MNI ASIA OPEN: Geopol Jitters Not Reflected in Rate Cut Ests

EXECUTIVE SUMMARY

- MNI FED: Two Cuts Priced This Year Headed Into FOMC Week

- MNI SECURITY: Trump Says "It's Not Too Late For Iran To Make A Deal"

- MNI SECURITY: Israel's Operation Against Iran Could Last Two-Three Weeks - Ynet

- MNI MIDEAST: Iran Launches Retaliatory Drone Wave Following Israeli Strikes

- MNI US DATA: U.Mich Inflation Exp. Imply More Republican Responses

US

MNI FED: Two Cuts Priced This Year Headed Into FOMC Week

As we head into the June Fed meeting week, market pricing is reflective of the FOMC’s messaging (that we describe in our preview):

- The next cut is only fully priced by the October FOMC meeting, with September seeing a roughly 80% implied probability of bringing the next 25bp reduction. Exactly 50bp of cuts are priced through end-2025, implying two Q4 cuts.

- That’s a shift from just after the May meeting, after which the next cut was fully priced by September, and there were closer to three cuts priced for the rest of the year.

- Overall cuts are seen backloaded this year (after 15bp in September, 29bp of cuts priced in Q4 - Oct/Dec combined), but falls off in Q1 (just 21bp cuts priced, 9bp of cuts priced for January and 12bp for March)

MNI FED WATCH: Rates Steady As Tariffs Lift Inflation Forecast

Federal Reserve officials are expected to hold interest rates steady Wednesday for a fourth straight meeting and mark up their inflation and unemployment forecasts as President Trump's tariffs begin eating away at growth. Fed Chair Jerome Powell and his colleagues maintain that monetary policy is "in a good place" to wait until later in the year before deciding on any policy moves. Since the FOMC last met in May, the U.S.-China trade clash had de-escalated, re-escalated and de-escalated again, while the 90-day pause on the April 2 "reciprocal tariffs" is set to expire next month.

NEWS

MNI SECURITY: Trump Says "It's Not Too Late For Iran To Make A Deal"

US President Donald Trump has told Reuters that, “it's not too late for Iran to make a deal.” The interview with Reuters is the latest in an uncharacteristic string of one-on-one interviews with mainstream media outlets, a press strategy that indicates the White House is trying to get ahead of press speculation about US involvement in the Israeli strikes. It also appears an attempt to head-off reporting Washington was broadsided by Israel’s strikes.

MNI SECURITY: E3 Leaders 'Urge De-Escalation' & 'Back Israel Self-Defence'

Speaking to Bloomberg News, British Prime Minister Sir Keir Starmer says that his gov't has "grave concerns" about Iran's nuclear programme, and that it backs Israel's right to self-defence. He goes on to call for de-escalation in the situation. These comments mirror almost exactly those from French President Emmanuel Macron and German Chancellor Friedrich Merz, with the 'E3' (the three European signatories to the 2015 Joint Comprehensive Plan of Action, the Iran nuclear deal) acting in concert following a joint call between the three leaders earlier today.

MNI SECURITY: Israel's Operation Against Iran Could Last Two-Three Weeks - Ynet

Israel's Ynet reports that Israeli officials estimate fighting with Iran, "could stretch for two to three weeks, with more strikes on tap." Ynet notes that Israeli Prime Minister Benjamin Netanyahu, "is expected to speak on Friday with U.S. President Donald Trump as the Israeli Air Force continues strikes in Iran entering their 12th hour, including attacks in Iran's western Hamadan province."

MNI MIDEAST: Iran Launches Retaliatory Drone Wave Following Israeli Strikes

Reuters reports that, according to the US State Department, the US Embassy (likely in Amman) has "indications there may be missiles, drones, or rockets flying over Jordanian airspace". There have been numerous reports over the past hour that Iran has launched at least a first wave of ~100 retaliatory drones/missiles against Israel following the overnight attacks on nuclear and political sites and key military commanders and scientists.

US TSYS

MNI US TSYS: Risk-Off Gains Traction as Iran Retaliates Against Israeli Strikes

- Treasuries look to finish broadly lower Friday, off late session lows amid some position squaring amid reports Iran has retaliated against Israel's heavy bombing the night before with dozens of their own missile Friday.

- Israel struck over 200 targets in Iran including nuclear facilities overnight, killing several military commanders. Iran has 7 known nuclear facilities: Arak, Bushehr, Darkhovin, Fordow, Karun, Natanz and Isfahan -- of which the last 2 were hit. Israeli officials said the operation would last several days.

