MNI ASIA OPEN: Flash PMIs Beat, Megabill Passes House

EXECUTIVE SUMMARY

- MNI FED: Powell To Deliver Semi-Annual Testimony Jun 24

- MNI FED: NY Fed's Williams: "Optimal" Level Of Reserves Is Case-Dependent

- MNI US DATA: Very Mild Trend Rise In Jobless Claims Continues

- MNI US DATA: Existing Home Sales Disappoint, Highest Relative Supply Since 2016

- MNI US DATA: Flash PMIs Surprise Stronger For Both Mfg And Services In May

US

MNI FED: Powell To Deliver Semi-Annual Testimony Jun 24

Fed Chair Powell is scheduled to deliver Semi-Annual Monetary Policy testimony before the House Financial Services Committee on Tuesday June 24 at 1000ET. Based on previous testimonies, this likely means the Semi-Annual Monetary Policy Report prepared by the Fed will be released on Friday Jun 20, with the hearing before the U.S. Senate Committee on Banking, Housing, and Urban Affairs likely on Wednesday June 25.

- The House appearance will be is less than a week after the June FOMC decision / press conference / quarterly projections on June 18, so it's unclear whether we will get any new revelations from Powell in Congress that haven't already been covered, but we wouldn't be surprised to see Powell pressed relatively more aggressively by congressional representatives on fiscal issues.

MNI FED: NY Fed's Williams: "Optimal" Level Of Reserves Is Case-Dependent

There are multiple factors that should be weighed in considering the "optimal" level of bank reserves, NY Fed President Williams said in a speech at a monetary policy implementation event this afternoon (link). There's little new here and Williams was speaking in the abstract, as in, not directly addressing the Fed's balance sheet policy (the audience includes international central bank attendees), but with the Fed having eased up on QT in March and aiming to bring reserves down to "ample" from the currently "abundant", Williams's comments (and those due later from current SOMA head Perli) are worth noting.

NEWS

MNI SECURITY: Thune Says Senate "Stands Ready To Act" With New Russia Sanctions

Senate Majority Leader John Thune (R-SD) told reporters that “the Senate stands ready to act,” with new sanctions on Russia if President Vladimir Putin refuses to negotiate in good faith, according to Andrew Desiderio at Punchbowl News. Desiderio notes that Thune pitched the sanctions bill, introduced by Senators Lindsay Graham (R-SC) and Richard Rosenthal (D-CT), "amid pressure from Republicans", but "didn’t put a timetable on it".

MNI US: House Passes GOP Megabill In Major Win For Speaker Johnson And Trump

The House of Representatives has passed the GOP tax and spending bill in a 215-214 vote, with two Republicans voting 'no'. The bill’s passage is a major win for House Speaker Mike Johnson (R-LA) and President Donald Trump, who have consistently outperformed expectations in Congress. The new revised ‘Big Beautiful Bill’ includes a raft of sweeteners for conservatives. It accelerates work requirements for Medicaid, kicking them in at the end of 2026, rather than the start of 2029.

- The revised bill sharpens language on Biden-era Inflation Reduction Act clean energy credits. While it doesn’t rescind the credits entirely, it cuts them off sooner and makes then more difficult to attain. It also softens the rollback of credits for advanced nuclear reactors – a win for the nuclear sector.

US TSYS

MNI US TSYS: At/Near Late Session Highs, Curves Mixed After Bond Bounce

- Unwinding early weakness, Treasuries futures look to finish at/near session highs - trading sideways since midday. Rates opened weaker after the House has passed revised tax/spending bill. Jun'25 10Y futures currently trade +13.5 at 109-29.5, 109-26 high. Key near-term resistance has been defined at 110-21+, the May 16 high. A move above this level is required to signal a potential reversal.

- The revised bill sharpens language on Biden-era Inflation Reduction Act clean energy credits. While it doesn’t rescind the credits entirely, it cuts them off sooner and makes then more difficult to attain. It also softens the rollback of credits for advanced nuclear reactors – a win for the nuclear sector.

- Intermediate to long end Treasury futures remain under pressure after slightly lower than expected weekly claims, Continuing Claims higher than expected though prior is down-revised. Rates remained under pressure after S&P flash PMIs come out higher than expected.

- Manufacturing: 52.3 (cons 49.9, 20 responses) in the May prelim after 50.2 in April – highest since Feb and before that Jun 2022. Services: 52.3 (cons 51.0, 16 responses) in the May prelim after 50.8 in April – highest since March.

