MNI ASIA OPEN: Fed Reinforces Message Of Patience

MNI (NEW YORK) -

EXECUTIVE SUMMARY

- MNI: Fed Well-Placed To Assess Tariff Effects- May Minutes

- MNI BRIEF: Fed Nods To Shift To Flexible Inflation Target

- MNI: Households' View Of Economy Improved In 2024 - Fed Survey

- US DATA: Regional Fed Surveys Point To More Stable Activity In May

- MNI INTERVIEW: Alberta Pipeline Dream Hurt By Separation Talk

US TSYS: Modestly Weaker Having Held Key Round Levels

Cash Treasuries weakened Wednesday after three flat/positive sessions, with some light bear steepening in the cash curve.

- Treasury-negative headlines/macro developments were actually limited (a long-end Japanese bond auction went softly overnight), with yields moving lower in early trade before pushing sharply higher in late morning.

- At that point Tsys, found a bid as 30Ys touched 5.00% with 10Ys just under 4.50%. Overall, trade was mostly within Wednesday's ranges.

- The session featured a very solid 5Y Note auction, which saw a 0.4bp trade-through and a record-high takedown for 5s by indirect bidders (and one of the lowest-ever primary dealer takeups), helping yields consolidate into the close.

- The May FOMC meeting minutes cast a lightly hawkish tone in MNI's view, with little to no emphasis on the possibility of tariff-driven inflation proving to be a one-off shock. However the accounts were seen as relatively stale given developments in the last 3 weeks, and met with limited market reaction.

- In data, regional Fed surveys (Dallas services, Richmond manufacturing and services) were mixed but generally saw some stabilization in May, while Redbook retail sales continued to indicate resilient consumer activity into late May.

- Latest cash levels: 2-Yr yield is up 0.9bps at 3.9901%, 5-Yr is up 3bps at 4.0635%, 10-Yr is up 3.2bps at 4.4753%, and 30-Yr is up 2.1bps at 4.9717%.

- Note that with the Jun/Sep futures roll all but complete (all contracts 90+% through), September becomes the front contract.

- Thursday's schedule includes the 2nd reading of Q1 GDP alongside weekly jobless claims, with appearances by Fed's Barkin, Goolsbee. Kugler, Logan, and Daly.

NEWS

MNI: Fed Well-Placed To Assess Tariff Effects- May Minutes

Federal Reserve officials believe they can take their time in assessing the effects of fluid tariff policies, though they fear larger-than-expected tariffs will raise inflation and hurt employment, according to minutes of their May meeting released Wednesday. The FOMC said it is "well positioned to wait for more clarity on the outlooks for inflation and economic activity." Increased uncertainty about the outlook makes it "appropriate to take a cautious approach until the net economic effects of the array of changes to government policies become clearer," the minutes said.

FED: MNI BRIEF: Fed Nods To Shift To Flexible Inflation Target

Federal Reserve officials say the benefits of the 2020 shift to a flexible average inflation targeting framework have diminished and are looking at a strategy of flexible inflation targeting, according to minutes of the May Fed meeting released Wednesday. "Participants" said the strategy of flexible average inflation targeting has "diminished benefits in an environment with a substantial risk of large inflationary shocks or when ELB risks are less prominent," the minutes said. "Participants indicated that they thought it would be appropriate to reconsider the average inflation-targeting language in the Statement on Longer-Run Goals and Monetary Policy Strategy."

FED: MNI: Households' View Of Economy Improved In 2024 - Fed Survey

Inflation and prices continued to be the top financial concern among American households whose perceptions of their local and national economies continued to improve at the end of 2024, with a sizeable share of adults saying their family’s monthly income increased compared to the year before, the Federal Reserve reported Wednesday. In an annual survey, the Fed said 73% of adults reported “doing okay” financially (39%) or “living comfortably” (34%). The share who said they were better off rose 3 percentage points to 23%. Twenty-nine percent of adults said they were worse off financially than a year earlier, continuing to fall from the series high of 35% in 2022, yet still well above the levels seen in prior years.

