US DATA: Flash PMIs Surprise Stronger For Both Mfg And Services In May

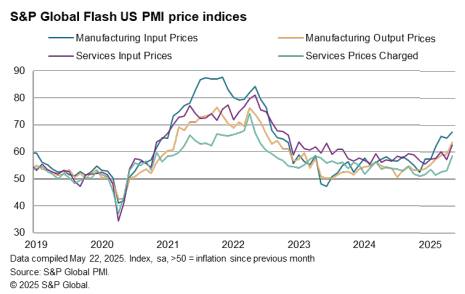

The S&P Global US flash PMIs for May were comfortably stronger than expected for both manufacturing and services, as they better reflected the de-escalation in US-China trade policies on May 12 compared to other surveys already seen for May. We had flagged as such beforehand. Output price inflation for goods & services inflation reached its highest since Aug 2022 whilst, interestingly, mfg inventory showed its largest jump on record which suggests the strong contribution to Q1 GDP growth might not reverse as soon as expected in Q2.

- Manufacturing: 52.3 (cons 49.9, 20 responses) in the May prelim after 50.2 in April – highest since Feb and before that Jun 2022.

- Services: 52.3 (cons 51.0, 16 responses) in the May prelim after 50.8 in April – highest since March.

- Composite: 52.1 (cons 50.3, 5 responses) in the May prelim after 50.6 in April – highest since March.

Press release highlights:

- "US business activity growth and expectations for future output improved from lows seen in April, according to flash PMI® survey data for May. However, they both remained historically subdued amid ongoing concerns over the detrimental impact of tariffs on demand, supply chains, and prices.

- Export orders continued to fall, dropping especially sharply for services, supply chain delays intensified, and prices charged for goods and services surged to an extent not seen since August 2022, overwhelming linked to tariffs.

- Manufacturing input inventory holdings meanwhile showed the largest jump on record as firms sought to safeguard against further tariff related issues."

- Data were collected 12-21 May

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Cleveland Fed On Extent Of Passing On Of Tariff Cost Anticipation

The Cleveland Fed doesn’t produce a business activity index like some regional Feds do but it has published some tariff-focused questions it asked respondents in its District through Feb 6-13 (see in full here). Whilst this predates the significant escalation in tariff announcements since Apr 2, almost half of those affected were already passing anticipated cost increases on. There were however suggestions of it continuing to become harder to pass these cost increases on.

- 64% of respondents saw tariffs impacting their business, with 24% unsure and 12% seeing no impact.

- The highest shares expecting an impact were retail (82%), mfg (75%), construction (70%) whilst professional and business services were the least likely to be impacted (21% yes vs 36% no).

- Of those expecting an impact, 85% expected an increase in input costs vs 75% expecting an increase in selling prices.

- That question doesn’t offer magnitudes but there are hints elsewhere at the continued reduction in pricing power noted in multiple editions of the Fed’s Beige Book (to be updated tomorrow) and most recently today’s Philly Fed non-manufacturing survey. Specifically, whilst 38% see no change in their ability to pass on price increases compared to one year ago, 36% find it “somewhat harder” and 12% “significantly harder” vs 13% somewhat and 1% much easier.

- This tallies with 60% of respondents expecting demand to decrease (31% saw no change, 9% an increase) and 22% expecting employment to decline (75% no change, 3% increase).

- That said, 46% of respondents were already passing anticipated cost increases through to customers (in answer to "What actions, if any, are you taking in anticipation of tariffs on imports?”). Also of note considering the Trump administration's plan to boost domestic production, 29% suggested they were finding new domestic suppliers but just 4% anticipated bringing outsourced production or processes in house.

GILTS: Sell Off On IMF Headlines Quickly Fades, Steepening Intact

Gilt futures have regained around 30 of the ~40-tick sell off seen at the turn of the hour.

- The move lower in futures came as the IMF downgraded their economic growth outlook for the UK, which, when coupled with the already fragile fiscal backdrop and thinner-than-usual liquidity, weighed on gilts.

- This serves as a reminder of UK market sensitivity to headlines pointing to a deepening of the well-documented fiscal issues, which stem from limited fiscal headroom and tepid economic growth.

- Still, the prospect of deeper rate cuts from the BoE provides some insulation, meaning the contract stopped short of testing previous session lows.

- Spill over from a bounce in Tsys had seen futures trade as high as 92.56 ahead of the headlines, although initial resistance at 92.63 remains untouched.

- Curve steepening theme remains intact, with yields 6bp lower to 2bp higher on the day.

EQUITIES: Program buyer on the Cash Open

- Decent program buyer on the Cash Open with 2006 names, the most since the 9th April.

- The early bids on the Equity Cash Open are met by sellers, and SPX is still short of Yesterday's high of 5232.94, now trading at 5222.62.