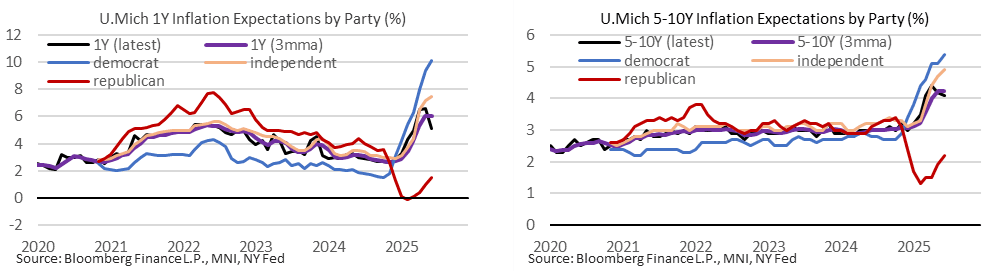

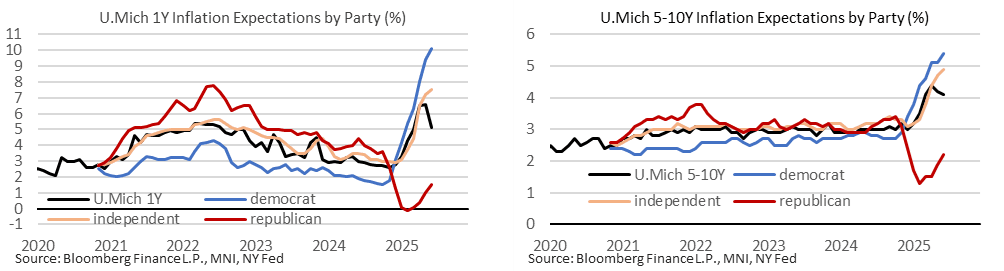

- Treasuries came under pressure after latest UofM sentiment came out higher than expected, 1Y inflation much lower than expected (5-10Y in-line). Details implied a notably heavier response from republican-leaning respondents, who have much lower inflation expectations under the Trump administration.

- According to data pulled in by Bloomberg, whilst the median 1Y expectations slipped from 6.6% to 5.1%, democrats increased from 9.4% to 10.1%, independents from 7.2% to 7.5% and republicans from 1.0% to 1.5%.

- After the bell, Tsy Sep'25 10Y futures currently trade -14 at 110-20 vs. 110-14 low, technical support below at 109-28 (Low Jun 6 / 11). Curves steeper: 2s10s +1.512 at 46.245, 5s30s +1.914 at 89.213.

- Cross asset: Stocks remain weaker (SPX eminis -68.75 at 5980.75), Gold higher at 3437.00, Bbg US$ index +2.95 at 1202.97.

- Aside from geopolitical risks, markets await the next FOMC policy announcement next week Wednesday.

OVERNIGHT DATA

MNI US DATA: U.Mich Inflation Exp. Imply More Republican Responses

A correction to our earlier post on U.Mich inflation expectations when looking by political leaning: we hadn’t appreciated the series breakdown by democrat/independent/republican was on a three-month average. There still looks like there was a sizeable increase in the share of republican responses in this initial survey, but to less extent than we first thought.

- Median 1Y inflation expectations surprisingly fell to 5.1% (cons 6.4) in preliminary June results after 6.6% in May. However, a three-month average inched up from 6.03% to 6.07%.

- Against that, and as noted before, Bloomberg reports that democrats increased from 9.4% to 10.1%, independents from 7.2% to 7.5% and republicans from 1.0% to 1.5%. These are three-month averages, per the latest full “Data Booklet” that U.Mich published which was only up to April - pg 73 here: https://data.sca.isr.umich.edu/fetchdoc.php?docid=78603.

- Median 5-10Y inflation expectations meanwhile fell to 4.1% as expected after 4.2% in May, although the three-month average was unchanged at 4.23%. Again, democrats increased from 5.1% to 5.4%, independents from 4.7% to 4.9% and republicans from 1.9% to 2.2%.

MNI US DATA: U.Mich Inflation Expectations Seem To Be Affected By Weight Change

- The U.Mich consumer survey saw surprisingly low near-term inflation expectations in the preliminary June survey, at 5.1% (cons 6.4%) for 1Y out after 6.6% in May. The 5-10Y meanwhile was as expected at 4.1% after 4.2%.

- However, the details imply to us a notably heavier response from republican-leaning respondents, who have much lower inflation expectations under the Trump administration.