FED/MNI: INVITE:Livestream MNI Connect VC with Fed Mary Daly On July 10

You are invited to listen to a Livestreamed MNI Connect Video Conference with the San Francisco Fed President Mary Daly. Details below:

- Mary Daly joins us to discuss the ‘The US Economic Outlook and Challenges for Policymakers'

- DATE: Thursday, 10 July 2025

- TIME: 2:30 pm - 4 pm ET; 11:30am - 1pm PT; 7:30pm - 9pm London

- This event will be run as a Zoom Webinar and is a public, on-the-record event.

- To register please go to: MNI Webcast Registration

US: MNI/POLITICO: White House To Send Congress 'Small Package' Of DOGE Cuts - Politico

Politico reports that the White House is expected to send a “small package” of DOGE cuts for Congress to codify as soon as next week. See previous bullet: US: Johnson Promises To Codify DOGE Cuts After Musk Pans "Big Beautiful Bill". The package of cuts, known as rescissions, could test the water for a larger package of spending cuts down the line as the White House and Republican leadership in Congress look to get fiscal hawks on board with the ‘One Big Beautiful’ tax and spending bill that passed the House last week.

CANADA: MNI INTERVIEW: Alberta Pipeline Dream Hurt By Separation Talk

Alberta’s talk of separating from Canada endangers planned new energy pipelines, a former deputy prime minister who represented that province told MNI, adding that potential investors in the province are already backing away. “This discussion is singularly unhelpful and for both the province of Alberta and for the country," said Anne McLellan, who has also served as Canada's natural resources minister. "The last thing you want to do is put in play issues that could potentially stand in the way of attracting foreign investment.”

EUROPE: MNI BRIEF: EC Plan To Boost High-Tech Startup Sectors

The European Commission has launched its new "Scaleup and Startup" strategy to turn Europe into a global powerhouse for the launch and development of global technology-driven companies in the EU, aiming to prevent the bloc falling even further behind the US and China in cutting-edge sectors, like AI, quantum computing and advanced microchips.

OVERNIGHT DATA

US DATA: Richmond Fed Surveys Point To Slightly Better Activity In May (1/2)

The Richmond Fed's regional manufacturing and services surveys for May showed improved activity, as expected - but remained in negative territory.

- Unlike some other regional Fed reports, there is limited anecdotal "evidence" or commentary for what is driving these survey results, but the figures are consistent with other "soft" data that the worst of the tariff fears may have subsided but sentiment remains weak.

- Further obscuring the read-through is the survey dates, which (based on the survey methodology) will have been conducted between April 24 and May 21, so it straddles both sides of the US-China trade war climbdown on May 12.

- The headline manufacturing composite index rose to -9 (in line with consensus) from -13, improving after two large monthly declines. The three components of the composite ticked higher: new orders ticked only slightly higher, to -14 from -15, shipments to -10 from -17, and employment to -2 from -5. Expectations, while still (unusually) negative for the 3rd consecutive month, saw a drastic improvement, rising 31 points to -6.

- The services readings similarly largely improved in some aspects but were still weak. The local business conditions index jumped 12 points to -18 (no consensus), with the 6-month outlook up 11 points to -18.

- Both marked the 3rd consecutive negative reading, and the report notes that regional service sector activity overall slowed in May, with the revenues index falling 4 points to -11, and employment fell 8 points to 0 (albeit demand, and expected future employment, revenues and demand, rose).

US DATA: Richmond Fed Regional Price Pressures Remained Elevated In May (2/2)

The Richmond Fed's May business surveys showed no discernable change in heightened inflation dynamics seen in prior months.

- In manufacturing, current prices paid were unchanged vs April at 5.4% (all prices are expressed as reported price changes versus 12 months earlier), with prices received 2.7% (compare these to 2.4% / 1.2%, respectively, at the start of 2025). Inflation expectations (expected price change in next 12 months) dipped by 1ppt (prices paid to 7.0%, received 5.0%) but were still very high (4.0%/3.0% respectively at the start of 2025).

- Similarly for services, current prices received was unchanged at 3.0%, with prices paid up 0.1pp to 5.0% (3.6% and 4.7% at the start of 2025). Expectations were mixed, potentially suggestive of tougher margin pressures: expected 12M prices paid ticked up to 6.0% from 5.9%, with received down to 3.6% from 4.2% (respectively these were 4.1% / 3.6% at the start of 2025).

- Overall price pressures looked elevated in the region, though look short of the heights of the pandemic supply chain/reopening price pressures. And again, the survey was conducted on both sides of various tariff developments, most notably May 12's US-China truce, so June's survey may provide a more relevant snapshot.

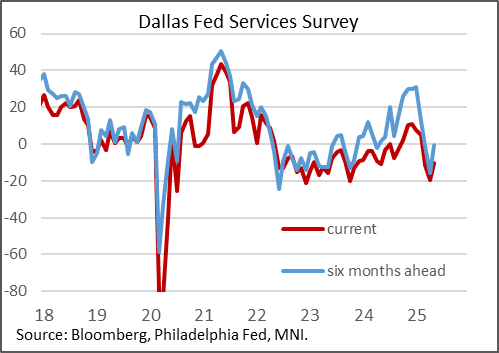

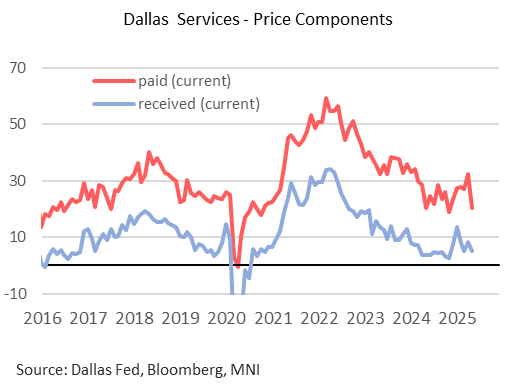

US DATA: May Dallas Fed Services Activity Shows Stabilization, Weak Retail Sales

May's Texas Service Sector Outlook Survey conducted by the Dallas Fed implied a contraction in activity in the region, albeit at a less negative pace than earlier in the year. Retail sales were a surprisingly negative category amid the overall stabilization.

- The general business activity index rose to -10.1 (from -19.4 prior), while the 6-month outlook up to -0.3 from -16.0. Both were the strongest readings since February, though that contrasts with positive readings in late 2024.

- There's evidence that tariff-related developments (most notably the May 12 announcement that the US and China would hold off on punitive levies for the time being - the survey was conducted May 13-21) saw a sharp drop in the outlook uncertainty index, to 18.7 from 40.5. Various other subcategories readings were little changed, including employment.

- However, there were signs of weakness in other key categories. The revenue index, "a key measure of state service sector conditions" per the Dallas Fed report, fell 9 points to -4.7, "suggesting revenue contracted slightly" (albeit future revenue/employment/capex expectations were positive).

- And the retail sales reading (which is a subsection of the overall service sector survey) showed a sharp contraction in activity, dropping 33 points to -30.5, weakest since April 2020, with much more mixed forward expectations than seen in the broader survey.

- Inflationary pressures appeared to abate sharply. Current prices paid pulled back toa 6-month low 20.5 (32.5 prior), with received reversing April's rise to dip to 5.2 (8.4 prior).

US DATA: Redbook Retail Sales Remain Solid Through Late May

The Johnson Redbook retail sales index showed continued robust growth into the Memorial Day weekend, rising 6.1% Y/Y in the week ending May 24 (Saturday), up from 5.4% the prior week.

- For May so far, sales are up 5.8% Y/Y (vs retailers' targeted 5.4%, and the month-to-date growth of 5.6% as of the prior week).

- There was no mention of tariffs and little sign of consumer pessimism in the report: "Memorial Day promotions helped to drive demand for a wide variety of summer and picnic products and seasonal apparel, which were the main focus for most consumers. Seasonal merchandise sold well in regions experiencing warm temperatures. Department stores noted increased activity in items related to school graduation, including women's wear, men's wear, footwear, and women's accessories. Additionally, discounters reported strong business in the grocery division in anticipation of the long Memorial Day weekend."

- Redbook sales have risen 5+% in 3 consecutive months, so this would mark the 4th month in a row - while that hasn't directly translated into the "official" retail series, it it does accounts for 80% Census Bureau sales, suggesting the latter looks to remain relatively robust in May (that data is only out on June 17).

US DATA: Composite MBA Applications Dip As Swap Spread Re-Widens A Touch

- MBA composite mortgage applications dipped -1.2% last week (sa) after a heavier -5.1% the week prior.