- That said, there were no obvious headline or block driver as Treasury futures extend session highs around midday, curves turned mixed, off steeper levels as bonds rebound: 2s10s -3.235 at 54.466, 5s30s +1.942 at 94.934.

- Cross asset: BBG UD$ index off highs (BBDXY +1.86 at 1220.70 vs. 1222.36)., Gold declines to 3293.15, Stocks mixed, SPX eminis little firmer at 5874.0 (+12.75).

OVERNIGHT DATA

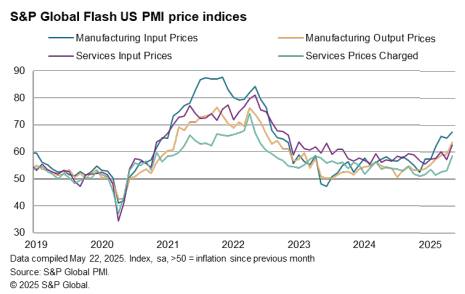

MNI US DATA: Flash PMIs Surprise Stronger For Both Mfg And Services In May

The S&P Global US flash PMIs for May were comfortably stronger than expected for both manufacturing and services, as they better reflected the de-escalation in US-China trade policies on May 12 compared to other surveys already seen for May. We had flagged as such beforehand. Output price inflation for goods & services inflation reached its highest since Aug 2022 whilst, interestingly, mfg inventory showed its largest jump on record which suggests the strong contribution to Q1 GDP growth might not reverse as soon as expected in Q2.

- Manufacturing: 52.3 (cons 49.9, 20 responses) in the May prelim after 50.2 in April – highest since Feb and before that Jun 2022.

- Services: 52.3 (cons 51.0, 16 responses) in the May prelim after 50.8 in April – highest since March.

- Composite: 52.1 (cons 50.3, 5 responses) in the May prelim after 50.6 in April – highest since March.

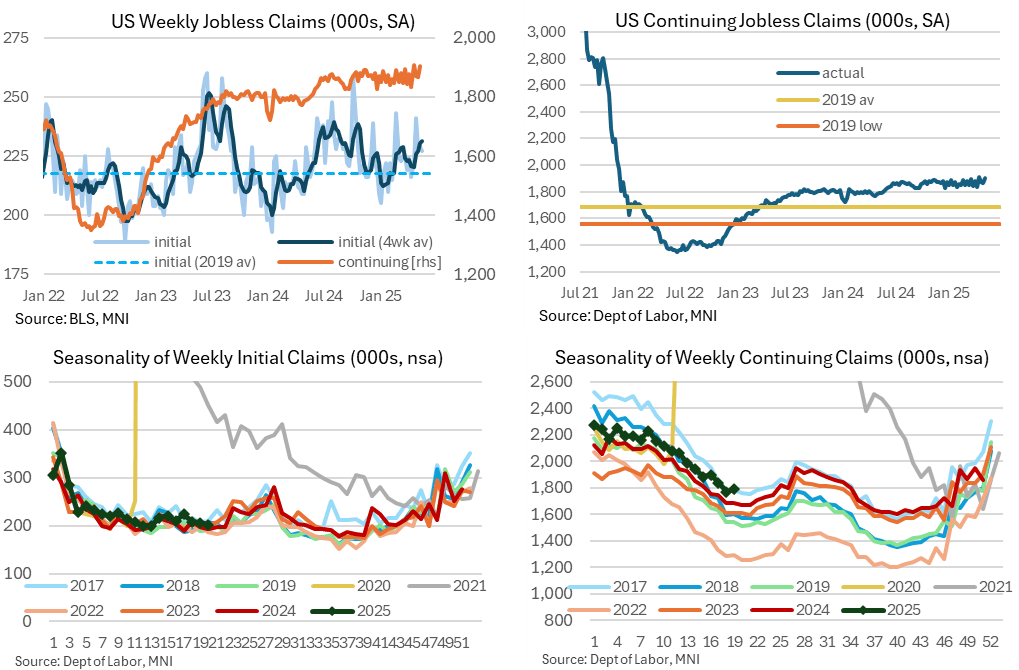

MNI US DATA: Very Mild Trend Rise In Jobless Claims Continues

Weekly jobless claims data show some trend softening in labor market conditions but it’s at a slow pace and for now continues to point to a low firing, low hiring environment. Initial jobless claims: 227k (sa, cons 230k) in the week to May 17 – a payrolls reference period – after an unrevised 229k in the week prior. Continuing claims: 1903k (sa, cons 1882k) in the week to May 10 after a downward revised 1867k (initial 1881k).

