US DATA: May Dallas Fed Services Activity Shows Stabilization, Weak Retail Sales

May-28 15:23

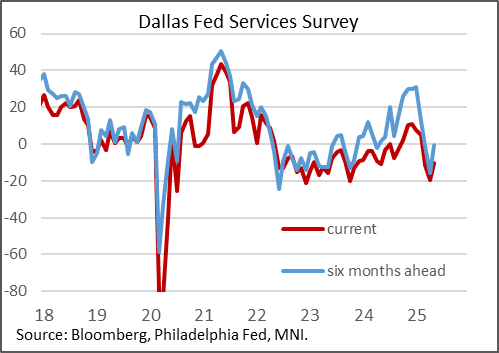

May's Texas Service Sector Outlook Survey conducted by the Dallas Fed implied a contraction in activity in the region, albeit at a less negative pace than earlier in the year. Retail sales were a surprisingly negative category amid the overall stabilization.

- The general business activity index rose to -10.1 (from -19.4 prior), while the 6-month outlook up to -0.3 from -16.0. Both were the strongest readings since February, though that contrasts with positive readings in late 2024.

- There's evidence that tariff-related developments (most notably the May 12 announcement that the US and China would hold off on punitive levies for the time being - the survey was conducted May 13-21) saw a sharp drop in the outlook uncertainty index, to 18.7 from 40.5. Various other subcategories readings were little changed, including employment.

- However, there were signs of weakness in other key categories. The revenue index, "a key measure of state service sector conditions" per the Dallas Fed report, fell 9 points to -4.7, "suggesting revenue contracted slightly" (albeit future revenue/employment/capex expectations were positive).

- And the retail sales reading (which is a subsection of the overall service sector survey) showed a sharp contraction in activity, dropping 33 points to -30.5, weakest since April 2020, with much more mixed forward expectations than seen in the broader survey.

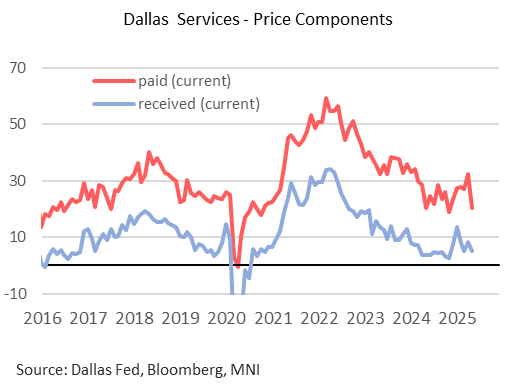

- Inflationary pressures appeared to abate sharply. Current prices paid pulled back toa 6-month low 20.5 (32.5 prior), with received reversing April's rise to dip to 5.2 (8.4 prior).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Early Equities Roundup: Chip Makers, Autos & E-Commerce Weaker

Apr-28 15:21

- Stocks trade mixed midmorning Monday, the Dow outperforming near steady to weaker SPX eminis and Nasdaq indexes. Currently, the DJIA trades up 81.35 points (0.2%) at 40194.74, S&P E-Minis down 15.5 points (-0.28%) at 5533.5, Nasdaq down 127.9 points (-0.7%) at 17256.44.

- Information Technology and Consumer Discretionary sectors underperformed as they pared last week's gains:

- Semiconductor makers weighed on the IT sector: NVIDIA -2.41%, Micron Technology -1.29%, Cadence Design Systems -1.03%, Applied Materials -0.92% and Advanced Micro Devices -0.73%. E-commerce and autos weighed on the Discretionary sector with eBay -0.88%, Best Buy -0.83%, Tractor Supply -0.80%, Tesla -0.64% and Amazon.com -0.50%.

- On the positive side, Financials and Health Care sectors led gainers in the first half, insurance and financial services firms bounced back from Friday's selling: Apollo Global Management +2.47%, Aon +1.88%, Synchrony Financial +1.65%, Blackstone +1.61% and Progressive Corp +1.59%. Pharmaceuticals buoyed the Health Care sector: Mettler-Toledo Int +2.27%, Charles River Labs +2.14%, AbbVie +1.97%, Revvity +1.90% and Bristol-Myers Squibb +1.73%.

- Expected earnings announcements after today's close: Alexandria Real Estate, Cadence Design, SBA Comm, Crown Holdings, Welltower, Solaris Energy, Noble Corp, Brown & Brown, Nucor Corp, Teradyne Inc, Universal Health Services, EZCORP and Waste Management Inc.

FED: US TSY 26W AUCTION: NON-COMP BIDS $1.495 BLN FROM $68.000 BLN TOTAL

Apr-28 15:15

- US TSY 26W AUCTION: NON-COMP BIDS $1.495 BLN FROM $68.000 BLN TOTAL

FED: US TSY 13W AUCTION: NON-COMP BIDS $2.309 BLN FROM $76.000 BLN TOTAL

Apr-28 15:15

- US TSY 13W AUCTION: NON-COMP BIDS $2.309 BLN FROM $76.000 BLN TOTAL