'd seen.

- Portfolio management & investment advice: 1.9% M/M in June after an unrevised -0.8% M/M in May.

Within that, portfolio management increased 2.2% after -0.9%. Citi had eyed 2.5% for portfolio mgmt whilst Nomura had looked for 4.3% for the broader portfolio & invt advice.

MNI US DATA: Core PCE Estimates Could Be Trimmed Following Neutral PPI Readthrough

- Our crude proxy for key PPI contributions to core PCE sees another broadly neutral month in June, implying a boost of 0.02pp after a slightly upward revised 0.01pp in May (initially -0.01pp). For comparison, it follows -0.07pp in Apr, 0.07pp in Mar and 0.19pp in Feb.

- As such, it could leave core PCE estimates drift back a little closer to yesterday’s core CPI of 0.23% M/M vs pre-PPI core PCE estimates averaging 0.31% M/M. Of course that does also depend on what analysts expectations for particular line items.

- Reiterating how it’s not an exact science: whilst this rough proxy implies little boost from PPI details in May, there was still a slight gap between the 0.18% M/M currently seen for core PCE and 0.13% for core CPI.

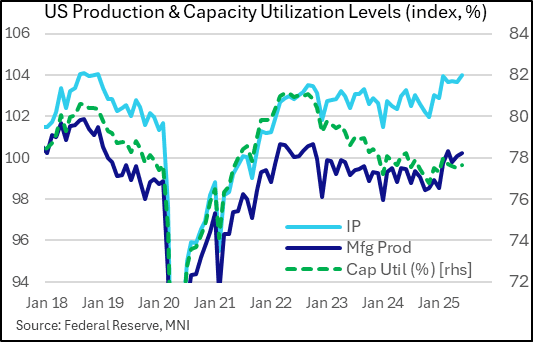

MNI US DATA: Industrial Production Picks Up In June, But Momentum Remains Weak

Industrial production rose by 0.3% M/M in June (0.1% expected), a figure that looks even more solid when considering the upward revision to prior (May 0.0%, albeit very slightly negative unrounded at -0.03%, rev from -0.2%). Capacity utilization unexpectedly rose to 77.6% (expected unchanged at 77.4%, rev up to 77.5% in May).

- While momentum in the industrial sector remains weak, this was the biggest rise in IP since February. And all major market groups (consumer goods, business equipment, nonindustrial supplies, and materials) all saw expansions for the first time since February.

- On a 3M/3M annualized basis, IP is rising at just a 1.1% clip, the slowest since January; that's 2.1% for manufacturing, slowest since February. Both have slowed considerably since February/March in what seems to be tariff front-running effects dissipating.

- Overall, industrial / manufacturing production looks to be stabilizing at a weak level amid a period of considerable tariff policy-related uncertainty that has caused output to fluctuate. We note that motor vehicle and parts production fell 2.6% in June (+4.6% in May), with production of electrical equipment, appliances, and components down 2.5% (after +2.4%), suggesting mixed sectoral dynamics at best.

- ISM manufacturing picked up to a 3-month high 49.0 in June, while core durable goods orders picked up strongly in May (+1.7%), boding well for upcoming output/business investment. But momentum in the latter (0.4% 3M/3M annualized) remains very weak, and the ISM remains slightly contractionary.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 203.64 points (0.46%) at 44225.36

S&P E-Mini Future up 20.75 points (0.33%) at 6304.5

Nasdaq up 57.7 points (0.3%) at 20736.45

US 10-Yr yield is down 3 bps at 4.4513%

US Sep 10-Yr futures are up 10.5/32 at 110-19.5

EURUSD up 0.0035 (0.3%) at 1.1636

USDJPY down 1.02 (-0.69%) at 147.87

WTI Crude Oil (front-month) up $0.05 (0.08%) at $66.57

Gold is up $23.01 (0.69%) at $3347.65

European bourses closing levels:

EuroStoxx 50 down 56.1 points (-1.05%) at 5298.07

FTSE 100 down 11.77 points (-0.13%) at 8926.55

German DAX down 50.91 points (-0.21%) at 24009.38

French CAC 40 down 44.12 points (-0.57%) at 7722.09

US TREASURY FUTURES CLOSE

3M10Y -2.487, 10.843 (L: 8.468 / H: 14.533)

2Y10Y +2.641, 56.381 (L: 50.67 / H: 61.262)

2Y30Y +4.706, 112.391 (L: 104.416 / H: 120.39)

5Y30Y +4.544, 102.454 (L: 95.702 / H: 107.895)

Current futures levels:

Sep 2-Yr futures up 4.25/32 at 103-21 (L: 103-16.75 / H: 103-22.875)

Sep 5-Yr futures up 9.25/32 at 108-4 (L: 107-26.5 / H: 108-05.75)

Sep 10-Yr futures up 10.5/32 at 110-19.5 (L: 110-08.5 / H: 110-21.5)

Sep 30-Yr futures up 6/32 at 112-5 (L: 111-11 / H: 112-23)

Sep Ultra futures up 1/32 at 114-25 (L: 113-20 / H: 115-21)

MNI US 10YR FUTURE TECHS: (U5) Support Has Been Breached

- RES 4: 112-15 61.8% retracement of the Apr 7 - 11 sell-off

- RES 3: 112-12+ High Jul 1 and a bull trigger

- RES 2: 111-13+/111-28 High Jul 10 / High Jul 3

- RES 1: 111-01 20-day EMA

- PRICE: 110-12+@ 11:17 BST Jul 16

- SUP 1: 110-08+ Low Jul 14

- SUP 2: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 3: 109-28 Low Jun 6 and 11

- SUP 4: 109.25 Low May 27

Treasury futures traded lower yesterday. The contract has breached an important support at 110-17, 61.8% of the May 22 - Jul 1 bull leg. Note that price has also traded through a trendline support at 110-23+. The line is drawn from the May 22 low. This strengthens a bearish theme and a continuation would open 110-03, the 76.4% retracement. Resistance to watch is 111-13+, Jul 10 high. Initial resistance is at 111-01, the 20-day EMA.

SOFR FUTURES CLOSE

Sep 25 +0.010 at 95.830

Dec 25 +0.035 at 96.115

Mar 26 +0.065 at 96.375

Jun 26 +0.085 at 96.610

Red Pack (Sep 26-Jun 27) +0.090 to +0.10

Green Pack (Sep 27-Jun 28) +0.060 to +0.080

Blue Pack (Sep 28-Jun 29) +0.040 to +0.055

Gold Pack (Sep 29-Jun 30) +0.020 to +0.035

Of note: Another LARGE SOFR futures fly traded on the screen overnight: appr 23,000 SFRH'29/SFRU'29/SFRH'30 flys, the spread spanning Blues through Golds reportedly bought at -0.010 (steady). This after paper sold 25,000 SFRM'27/SFRU'27/SFRZ'27 flys at -0.005 yesterday (opener). The latter a potential year end funding play, albeit on deferred contracts that wont expire for over 2 years. Traders remind back spds aren't typically volatile, an opportunity to park capital and avoid current real vol in nearer expirys.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.37% (+0.04), volume: $2.784T

- Broad General Collateral Rate (BGCR): 4.36% (+0.04), volume: $1.131T

- Tri-Party General Collateral Rate (TCR): 4.36% (+0.04), volume: $1.107T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $101B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $252B

FED Reverse Repo Operation

RRP usage slips to $197.086B this afternoon from $198.277B yesterday, total number of counterparties at 35. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

MNI PIPELINE: Corporate Bond Update: $4B JPM 11NC10 Debt Launched

- Date $MM Issuer (Priced *, Launch #)

- 07/16 $4B #JP Morgan 11NC10 +112.5

- 07/16 $2.75B #Citigroup PerpNC5 6.875%

- 07/16 $2.2B #Indonesia Sukuk $1.1B 5Y 4.55%, $1.1B 10Y 5.2%

- 07/16 $2.2B #Kioxia Holdings $1.1B 5NC2 6.25%, $1.1B 8NC3 6.625%

- 07/16 $500M #Golub Capital Private Cr 3Y +183

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform Post-CPI, Pre-Labour Data

Bunds outperformed Gilts Wednesday following firmer-than-expected UK inflation data.

- Gilt yields gapped higher on the open, following UK June CPI coming in above consensus on most measures.

- But the move faded somewhat as the report was digested, with the broader scope of the report not significantly differing from the BOE's existing expectations for inflation developments (and greater focus anyhow on upcoming labour market data).

- In early afternoon trade, global core FI rallied as US PPI data came in on the soft side

- Volatility picked up toward the cash close on reports that US President Trump planned to soon fire Federal Reserve Chair Powell. This saw long-end yields rise again but Trump's denial made just before the European cash close saw Gilt and Bund yields have a final dip.

- The German curve leaned bull steeper on the day, with the UK's leaning bear flatter - the belly outperformed on both curves.

- Periphery/semi-core EGB spreads were little changed.

- Thursday's highlight is the UK labour market report - our preview is here. The main focus this month will be on a combination of private regular average earnings and the notoriously revised payrolls numbers.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.7bps at 1.86%, 5-Yr is down 3.3bps at 2.23%, 10-Yr is down 2.5bps at 2.687%, and 30-Yr is down 1.2bps at 3.214%.

- UK: The 2-Yr yield is up 1.9bps at 3.855%, 5-Yr is up 1.1bps at 4.042%, 10-Yr is up 1.4bps at 4.639%, and 30-Yr is up 1.1bps at 5.469%.

- Italian BTP spread down 0.4bps at 85.6bps / French OAT down 0.2bps at 69.8bps

MNI FOREX: Very Volatile USD Swings as Trump Headlines on Fed Chair Dominate

- Initial price action on Wednesday saw the US dollar extend its cautious recovery, underpinned by prior US inflation data which showed signs of increasing passthrough to consumer prices from tariffs. However, volatile greenback swings then ensued as headlines surrounding President Trump’s potential intentions to fire Fed Chair Powell dominated global markets.

- Initial reporting suggested that President Trump indicated to Republican lawmakers that he will "likely" fire Federal Reserve Chair Jerome Powell soon, after receiving approval from them to make the move, a senior White House official told journalists. This prompted a severe reversal lower for the dollar, with the DXY dropping as much as 1.15% as short-term greenback longs were swiftly pressured. Alongside downside pressure for both equities and front-end US yields, USDJPY rapidly sold off to an intra-day low of 146.92, around 225 pips off the overnight highs.

- However, shortly after the significant greenback selloff Trump addressed journalists in the White House - appearing alongside PM of Bahrain – where he appeared to downplay these rumours, stating he was not planning on firing the Fed Chair and that reports of drafting a letter to fire Jerome Powell aren’t true.

- The USD snapped sharply higher as a result, although the USD index remains ~0.25% lower on the session ahead of the APAC crossover amid the heightened lingering uncertainty. USDJPY settled just above the 148 mark, down ~0.5% on the session.

- EURUSD has been equally volatile, trading a 1.1563-1.1721 range. The pair currently operates around 1.1640 as markets digest the latest developments in the US. The move down in recent sessions appears corrective and trend signals continue to highlight a dominant uptrend.

- A quick mention to GBPUSD which had a very limited reaction to firmer-than-expected CPI data on Wednesday. Late currency volatility also had less of an impact on GBP, ahead of key labour market data due Thursday. A close at current levels (1.3420) would keep the focus on the most recent breach of trendline support, drawn from the January lows.

- Elsewhere, Australian employment data and US retail sales will be highlights on the global calendar.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 17/07/2025 | 0600/0700 | *** | Labour Market Survey | |

| 17/07/2025 | 0900/1100 | *** | HICP (f) | |

| 17/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 17/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 17/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/07/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/07/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1400/1000 | Fed Governor Adriana Kugler | ||

| 17/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 17/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 17/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 17/07/2025 | 1645/1245 | San Francisco Fed's Mary Daly | ||

| 17/07/2025 | 1730/1330 | Fed Governor Lisa Cook | ||

| 17/07/2025 | 2000/1600 | ** | TICS | |

| 17/07/2025 | 2230/1830 | Fed Governor Christopher Waller | ||

| 18/07/2025 | 2330/0830 | *** | CPI |