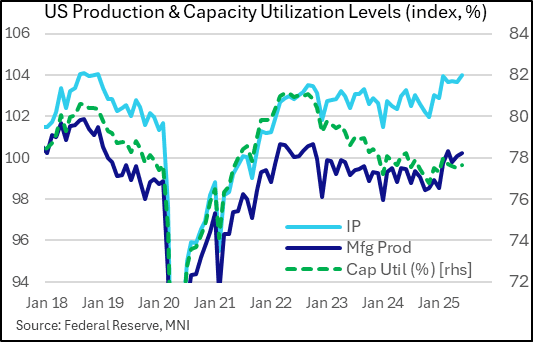

US DATA: Industrial Production Picks Up In June, But Momentum Remains Weak

Industrial production rose by 0.3% M/M in June (0.1% expected), a figure that looks even more solid when considering the upward revision to prior (May 0.0%, albeit very slightly negative unrounded at -0.03%, rev from -0.2%).

- To be sure, the volatile utilities sector played an outsized role in the pickup, rising 2.8% after falling 2.5% in May. But manufacturing production was better than expected too - up 0.1% M/M (0.0% expected, with a 0.2pp upward revision to prior to 0.3%)), helping offset a 0.3% contraction in mining (+0.1% prior).

- Capacity utilization unexpectedly rose to 77.6% (expected unchanged at 77.4%, rev up to 77.5% in May).

- While momentum in the industrial sector remains weak, this was the biggest rise in IP since February. And all major market groups (consumer goods, business equipment, nonindustrial supplies, and materials) all saw expansions for the first time since February.

- On a 3M/3M annualized basis, IP is rising at just a 1.1% clip, the slowest since January; that's 2.1% for manufacturing, slowest since February. Both have slowed considerably since February/March in what seems to be tariff front-running effects dissipating.

- Overall, industrial / manufacturing production looks to be stabilizing at a weak level amid a period of considerable tariff policy-related uncertainty that has caused output to fluctuate. We note that motor vehicle and parts production fell 2.6% in June (+4.6% in May), with production of electrical equipment, appliances, and components down 2.5% (after +2.4%), suggesting mixed sectoral dynamics at best.

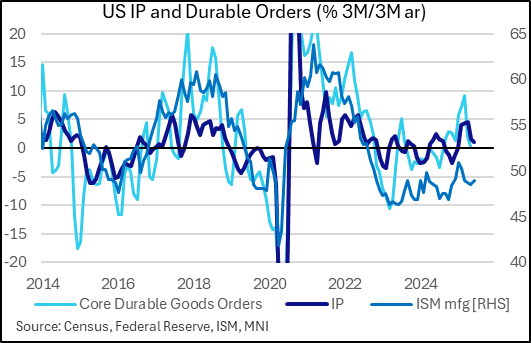

- ISM manufacturing picked up to a 3-month high 49.0 in June, while core durable goods orders picked up strongly in May (+1.7%), boding well for upcoming output/business investment. But momentum in the latter (0.4% 3M/3M annualized) remains very weak, and the ISM remains slightly contractionary.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY TECHS: E-MINI S&P: (U5) Support Remains Intact

- RES 4: 6200.00 1.500 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6172.50 High Feb 24

- RES 2: 6134.00 High Feb 26

- RES 1: 6128.75 High Jun 11

- PRICE: 6069.25 @ 07:42 BST Jun 16

- SUP 1: 5979.00/5882.88 Low Jun 13 / 50-day EMA

- SUP 2:5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis remains bullish and the contract traded to a fresh cycle high last Wednesday, reinforcing current bullish conditions. For now, the most recent pullback is considered corrective. The contract has pierced support at 5990.75, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5882.88. Key short-term resistance has been defined at 6128.75, the Jun 11 high.

EQUITIES: US Cash Opening Calls

SPX: 6,021.6 (+0.7%); DJIA: 42,458 (+0.6%/+261pts); NDX: 21,830.9 (+0.9%).

BONDS: Off Lows As Oil Ticks Lower

A steady downtick in crude oil futures through the London morning into early NY trade initially allowed core global FI markets to base and has limited any selling pressure in the time since.

- Brent & WTI trade a little over $1 lower on the day after Friday highs capped the opening spike higher that came on the back of the weekend Israel-Iran escalation.

- While Israel-Iran commentary remains relatively hardline, there has been a lack of meaningful escalation since the London open, weighing on crude in that window.

- Core global bond curves hold steeper on the day (some twist, some bear) with major traded inflation metrics (5y5y and 2-Year zero coupon swaps) mostly back to unchanged on the day, with cues from oil dominating in the latter as well.