- The surprise pop higher reverses two weeks of improvement seen since breaking above the 1900k level for a fresh 3+ year high back in the week to Apr 19.

- The non-seasonally adjusted data meanwhile show initial claims within typical narrow ranges for the time year whilst continuing claims are right at the top of readings in “normal” years for the time of year (as has been the case for the past month in the latter).

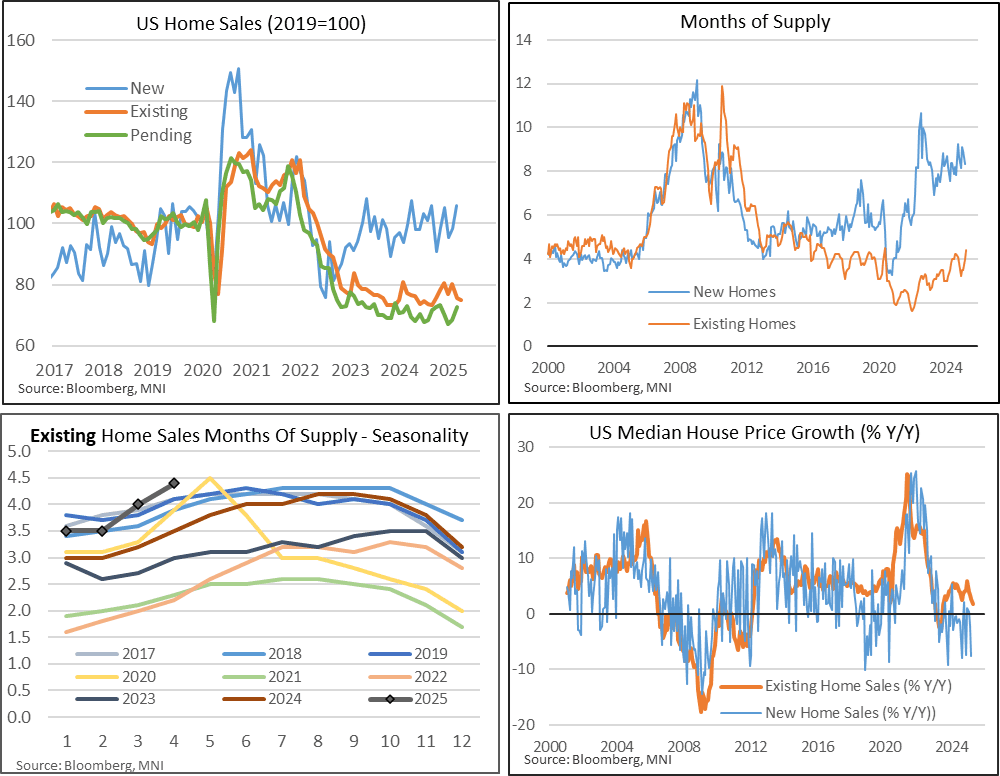

MNI US DATA: Existing Home Sales Disappoint, Highest Relative Supply Since 2016

Existing home sales bely prior pick-up in pending home sales, chalking up the lowest April since 2009. With inventories also rising, the relative supply of 4.4 months was the highest for an April since 2016. Existing home sales disappointed in April at 4.00m (cons 4.10m) after 4.02m, for the lowest seasonally adjusted annualized level since Sep 2024.

- It left a -0.5% M/M decline after the heavy -5.9% in March, confounding expectations of at least some improvement after pending home sales had increased 6.1% M/M in March after 2.1% in Feb following a weak turn of the year. It’s a weak April release though, with the lowest non-seasonally adjusted level of sales for an April since 2009.

MNI CANADA DATA: Apr Industrial Prices +2% YOY On Gold, Seventh Straight Increase

- Canada's April Industrial Product Price Index +2% YOY, seventh straight increase driven by gold, silver and aluminum. Gasoline was a key moderator of gains due to a base effect amid rising crude prices.

- IPPI dropped for the first time after six straight monthly gains, -0.8% MOM in April. The decline was partly due to CAD-USD changes and was led by lower energy and oil prices.