- The breakdown was more mixed than usual, with new purchase applications rising 2.7% after -5.2% whilst refis saw further weakness with -7.1% after -5.0%.

- Relative levels: composite at 50% of 2019 average levels, new purchases at 63% and refis at 37%.

- The 30Y confirming mortgage rate increased 6bps to 6.98% as it started to reflect what has been a sharper climb in 10Y swap rates although one that fizzled out last week with no change in average rates for the latter.

- It saw the confirming rate to swap spread rise 6bps to 302bps having tightened 19bps from 3.15% to 2.96% in the first half of May.

US 10YR FUTURE TECHS: (U5) Bear Cycle Remains In Play

- RES 4: 112-04+ High May 2

- RES 3: 111-25 High May 7

- RES 2: 111-05+ High May 9

- RES 1: 110-21+/23 50-day EMA / High May 16 and a key resistance

- PRICE: 110-05+ @ 11:20 BST May 28

- SUP 1: 109-12+ Low May 22

- SUP 2: 109-09+ Low Apr 11 and key support

- SUP 3: 109-00 Round number support

- SUP 4: 108-25+ 0.764 proj of the Apr 7 - 11 - May 1 price swing

A bear cycle in Treasury futures remains in play for now, and short-term gains are considered corrective. The recent breach of 110-03+, 76.4% of the Apr 11 - May 1 bull leg, strengthened a bearish theme and has exposed key support at 109-09+, the Apr 11 low and a bear trigger. Key near-term resistance has been defined at 110-23, the May 16 high. A clear break of this level is required to signal a potential reversal.

US TSYS/OVERNIGHT REPO: SOFR Jumps Post-Holiday, With Month-End Yet To Come

Secured rates saw a large jump Tuesday versus last week's unusually soft levels, with SOFR up 5bp (vs Friday, after Monday's holiday) to 4.31%. That brings SOFR back to levels last seen on May 15. Elsewhere, GCF Treasury Repo printed 4.38%, up 8bp and the highest since May 2.

- As we noted Tuesday, downward pressures on secured rates last week exerted in part by temporary GSE cash in the system was due to dissipate this week, and upside pressures are likely to persist toward week-end exacerbated by Friday's month-end dynamics.

- Other factors to watch include Friday's $46B in net new cash raised via coupon auction settlements (upward rate pressure), while Thursday's rates could be temporarily subdued in the meantime by $29B in net bill paydown (downward rate pressure).

- Effective Fed funds was as usual unchanged Tuesday (4.33%).

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.31%, 0.05%, $2655B

* Broad General Collateral Rate (BGCR): 4.30%, 0.04%, $1061B

* Tri-Party General Collateral Rate (TGCR): 4.30%, 0.04%, $1025B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $115B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $293B

US TSYS/OVERNIGHT REPO: RRP Takeup Jumps, Further Rises Expected To Be Limited

Takeup of the Fed's overnight reverse repo facility jumped Wednesday, rising $35.6B to $173.6B, the second-highest total of the month ($180.4B May 19).

- ON RRP takeup has been somewhat erratic the last few sessions, though it's not expected to rise much past Wednesday's levels (ie remaining below $200B).

- One exception of course could be at the end of this week, given the typical temporary rise amid month-end dynamics.

BONDS: EGBs-GILTS CASH CLOSE: Yields Continue To Back Up

European yields backed up Wednesday, continuing their rise from Tuesday's lows, with Gilts underperforming Bunds.

- A soft long-end Japanese bond auction overnight set a weaker tone for global core FI early.

- In data, ECB 1-year ahead inflation expectations surprisingly rose but longer-term expectations were steady, muting the impact.

- On the day, the UK curve leaned bear steeper to the 10Y segment, with 30Y outperforming. The German curve more clearly bear steepened.

- BTPs led broader gains in much of the session, with 10Y yields falling to the lowest levels since February. 10-year EGB periphery/semi-core spreads tightened 0.3-1.0bps vs Bunds on the day.

- Thursday's calendar includes an appearance by BOE's Bailey; in data we get Spanish retail sales, and Italian confidence indicators and industrial sales.

- Attention for the week is on Friday's flash May inflation readings from Germany, Italy and Spain.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 0.6bps at 1.797%, 5-Yr is up 1.4bps at 2.107%, 10-Yr is up 2.2bps at 2.554%, and 30-Yr is up 2.9bps at 3.031%.

- UK: The 2-Yr yield is up 5.5bps at 4.075%, 5-Yr is up 5.4bps at 4.206%, 10-Yr is up 6.1bps at 4.727%, and 30-Yr is up 4.5bps at 5.48%.

- Italian BTP spread down 0.4bps at 98.1bps / French OAT down 0.5bps at 67.3bps

FOREX: USD Index Extends Bounce from Weekly Lows to 1.2%

- The greenback continues to trade with a more constructive manner on Wednesday, as a stable equity backdrop provides a more supportive tone for the USD index. This has allowed the DXY to extend the bounce off the week’s lows to 1.2%, narrowing the gap to both the 100.00 handle and initial resistance at the 20-day EMA.

- Headlines and newsflow have been few and far between for markets, with a semblance of stability for the Japanese yield curve also helping contain markets, as well as reduced headlines on the flow of trade deals with the US.

- USDJPY has once again outperformed, rising 0.45% on the session and threatening to close back above the 145.00 handle for the first time since May 16. Despite this week’s strong bounce, a technical downtrend in USDJPY remains intact and short-term gains are considered corrective. On the upside, initial firm resistance to watch is 145.68, the 50-day EMA.

- In similar vein, EURUSD has slipped back below the 1.13 handle as price looks to snap the uptrendline drawn off the early May low. 1.1284, the 38.2% retracement for the upleg off 1.1065, has been tested and clearance below would open the 50-dma which had successfully held as support when tested earlier this month.

- NZD is outperforming following the RBNZ rate decision. While the bank cut rates - as expected - by 25bps to 3.25%, the board suggested that the base rate is near the 'neutral' zone, which may limit the space for further rate cuts ahead.

- Latin American currencies have been notable laggards on the session, as markets react to the firmer dollar and weigh risks related to fiscal and monetary policy trajectories across the region. Both the Mexican peso and the Brazilian real have fallen 0.75%, with the former taking a hit leading into Banxico’s quarterly report, which downgraded both 2025 and 2026 growth forecasts for the Mexican economy.

- The second reading of US Q1 GDP/PCE will take focus on Thursday, before markets turn their attention to Friday’s release of April Core PCE. Central bank rate decisions for the BOK and SARB are also scheduled.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 29/05/2025 | 0130/1130 | * | Private New Capex and Expected Expenditure | |

| 29/05/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 29/05/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 29/05/2025 | 0900/1000 | BOE's Breeden opening remarks at conference on non-bank financial sector and financial stability | ||

| 29/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 29/05/2025 | 1230/0830 | * | Current account | |

| 29/05/2025 | 1230/0830 | * | Payroll employment | |

| 29/05/2025 | 1230/0830 | *** | GDP | |

| 29/05/2025 | 1230/0830 | Richmond Fed's Tom Barkin | ||

| 29/05/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 29/05/2025 | 1445/1545 | BOE's Saporta panellist on hedge funds' role in recent crises | ||

| 29/05/2025 | 1500/1100 | ** | DOE Weekly Crude Oil Stocks | |

| 29/05/2025 | 1500/1600 | BOE's Bailey speech and fireside chat at Irish IAIM Dinner | ||

| 29/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 29/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 29/05/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 29/05/2025 | 1800/1400 | Fed Governor Adriana Kugler | ||

| 29/05/2025 | 2000/1600 | San Francisco Fed's Mary Daly | ||

| 30/05/2025 | 2330/0830 | ** | Tokyo CPI | |

| 30/05/2025 | 2330/0830 | * | Labor Force Survey | |

| 30/05/2025 | 2350/0850 | ** | Industrial Production | |

| 30/05/2025 | 2350/0850 | * | Retail Sales (p) | |

| 29/05/2025 | 0025/2025 | Dallas Fed's Lorie Logan | ||

| 30/05/2025 | 0130/1130 | * | Building Approvals | |

| 30/05/2025 | 0130/1130 | ** | Retail Trade |