- According to data pulled in by Bloomberg, whilst the median 1Y expectations slipped from 6.6% to 5.1%, democrats increased from 9.4% to 10.1%, independents from 7.2% to 7.5% and republicans from 1.0% to 1.5%.

- 5-10Y overall figure dipped from 4.2% to 4.1%, but democrats increased from 5.1% to 5.4%, independents from 4.7% to 4.9% and republicans from 1.9% to 2.2%.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 787.94 points (-1.83%) at 42175.98

S&P E-Mini Future down 65.75 points (-1.09%) at 5982.25

Nasdaq down 231.3 points (-1.2%) at 19428.19

US 10-Yr yield is up 5.9 bps at 4.4185%

US Sep 10-Yr futures are down 14/32 at 110-20

EURUSD down 0.0046 (-0.4%) at 1.1538

USDJPY up 0.4 (0.28%) at 143.89

WTI Crude Oil (front-month) up $5.53 (8.13%) at $73.57

Gold is up $50.04 (1.48%) at $3436.19

European bourses closing levels:

EuroStoxx 50 down 70.35 points (-1.31%) at 5290.47

FTSE 100 down 34.29 points (-0.39%) at 8850.63

German DAX down 255.22 points (-1.07%) at 23516.23

French CAC 40 down 80.43 points (-1.04%) at 7684.68

US TREASURY FUTURES CLOSE

3M10Y +7.377, 5.436 (L: -8.878 / H: 7.494)

2Y10Y +1.314, 46.047 (L: 43.035 / H: 48.902)

2Y30Y +2.275, 95.208 (L: 91.239 / H: 96.397)

5Y30Y +1.812, 89.111 (L: 86.616 / H: 89.666)

Current futures levels:

Sep 2-Yr futures down 3.375/32 at 103-19.625 (L: 103-18.125 / H: 103-26.125)

Sep 5-Yr futures down 8/32 at 107-31.75 (L: 107-27.75 / H: 108-15.25)

Sep 10-Yr futures down 14/32 at 110-20 (L: 110-14 / H: 111-13)

Sep 30-Yr futures down 1-01/32 at 113-9 (L: 112-28 / H: 114-30)

Sep Ultra futures down 1-09/32 at 116-14 (L: 115-30 / H: 118-16)

MNI US 10YR FUTURE TECHS: (U5) Key S/T Resistance Remains Exposed

- RES 4: 111-30 76.4% retracement of the May 1 - 22 downleg

- RES 3: 111-20 1.0% 10-dma envelope

- RES 2: 111-14+ High Jun 5 & 61.8% of the May 1 - 22 downleg

- RES 1: 111-13 Intraday high

- PRICE: 110-01+ @ 11:08 BST Jun 13

- SUP 1: 110-17+/109-28 20-day EMA / Low Jun 6 / 11

- SUP 2: 109-12+ Low May 22 and the bear trigger

- SUP 3: 109-09+ Low Apr 11 and key support

- SUP 4: 108-25+ 0.764 proj of the Apr 7 - 11 - May 1 price swing

Treasury futures have traded to a fresh short-term high today, as the contract extends the recovery from the Jun 11 low. Attention is on key short-term resistance at 111-14+, a Fibonacci retracement and the Jun 5 high. Clearance of this hurdle would be bullish. On the downside, a reversal lower would refocus sights on 109-28, the Jun 6 / 11 low. A break of this level would be bearish and open the bear trigger, at 109-12+, May 22 low.

SOFR FUTURES CLOSE

Jun 25 -0.005 at 95.685

Sep 25 -0.015 at 95.905

Dec 25 -0.035 at 96.150

Mar 26 -0.050 at 96.355

Red Pack (Jun 26-Mar 27) -0.055 to -0.05

Green Pack (Jun 27-Mar 28) -0.055 to -0.045

Blue Pack (Jun 28-Mar 29) -0.045 to -0.04

Gold Pack (Jun 29-Mar 30) -0.045 to -0.04

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.28% (+0.00), volume: $2.663T

- Broad General Collateral Rate (BGCR): 4.27% (+0.00), volume: $1.098T

- Tri-Party General Collateral Rate (TCR): 4.27% (+0.00), volume: $1.062T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $114B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $290B