- Influence of U.S. tariffs seen in some monthly industrial price declines: "Prices for softwood lumber (-11.1%) posted their largest month-over-month decrease since June 2022 (-29.4%) and were the main driver for the monthly decline in April 2025. Many buyers decided not to increase their inventory due to potential tariffs" StatsCan said. “Prices for motorized and recreational vehicles fell 0.9% on a monthly basis in April, posting their largest monthly decline since June 2020 (-1.2%).”

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 1.29 points (0%) at 41859.15

S&P E-Mini Future down 0.75 points (-0.01%) at 5860

Nasdaq up 53.1 points (0.3%) at 18925.73

US 10-Yr yield is down 6.2 bps at 4.5367%

US Jun 10-Yr futures are up 12.5/32 at 109-28.5

EURUSD down 0.0052 (-0.46%) at 1.1279

USDJPY up 0.33 (0.23%) at 144.01

Gold is down $24.78 (-0.75%) at $3290.21

European bourses closing levels:

EuroStoxx 50 down 29.98 points (-0.55%) at 5424.48

FTSE 100 down 47.2 points (-0.54%) at 8739.26

German DAX down 123.23 points (-0.51%) at 23999.17

French CAC 40 down 46.05 points (-0.58%) at 7864.44

US TREASURY FUTURES CLOSE

3M10Y -6.453, 18.595 (L: 17.866 / H: 27.714)

2Y10Y -3.261, 54.44 (L: 54.202 / H: 62.696)

2Y30Y -1.507, 105.57 (L: 105.039 / H: 116.003)

5Y30Y +1.975, 94.967 (L: 93.281 / H: 100.889)

Current futures levels:

Jun 2-Yr futures up 1.125/32 at 103-10 (L: 103-08.375 / H: 103-11.25)

Jun 5-Yr futures up 7.25/32 at 107-18.75 (L: 107-10 / H: 107-19.75)

Jun 10-Yr futures up 13/32 at 109-29 (L: 109-13 / H: 109-30)

Jun 30-Yr futures up 17/32 at 111-10 (L: 110-01 / H: 111-14)

Jun Ultra futures up 19/32 at 114-1 (L: 112-09 / H: 114-05)

MNI US 10YR FUTURE TECHS: (M5) Bear Cycle Extension

- RES 4: 112-20+ High May 1 and a bull trigger

- RES 3: 112-01+ High May 2

- RES 2: 111-22 High May 7 and a key near-term resistance

- RES 1: 110-21+ High May 16

- PRICE: 109-26 @ 12:35 ET May 22

- SUP 1: 109-13 Intraday low

- SUP 2: 109-08 Low Apr 11 and key support

- SUP 3: 108-26+ 76.4% retracement of the Jan 13 - Apr 7 bull cycle

- SUP 4: 108-21 Low Feb 19

Treasury futures traded lower Wednesday extending the bear cycle that started early May. The recent breach of 110-01+, 76.4% of the Apr 11 - May 1 bull leg, strengthened a bearish theme and has exposed key support at 109-08, the Apr 24 low and a bear trigger. Key near-term resistance has been defined at 110-21+, the May 16 high. A move above this level is required to signal a potential reversal.

SOFR FUTURES CLOSE

Jun 25 steady00 at 95.683

Sep 25 -0.005 at 95.895

Dec 25 +0.005 at 96.170

Mar 26 +0.010 at 96.380

Red Pack (Jun 26-Mar 27) +0.020 to +0.050

Green Pack (Jun 27-Mar 28) +0.050 to +0.055

Blue Pack (Jun 28-Mar 29) +0.055 to +0.065

Gold Pack (Jun 29-Mar 30) +0.070 to +0.075

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.26% (-0.01), volume: $2.517T

- Broad General Collateral Rate (BGCR): 4.26% (+0.00), volume: $1.043T

- Tri-Party General Collateral Rate (TCR): 4.26% (+0.00), volume: $1.013T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $300B

FED Reverse Repo Operation

RRP usage inches up to $173.018B this afternoon from $162.082B yesterday, total number of counterparties at 37. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

MNI PIPELINE: Corporate Bond Update: $1.25B SEB 2Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 05/22 $1.25B #SEB (Skandinaviska Enskilda Banken) $750M 3Y +50, $500M 3Y SOFR+75

- 05/22 $1B *Finnvera WNG 5Y SOFR+50

- 05/22 $Benchmark Telecom Argentina 8Y 9.5%a

MNI BONDS: EGBs-GILTS CASH CLOSE: Countervailing Factors See Twist Steepening

Long-end European bonds remained under pressure Thursday, though yields closed near session lows.

- After gapping higher at the open, yields traded mixed across the curve through the rest of the day. Short-end instruments rallied consistently, with long-end (particularly 30Y) Gilts and Bunds seeing the weakest levels in early afternoon before staging a partial recovery.

- Multiple factors were at play. The short end benefited from dovish ECB repricing after weak flash eurozone Services PMIs.

- Eurozone and UK curves twist steepened however, with longer-dated global yields remaining underpinned by US fiscal concerns as expansive fiscal legislation moved closer to fruition in Washington.

- The twist steepening held by session's cash close in both Germany and the UK, though yields finished near the lows and futures continued to rally after the close.

- The ECB's April meeting accounts noted that "it was argued that the optimal monetary policy response depended on the outcome of tariff negotiations".

- Periphery/semi-core EGB spreads mostly widened in a mixed day for risk assets.

- Friday's calendar highlight is UK retail sales, while we also get German GDP data and French consumer confidence, as well as ana appearance by ECB's Lane.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 4bps at 1.831%, 5-Yr is down 2.1bps at 2.172%, 10-Yr is down 0.3bps at 2.643%, and 30-Yr is up 1.5bps at 3.151%.

- UK: The 2-Yr yield is down 5.2bps at 4.031%, 5-Yr is down 4bps at 4.201%, 10-Yr is down 0.6bps at 4.751%, and 30-Yr is up 3.2bps at 5.55%.

- Italian BTP spread up 1.3bps at 100.9bps / French OAT up 1.3bps at 68bps

MNI FOREX: USD Trades with Constructive Tone, JPY Volatility Stands Out

- The US Dollar has traded on a firmer footing Thursday, with the USD index currently up around 0.55% as we approach the APAC crossover. This theme has been underpinned by a more stable session for treasuries, where yields have had a strong reversal lower from the week’s highest levels. Nominal 30Y yields are down 9-10bp from highs, having rejected the 2023 peak around 5.15% for now.

- The most notable moves in G10 FX were once again dominated by the volatile Japanese yen, which remains sensitive to both domestic headlines and the prevailing sentiment surrounding US assets. USDJPY received an early session boost to 144.40 on headlines related to the meeting between US Tsy Secretary Bessent and Japan FinMin Kato where they discussed a shared belief that exchange rates should be market determined.

- However, this sentiment was quickly faded, and subsequent headlines from BOJ’s Noguchi on not intervening in JGB bond markets and the initial twist steepening of the treasury curve prompted an impressive USDJPY selloff to session lows of 142.81. In another impressive swing, the subsequent flattening of the US curve and late comments on no secret talks on fx policy from Miran extended a relief recovery back towards session highs.

- Separately, EUR weakness has stood out following weaker-than-expected German and Eurozone flash services PMIs. Price action has been uninspiring, however, EURUSD is down 0.5% on Thursday, with spot gravitating towards the 1.1265 mark, but still up over a big figure on the week. Single currency weakness also stands out against sterling, as EURGBP has also fallen around half a percent to trade below 0.8400 and close in on last week’s pullback lows located at 0.8394. GBPUSD has broadly respected a 1.3400-50 range, outperforming the likes of AUD and NZD which have adjusted lower in tandem with the broader greenback strength.

- New Zealand retail sales and Japan national CPI data are due in Friday’s APAC session. This will be followed by UK and Canadian retail sales, with US new home sales highlighting the US docket.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 23/05/2025 | 0600/0800 | ** | Unemployment | |

| 23/05/2025 | 0600/0700 | *** | Retail Sales | |

| 23/05/2025 | 0600/0800 | *** | GDP (f) | |

| 23/05/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 23/05/2025 | 0830/1030 | ECB's Lane Inflation Lecture in Florence | ||

| 23/05/2025 | 1230/0830 | * | Quarterly financial statistics for enterprises | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1335/0935 | Kansas City Fed's Jeff Schmid | ||

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1600/1800 | ECB's Schnabel Speech on Financial Education and Monpol | ||

| 23/05/2025 | 1600/1200 | Fed Governor Lisa Cook | ||

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |