US TSYS: Curves Steepen to New 4+ Year Highs, Pres Trump Trolls Chair Powell

Jul-16 19:50

- Treasuries look to finish near moderate late session highs, early support after lower than expected PPI inflation measures leavened by up-revisions to May reads. The main headline reading was flat PPI % M/M (0.01% unrounded), vs expectations of a 0.2% rise (though this was offset by an upward revision to May, to 0.30% from 0.13%). That left Y/Y PPI at the softest level (2.3%) since September 2024, and down from 2.7% in May.

- Industrial production rose by 0.3% M/M in June (0.1% expected), a figure that looks even more solid when considering the upward revision to prior (May 0.0%, albeit very slightly negative unrounded at -0.03%, rev from -0.2%). Capacity utilization unexpectedly rose to 77.6% (expected unchanged at 77.4%, rev up to 77.5% in May).

- Tsys pared gains after headlines that Pre Trump asked GOP lawmakers if he should fire Fed Chairman Powell now - before the end of his term in May 2026. US$ and equities reacted more sharply, both selling off on the chatter before rebounding late morning after Trump denied reports of an imminent termination of the Fed Chair (unless cause found under pretense of funds misuse for Fed headquarter renovation).

- Currently, Sep'25 10Y contract trades +11 at 110-20 vs. 110-21.5 high. Initial technical resistance above at 111-01 (20-day EMA). Support below at 110-08.5 (Low Jul 14). Curves bounced off lows on wide ranges: 2s10s +2.641 at 56.381; 5s30s +4.649 at 102.55p vs. 107.895 high - highest intraday level since October 2021.

- Focus turns to Thursday's weekly jobless claims, Retail Sales, Import/Export Prices and TIC flows as well as several Fed speakers ahead the start of late Friday's policy Blackout.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Macro Since Last FOMC: Labor - Wages Surprise Hotter

Jun-16 19:49

- On the flip side, wage growth has also started to come in hotter. We wouldn’t put too much weight on the surprisingly strong 0.42% M/M increase in average hourly earnings in May in isolation but it followed a strong 6.6% annualized increase in unit labor costs in Q1 (strongest since 1Q24 and before that 3Q22).

- Productivity growth played a role here, falling -1.5% annualized for its first decline since 2Q22 after a period of some particularly strong gains, but the underlying wage growth series was still strong.

- Whilst Powell has previously said he doesn’t expect inflationary pressures to come from the labor market, wage growth is starting to warrant closer inspection.

US OUTLOOK/OPINION: Macro Since Last FOMC: Labor - Solid NFPs But Other Cracks

Jun-16 19:47

- We characterized the single payrolls report since the last FOMC meeting as being “good enough to keep the Fed patient”.

- Nonfarm paryolls growth modestly beat expectations in May with 139k (cons 126k) although was marred by a 95k two-month downward revision. It left a three-month average of 135k, which is still reasonable considering heavy restrictions in immigration policies see long-term breakeven estimates of 100k start to be a more realistic comparison.

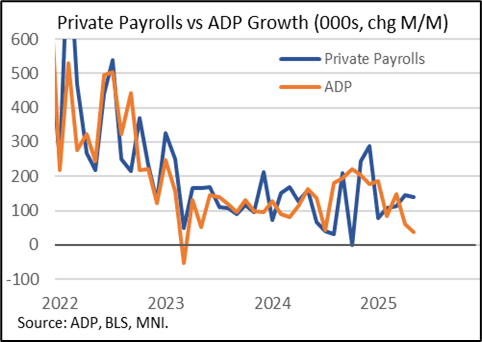

- Private sector job creation has driven that almost entirely, with a three-month average of 133k, although the separate ADP report points to a more modest trend with a three-month average of 81k including just 37k in May.

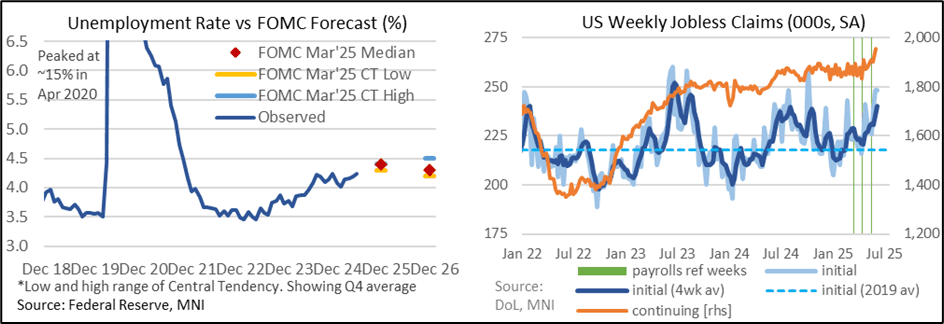

- The unemployment rate continued a slow upward trajectory as it increased from 4.187% to 4.244%, a fourth consecutive monthly increases. Whilst it has only increased a combined 0.11pp in the latest three months, it has nevertheless inched above November’s recent high of 4.23% for technically the highest since Oct 2021.

- On its own, and ahead of fresh projections to be formed at this meeting, it’s unlikely to trouble the median FOMC projection for an unemployment rate of 4.4% in 4Q25 from the March SEP (projections of course made ahead of reciprocal tariff announcements).

- However, whilst the initial resilience to policy changes under the second Trump administration might tempt some on the FOMC to leave their forecasts unchanged, the past two weeks of jobless claims data have provided a warning shot with signs of more pronounced deterioration.

FED: Jun 2025 FOMC Analyst Views: Same Dots Seen, But A Close Call (1/2)

Jun-16 19:40

None of the 28 analysts whose June FOMC previews were seen by MNI expect a rate cut in June – or, for that matter, July. Here we review the expected revisions to the quarterly economic projections:

- Macro Forecasts/Dot Plot: The FOMC's 2025 rate dot median is seen unchanged by the median analyst, at 3.9% (2 cuts from current levels by year-end).

- However that's an extremely close call: 11 of 24 analysts who expressed an opinion expect it to shift up 25bp vs March's, to 4.1%, with the other 13 see it remaining at 3.9%.

- Of the 17 analysts who had a view on the 2026 median, 7 saw an upward shift by 25 to 3.6% (the remaining 10 saw no change at 3.4%).

- The longer-run dot is more unanimously seen remaining at 3.0%, with 12 of 15 analysts seeing no change (3 see a rise to 3.1%).

- Analysts who expressed an opinion on the macroeconomic forecast portion of the SEP are largely unanimous that 2025 GDP will be revised lower while unemployment and inflation are revised higher; dynamics for 2026 were due to see revisions largely in the same direction though somewhat mixed.

MNI Markets Team Expectations For June 2025 Summary Of Economic Projections Medians