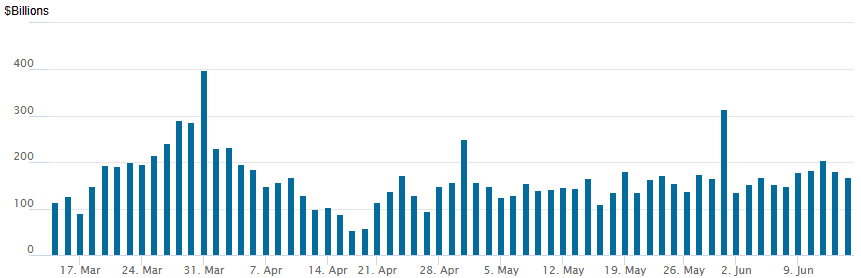

FED Reverse Repo Operation

RRP usage retreats to $168.645B this afternoon from $181.417B yesterday, total number of counterparties at 27. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

PIPELINE: Corporate Bond Roundup

No new corporate bond issuance Friday, $4.5b Priced Thursday, $22.8B total on week

- Date $MM Issuer (Priced *, Launch #)

- 06/12 $2B *Export Development Canada (EDC) 5Y SOFR+41

- 06/12 $1.5B *Analog Devices $850M 3Y +40, $650M 5Y +55

- 06/12 $1B *HA Sustainable $600m 5.5Y +225, $400m 10Y +245

MNI BONDS: EGBs-GILTS CASH CLOSE: Weaker On Geopolitics

European yields rose Friday, but still closed lower for the week.

- Geopolitical risk was the dominant theme, with Israel's strikes on Iran overnight seeing Bunds and Gilts rally strongly on Friday's open.

- But from there, yields would head higher: with Iran not immediately retaliating, oil prices retraced and equities found their footing.

- In a lighter session for data, the UK BoE/Ipsos survey showed inflation expectations didn't pick up further in May, but medium-term readings remain elevated. Final May HICP prints from Germany, France and Spain were unsurprising, and while April Eurozone industrial production was below-consensus, this comes after Q1 distortions.

- The German curve bear steepened, while the UK's leaned bear flatter. On the week, Bunds and Gilts closed stronger, with some modest bull flattening in both the German (2Y -2.4bp, 10Y -4.1bp) and UK (2Y -7.3bp, 10Y -9.4bp) curves.

- Periphery EGB spreads closed slightly wider, with BTPs underperforming.

- Next week's schedule is highlighted by the BOE decision Thursday, preceded by UK CPI Wednesday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4bps at 1.856%, 5-Yr is up 5.7bps at 2.136%, 10-Yr is up 5.7bps at 2.535%, and 30-Yr is up 5.5bps at 2.987%.

- UK: The 2-Yr yield is up 7.4bps at 3.94%, 5-Yr is up 7.9bps at 4.064%, 10-Yr is up 7.3bps at 4.55%, and 30-Yr is up 6.7bps at 5.26%.

- Italian BTP spread up 2.2bps at 94.9bps / French OAT up 1.3bps at 72.2bps

MNI FOREX: Israeli Strikes Can Only Provide So Much for Support For Dollar

- The USD Index rallied sharply on the back of the initial reports that Israel was pursuing broad military strikes against Iranian nuclear facilities, partially reversing a decent part of the week's trade-led weakness. EUR was among the hardest hit, prompting EUR/USD to post a near 150 pip fade off the cycle high at the Friday low.

- This price action soon reversed, however, as markets parsed the contained fallout for oil prices, production and supply from the Israeli strikes. As a result, the USD Index faded well, ensuring the definitive down-trendline resistance drawn off the early February high was never really under threat - a key theme that stays in focus headed into next week's Fed meeting.

- Looking ahead, any material escalation in geopolitical tensions could reignite risk-off. Iran's leadership have pledged a firm response to the Israeli strikes, and any action made toward US interests in the area could see increased ire from Trump - who has continued to press for a nuclear deal with Tehran. This continues to support front-end vols - with AUD, NZD seen among the most sensitive across early Friday trade.

- Sizeable options influence could play a part in spot vol in the coming few sessions - next week sees a major strike rolling off on Monday in USD/JPY at Y145.00: $4.9bln, as well as E4.6bln in EUR/USD at $1.1700.

- Central banks are of more interest next week, with both the BoJ, BoE and Fed rate decisions all due. No change is expected at any of the three meetings, however their views on policy further down the line - particularly into year-end, will be carefully watched.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 16/06/2025 | 0800/1000 | *** | HICP (f) | |

| 16/06/2025 | 1030/1230 | ECB Cipollone At Osservatorio Banca Impresa 2030 Meeting | ||

| 16/06/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/06/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 16/06/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 16/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 16/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 16/06/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 16/06/2025 | - | FOMC Meetings with S.E.P. | ||

| 17/06/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement |